EXERCISE 5-10

EXERCISE 5-11

(a) $1,420 ($1,500 – $80) (g) $7,700 ($290 + $7,410)

EXERCISE 5-12

(a) Earnings have high quality if they provide a full and transparent depiction

of how a company performed.

EXERCISE 5-12 (Continued)

(c) In order to identify potential aggressive accounting techniques one

should examine the factors that are causing net income to differ from net

*EXERCISE 5-13

(a) (1) April 5 Purchases …………………………………… 27,000

Accounts Payable ……………….. 27,000

(b) May 4 Accounts Payable

($27,000 – $3,600) ……………………… 23,400

Cash …………………………………… 23,400

SOLUTIONS TO PROBLEMS

PROBLEM 5-1A

(a)

General Journal

Date Account Titles Debit Credit

May 1 Inventory …………………………………………………

Accounts Payable …………………………….

8,000

8,000

5 Accounts Payable……………………………………

Inventory ………………………………………….

200

200

PROBLEM 5-1A (Continued)

General Journal

Date Account Titles Debit Credit

May 19 Inventory ………………………………………………….

Cash …………………………………………………

250

250

24 Cash ………………………………………………………..

5,500

29 Sales Returns and Allowances………………….

Cash …………………………………………………

124

124

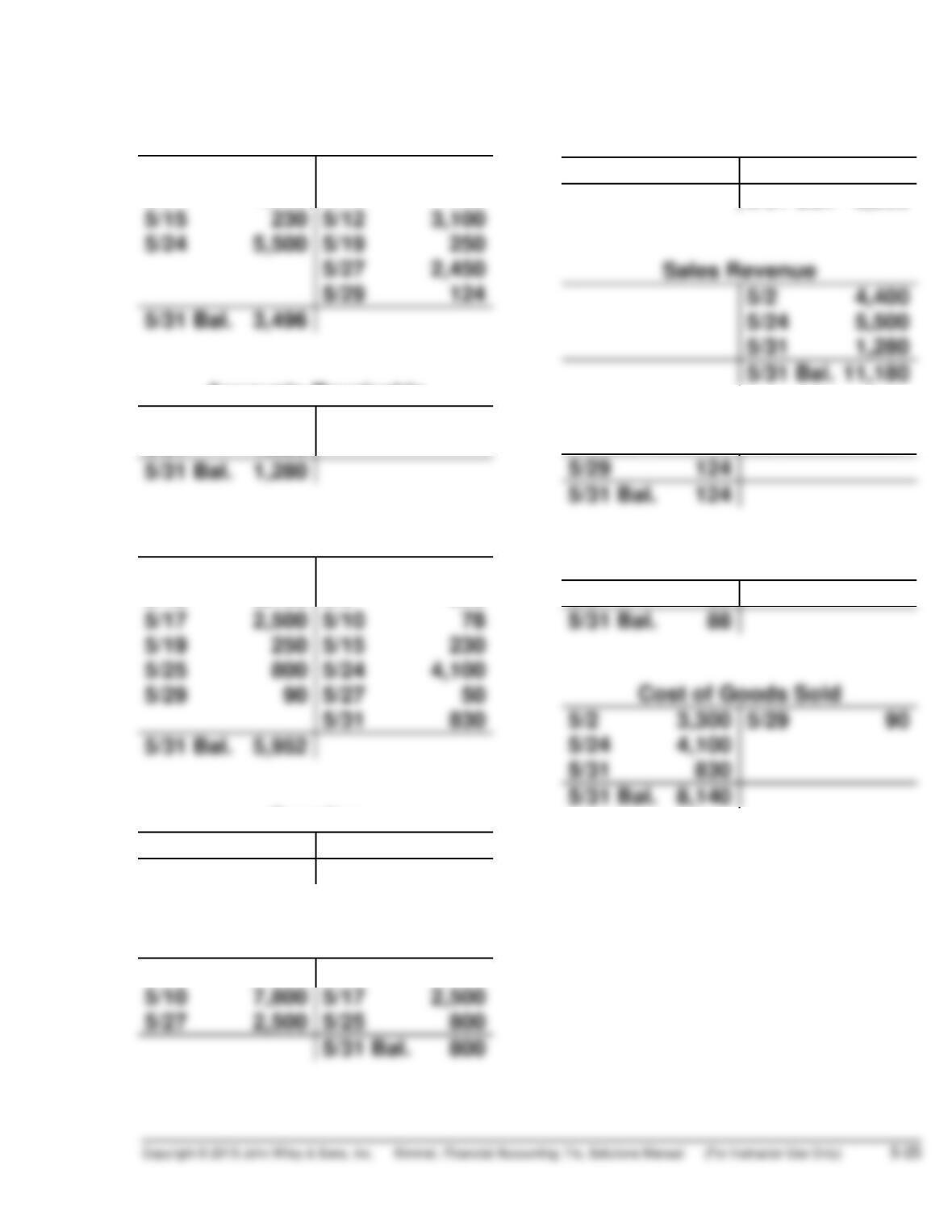

PROBLEM 5-1A (Continued)

(b)

Cash

5/1 Bal. 8,000

5/9 4,312

5/10 7,722

5/11 900

Accounts Receivable

5/2 4,400

5/31 1,280

5/9 4,400

Inventory

5/1 8,000

5/12 3,100

5/2 3,300

5/5 200

Supplies

5/11 900

5/31 Bal. 900

Accounts Payable

5/5 200

5/1 8,000

Common Stock

5/1 Bal. 8,000

5/31 Bal. 8,000

Sales Returns and Allowances

