5-41

PROBLEM 5-54 (50 MINUTES)

1.

Activity Cost Pool

Type of Activity

I:

Machine-related costs

Unit-level

II:

Setup and inspection

Batch-level

III:

Engineering

Product-sustaining-level

IV:

Plant-related costs

Facility-level

2.

Calculation of pool rates:

I:

Machine-related costs:

II.

Setup and inspection:

III.

Engineering:

IV.

Plant-related costs:

5-42

PROBLEM 5-54 (CONTINUED)

3.

Unit costs for odds and ends:

I:

Machine-related costs:

II:

Setup and inspection:

Odds: $9,000 per run ÷ 25 units per run

=

$360 per unit

Ends: $9,000 per run ÷ 125 units per run

=

$72 per unit

III:

Engineering:

Odds:

units 1,000

75% orders change 200 order change per $1,800

units 5,000

25% orders change 200 order change per $1,800

IV.

Plant-related costs:

Odds:

units 1,000

80% ft. sq. 3,840 ft. sq. per $100

Ends:

units 5,000

20% ft. sq. 3,840 ft. sq. per $100

Chapter 05 – Activity-Based Costing and Management

5-43

PROBLEM 5-54 (CONTINUED)

4.

New product cost per unit using the ABC system:

Odds

Ends

Direct material ……………………………………………………….

$ 160.00

$240.00

Direct labor ……………………………………………………….

Manufacturing overhead:

Machine-related …………………………………………………….

Setup and inspection …………………………..

Engineering ……………………………………………………….

Plant-related ……………………………………………………….

307.20

15.36

5.

New target prices:

Odds

Ends

New product cost (ABC) ………………………………………………

$2,017.20

$725.36

6.

Full assignment of overhead costs:

Odds

Ends

Manufacturing overhead costs:

Machine-related …………………………………………………….

$ 800.00

$ 200.00

Setup and inspection …………………………..

Engineering ……………………………………………………….

Plant-related ……………………………………………………….

307.20

Total overhead cost per unit …………………………..

$1,737.20

$ 305.36

Chapter 05 – Activity-Based Costing and Management

5-44

PROBLEM 5-54 (CONTINUED)

7.

Cost distortion:

Odds

Ends

Traditional volume-based costing system:

reported product cost ……………………………………………

$ 664.00

$996.00

Activity-based costing system:

reported product cost ……………………………………………

2,017.20

Amount of cost distortion per unit ……………………………….

)

$270.64

Traditional

system

Traditional

system

Production volume ………………………………………………………

1,000

5,000

Total amount of cost distortion for entire

product line …………………………………………………………..

Chapter 05 – Activity-Based Costing and Management

5-45

PROBLEM 5-55 (45 MINUTES)

1.

a.

GSCC’s predetermined overhead rate, using direct-labor cost as the single cost

driver, is $10 per direct labor dollar, calculated as follows:

Overhead rate

=

cost labor–direct budgeted

cost overhead–ingmanufactur total

=

$12,000,000/$1,200,000

=

b.

The full product costs and selling prices of one pound of Jamaican and one

pound of Colombian coffee are calculated as follows:

Jamaican

Colombian

Direct material ………………………………….

$2.90

$ 3.90

Direct labor ………………………………………

.40

.40

Full product cost ……………………………..

$7.30

$8.30

Markup (30%) …………………………………..

Selling price …………………………………….

$9.49

2.

The new product cost, under an activity-based costing approach, is $11.06 per pound

of Jamaican and $4.62 per pound of Columbian coffee, calculated as follows:

Activity

Cost Driver

Budgeted

Activity

Budgeted

Cost

Unit Cost

Purchasing

Purchase orders

2,316

$2,316,000

$1,000

Material handling

Setups

3,600

2,880,000

800

Quality control

Batches

1,440

400

Roasting

Roasting hours

3,844,000

Blending

Blending hours

1,344,000

Packaging

Packaging hours

1,040,000

Chapter 05 – Activity-Based Costing and Management

5-46

PROBLEM 5-55 (CONTINUED)

Jamaican Coffee

Standard cost per pound:

Direct material ……………………………………………………………………………

$2.90

Direct labor ………………………………………………………………………………..

