5-74

PROBLEM 5-66 (CONTINUED)

PROBLEM 5-67 (45 MINUTES)

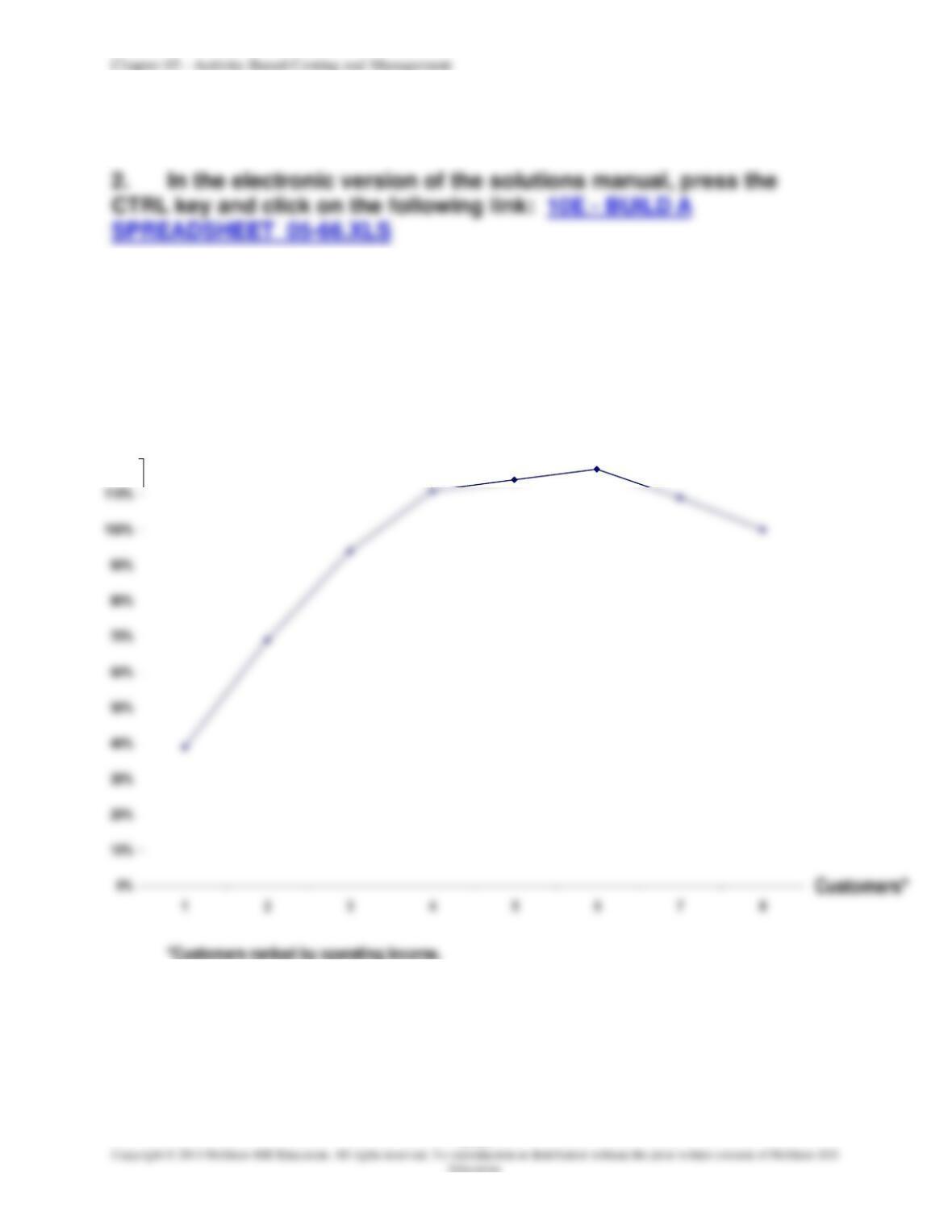

1. Customer-profitability profile (supporting details in the table following the profile):

Cumulative Operating Income as a

Percentage of Total Operating Income

120%

5-75

PROBLEM 5-67 (CONTINUED)

Supporting details for customer-profitability profile:

Customer

Numbera

Customer

Operating

Income

Cumulative

Operating

Income

Cumulative

Operating

Income as a

Percentage of

Total

Operating

Income

(1)

Network-All, Inc.