Sales Discounts

5/9 88

PROBLEM 5-1A (Continued)

(c) WATERS HARDWARE STORE

Income Statement (Partial)

For the Month Ended May 31, 2014

Sales

Sales revenue …………………………………………….. $11,180

PROBLEM 5-2A

June 1 Inventory ……………………………………………………… 1,040

Accounts Payable …………………………………. 1,040

9 Accounts Payable ($1,040 – $40) …………………… 1,000

Cash …………………………………………………….. 980

Inventory ($1,000 X .02) …………………………. 20

15 Cash ……………………………………………………………. 1,200

PROBLEM 5-2A (Continued)

June 26 Accounts Payable…………………………………………. 720

Cash ……………………………………………………… 713

Inventory (720 X .01) ………………………………. 7

PROBLEM 5-3A

(a)

General Journal

Date Account Titles Debit Credit

Apr. 5 Inventory ………………………………………………..

.

Accounts Payable …………………………….

.

1,500

1,500

.

.

12 Inventory ………………………………………………..

.

Accounts Payable …………………………….

.

830

830

14 Accounts Payable ($1,500

–

$200) ……………

.

Cash …………………………………………………..

Inventory ($1,300 X 3%) ……………………..

.

1,300

1,261

39

–

.

PROBLEM 5-3A (Continued)

Date Account Titles Debit Credit

Apr. 27 Sales Returns and Allowances………………..

.

Accounts Receivable ……………………….

.

80

80

.

(b)

Cash

4/1 Bal. 2,500

4/7 80

Inventory

4/1 Bal. 3,500

4/5 1,500

4/9 200

4/10 820

Common Stock

4/1 Bal. 6,000

Sales Revenue

4/10 1,340

Sales Returns and Allowances

4/27 80

4/30 Bal. 80

PROBLEM 5-3A (Continued)

(c) FLINT HILLS PRO SHOP

Trial Balance

April 30, 2014

Debit Credit

Cash ……………………………………………………………….