.40

Total cost …………………………………………………………………………………..

*Budgeted sales ÷ purchase order size

2,000 lbs. ÷ 500 lbs. = 4 orders

Colombian Coffee

Standard cost per pound:

Direct material ……………………………………………………………………………

$3.90

Direct labor ………………………………………………………………………………..

.40

Total cost …………………………………………………………………………………..

$4.62

*Budgeted sales ÷ purchase order size

100,000 lbs. ÷ 50,000 lbs. = 2 orders

Chapter 05 – Activity-Based Costing and Management

5-47

PROBLEM 5-55 (CONTINUED)

3.

a.

The ABC analysis indicates that several activities other than direct labor drive

b.

The implication of the ABC analysis is that the low-volume products are using

Chapter 05 – Activity-Based Costing and Management

5-48

PROBLEM 5-56 (60 MINUTES)

1.

Kara Lindley’s predecessor at Pensacola Air Industries (PAI) would have used a 10

percent material-handling rate, calculated as follows:

Payroll ………………………………………………………………………..

$270,000

Employee benefits……………………………………………………….

54,000

Telephone …………………………………………………………………..

Other utilities ………………………………………………………………

33,000

Materials and supplies …………………………………………………

Depreciation ……………………………………………………………….

Total Material-Handling Department costs …………………….

$432,000

=

2.

a.

The revised material-handling costs to be allocated on a per-purchase-order

basis is $1.00, calculated as follows:

Total Material-Handling Department costs …………………………………..

Deduct: Direct costs:

Direct government payroll ………………………………

Direct phone line ……………………………………………

Material-handling costs applicable to purchase orders ………………..

Material-handling cost per purchase order

b.

Purchase orders might be a more reliable cost driver than is the dollar amount of

Chapter 05 – Activity-Based Costing and Management

5-49

PROBLEM 5-56 (CONTINUED)

3.

There is a $111,900 reduction in material-handling costs allocated to government

contracts by PAI as a result of the new allocation method, calculated as follows:

Previous method:

Government material …………………………………………………..

$ 3,009,000

Total (previous method) ………………………………………………

New method:

Directly traceable material-handling costs

Total (new method) ……………………………………………………..

Net reduction ………………………………………………………………

Chapter 05 – Activity-Based Costing and Management

5-50

PROBLEM 5-56 (CONTINUED)

4.

A forecast of the cumulative dollar impact over a three-year period from 20×4 through

20×6 of Kara Lindley’s recommended change for allocating Material-Handling

Department costs to the Government Contracts Unit is $351,519, calculated as

follows:

20×5

20×6

Calculation of forecasted variable material-handling costs:

Direct-material (DM) cost:

Material-handling rate (10% of DM cost) ……………………….

Deduct: Direct traceable costs ……………………………………..

Variable material-handling costs …………………………..

Calculation of forecasted purchase orders:

Government purchase orders (33% of total) ………………….

Calculation of material-handling costs allocated to government contracts:

Variable material-handling costs …………………………..

Variable material-handling costs per purchase

order (rounded) …………………………………………………….

Projected variable material-handling

costs (rounded) …………………………………………………….

Fixed material-handling costs ………………………………………

Total material-handling costs allocated to

government contracts ……………………………………………

Chapter 05 – Activity-Based Costing and Management

5-51

PROBLEM 5-56 (CONTINUED)

Calculation of cumulative dollar impact:

Government material at 70% ………………………………………..

$ 3,099,600b

$ 3,177,090 c

Material-handling at 10% (previous method) …………………

Deduct: Material-handling costs allocated to

government contracts (new method) ………………………

Net reduction in government contract

b70% $4,428,000 = $3,099,600

d10% $3,099,600 = $309,960

In summary, the cumulative dollar impact of the recommended change in allocating

Material-Handling Department costs is $351,519, calculated as follows:

Total ……………………………………………..

5.

a.

Referring to the standards of ethical conduct for management accountants, Kara

Lindley faces the following ethical issues:

Competence:

5-52

PROBLEM 5-56 (CONTINUED)

• Communicate unfavorable as well as favorable information and professional

judgments and opinions.

Credibility:

b.

