Appendix

Capital Investment Decisions: An Overview

Solutions to Review Questions

A-1.

The timing is important because cash received earlier has a greater economic

A-2.

The time value of money merely states that cash received earlier has a greater

A-3.

Revenues represent the accounting measure of inflows to the firm. Revenues

A-4.

Expenses represent the accounting measure of outflows from the firm. Expenses

after cash is spent.

A-5.

Depreciation is an accounting measure of the use of a capital asset and is not a

Solutions to Critical Analysis and Discussion Questions

A-6.

To determine which, if either, project should be approved, the net present value

A-7.

The four types of cash flows are:

A-8.

A-9.

The total amount depreciated over the life of the machine (and, therefore, often

A-10.

Although the working capital might be assumed to be returned to the firm at the

A-11.

The net present value analysis for a new plant considered in this appendix

Solutions to Exercises

A-12. (20 min.) Present Value of Cash Flows: Star City.

a. At 20%

Time

Year

0

1

2

3

4

5

A-13. (25 min.) Present Value of Cash Flows: Rush Corporation.

a.

Year

Depreciation

Tax Shield

at 40%

PV Factor

(8%)

Present

Value

1

$120,000

$ 48,000

.926

$ 44,448

4

.735

$600,000

$240,000

$195,996

b.

Year

Depreciation

Tax Shield

at 40%

PV Factor

(8%)

Present

Value

.857

.681

A-14. (30 min.) Present Value Analysis in Nonprofit Organizations: Johnson Research Organization.

Year

0

1

2

3

4

5

6

7

Investment flows ……………..

$(6,000,000

)

Periodic operating flows:

Annual cash savings …….

$1,400,000

$1,400,000

$1,400,000

$1,400,000

$1,400,000

$1,400,000

$1,400,000

Disinvestment flows ……..

$(6,000,000

)

PV factor 10% …………….

Present value ……………..

)

$1,090,800

$ 991,200

$ 901,200

$ 819,600

$ 745,200

$ 676,800

$ 820,800

Solutions to Problems

A-15. (35 min.) Compute Net Present Value; Compare to Accounting Income:

Lucas Company.

a. Accounting income each year will be $500. The total over four years is $2,000.

b.

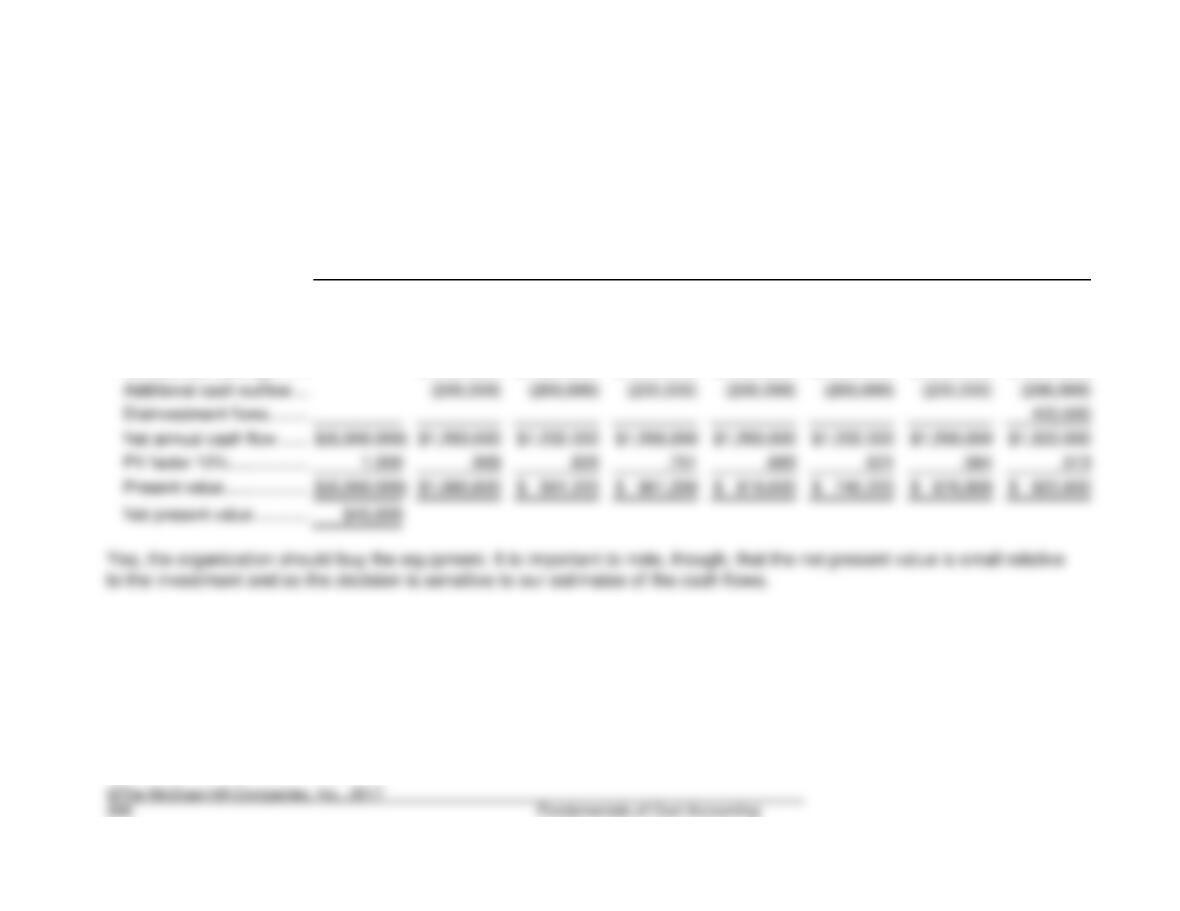

A-16. (35 min.) Sensitivity Analysis in Capital Investment Decisions: Square

Manufacturing.

