COMPREHENSIVE PROBLEM SOLUTION

(a)

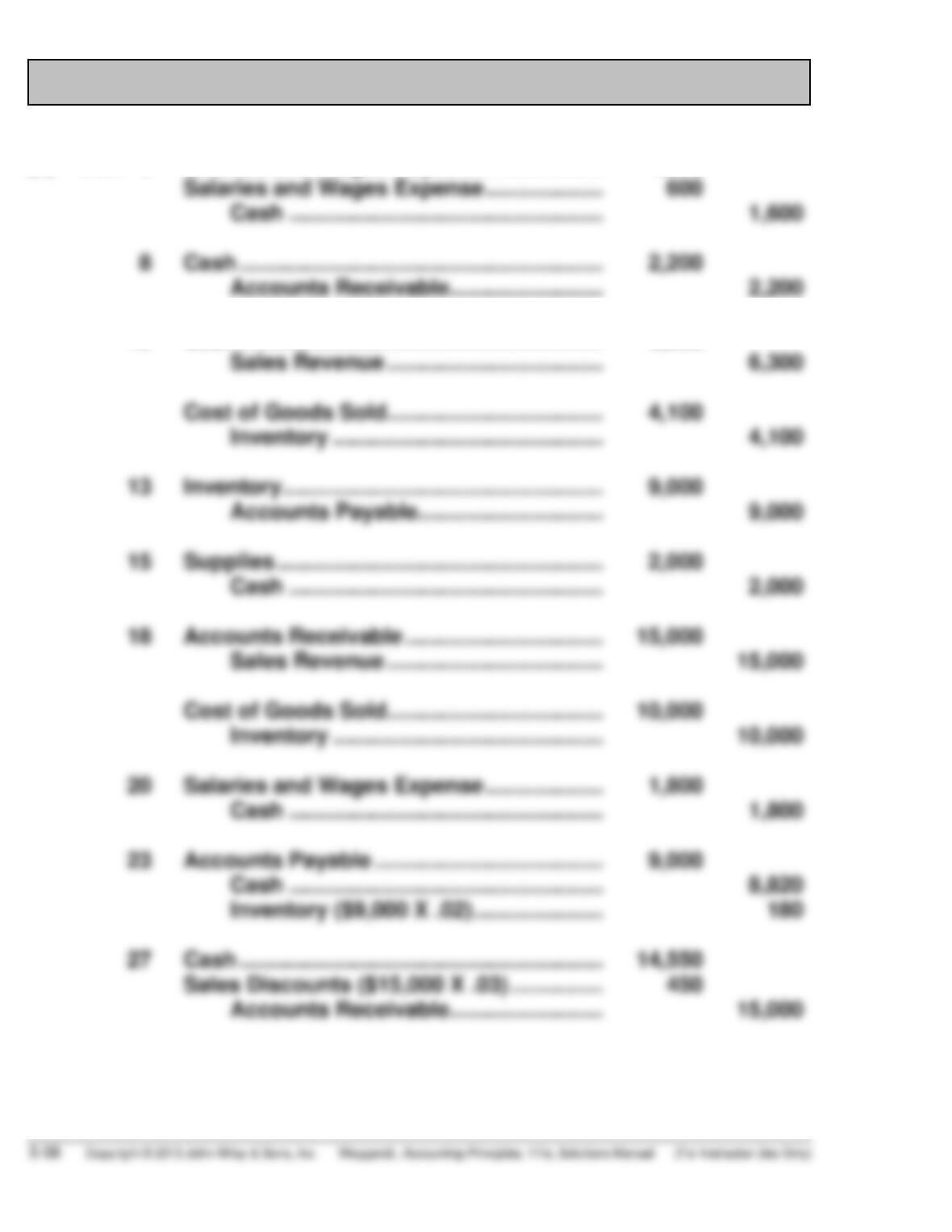

Dec. 6

Salaries and Wages Payable …………………..

Salaries and Wages Expense ………………….

Cash ………………………………………………

1,000

600

1,600

8

Cash ……………………………………………………..

Accounts Receivable……………………….

2,200

Cost of Goods Sold ………………………………..

Inventory ………………………………………..

13

Inventory ……………………………………………….

Accounts Payable …………………………..