The steps Kara Lindley could take to resolve this ethical conflict are as follows:

• Lindley should first follow the established policies at PAI.

• If this approach does not resolve the conflict or if such policies do not exist,

she should discuss the problem with her immediate superior, except when it

Chapter 05 – Activity-Based Costing and Management

5-53

PROBLEM 5-57 (45 MINUTES)

1.

An activity-based costing system is a two-stage process of assigning costs to

products. In stage one, activity-cost pools are established. In stage two a cost driver is

2.

Queensland Electronics should not continue with its plans to emphasize the Zodiac

model and phase out the Novelle model. As shown in the following activity-based

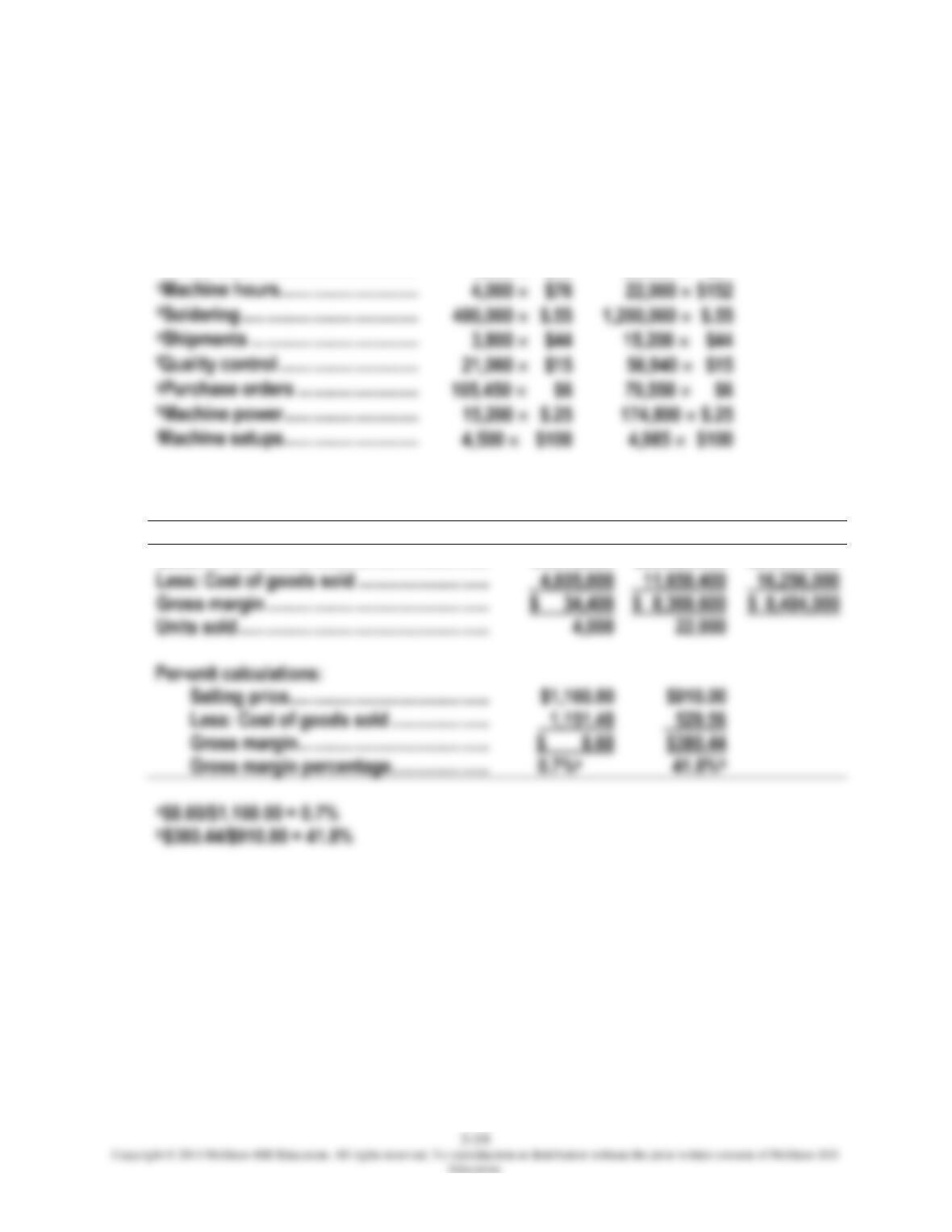

costing analysis, the Zodiac model has a gross margin of less than 1 percent, while

the Novelle model generates a gross margin of nearly 42 percent.

Cost per event for each cost driver:

Soldering ………………..

$ 880,000

1,600,000

=

$ .55 per solder joint

Shipments ………………

836,000

19,000

=

44.00 per shipment

Quality control ………..

78,000

=

15.00 per inspection

Purchase orders ……..

=

6.00 per order

Machine power ………..

=

.25 per hour

Machine setups ……….

=

100.00 per setup

Costs per model:

Zodiac

Novelle

Direct costs:

Materiala ……………………………………………………….………

$2,316,000

$ 4,642,000

Direct laborb ……………………………………………………….

196,000

462,000

Machine hoursc ……………………………………………………..

Total direct costs ……………………………………………………….

$2,816,000

$ 8,448,000

Assigned costs:

Solderingd …………………………………………………………….

Shipmentse ……………………………………………………………

167,200

668,800

Quality controlf ……………………………………………………..

315,900

854,100

Purchase ordersg …………………………………………………..

632,700

477,300

Machine powerh …………………………………………………….

Machine setupsi …………………………………………………….

Total assigned costs ……………………………………………………

$1,789,600

Chapter 05 – Activity-Based Costing and Management

PROBLEM 5-57 (CONTINUED)

Calculations:

Zodiac

Novelle

aMaterial …………………………………..

4,000 $579

22,000 $211

bDirect labor ……………………………..

4,000 $49

22,000 $21

cMachine hours …………………………

22,000 $152

eShipments ………………………………

gPurchase orders ……………………..

Profitability analysis:

Zodiac

Novelle

Total

Sales ……………………………………………………..

$4,640,000

$20,020,000

$24,660,000

Less: Cost of goods sold ……………………….

Gross margin …………………………………………

$ 8,404,000

Units sold ………………………………………………

Per-unit calculations:

Selling price …………………………………….

Less: Cost of goods sold …………………

Gross margin …………………………………..

Gross margin percentage …………………

5-55

PROBLEM 5-58 (60 MINUTES)

1.

General advantages associated with activity-based costing include the following:

• Provides management with a more thorough understanding of complex product

costs and product profitability for improved resource management and pricing

5-56

PROBLEM 5-58 (CONTINUED)

2.

Using Ultratech’s unit cost data, the total contribution margin expected from the PC

board is $4,720,000, calculated as follows:

Per Unit

Total for

40,000

Units

Revenue ……………………………………………………………………..

$600

$24,000,000

Direct material …………………………………………………………….

$280

$11,200,000

Material-handling charge (10% of material) …………………..

Total cost ……………………………………………………………..

$482

$19,280,000

Unit contribution margin ……………………………………………..

$118

*Variable overhead rate: $2,240,000 ÷ 280,000 hr. = $8 per hr.

The total contribution margin expected from the TV board is $3,900,000, calculated as

follows:

Per Unit

Total for

65,000

Units

Revenue ……………………………………………………………………..

$300

$19,500,000

Direct material …………………………………………………………….

$160

$10,400,000

Material-handling charge (10% of material) …………………..

Total cost ……………………………………………………………..

$240

$15,600,000

Unit contribution margin ……………………………………………..

*Variable-overhead rate: $2,240,000 ÷ 280,000 hr. = $8 per hr.

5-57

PROBLEM 5-58 (CONTINUED)

3.

The pool rates, which apply to both the PC board and the TV board, are calculated as

follows:

Procurement ……………………….

$800,000/4,000,000

=

$.20 per part

Production scheduling ………..

$440,000/110,000

=

$4.00 per board

Packaging and shipping ………

$880,000/110,000

=

$8.00 per board

Machine setup …………………….

$892,000/278,750

=

$3.20 per setup

Hazardous waste disposal …..

=

$6.00 per lb.

Quality control …………………….

$1,120,000/160,000

=

$7.00 per inspection

General supplies …………………

$132,000/110,000

=

$1.20 per board

Machine insertion ………………..