$186,000

$186,000

39%

(2)

Golden Gate Service Associates

69%

(3)

Graydon Computer Company

94%

(4)

Mid-State Computing Company

(5)

Caltex Computerb

(6)

The California Group

(7)

Tele-Install, Inc.

(8)

Trace Telecomc

aCustomer numbers are ranked by operating income.

2. Memorandum

Date: Today

To: I. Sellit, Vice President for Marketing

From: I. M. Student

Subject: Customer-profitability profile

Chapter 05 – Activity-Based Costing and Management

5-76

SOLUTIONS TO CASES

CASE 5-68 (45 MINUTES)

1.

Activity-based costing (ABC) differs from traditional costing in that it focuses on activities

that consume resources as the fundamental cost drivers. ABC is a two-stage cost

2.

Calculations of total activity cost pools and pool rates:

Material handling ……

($113,208 1.06) [(5 parts 5,000 units) + (10 parts 5,000 units)]

= $120,000* (25,000 parts + 50,000 parts)

= $120,000 75,000 parts = $1.60 per part

*Rounded

Inspection ……………..

($235,850 1.06) (5,000 hours + 7,500 hours)

= $250,000* 12,500 hours = $20 per inspection hour

*Rounded

Machining ……………..

($849,056 1.06) (15,000 hours + 30,000 hours)

= $900,000* 45,000 hours = $20 per machine hour

*Rounded

Assembly ………………

($433,962 1.06) (6,000 hours + 5,500 hours)

= $460,000* 11,500 hours = $40 per assembly hour

*Rounded

Chapter 05 – Activity-Based Costing and Management

5-77

CASE 5-68 (CONTINUED)

3.

JY–63

JY–63

RX–67

RX–67

20×4

Cost

Data

Estimated

20×5

Product

Cost

20×4

Cost

Data

Estimated

20×5

Product

Cost

Direct material:

No cost increase …………………….

Direct labor:

Direct labor

1.08 cost increase* ……………

Material handling:

Number of parts

5,000

$1.60 per unit ……………………

40,000

80,000

Inspection:

Inspection hours

5,000

7,500

$20 per hour …………………….

$20 per hour …………………….

Assembly:

5-78

CASE 5-68 (CONTINUED)

4.

CINCINNATI CYCLE COMPANY

BUDGETED STATEMENT OF GROSS MARGIN FOR 20X5

JY–63

RX–67

Total

Sales revenue ………………………………………….

$3,621,000

$4,459,000

$8,080,000

Cost of goods manufactured and sold:

Beginning finished-goods inventory …………

$ 480,000

$ 600,000

$1,080,000

Add:

Direct material……………………………….

3,500,000

Direct labor …………………………………..

600,000

Material handling …………………………..

Inspection …………………………………….

100,000

150,000

250,000

Machining ……………………………………..

Assembly ……………………………………..

Cost of goods available for sale ……………….

$3,560,000

$5,350,000

$8,910,000

Less:

Ending finished-goods inventory* …

431,200

665,000

Cost of goods sold …………………………………..

$3,128,800

$4,685,000

$7,813,800

*Ending finished-goods inventory = (total product cost

units produced) ending

inventory in units:

Chapter 05 – Activity-Based Costing and Management

5-79

CASE 5-69 (60 MINUTES)

1.

Regular

Model

Advanced

Model

Deluxe

Model

Product costs based on traditional, volume-

based costing system ………………………….

$210.00

$430.00

$464.00

2.

Product costs based on activity-based costing system:

Regular

Model

Advanced

Model

Deluxe

Model

Direct material ………………………………………….

$ 20.00

$ 50.00

$ 84.00

Direct labor ………………………………………………

Machinery depreciation and maintenancea …

Engineering, inspection and

repair of defectsb …………………………………

material handlingc ……………………………….