9,000

9,000

15

Supplies ………………………………………………..

Cash ………………………………………………

2,000

2,000

18

Accounts Receivable …………………………..

Sales Revenue ………………………………..

Cost of Goods Sold ………………………………..

Inventory ………………………………………..

15,000

10,000

15,000

10,000

20

Salaries and Wages Expense ………………….

Cash ………………………………………………

1,800

1,800

Inventory ($9,000 X .02) ……………………

27

Cash ……………………………………………………..

COMPREHENSIVE PROBLEM SOLUTION (Continued)

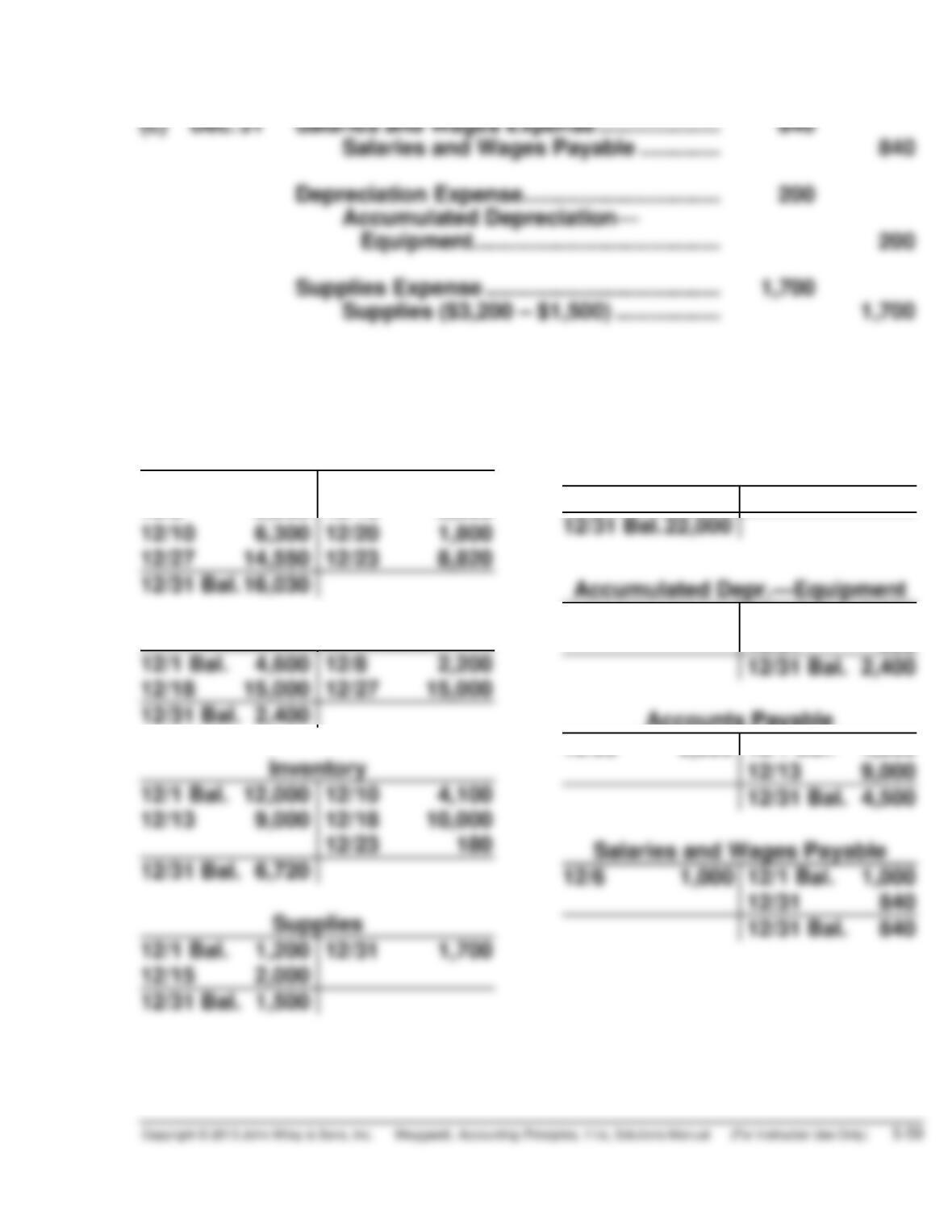

(c)

Dec. 31

Salaries and Wages Expense …………………..

