CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Prob. 19–3A (FIN MAN); Prob. 5–3A (MAN)

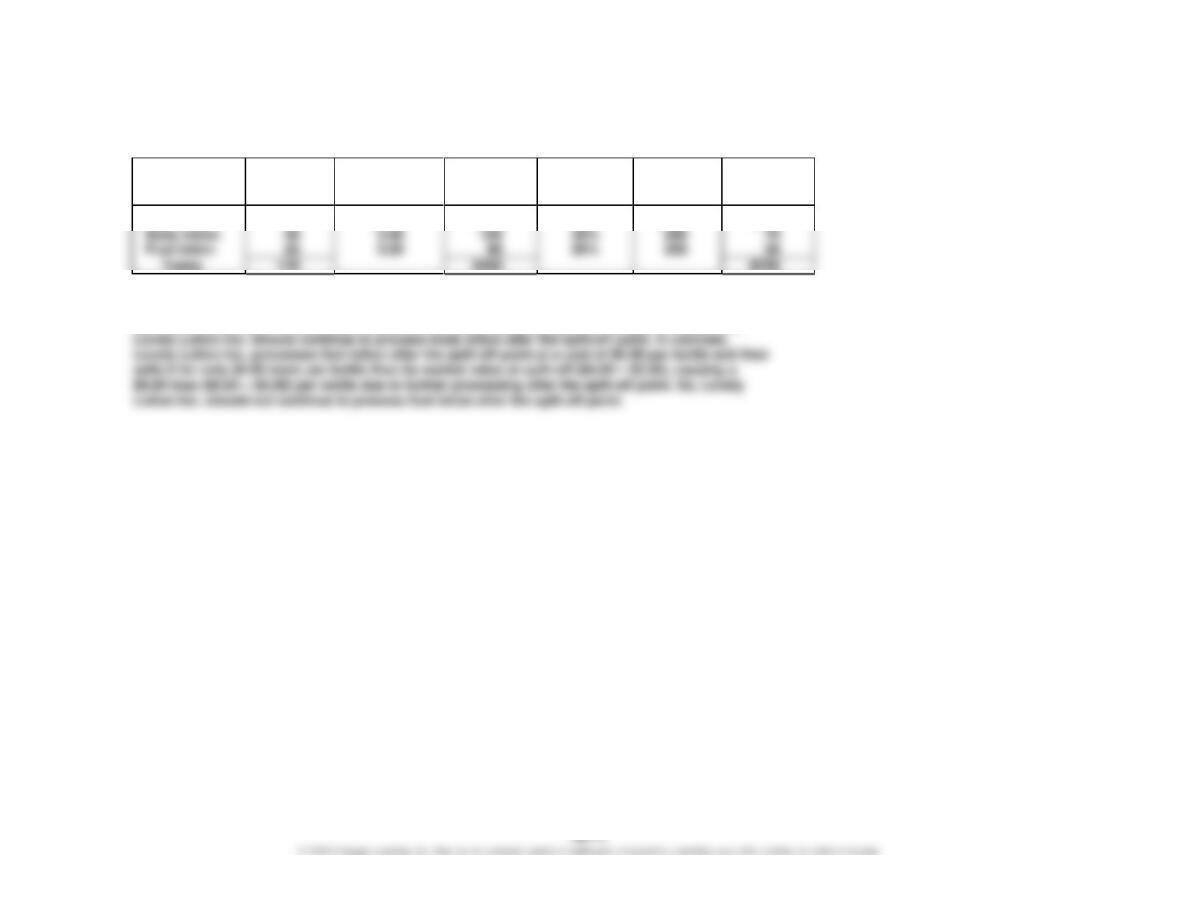

1.

Joint Product

Bottles

per Batch

Market Value

per Bottle at

Split-Off

Total Market

Value at

Split-Off

Percent of

Total MV at

Split-Off

Joint Costs

Allocation

Hand lotion

80

$2.50

$200

50%

$250

$125

Body lotion

Foot lotion

Totals

145

$400

$250

2. Lovely Lotion Inc. processes body lotion after the split-off point at a cost of $0.25 per bottle and

then sells it for $2.75 more per bottle than its market value at split-off ($5.75 – $3.00), providing a

$2.50 extra profit ($2.75 – $0.25) per bottle due to further processing after the split-off point. So,

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Prob. 19–3A (FIN MAN); Prob. 5–3A (MAN) (Concluded)

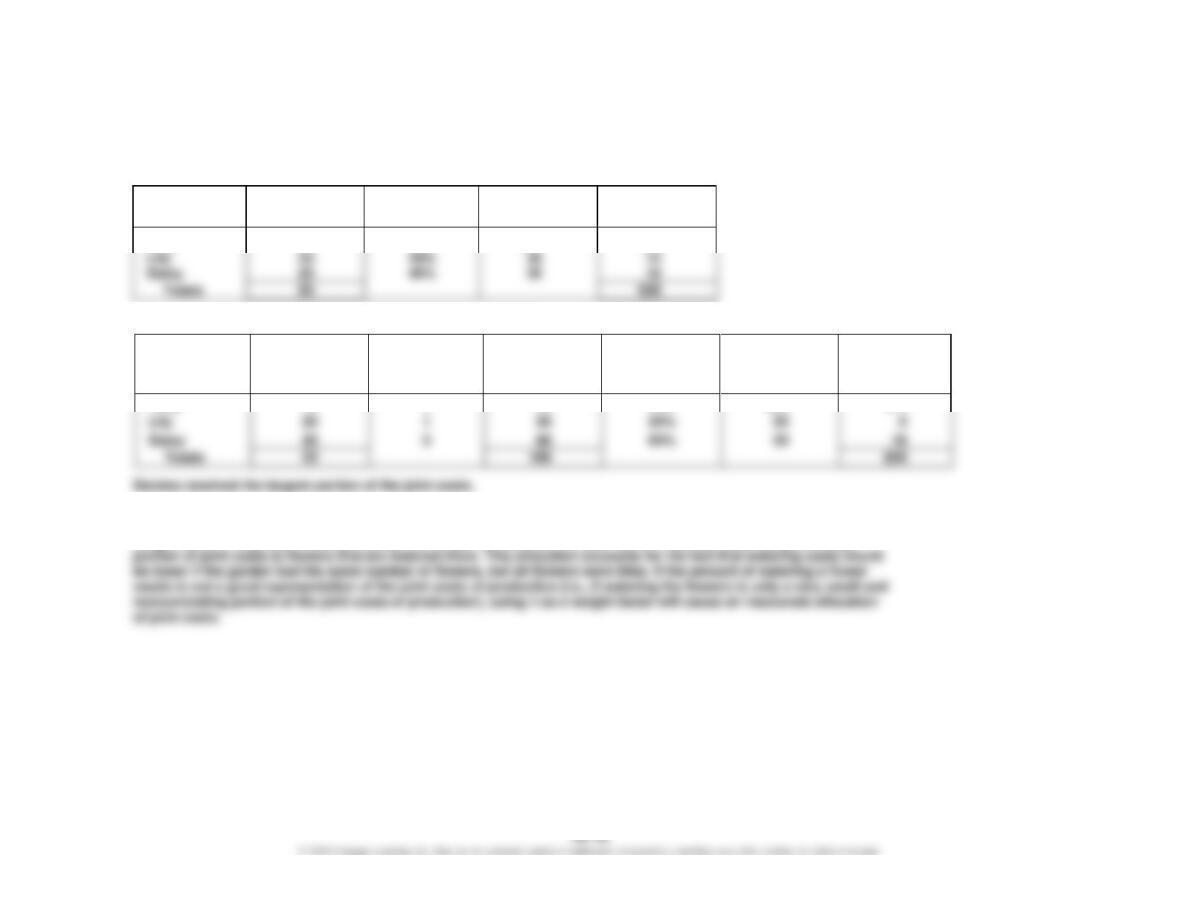

3.

Joint Product

Bottles

per Batch

Market Value

per Bottle

at Split-Off

Total

Market Value

at Split-Off

Market Price

per Bottle

Added Cost

per Bottle

NRV

per Bottle

Total Net

Realizable

Value

Greater of

Total NRV

and Total

Market Value

at Split-Off

Proportion

Joint Costs

Allocation

Hand lotion

$2.50

Body lotion

120.00

5.75

Foot lotion

4.00

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Prob. 19–4A (FIN MAN); Prob. 5–4A (MAN)

1.

Joint Product

Flowers

per Harvest

Proportion

Joint Costs

Allocation

Tulip

10

20%

$30

$ 6

Lilies and daisies received the largest portion of the joint costs.

2.

Joint Product

Flowers per

Harvest

Weight

Factor

Weighted

Flowers

of Water

Weighted

Percent of Water

Joint Costs

Allocation

Tulip

10

2

20

20%

$30

$ 6

Lily

20

1

20

20%

30

3. As we saw from the answers to parts (1) and (2), using the weighted average method substantially changes the

allocation of the joint costs. Given this discrepancy, considering whether the amount of watering is an appropriate

weight factor is important, because using it to weight the allocation of joint costs to each product assigns a larger

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Prob. 19–1B (FIN MAN); Prob. 5–1B (MAN)

1. When using the sequential method, the support departments are often allocated in

2. Personnel Department cost allocation:

Maintenance Department:

10 ÷ (10 + 41 + 49) = 10%

10% × $15,000 = $1,500

Molding Department:

41 ÷ (10 + 41 + 49) = 41%

41% × $15,000 = $6,150

Assembly Department:

49 ÷ (10 + 41 + 49) = 49%

49% × $15,000 = $7,350

168 ÷ (168 + 112) = 60%

60% × $12,900 = $7,740

112 ÷ (168 + 112) = 40%

40% × $12,900 = $5,160

3. The reciprocal services method is the most accurate method of support

department cost allocation. However, Hooligan Adventure Supply may be

discouraged from using this method because of its high level of complexity. In

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Prob. 19–2B (FIN MAN); Prob. 5–2B (MAN)

1. In choosing a cost driver, Kizzle’s management should consider how well the driver

represents the costs of the department. For example, Janitorial costs are often

2. Total cost to be allocated from Maintenance (M):

Total costs of Maintenance include 1 ÷ (1 + 2 + 2) = 20% of Janitorial costs

Thus, M = $4,200 + (0.2 × J)

Now plug the value for J into the M equation:

M = $4,200 + (0.2 × $4,000)

= $4,200 + $800

= $5,000

Maintenance cost allocation:

Janitorial:

16 ÷ (16 + 40 + 24) = 20%

20% × $5,000 = $1,000

50% × $5,000 = $2,500

Cooking:

24 ÷ (16 + 40 + 24) = 30%

30% × $5,000 = $1,500

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Prob. 19–2B (FIN MAN); Prob. 5–2B (MAN) (Concluded)

Janitorial cost allocation:

Maintenance:

1 ÷ (1 + 2 + 2) = 20%

20% × $4,000 = $800

40% × $4,000 = $1,600

Cooking:

2 ÷ (1 + 2 + 2) = 40%

40% × $4,000 = $1,600

3. The reciprocal services method is the most difficult of the three support department

cost allocation methods. However, it is also the most accurate method. As Kizzle’s

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Prob. 19–3B (FIN MAN); Prob. 5–3B (MAN)

1.

Joint Product

Bottles

per Batch

Market Value

per Bottle

at Split-Off

Total

Market

Value at

Split-Off

Market

Price

per Bottle

Added

Cost per

Bottle

NRV

per Bottle

Total Net

Realizable

Value

Greater of

Total NRV

and Market

Value at

Split-Off

Proportion

Joint Costs

Allocation

Morning glory

$30,000

$11,100

Snowflake sparkle

Sea breeze hand

soap

12,500

0.60

18,000

30,000

2. McKenzie’s Soap Sensations, Inc., always processes each variety of hand soap beyond the split-off point, because the net realizable value of each variety of hand

soap after further processing (beyond the split-off point) is higher than the market value of each variety of hand soap at the split-off point.

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Prob. 19–4B (FIN MAN); Prob. 5–4B (MAN)

1.

Joint Product

Roses per Harvest

Proportion

Joint Costs

Allocation

Red roses

80

40%

$110

$ 44.00

White roses

Peach roses

2.

Joint Product

Roses per Harvest

Weight

Factor

Weighted

Roses of

Fertilizer

Weighted

Percent of

Fertilizer

Joint Costs

Allocation

White roses

Peach roses

3. The cost of the type of fertilizer required by each type of rose may be a good weight factor. If fertilizer is a significant cost of

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

MAKE A DECISION

MAD 19–1 (FIN MAN); MAD 5–1 (MAN)

a. Because company bonuses are based on cost allocations, an accurate cost

allocation is important. Thus, the reciprocal services method is advisable.

d. Maintenance costs are likely controllable by the GMs and should be allocated for

performance evaluation purposes. The GMs can’t control the square footage their

plant uses, so the Janitorial costs should likely be ignored when evaluating GM

performance.

MAD 19–2 (FIN MAN); MAD 5–2 (MAN)

a. Management has noted the need for highly accurate support department cost

allocation because cost management performance affects a portion of company

bonuses. In addition, management is not worried about using a highly complex

method. Thus, the reciprocal services method should be used because it is the

most accurate, and its complexity is not expected to pose a significant problem.

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

MAD 19–2 (FIN MAN); MAD 5–2 (MAN) (Concluded)

d. Security Department cost allocation:

Janitorial Department:

$10,000 ÷ ($10,000 + $450,000 + $540,000) = 1%

Production Department 1:

$450,000 ÷ ($10,000 + $450,000 + $540,000) = 45%

Production Department 2:

$540,000 ÷ ($10,000 + $450,000 + $540,000) = 54%

Janitorial Department cost allocation:

Production Department 1:

54,000 ÷ (54,000 + 36,000) = 60%

Production Department 2:

36,000 ÷ (54,000 + 36,000) = 40%

e. Because Janitorial costs increase with the number of vehicles produced (a

f. The market value at split-off and net present value methods may not fairly allocate

joint costs because all joint products are produced and sold at similar margins.

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

MAD 19–3 (FIN MAN); MAD 5–3 (MAN)

Orange Julius Flavor

Market Value

per Cup at

Split-Off

Market

Price per

Cup After

Further

Processing

Added Cost

per Cup

Net Realizable

Value

per Cup

Greater of

NRV and

Market Value

at Split-Off

per Cup

Strawberry orange

a. Yes. Joyous Julius, Inc., should discontinue processing its tropical orange and coconut orange flavors, because they are

worth more at the split-off point than after further processing (see table above).

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

MAD 19–3 (FIN MAN); MAD 5–3 (MAN) (Concluded)

c. Pure orange: 900 + 150 + 130 + 100 = 1,280

Orange Julius Flavor

Cups per

Batch

Market

Value

per Cup at

Split-Off

Total Market

Value at

Split-Off

Market

Price

per Cup

Added Cost

per Cup

Net

Realizable

Value

per Cup

Total Net

Realizable

Value

Greater of

NRV or Market

Value at

Split-Off

Proportion

Joint

Costs

Allocation

Raspberry orange

2,500

Mango orange

2,500

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

MAD 19–4 (FIN MAN); MAD 5–4 (MAN)

a. Management’s highest priority with regard to the cost allocation process is to keep

it simple and cost-effective. In addition, performance evaluations do not depend on

them, and William’s Ball & Jersey Shop is a small company, so the different support

department cost allocation methods are unlikely to yield significant cost allocation

differences. Thus, the direct method should be used, because it is the simplest and

c. William needs to know the market value of the toddler-size jersey at the split-off

point and the market price of the toddler-size jersey after further processing. In

addition, it would be helpful to know the current exact share of the joint production

costs that the toddler-size jersey will incur. Finally, any information about market

demand for the product and whether or not there may be risks of cannabilization

costs (sales of other products decreasing as a result of the new product line) should

also be considered.

e. Support Department 1 cost allocation:

Production Department 1:

22 ÷ (22 + 18) = 55%

Production Department 2:

18 ÷ (22 + 18) = 45%

Production Department 1:

2,280 ÷ (2,280 + 1,720) = 57%

Production Department 2:

1,720 ÷ (2,280 + 1,720) = 43%

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

TAKE IT FURTHER

TIF 19–1 (FIN MAN); TIF 5–1 (MAN)

a. The line manager exhibited motivated reasoning; that is, she ignored evidence

against her preference and overweighted evidence for her preference. She acted

out of her own self-interest rather than considering what the best decision would

be, given all the facts. Even though her motivated reasoning may not have been a

conscious decision, motivated reasoning can lead us to make unethical choices

without our feeling unethical about them.

joint cost allocations to reflect.

TIF 19–2 (FIN MAN); TIF 5–2 (MAN)

Liam: The direct method is simple and easy to use. It is easily implemented and

communicated, so choosing this method will likely result in few cost accounting errors

Rose: The sequential method is a compromise between practicality and accuracy. It is

more difficult to implement and use than the direct method, but it is not as complex as

Miranda: The reciprocal services method is the most accurate method. It accounts for all

inter-support-department services and provides the most precise support department

cost possible. The downside is that it requires a lot of technical expertise and

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

TIF 19–3 (FIN MAN); TIF 5–3 (MAN)

The content of the memo should be similar to the following response:

I disagree with the Mackalite production manager’s argument. Although the two

products come from an inseparable process, Mackalite is more costly to make because

it requires more heat than Jemmerite in the joint production process. In other words, if

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

CERTIFIED MANAGEMENT ACCOUNTANT (CMA®)

EXAMINATION QUESTIONS (ADAPTED)

1. b. Using the direct method of allocation, only the hours of the production departments

2.

a.

Total overhead in the Machining Department would be $407,500, determined

as follows:

Machining overhead

$200,000

Maintenance ($350,000 × 0.5)

Systems [($95,000 + $35,000*) × 0.25**]

$407,500

3. b. The units should be processed after the split-off point only if the additional cost

is less than the additional revenue. Only J-60 units warrant further processing.

B-40

J-60

H-102

Additional revenue

$2.25

$1.70

$2.50