Factory depreciation, taxes, insurance,

aPool I:

Depreciation, machinery ………………………………………………………

$2,960,000

Maintenance, machinery ………………………………………………………

Total ……………………………………………………………………………………

$3,200,000

Chapter 05 – Activity-Based Costing and Management

5-80

CASE 5-69 (CONTINUED)

bPool II:

Engineering ………………………………………………………………………..

$ 700,000

Inspection and repair of defects …………………………………………..

Total ……………………………………………………………………………………

$1,450,000

cPool III:

Purchasing, receiving, and shipping …………………………………….

$ 500,000

Material handling …………………………………………………………………

Total ……………………………………………………………………………………

$1,300,000

dPool IV:

Depreciation, taxes, and insurance for factory ………………………

$ 600,000

Miscellaneous manufacturing overhead ……………………………….

Total ……………………………………………………………………………………

$1,190,000

3.

Regular

Model

Advanced

Model

Deluxe

Model

Product costs based on activity-based

costing system …………………………………………..

5-81

CASE 5-69 (CONTINUED)

4.

MEMORANDUM

Date:

Today

To:

President Madison Electric Pump Corporation

From:

I.M. Student

Subject:

Product costing

Based on the cost data from our traditional, volume-based product-costing system,

our regular model is not very profitable. Its reported actual contribution margin is only

5-82

CASE 5-69 (CONTINUED)

5.

The company should adopt and maintain the activity-based costing system. The price

of the regular model should be lowered to the $212. Lowering the price should enable

the firm to regain its competitive position in the market for the regular model. Further

Chapter 05 – Activity-Based Costing and Management

CASE 5-70 (20 MINUTES)

Regular

Model

Advanced

Model

Deluxe

Model

Traditional, volume-based costing system:

reported product cost …………………………………

Activity-based costing system:

reported product cost …………………………………

Amount of cost distortion per unit ……………………..

Traditional

Traditonal

Traditional

system

system

system

overcosts

undercosts

overcosts

Advanced

model by

model by

$17.98

Product volume ………………………………………………

20,000

1,000

10,000

Total amount of cost distortion for entire

product line ………………………………………………..

5-84

CASE 5-71 (20 MINUTES)

1.

The controller, Erin Jackson, has acted ethically up to this point. She correctly

pointed out to the president that the firm’s traditional, volume-based product-costing

2.

The production manager, Alan Tyler, is not acting ethically. Although we can

3.

Jackson has an ethical obligation to the president, to the company, to her profession,

and to herself to report accurate product-costing data to the president. There is

nothing wrong with her offer to her friend to go over her analysis again to verify its

accuracy. However, she must report what she finds with no suppression or alteration

of the data. Several of the ethical standards for managerial accounting apply in this

case. (See Chapter 1 for a listing of these standards.) The standards that are most

clearly relevant include the following:

Integrity:

Credibility:

5-85

CASE 5-71 (CONTINUED)

Jackson is in a tough spot. Her professional obligation to report accurate product

costs is clear. She cannot ethically avoid this responsibility. Yet her friend Tyler is in

a tenuous position. What can Jackson ethically do for him? First, she can be

FOCUS ON ETHICS (See page 192 in the text.)

This scenario explores ethical issues surrounding activity-based costing. Among

the potential ethical issues in this situation are the following:

• How did the product proliferation problem at the Charlotte plant come about? Were

product-line managers more concerned with maintaining their spheres of influence

than making product discontinuance decisions that would be in the company’s best

interest? At the very least, the company seems to exhibit a lack of discipline and

focus. Products that have been dropped as a result of sound analysis should not

routinely creep back into the product line.

• Why did top management refuse to adopt the recommendations of the ABC

analysis? It is sometimes said that top managers are compensated and rewarded

• Alternatively, perhaps management is genuinely concerned about the implications

for their employees if a large number of products are dropped. Is it ethical for

management to put the interests of their employees ahead of those of the company’s

shareholders?

• Was it ethical for Xavier’s top management to sell the Engine Parts Division,

probably suspecting that the Charlotte plant would be closed and people would be

laid off?