Salaries and Wages Payable …………….

840

840

Accumulated Depreciation—

Equipment …………………………………….

Supplies Expense …………………………………..

Supplies ($3,200 – $1,500) ………………..

(b) & (c) General Ledger

Cash

12/23 8,820

12/31 Bal. 16,030

12/31 Bal. 22,000

12/1 Bal. 7,200

12/8 2,200

12/6 1,600

12/15 2,000

Accounts Receivable

12/1 Bal. 4,600

12/18 15,000

12/8 2,200

12/27 15,000

12/31 Bal. 2,400

12/23 180

12/31 Bal. 6,720

12/13 9,000

12/31 Bal. 4,500

12/6 1,000

12/1 Bal. 1,000

Supplies

12/31 Bal. 1,500

12/1 Bal. 1,200

12/31 1,700

Equipment

12/1 Bal. 22,000

12/1 Bal. 2,200

12/31 200

12/31 Bal. 2,400

Accounts Payable

12/23 9,000

12/1 Bal. 4,500

12/31 840

12/31 Bal. 840

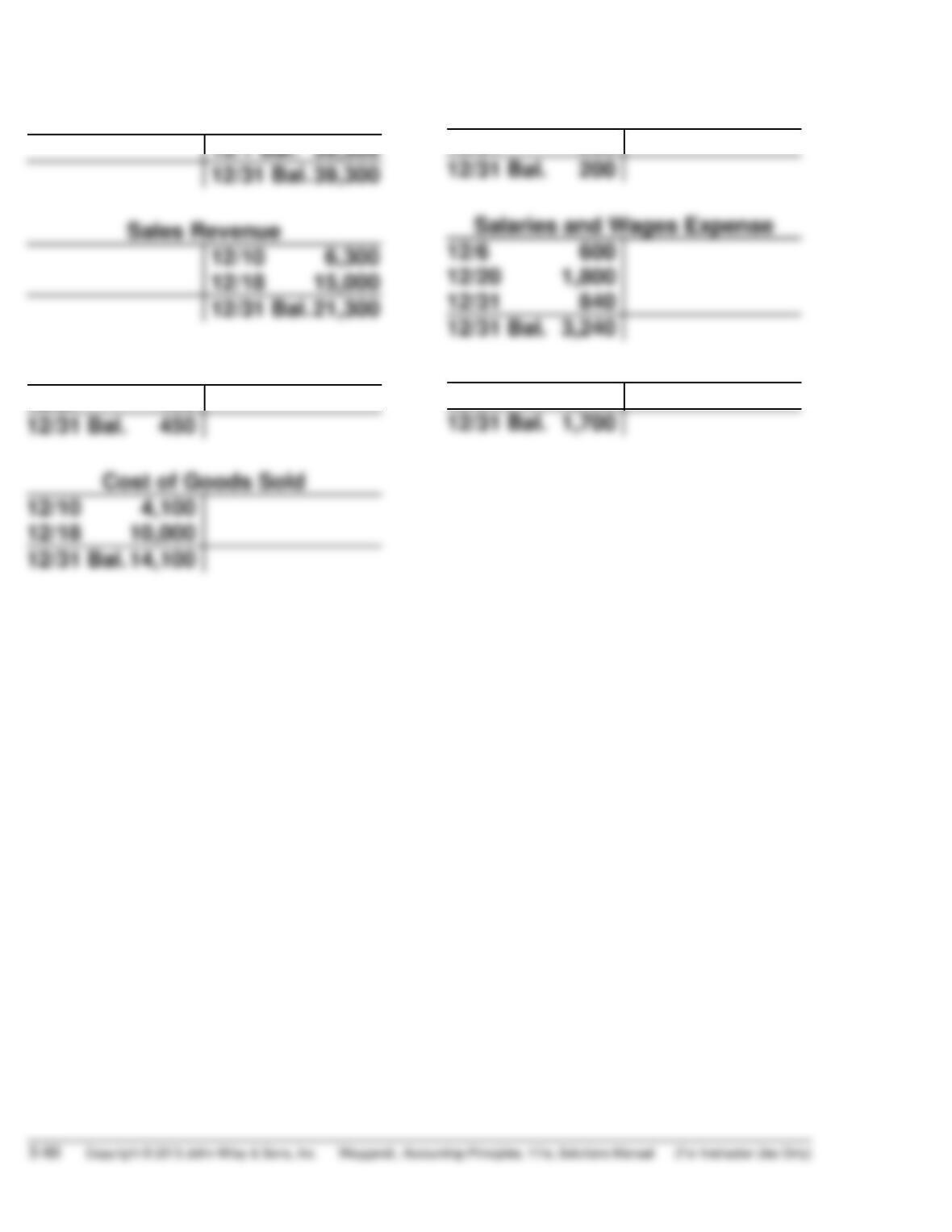

COMPREHENSIVE PROBLEM SOLUTION (Continued)

Owner’s Capital

12/1 Bal. 39,300

12/31 Bal. 39,300

12/31 Bal. 21,300

12/31 Bal. 3,240

Sales Discounts

12/27 450

12/31 Bal. 450

12/31 Bal. 14,100

Depreciation Expense

12/31 200

12/31 Bal. 200

Supplies Expense

12/31 1,700

12/31 Bal. 1,700

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(d) RODRIGUEZ DISTRIBUTING COMPANY

Adjusted Trial Balance

December 31, 2017

DR.

CR.

Cash ……………………………………………………….

$16,030

Accounts Receivable ………………………………….

2,400

Supplies …………………………………………………….

Equipment …………………………………………………

Accumulated Depreciation—Equipment ………

$ 2,400

Accounts Payable ………………………………………

4,500

Salaries and Wages Payable ……………………….

840

Owner’s Capital ………………………………………….

39,300

Sales Revenue ……………………………………………

21,300

Sales Discounts …………………………………………

Cost of Goods Sold …………………………………….

Depreciation Expense …………………………………

Salaries and Wages Expense ………………………

3,240

Supplies Expense …………………………..………….

$68,340

(e) RODRIGUEZ DISTRIBUTING COMPANY

Income Statement

For the Month Ending December 31, 2017

Sales revenue …………………………………………….