$1,587

(d) FLINT HILLS PRO SHOP

Income Statement (Partial)

For the Month Ended April 30, 2014

Sales

Sales revenue ……………………………………………………………. $2,150

PROBLEM 5-4A

(a) LAMBERT DEPARTMENT STORE

Income Statement

For the Year Ended November 30, 2014

Sales

Sales revenue ……………………………. $904,000

Less: Sales returns and

Income from operations …………………….. 45,900

Other revenues and gains

Gain on disposal of plant assets … 2,000

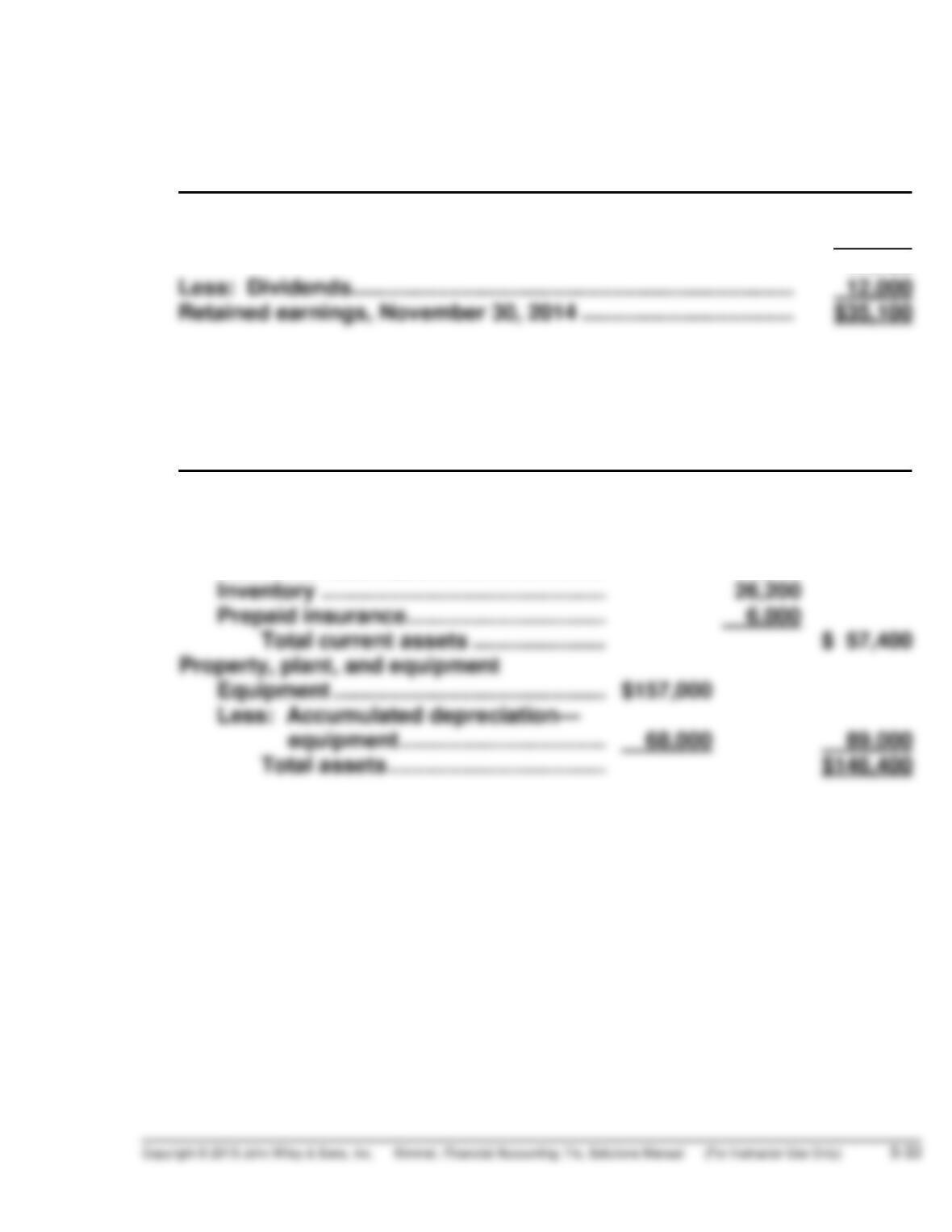

PROBLEM 5-4A (Continued)

