Results for the Years Ending December 31

Selected Income Statement Growth Rates:

Sales growth rate 54.69 % 37.13 %

Gross profit growth rate 60.99 % 30.66 %

Accounts Receivable Analysis

Sales growth rate 54.69 % 37.13 %

NOTES: “N/M” indicates a calculated rate is not meaningful for analysis

2013 vs. 2012

2012 vs. 2011

Facebook, Inc. (FB / NASDAQ)

Additional Ratio Analysis

Growth Rate Comparisons Between December 31

Liquidity Ratios:

Current ratio 11.88 times 10.71 times

Quick ratio 11.88 times 10.71 times

Cash flow liquidity 14.25 times 10.68 times

Activity Ratios:

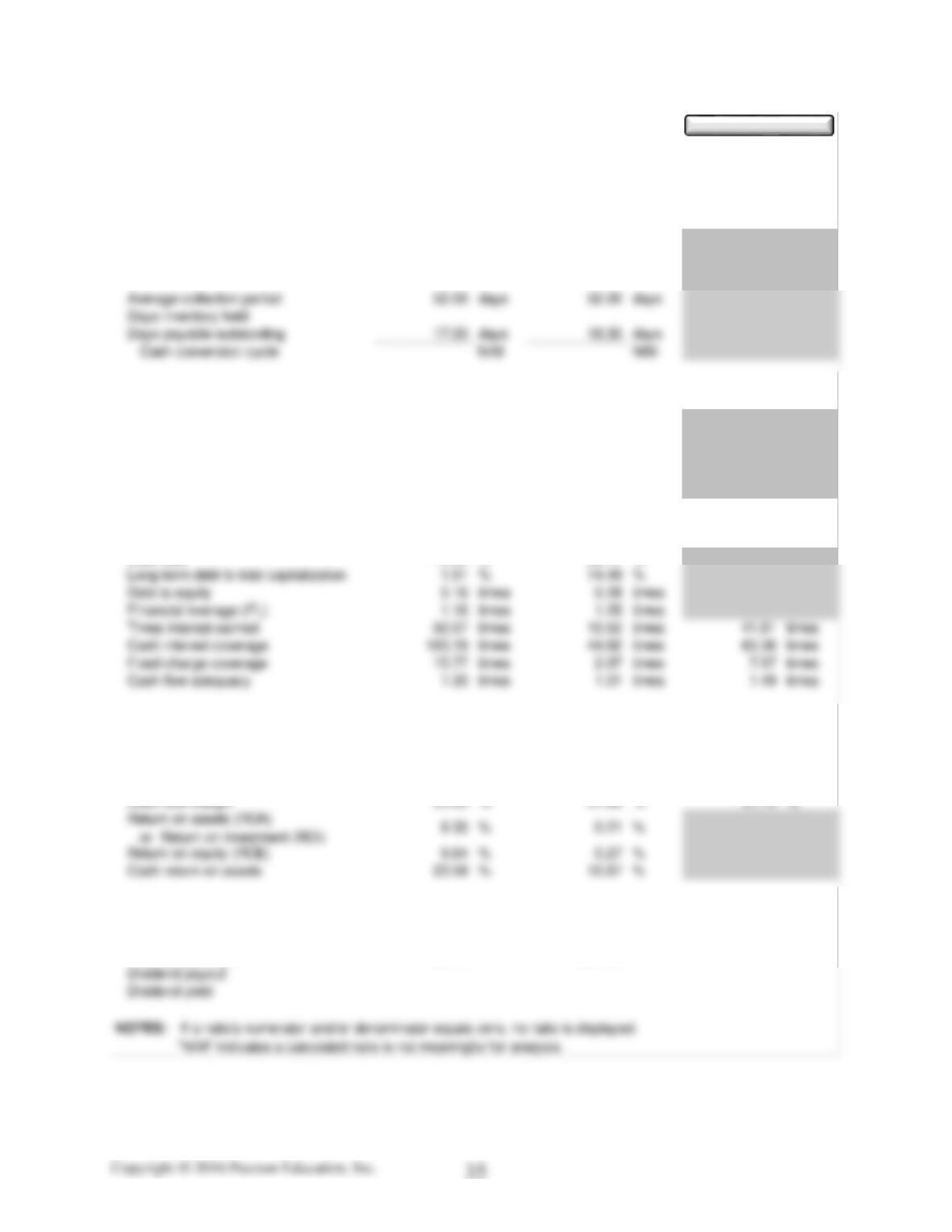

Accounts receivable turnover 7.10 times 7.08 times

Inventory turnover 0.00 0 0.00 0

Payables turnover 21.55 times 20.98 times

Fixed asset turnover 2.73 times 2.13 times

Total asset turnover 0.44 times 0.34 times

Leverage Ratios:

Debt ratio 13.55 % 22.17 %

Profitability Ratios:

Gross profit margin 76.18 % 73.20 % 76.83 %

Operating profit margin 35.62 % 10.57 % 47.32 %

Net profit margin 18.94 % 0.63 % 18.00 %

Market Ratios:

Earnings per share 0.62$ 0.02$ 0.52$

Price-to-earnings 88.15 01331.00 0 0.00 0

Facebook, Inc. (FB / NASDAQ)

Summary of Financial Statement Ratios

Results for the Years Ending December 31

2013

2012

2011

Show Formulas

Short-term liquidity

Facebook’s current, quick and cash flow liquidity ratios are extremely high and

increasing. This can be explained by the structure of the balance sheet. Cash and

short-term investments make up 64% of total assets and current assets make up

73% of total assets. Current liabilities make up a mere 6.1% of total assets. Cash

from operating activities (CFO) is significantly higher than net income every year

and has increased all three years with a significant increase in 2013.

As a service provider, Facebook does not have inventory. The firm pays their

suppliers quickly (in 17 days) and while they allow their customers a longer time

frame (52 days) to pay, the firm has no problem generating cash needed in a timely

manner. The cash conversion cycle of 35 days is good and could be shortened if

necessary by extending the time taken to pay suppliers.

The short-term liquidity for Facebook is excellent.

Operating efficiency

As noted under the “Short–term liquidity” section in the prior section Facebook has

Capital structure and long-term solvency

The capital structure of Facebook is low risk. The debt ratio has decreased from

consisting of total minimum operating lease payments of $978 and commitments in

the amount of $258 million to construct data center sites and maintain network

infrastructure. The total amount of these items is less than the reduction of the

long-term debt that has been eliminated from Facebook’s balance sheet in 2013.

The firm should have no issues paying these items in the future.

commitments and significant CFO.

Profitability

Profitability has been volatile over the three year period. In 2012, despite a 37%

growth in sales, operating expenses grew 191% causing significant declines in both

operating and net profit margins. A better financial picture emerged in 2013 as

sales grew 55% and operating expenses increased only 0.19%.

Gross profit margin decreased from 2011 to 2012, but rebounded in 2013. The

decline in 2012 was due to expansion of data centers, a 65% increase in headcount,

and increased compensation expenses triggered by the completion of the Facebook

IPO in this year. The lack of expenses related to the IPO in 2013 combined with

significant sales price and volume increases resulted in the gross profit margin

returning to a level similar to 2011.

Operating profit as a result of the above-mentioned increases in expenses dropped

from 47% in 2011 to 11% in 2012 before rebounding to 36% in 2013.

Net profit margin has followed the same pattern as operating profit margin.

Cash flow margin and cash return on assets have both increased due to the

increasing CFO which was previously discussed. The return on assets and return

on equity ratios have also improved as the result of the large increases in sales

combined with power expenses relative to sales in 2013.

Market Measures

Because Facebook did not go public until 2012, it is hard to assess the PE ratio

which was extremely high at 1331 at the end of 2012. The PE ratio has dropped

back to a level of 88 at the end of 2013 which is still high, but much lower than

(b)

Reasons to invest

Reasons not to invest

Short-term liquidity is excellent

Unsustainable sales growth

Minimal debt

Volatile profitability

Increasing sales

Increasing CFO

Increasing fixed and total asset turnover

Riskiness of technology

industry

Declining PE ratio

Case 5.4 (a)

Liquidity Ratios:

Current ratio 1.40 times 1.33 times

Quick ratio 0.84 times 0.87 times

Activity Ratios:

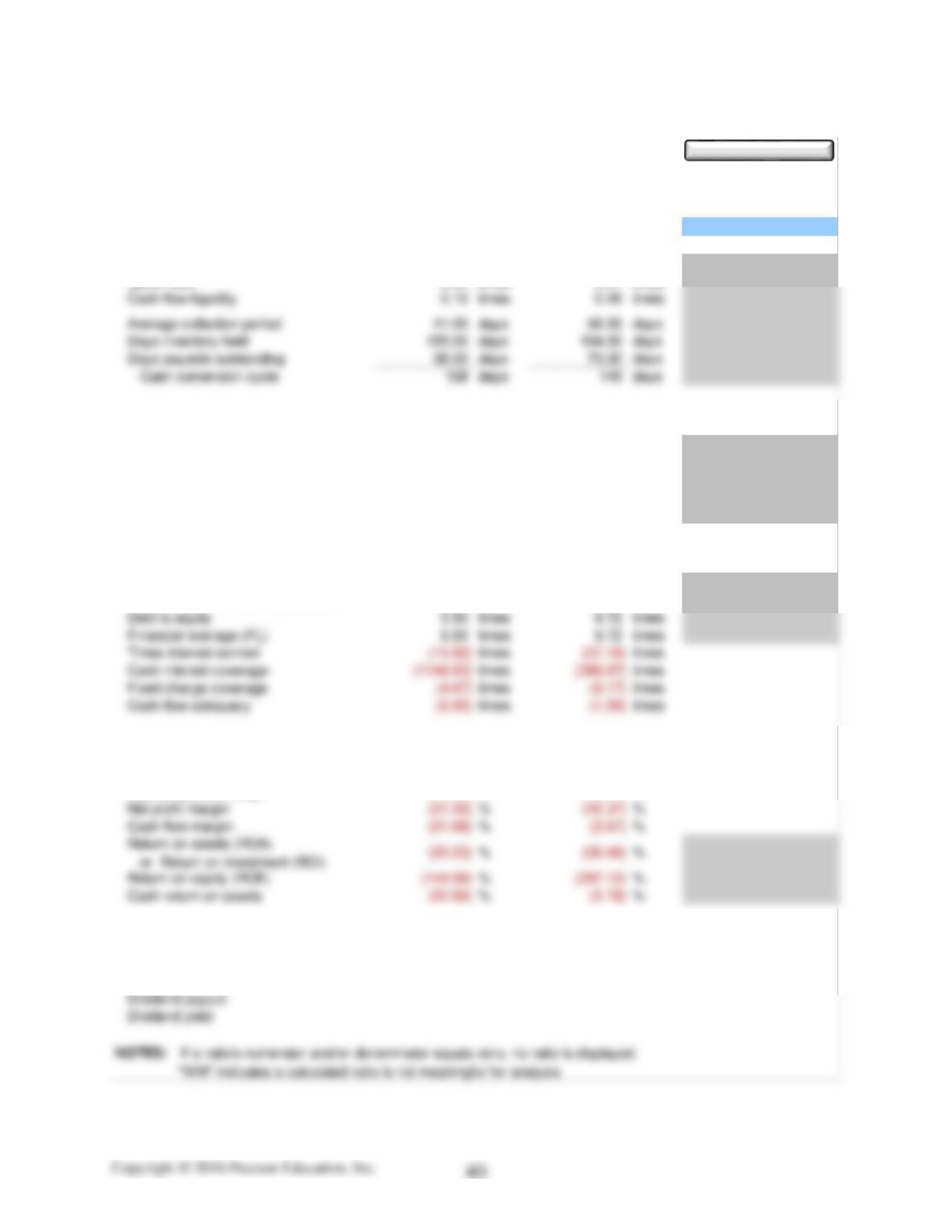

Accounts receivable turnover 8.98 times 6.31 times

Inventory turnover 2.37 times 2.23 times

Payables turnover 9.74 times 5.00 times

Fixed asset turnover 25.19 times 22.66 times

Total asset turnover 1.06 times 0.76 times

Leverage Ratios:

Debt ratio 84.62 % 89.72 %

Long-term debt to total capitalization 26.84 % 23.02 %

Profitability Ratios:

Gross profit margin 28.44 % 16.56 % 0.00 0

Operating profit margin (15.99) %(38.57) %0.00 0

Market Ratios:

Earnings per share (1.04)$ (1.74)$ –$

Price-to-earnings 0.00 N/M 0.00 N/M 0.00 0

Hydrogenics Corporation (HYGS / NASDAQ)

Summary of Financial Statement Ratios

Results for the Years Ending

Dec 31, 2013

Dec 31, 2012

Jan 0, 1900

Show Formulas

(b) As requested, an evaluation of Hydrogenics has been completed. The

following report includes an evaluation of short-term liquidity, capital structure

Short-term Liquidity

Hydrogenics current ratio is above one and has increased slightly as a result of

current assets decreasing at a slower rate than the decrease in current liabilities.