$21,300

Less: Sales discounts ……………………………….

450

Net sales ……………………………………………………

20,850

Cost of goods sold …………………………………….

Gross profit ……………………………………………….

Operating expenses

Salaries and wages expense ………………..

$3,240

Supplies expense ………………………………..

Depreciation expense ………………………….

5,140

Net income ………………………………………………..

$ 1,610

COMPREHENSIVE PROBLEM SOLUTION (Continued)

RODRIGUEZ DISTRIBUTING COMPANY

Owner’s Equity Statement

For the Month Ended December 31, 2017

Add: Net income…………………………………………………..

RODRIGUEZ DISTRIBUTING COMPANY

Balance Sheet

December 31, 2017

Assets

Current assets

Cash ……………………………………………………

$16,030

Accounts receivable …………………………….

Inventory …………………………………………….

Supplies ……………………………………………..

Total current assets ………………………..

Property, plant, and equipment

Equipment …………………………………………..

22,000

Less: Accumulated depreciation ………….

Total assets ……………………………………………….

$46,250

Liabilities and Owner’s Equity

Current liabilities

Accounts payable ………………………………..

$4,500

Salaries and wages payable …………………

Total current liabilities …………………….

BYP 5-1 FINANCIAL REPORTING PROBLEM

2012

2013

(a)

(1)

($156,508 – $108,249) ÷ $108,249

44.6% increase

Percentage change in sales:

(2)

Percentage change in net income:

(b)

Gross profit rate:

2011 ($108,249 – $64,431) ÷ $108,249

40.5%

(c)

Percentage of net income to sales:

2011 ($25,922 ÷ $108,249)

23.9%

Comment

The percentage of net income to sales increased 11.7% from 2011 to 2012

BYP 5-2 COMPARATIVE ANALYSIS PROBLEM

PepsiCo

Coca-Cola

(a)

(1)

2013 Gross profit

$35,1721

$28,4332

(2)

(3)

(4)

Percent change in operating

income, 2012 to 2013

6.5%5

increase

5.1%6

decrease

(b) PepsiCo has a higher gross profit but a lower gross profit rate than

Coca-Cola. This can be explained by PepsiCo’s higher sales.