LAMBERT DEPARTMENT STORE

Retained Earnings Statement

For the Year Ended November 30, 2014

Retained earnings, December 1, 2013 ……………………………….. $14,200

Add: Net income ……………………………………………………………. 32,900

47,100

LAMBERT DEPARTMENT STORE

Balance Sheet

November 30, 2014

Assets

Current assets

Cash ………………………………………………. $ 8,000

Accounts receivable ……………………….. 17,200

PROBLEM 5-4A (Continued)

LAMBERT DEPARTMENT STORE

Balance Sheet (Continued)

November 30, 2014

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ………………………………………. $26,800

Salaries and wages payable ……………………….. 6,000

Total current liabilities …………………………. $ 32,800

Long-term liabilities

(b) Profit margin: $32,900 ÷ $884,000 = 3.7%

(c) Revised net income = Current net income + increase in gross profit –

Revised net sales = Current net sales + .15 (current net sales)

Revised gross profit = Current gross profit + $40,443

PROBLEM 5-4A (Continued)

This plan increased net sales and gross profit but did not change the

gross profit rate. This is not surprising since the proposed change

affects selling expenses rather than cost of goods sold. An increase in

PROBLEM 5-5A

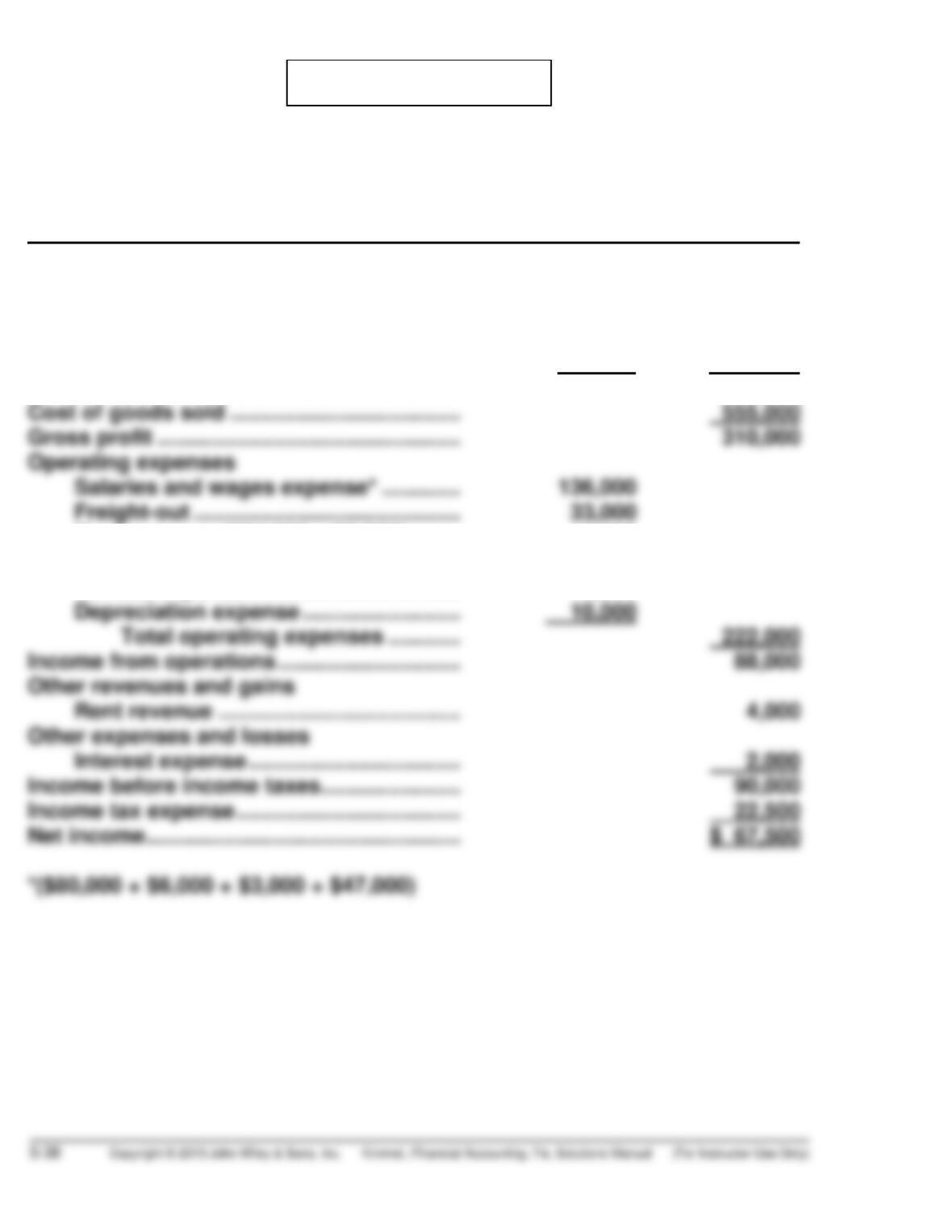

SUNDBERG COMPANY

Income Statement

For the Year Ended December 31, 2014

Sales

Sales revenue ………………………………… $911,000

Less: Sales returns and

allowances ………………………….. $28,000

Sales discounts……………………. 18,000 46,000

Net sales ……………………………………….. 865,000

Rent expense ($24,000 – $6,000) ……… 18,000

Advertising expense ………………………. 13,000

Utilities expense …………………………….. 12,000

PROBLEM 5-6A

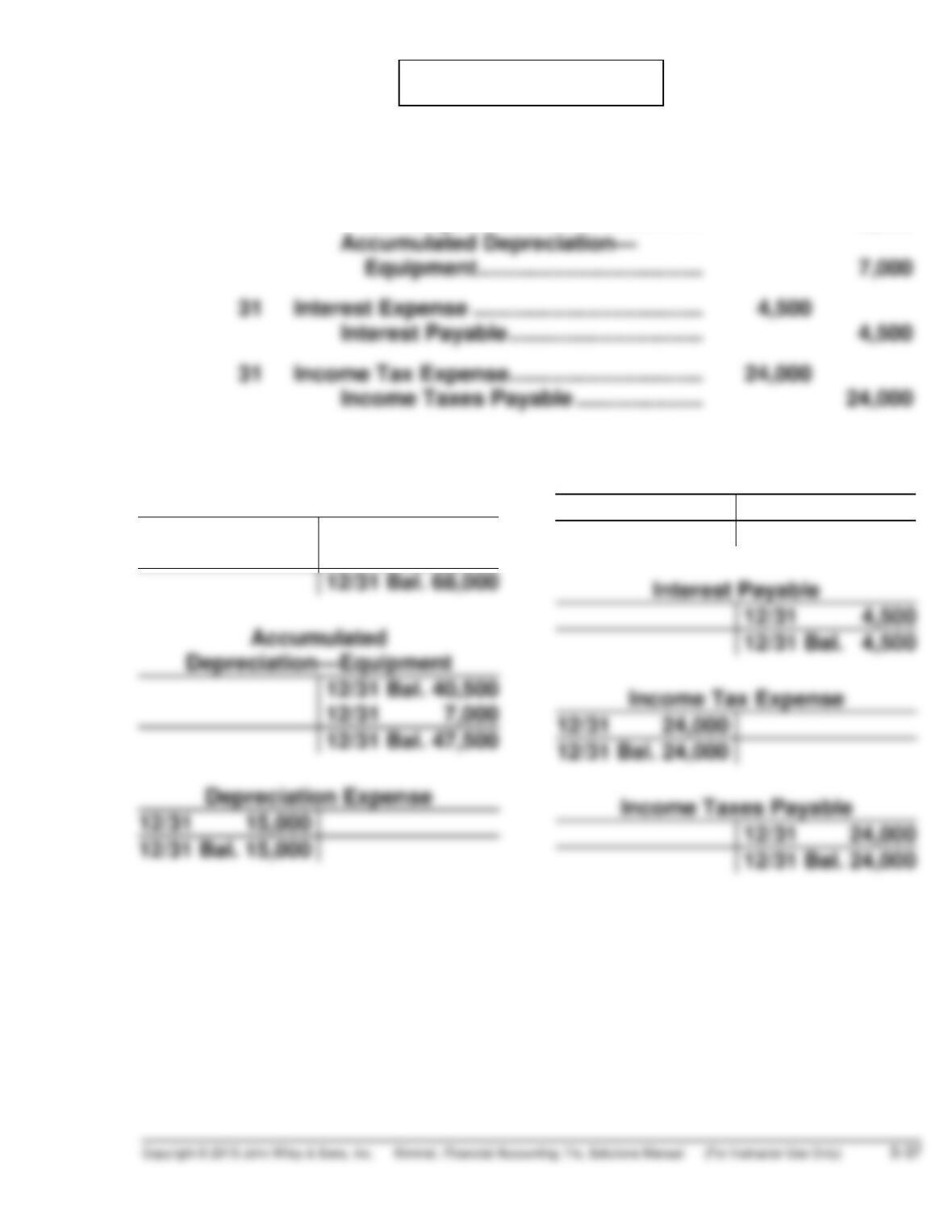

(a) Dec. 31 Depreciation Expense ………………………… 15,000

Accumulated Depreciation—

Buildings ………………………………… 8,000

(b)

Accumulated

Depreciation—Buildings

12/31 Bal. 60,000

12/31 8,000

Interest Expense

12/31 4,500

12/31 Bal. 4,500

PROBLEM 5-6A (Continued)

(c) CUSTOMER CHOICE WHOLESALE COMPANY

Adjusted Trial Balance

December 31, 2014

Debit Credit

Cash …………………………………………………….

.

Accounts Receivable ……………………………

.

.

Accumulated Depreciation—

Equipment ………………………………………..

.

Notes Payable ………………………………………

.

Accounts Payable ………………………………..

.

Interest Payable ……………………………………

.

.

.

Sales Discounts ……………………………………

.

Cost of Goods Sold ………………………………

.

Salaries and Wages Expense ………………..

.

.

$ 31,400

37,600

6,000

709,900

51,300

47,500

54,700

17,500

4,500

PROBLEM 5-6A (Continued)

(d) CUSTOMER CHOICE WHOLESALE COMPANY

Income Statement

For the Year Ended December 31, 2014

Sales

Sales revenue ………………………………………. $922,100

Less: Sales discounts …………………………. 6,000

Net sales …………………………………………………….. 916,100

Depreciation expense …………………………… 15,000

Utilities expense …………………………………… 11,400

Maintenance and repairs expense …………. 8,900

Advertising expense …………………………….. 5,200

Income tax expense …………………………………….. 24,000

Net income …………………………………………………. $ 81,100

CUSTOMER CHOICE WHOLESALE COMPANY

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, January 1 ………………………………………… $ 67,200

PROBLEM 5-6A (Continued)

CUSTOMER CHOICE WHOLESALE COMPANY

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ………………………………………… $ 31,400

Accounts receivable …………………. 37,600

Property, plant, and equipment

Land ………………………………………… 92,000

Buildings …………………………………. $200,000

Liabilities and Stockholders’ Equity

Current liabilities

Notes payable …………………………………………… $ 15,000

Long-term liabilities

Notes payable ($54,700 – $15,000) ……………… 39,700

Total liabilities …………………………………….. 100,700