The quick ratio, on the other hand, has decreased because inventories make up a

larger percentage of current assets. The current and quick ratios are acceptable

amounts, but the cash flow liquidity ratio is below one and decreasing

significantly. This is due to the negative cash flow from operating activities which

As sales have increased, accounts receivable has decreased. This is not an expected

pattern, but is a positive situation for Hydrogenics as they have reduced accounts

receivable through collection, rather than through write-offs of bad debts, as

evidenced by the valuation schedule in Note 27. The collection period has dropped

from 58 to 41 days which is a good improvement in this ratio. The allowance for

doubtful accounts has increased even though accounts receivable has decreased;

again, not an expected pattern. There is no indication that bad debt will increase in

2014, although Hydrogenics may be aware of high risk accounts that are not

up a significant portion of accounts receivable and revenues. Hydrogenics two

largest customers accounted for 34% of revenue and 42.6% of accounts receivable

at the end of 2013. Assessing the financial well being of these two customers is

warranted.

The cash conversion cycle increased 9 days. The improvements in average

collection period and inventory days held reduced the cash conversion cycle by a

total of 26 days, but Hydrogenics paid accounts payable 35 days faster in 2013,

compared to 2012, resulting in the overall increase.

Operating Efficiency

As discussed under short-term liquidity, Hydrogenics accounts receivable and

inventory turnovers have improved and the firm is paying suppliers quicker.

Total asset turnover has also improved due to the increased revenues and a decline

in total assets. The small turnover is a result of the large amount of cash and

goodwill that is included in total assets.

Capital Structure and Long-term Solvency

retained earnings (deficit) resulting in total stockholders’ equity increasing by 5%.

Hydrogenics addresses their sources of liquidity and their liquidity risks in

Note 27. Because the firm has sustained losses and generated negative cash flows

from operations since inception, it relies on external sources of funding through

common stock issuance and long-term debt. The majority of total liabilities is

current which means the firm will need to have enough cash to pay these bills

within one year; however, the long-term debt, including both principal and interest,

does not begin to come due for at least three years. This will allow Hydrogenics

some time to improve profitability and cash flow in order to begin paying down

long-term debt commitments.

Profitability

Revenues for Hydrogenics increased 33.81% overall in 2013 while operating

expenses increased 7.84% resulting in a favorable change. Hydrogenics has

operated at a net loss, however, the net loss is decreasing from 2012 to 2013. The

firm operates in two key segments, Onsite Generation and Power Systems.

Gross profit margin has improved from 16.6% in 2012 to 28.4% in 2013 due to

improved margins from the Onsite generation segment and increased revenue from

the Power Systems segment. The gross profit change for Onsite generation only a

1% improvement and is being harmed by the decrease in revenues in this segment.

Hydrogenics is affected by volume changes which indicates that fixed costs are

significant for the firm. As noted in the MDA the gross profit margin has declined

from 22% in 2011 to 15% in 2013. Power Systems gross profit has also increased

due to custom projects which have higher gross margins.

Raw materials and consumables and employee benefits are the largest expense

categories for Hydrogenics. Raw materials and consumables used are stable in

dollar amount and have actually declined in 2013. Employee benefits have

increased 38.6% due to increased salaries and wages and share-based

compensation. The MDA explains that the increase in SG&A is largely attributed

to increased marketing efforts and a higher level of activity in commercial

activities in the Power Systems segment. It appears that the increase in expenses

has resulted in favorable revenue increases.

Market Measures

Due to Hydrogenics’ losses, earnings per share is negative, but improving. The

firm does not pay dividends, nor should they be using scarce resources in this

manner. A positive sign is that the stock price for Hydrogenics has increased

substantially since the end of 2012. Clearly investors see value in the new and

innovative products that the firm has to offer.

Strengths

Innovative products

Ability to attract investors and creditors

Weaknesses

Reliance on two customers

Riskiness and competitiveness of industry

Negative cash flows from operating activities

Lack of profitability

High debt ratio

Investment potential

Hydrogenics is in a high risk industry and has a high risk capital structure. The

Creditworthiness

With a debt ratio currently at 85% it is not recommended that creditors loan more