The schedule of cash flows is ($000 omitted):

Year

Best Case

Expected

Worst

Case

0

($9,000

)

($9,000

)

($9,000

)

1

0

0

0

2

0

0

0

3

5

6

7

Net Present Value @ 14%

Note: In the following calculations, the present value factors are from Exhibit A.8. If you

use Excel or a financial calculator, the net present values might differ slightly.

a$2,802 = $(9,000) + ($6,000 x (0.592 + 0.519 + 0.456 + 0.400))

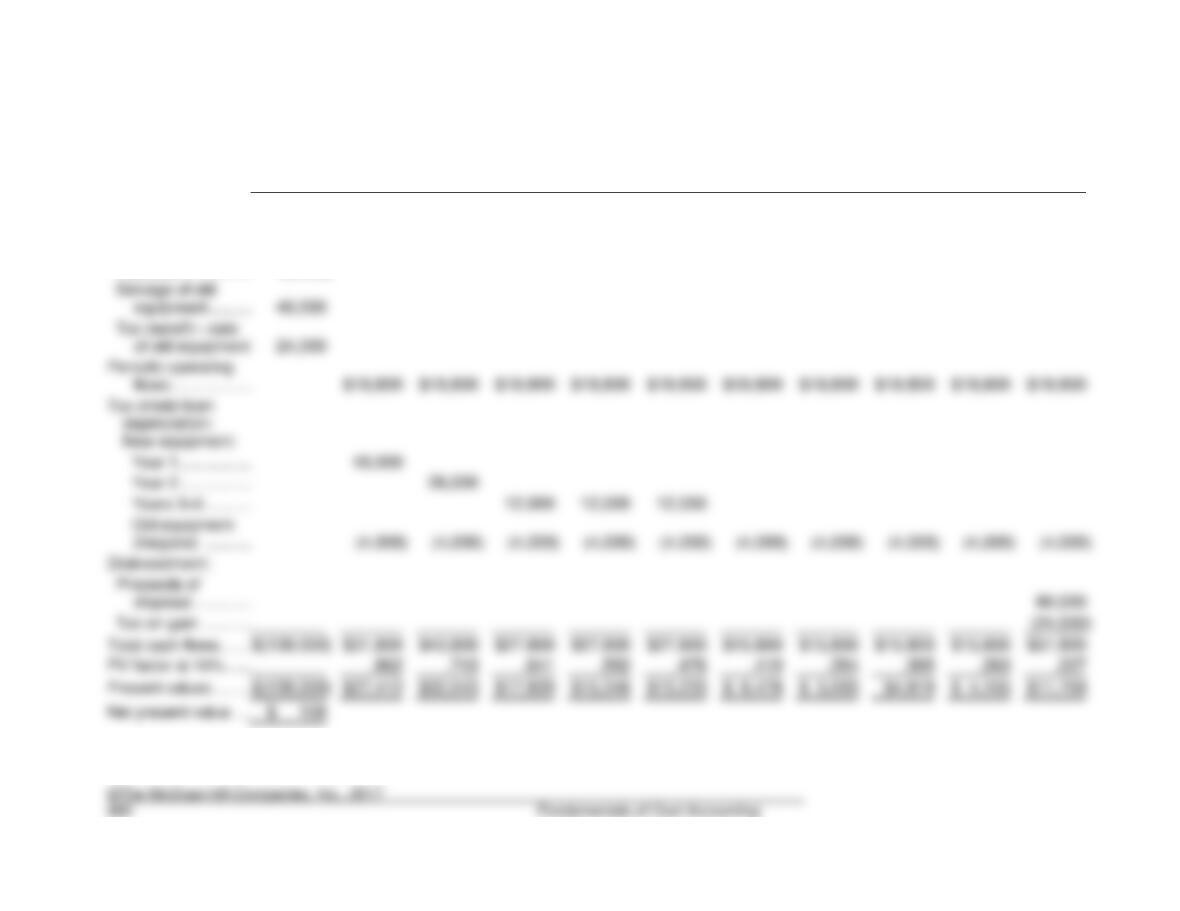

A-17. (40 min.) Compute Net Present Value: Dungan Corporation.

b. Depreciation schedule:

Year

Depreciation

Tax Shield

at 40%

Present Value

Factor (16%)

Present

Value

1

$ 40,000

$16,000

.862

$13,792

3

.641

4

.552

$200,000

$80,000

$54,624

A-17. (continued)

g.

Year

0

1

2

3

4

5

6

7

8

9

10

Investment flows:

Equipment cost ……………………………………………………

$(200,000

)

Removal ……………………………………………………………..

(3,000

)

New equipment:

Year 1 ……………………………………………………………..

Year 2 ……………………………………………………………..

Years 3–5 ………………………………………………………..

)

)

)

)

)

)

)

)

)

)

Disinvestment:

Tax on gain …………………………………………………………

)

Total cash flows …………………………………………………….

$(139,000

)

Present values ………………………………………………………

$(139,000

)

Net present value …………………………………………………..