=

$.80 per part

Manual insertion ………………….

=

$8.00 per part

Wave soldering ……………………

$264,000/110,000

=

$2.40 per board

Using activity-based costing, the total contribution margin expected from the PC

board is $3,464,000, calculated as follows:

Per Unit

Total for

40,000

Units

Revenue ………………………………………………………………………

$600.00

$24,000,000

Direct material ……………………………………………………………..

$280.00

$11,200,000

Production scheduling …………………………………………………

Packaging and shipping ……………………………………………….

Quality control

General supplies ………………………………………………………….

Wave soldering …………………………………………………………….

Total cost

Unit contribution margin

5-58

PROBLEM 5-58 (CONTINUED)

Using activity-based costing, the total contribution margin expected from the TV board

is $5,045,300, calculated as follows:

Per Unit

Total for

65,000

Units

Revenue ……………………………………………………………………..

$ 300.00

$19,500,000

Direct material …………………………………………………………….

$ 160.00

$10,400,000

Procurement ($.20 per part 26 parts) …………………………

5.20

338,000

Production scheduling ………………………………………………..

Packaging and shipping ………………………………………………

Hazardous waste disposal ($6 per lb. .03 lb.) ……………..

Quality control ($7.00 per inspection x 1 inspection) ……..

General supplies …………………………………………………………

Manual insertion ($8.00 per part x 1 part) ………………………

Wave soldering ……………………………………………………………

Total cost ……………………………………………………………….

$ 222.38

$14,454,700

Unit contribution margin ……………………………………………..

4.

The analysis using the previously reported costs indicates that the unit contribution of

the PC board is almost double that of the TV board. On this basis, management is

likely to accept the suggestion of the production manager and concentrate

Chapter 05 – Activity-Based Costing and Management

5-59

PROBLEM 5-59 (50 MINUTES)

1.

a.

The calculation of total budgeted costs for the Manufacturing Department at

Scott Manufacturing is as follows:

Direct material:

Tuff Stuff ($15.00 per unit 20,000 units) …………

$300,000

Total direct material …………………………………………….

Direct labor …………………………………………………………

Overhead:

Indirect labor ………………………………………………….

Fringe benefits ……………………………………………….

15,000

Indirect material ……………………………………………..

93,000

Power …………………………………………………………….

Setup ……………………………………………………………..

Quality assurance …………………………………………..

30,000

Other utilities ………………………………………………….

30,000

Depreciation …………………………………………………..

Total overhead ……………………………………………………

Total Manufacturing Department budgeted cost …..

b.

The unit costs of Tuff Stuff and Ruff Stuff, with overhead assigned on the basis

of direct-labor hours, are calculated as follows:

Tuff Stuff:

Direct material ………………………………………………..

$15.00

Overhead ($10.50 per hour 2 hours)* …………….

Tuff Stuff unit cost …………………………………….

$84.00

*Budgeted direct labor hours:

Ruff Stuff (20,000 units 3 hours) ……………………….

Total budgeted direct-labor hours ……………………….

Direct-labor rate: $2,400,000 per 100,000 hours

=

Overhead rate: $1,050,000 per 100,000 hours

=

$10.50 per hour

Chapter 05 – Activity-Based Costing and Management

5-60

PROBLEM 5-59 (CONTINUED)

Ruff Stuff:

Direct material ………………………………………………..

$ 9.00

Ruff Stuff unit cost …………………………………….

$112.50

*Budgeted direct labor hours

Total budgeted direct-labor hours ……………………….

100,000

Direct-labor rate: $2,400,000 per 100,000 hours

=

$24.00 per hour

Overhead rate: $1,050,000 per 100,000 hours

=

$10.50 per hour

2.

The total budgeted cost of the Fabricating and Assembly Departments, after

separation of costs into the activity cost pools, is calculated as follows:

Total

Fabricating

Assembly

Percent

Dollars

Percent

Dollars

Direct material ……….

$ 480,000

100%

$ 480,000

Overhead:

Indirect labor

$ 54,720

Fringe benefits

Indirect material

480,000

Setup

210,000

Quality assurance

Other utilities

Depreciation

Total overhead

$ 695,820