BYP 5-3 COMPARATIVE ANALYSIS PROBLEM

Amazon

Wal-Mart

(a)

(1)

2013 Gross profit

$6,7221

$115,0072

(2)

2013 Gross profit rate

11.0%3

24.3%4

(3)

2013 Operating income

(b) Wal-Mart has a much higher gross profit and gross profit rate than

Amazon. This can be explained by Wal-Mart’s higher markup.

BYP 5-4 REAL-WORLD FOCUS

The answers to this assignment will be dependent upon the articles

selected from the Internet by the student.

BYP 5-5 DECISION MAKING ACROSS THE ORGANIZATION

(a) (1) FAMILY DEPARTMENT STORE

Income Statement

For the Year Ended December 31, 2017

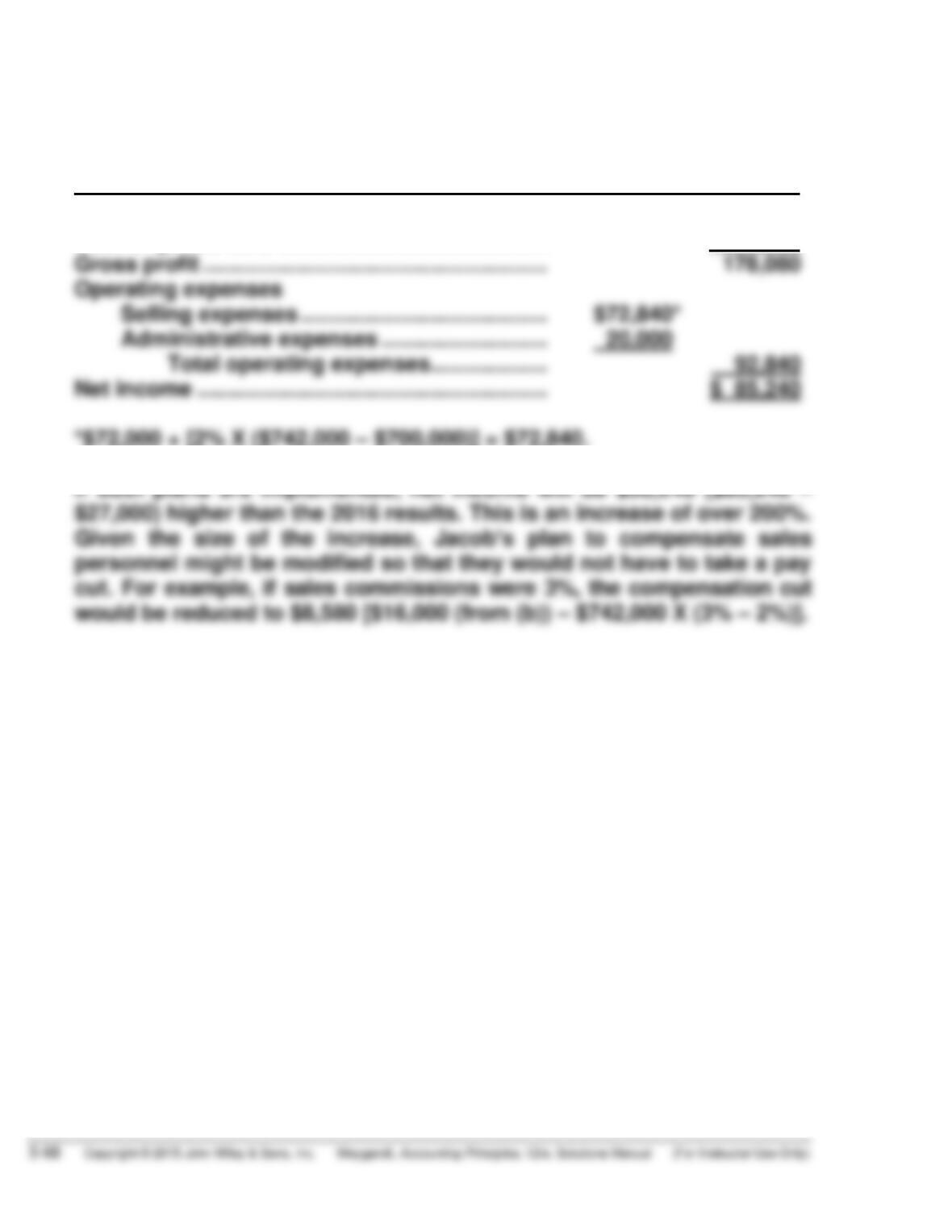

Net sales [$700,000 + ($700,000 X 6%)] …… $742,000

Cost of goods sold ($742,000 X 76%)* …….. 563,920

(2) FAMILY DEPARTMENT STORE

Income Statement

For the Year Ended December 31, 2017

Net sales ………………………………………………. $700,000

Cost of goods sold ………………………………… 553,000

(b) Amy’s proposed changes will increase net income by $31,080. Jacob’s

proposed changes will reduce operating expenses by $28,000 and

BYP 5-5 (Continued)

(c) FAMILY DEPARTMENT STORE

Income Statement

For the Year Ended December 31, 2017

Net sales ……………………………………………………. $742,000

Cost of goods sold …………………………………….. 563,920

*$72,000 + [2% X ($742,000 – $700,000)] = $72,840.

If both plans are implemented, net income will be $58,240 ($85,240 –

$27,000) higher than the 2016 results. This is an increase of over 200%.

BYP 5-6 COMMUNICATION ACTIVITY

(a), (b)

President

Surfing USA Co.

Dear Sir:

As you know, the financial statements for Surfing USA Co. are prepared in

accordance with generally accepted accounting principles. One of these

principles is the revenue recognition principle, which provides that revenues

should be recognized when they are earned.

Whether Parker makes a down payment with the purchase order is

irrelevant in recognizing sales revenue because at this time, you have not

done anything to earn the revenue. A down payment may be an indication

of Parker’s “good faith.” However, its effect on your financial statements is

limited entirely to recognizing the down payment as unearned revenue.

BYP 5-7 ETHICS CASE

(a) Tiffany Lyons, as a new employee, is placed in a position of res-

ponsibility and is pressured by her supervisor to continue an unethical

practice previously performed by him. The unethical practice is taking

(b) The stakeholders (affected parties) are:

• Tiffany Lyons, the assistant treasurer.

• Jay Barnes, the treasurer.

(c) Tiffany’s alternatives:

1. Tell the treasurer (her boss) that she will attempt to take every allow-

able cash discount by preparing and mailing checks within the

2. Join the team and continue the unethical practice of taking undeserved

cash discounts.

3. Go over her boss’s head and take the chance of receiving just and

reasonable treatment from an officer superior to Jay. The company

may not condone this practice. Tiffany definitely has a choice, but

BYP 5-8 ALL ABOUT YOU

In order for revenue to be recognized the performance obligation must be

satisfied. In this case Impact has an obligation to provide goods with a

BYP 5-9 FASB CODIFICATION ACTIVITY

(a) (1) Inventory is the aggregate of those items of tangible personal

property that have any of the following characteristics:

a. Held for sale in the ordinary course of business

b. In process of production for such sale

c. To be currently consumed in the production of goods or services

to be available for sale.

(2) A customer is a reseller or a consumer, either an individual or a

business that purchases a vendor’s products or services for end use

rather than for resale. This definition is consistent with paragraph

BYP 5-9 (Continued)

(b) 330–10–35-15 Only in exceptional cases may inventories properly be

IFRS EXERCISES

IFRS5-1

Expenses may be classified by “nature” or by “function”. The “nature–of–

expense” classification organizes expenses by type of expense, such as

IFRS5-2

By function

Cost of goods sold

By nature

Depreciation expense

By nature

Salaries and wages expense

By function

Selling expenses

By nature

Utilities expense

By nature

Delivery expense

IFRS5-3

MATILDA COMPANY

Comprehensive Income Statement

For the Year Ended 2017

(in thousands of euros)

Net income ……………………………………………………………………. €150

INTERNATIONAL FINANCIAL REPORTING PROBLEM

IFRS5-4

(a) Vuitton uses a multiple step format. The income statement isolates

(b) Vuitton uses Cost of Net Financial Debt rather than Interest Expense on

its income statement.

(c) Inventory is composed of: