Chapter 5

Cost Estimation

Learning Objectives

1. Understand the reasons for estimating fixed and variable costs.

2. Estimate costs using engineering estimates.

6. Identify potential problems with regression data.

7. Evaluate the advantages and disadvantages of alternative cost estimation methods.

8. (Appendix A) Use Microsoft Excel to perform a regression analysis.

9. (Appendix B) Understand the mathematical relationship describing the learning phenomenon.

Chapter Overview

I. WHY ESTIMATE COSTS?

II. BASIC COST BEHAVIOR PATTERNS

III. WHAT METHODS ARE USED TO ESTIMATE COST BEHAVIOR?

• Engineering Method

• Account Analysis Method

• Statistical Cost Estimation

o Relevant Range of Activity

o Scattergraphs and High-Low Estimates

o Number of Observations

o High-Low Cost Estimation

• Multiple Regression

• Practical Implementation Problems

o Effect of Nonlinear Relations

o Effect of Outliers

o Effect of Spurious Relations

o Effects of Using Data That do not Fit the Assumptions of Regression Analysis

o Regression Must Be Used With Caution

IV. LEARNING PHENOMENON

• Applications

o Decision Making

o Performance Evaluation

V. HOW IS AN ESTIMATION METHOD CHOSEN?

• Data Problems

• Effect of Different Methods on Cost Estimates

VI. APPENDIX A: REGRESSION ANALYSIS USING MICROSOFT EXCEL

• Using Microsoft Excel to Estimate Regression Coefficients

VII. APPENDIX B: LEARNING CURVES

Chapter Outline

LO 5-1 Understand the reasons for estimating fixed and variable costs.

WHY ESTIMATE COSTS?

• When managers make decisions, they need to compare the costs and benefits among

alternative actions.

BASIC COST BEHAVIOR PATTERNS

• The most important characteristic of costs for decision making is how they behave.

o Key terms for describing cost behavior:

o Activities can be measured by volume, by complexity, or by any other cost driver.

o Cost equation: TC = F + VX, where:

WHAT METHODS ARE USED TO ESTIMATE COST BEHAVIOR?

• Three general methods are used to estimate the relation between cost behavior and activity

levels.

LO 5-2 Estimate costs using engineering estimates.

• Engineering Method

o An engineering estimate is a cost estimate based on measurement and pricing of the

work involved in a task.

▪ A detailed step-by-step analysis is performed of what needs to be done; that is, the

activities that must be conducted. The times or costs are then estimated for each

activity.

o Advantages of engineering estimates:

▪ It can detail each step required to perform an operation permitting comparison with

similar operations in order to review productivity and to identify strengths and

weaknesses.

o Difficulties associated with engineering estimates:

LO 5-3 Estimate costs using account analysis.

• Account Analysis Method

o Account analysis is a cost estimation method that calls for a review of each account

making up the total cost being analyzed.

o Exhibit 5.1 shows an example of cost estimation using account analysis; in this example:

▪ Each major class of overhead costs is itemized and divided into its estimated variable

and fixed components.

o Account analysis helps determine the fixed cost (F) and the variable cost per unit (V) in

the cost equation: TC = F + VX.

▪ An estimate of the total cost (TC) in the future can be made for other activity levels

(X) as long as they are within the relevant range of the operations.

LO 5-4 Estimate costs using statistical analysis.

• Statistical Cost Estimation

o When random and unusual events are present, statistical analysis can use data from the

past several periods of operations or several locations as the basis for estimating cost

relations.

o Relevant Range of Activity

▪ When using statistical approaches to cost estimation, we need to ensure that the

activity levels of the past are relevant for the activity levels estimated. Extrapolations

beyond the upper and lower bounds of past observations are highly subjective.

o Scattergraphs and High-Low Estimates

▪ A scattergraph is a graph that plots costs against activity levels.

• This visual representation of the data provides a quick indication of the fixed-

variable relation of costs and activities.

o Number of Observations

▪ The number of observations needed for scattergraph depends on the availability of the

data, the variability within the data, the relative costs and benefits of collecting

reliable data, and the length of time the current process has been in operation.

▪ A line can be visually fitted (by way of “eyeball judgment”) to the data points as

closely as possible and extended to the vertical axis on the scattergraph.

• The slope of the line represents the estimated variable cost per unit; the slope is

referred to as the variable cost per unit because it represents the change in costs

that occurs as a result of changes in activity.

o High-Low Cost Estimation

▪ High-low cost estimation is the method that estimates costs based on two cost

observations, usually at the highest and lowest activity levels.

Total Cost (Y=TC)

x

x

x

x

x

x

x

x

• The slope of the total cost line, which estimates the increase in variable costs

associated with an increase of one unit of activity, can be estimated using the

following equation:

Variable cost per unit (V) =

y2 – y1

x2 – x1

• An estimate of the costs for any given activity level can then be computed using

the cost equation: TC = F + VX.

▪ The high-low method is easy to apply, but must be used carefully to ensure that the

two points chosen to prepare the estimates represent cost and activity relations over

the range of activity for which the prediction will be made.

See Demonstration Problem 2

o Statistical Cost Estimation Using Regression Analysis

▪ With computational tools included in many calculators or in spreadsheets such as

Microsoft Excel®, the additional cost of using all the data instead of two points is

quite small.

▪ Regression is a statistical procedure to determine the relation between variables.

LO 5-5 Interpret the results of regression output.

o Obtaining Regression Estimates

▪ The most important step in obtaining regression estimates for cost estimation is to

establish the existence of a logical relation between activities and the cost to be

estimated.

▪ Entering numbers that have no logical relation can result in misleading estimates; the

activities (i.e., independent variables) must be logically related to costs to be

estimated (i.e., dependent variables).

▪ A simple regression uses just a single predictor.

• The intercept term from the output of a regression program is an estimate of fixed

cost; the intercept at zero activity it is usually outside the relevant range of

observations.

o Correlation Coefficients

▪ In addition to the cost-estimating equation, the regression program provides other

useful statistics.

• Correlation coefficient (R, or multiple R) is a measure of the linear relation

between two or more variables, such as cost and some measure of activity.

• The square of R (or R2) is called the coefficient of determination; it is the square

of the correlation coefficient, interpreted as the proportion of the variation in the

dependent variable explained by the independent variable(s).

▪ Example : The regression results in Exhibit 5.3 where the linear relation between

overhead cost and repair-hours used is estimated are as follows:

Correlation coefficient (R) … .910

R2 …………………………… .828

• Because the correlation coefficient (R) of .910 is close to ±1.0, the data points are

▪ The most commonly used regression technique is called ordinary least squares

regression (OLS).

• With this technique, the regression line is computed so that the sum of the squares

of the vertical distances from each point to the regression line is minimized.

o Confidence in the Coefficients

▪ In many cases, it can be desirable to determine whether the estimated coefficient on

the independent variable is significantly different from zero. For example, when

determining fixed and variable costs, if the estimated coefficient is significantly

different from zero, we can conclude that the cost is not totally fixed.

• The t-statistic is used to test the significance of the coefficient; the t-statistic, t, is

the value of the estimated coefficient, b, divided by its standard error.

The t-statistic is computed as the value of the estimated coefficient, b, divided

by its estimated standard error (SEb):

• The significance level of the t statistic is called the p-value. A very small p-value

(close to zero) means that the probability that the true value of the coefficient is

zero, given the data, is virtually zero.

• Example: From the regression results in Exhibit 5.3, where the linear relation

between overhead cost and repair-hours used is estimated, b = $12.52 and SEb =

1.5843.

• Multiple Regression (See Business Application box “Using Statistical Analysis to Improve

Profitability.”)

o Management might wish to see whether a better estimate can be obtained using additional

predictor variables.

o The adjusted R-squared (R2) is the correlation coefficient squared and adjusted for the

number of independent variables used to make the estimate.

▪ This adjustment to R2 recognizes that as the number of independent variables

increases, R2 (unadjusted) increases.

LO 5-6 Identify potential problems with regression data.

• Practical Implementation Problems

o Some of the more common problems with using regression estimates include

▪ Attempting to fit a linear equation to nonlinear data

o Effect of Nonlinear Relations

▪ The effect of attempting to fit a linear model to nonlinear data is likely to occur when

the firm is operating near its capacity limits.

▪ One way to overcome the problem is to define a relevant range of activity and use the

range for one set of cost-estimating regression equations.

• A different equation could be derived for the levels between 81 and 100 percent

capacity.

o Effect of Outliers

▪ Because regression minimizes the sum of the squared deviations from the regression

line, observations that lie a significant distance away from the line could have an

overwhelming effect on the regression estimates.

o Effect of Spurious Relations

▪ Spurious relations may result from including many variables in the regression in the

hope of finding relations among the variables.

o Effects of Using Data That do not Fit the Assumptions of Regression Analysis

o Regression Must Be Used With Caution

▪ A regression estimate is only an estimate; users should:

• Fully understand the method and its limitations

LEARNING PHENOMENON

• Learning affects labor costs. The more experience that workers have in performing a task, the

less time they spend on it.

o The learning phenomenon refers to the systematic relationship between the amount of

experience in performing a task and the time required to perform it.

o Example: Using the incremental unit-time learning model with an 85 percent learning

rate for workers, whenever the output units are doubled (say from the first unit to the

second unit or from the second unit to the fourth unit, and so on), the time it takes to

produce the new output volume will be 85 percent of what it took to produce half of it

previously.

▪ That is:

• Applications

o Decision Making

▪ The learning phenomenon means that variable costs tend to decrease per unit as the

volume of activity increases. Thus, a linear cost estimate will overstate the variable

cost per unit.

LO 5-7 Evaluate the advantages and disadvantages of alternative cost

estimation methods.

HOW IS AN ESTIMATION METHOD CHOSEN?

• The most informative estimate of cost behavior results from using several methods because

each has the potential to provide information that the others do not.

o In general, the more sophisticated methods yield more accurate cost estimates than the

simpler methods do.

actually follow curvilinear, step, semivariable, and other patterns.

• Data Problems

o No matter which method is used to estimate costs, the results are only as good as the data

used.

• Effect of Different Methods on Cost Estimates

o Each cost estimation method can yield a different estimate of the costs that are likely to

result from a particular management decision.

LO 5-8 (Appendix A) Use Microsoft Excel to perform a regression analysis.

APPENDIX A: REGRESSION ANALYSIS USING MICROSOFT EXCEL

• Using Microsoft Excel to Estimate Regression Coefficients

o The following steps are based on Version 12 of Excel (part of Microsoft Office 2013).

▪ Step 1: Ensure you have the Analysis TookPak installed. See Exhibits 5.9 and 5.10.

(If not, install it. See Exhibits 5.11 through 5.13.)

o Exhibits 5.19 and 5.20 illustrate the performance of a multiple regression.

LO 5-9 (Appendix B) Understand the mathematical relationship describing

the learning phenomenon.

APPENDIX B: LEARNING CURVES

• Engineers have found the following mathematical relationship for the learning phenomenon:

o Example (continued from previous example): With the same incremental unit-time

Unit

Produced

(X)

Labor time

required to produce

the Xth unit

Cumulative

total time

in labor

hours

Total cost

(@ $40

per hour)

Average

cost

per unit

1

120 hours

120 hours

$4,800

$4,800

2

102.00 (= 120 × .85)

222

8,880

4,440

8

73.70 (= 86.7 × .85)

28,492

3,561

▪ The relation between total and average costs is shown below. The average cost per

unit declines as the labor time required is decreasing to reflect the impact of the

learning phenomenon.

$25,000

$30,000

Matching

A.

Account analysis

H.

Independent variable

B.

Adjusted R-squared (R2)

I.

Learning phenomenon

C.

Coefficient of determination

J.

Regression

D.

Correlation coefficient

K.

Relevant range

E.

Dependent variable

L.

Scattergraph

F.

Engineering estimate

M

t-statistic

G.

High-low cost estimation

_____ 1. A cost estimate based on measurement and pricing of the work involved in a task.

_____ 2. Represents the limits within which a cost estimate may be valid.

_____ 3. A graph that plots costs against activity levels.

_____ 4. The value of the estimated coefficient divided by its standard error.

_____ 5. A cost estimation method that calls for a review of each account making up the total

cost being analyzed.

_____ 6. A measure of the linear relation between two or more variables.

_____ 7. The X term, or predictor, on the right-hand side (RHS) of a regression equation.

_____ 8. A systematic relationship between the amount of experience in performing a task and

the time required to perform it.

_____ 9. Statistical procedure to determine the relation between variables.

_____ 10. The Y term, or the left-hand side (LHS) of a regression equation.

_____ 11. The proportion of the variation in the dependent variable explained by the

independent variable(s).

_____ 12. A method to estimate costs based on two cost observations on the scattergraph,

usually at the highest and lowest activity levels.

_____ 13. Correlation coefficient squared and adjusted for the number of independent variables

used to make the estimate.

Multiple Choice Answers

1. F

Multiple Choice

1. Cost estimation:

a. Is useful for decision making.

b. Is based on past cost pattern.

c. Differentiates between variable and fixed costs.

d. All of the above.

2. Engineering estimates:

a. Are very time consuming.

b. For labor time may use time and motion study.

c. Requires data from prior activities.

d. Both a and b.

3. You are asked to conduct an account analysis of overhead. For last month, 450 labor hours

were incurred while spending $12,750 on overhead costs. You determined that fixed

overhead accounted for 40% of total overhead costs. Which of the following statements is

correct?

a. Last month’s fixed overhead cost was $5,200.

b. Variable overhead per labor hour was $17.

c. The projected overhead cost for 475 labor hours will be $13,750.

d. There is not information determine which statement is correct.

Use the following information to answer questions 4 – 6:

For a typical quarter, the highest activity is 450 machine hours with overhead of $26,250; the

lowest activity is 250 machine hours with overhead of $18,750.

4. What is the variable overhead per machine hour?

a. $30.50

b. $32.50

c. $35.50

d. $37.50

5. What is the fixed overhead cost?

a. $8,500

b. $8,750

c. $9,375

d. $9,650

6. What is the projected overhead costs if next quarter’s activity is expected to be 360 machine

hours?

a. $19,425

b. $20,935

c. $21,355

d. $22,875

7. The following shows a partial printout of a regression analysis:

Coefficients

Intercept

6903.83329

X Variable 1

3.02097535

Which of the following statement about this regression analysis is correct?

a. The fixed cost component is $6,903.

b. The variable cost per unit is $3.02.

c. Projected total cost for 400 units of activity will be $8,111.

d. All of the above.

8. Regression analysis:

a. Is always accurate.

b. Uses statistical techniques.

c. May involve more than one predictor variable.

d. Both b and c.

9. The data used to estimate cost function:

a. May be misplaced.

b. Are not subjected to inflation.

c. Never include allocated costs.

d. Are all within the relevant range.

10. It takes 80 hours of labor time to complete the first unit of output. Assuming that the

company adopts the individual unit-time learning model with a 90 percent learning rate:

a. The 2nd unit will take 72 hours.

b. The time to finish the 3rd unit can’t be determined.

c. The fourth unit will take 64 hours.

d. Direct materials will be reduced because of learning.

11. High-low cost estimation:

a. Provides a very precise cost estimate.

b. Assumes that costs behave linearly.

c. Uses extreme points which are always representative of the rest of the data.

d. Is used to determine total product costs.

12. Which of the following statements about learning is correct?

Multiple Choice Answers

1. d (LO1)

Demonstration Problem 1

John, a cost analyst for a manufacturing firm, was asked to estimate the overhead costs at one of

the factories. He interviewed the supervisor and several workers there to get a feel of how

overhead costs changed. His experience with the cost accounting system pointed to the use of

machine hours as the cost driver for overhead items.

Over the last 12 months, the total overhead costs were $103,918. John determined that total fixed

overhead costs totaled $4,620 per month; the rest are variable costs. For the same period of time,

4,519 machine hours were incurred in that factory.

Required:

1. What is the general cost equation (TC = F + VX) that describes the relation between

overhead costs and machine hours?

2. If the factory expects to spend 400 machine hours next month, what is the expected amount

of overhead costs?

Demonstration Problem 1 – Solution

Part 1

Total variable overhead costs = Total overhead costs – Total fixed costs

Part 2

Demonstration Problem 2

(Continued from Demonstration Problem 1)

John, a cost analyst for a manufacturing firm, was asked to estimate the overhead costs at one of

the factories. He interviewed the supervisor and several workers there to get a feel of how

overhead costs changed. His experience with the cost accounting system pointed to the use of

machine hours as the cost driver for overhead items. Over the last 12 months, the total overhead

costs were $103,918, out of which John determined $4,620 to be fixed cost per month and the

rest variable cost. For the same period of time, 4,519 machine hours were incurred in that factory.

The cost analyst, John, went back to the accounting information system to look for more relevant

data. The following breakdown of the overhead costs and the associated machine hours over the

same 12-month period was available:

Month

Overhead

Machine Hours

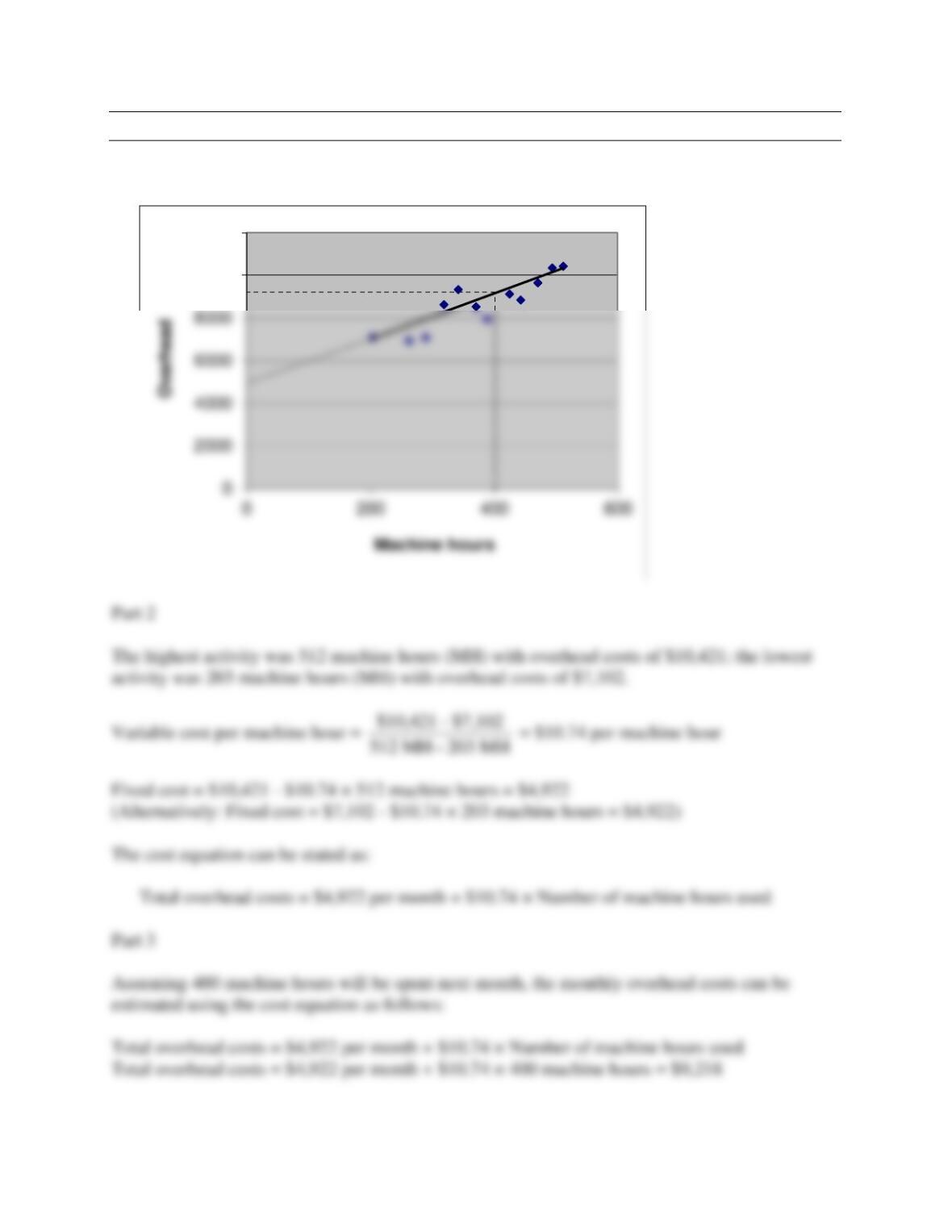

1

$ 7,102

203

2

8,620

319

3

9,120

425

4

7,092

289

5

7,965

388

6

9,641

471

7

10,421

512

8

8,834

443

9

6,935

262

10

8,520

371

11

10,342

494

12

9,326

342

Total

$103,918

4,519

Required:

1. Plot the data using scattergraph.

2. Use the high-low method to estimate the cost function.

3. Predict overhead costs when 400 machine hours are expected to be spent for the coming

month.

Demonstration Problem 2 – Solution

Part 1

10000

12000

Demonstration Problem 3

(Continued from Demonstration Problem 2)

John, a cost analyst for a manufacturing firm, was asked to estimate the overhead costs at one of

the factories. He interviewed the supervisor and several workers there to get a feel of how

overhead costs changed. His experience with the cost accounting system pointed to the use of

machine hours as the cost driver for overhead items. Over the last 12 months, the total overhead

costs were $103,918, out of which John determined $4,620 to be fixed cost per month and the

rest variable cost. For the same period of time, 4,519 machine hours were incurred in that factory.

The cost analyst, John, went back to the accounting information system to look for more relevant

data. The following breakdown of the overhead costs and the associated machine hours over the

same 12-month period was available:

Month

Overhead

Machine Hours

1

$ 7,102

203

2

8,620

319

3

9,120

425

4

7,092

289

5

7,965

388

6

9,641

471

7

10,421

512

8

8,834

443

9

6,935

262

10

8,520

371

11

10,342

494

12

9,326

342

Total

$103,918

4,519

John recently attended a workshop on statistical analysis. He was interested in applying the

regression analysis to solve the relation between overhead costs and machine hours.

Required:

1. Determine the cost equation using the regression analysis and interpret the regression results.

2. Predict overhead costs when 400 machine hours are expected to be spent for next month.

3. Indicate the t-statistic and the p-value associated with the estimated coefficient, b.

4. Given a t value of 2.228, construct the 95 percent confidence interval around the estimated

coefficient, b.

Demonstration Problem 3 – Solution

Part 1

John’s analysis indicated that a logical relation exists between overhead costs and machine hours.

Microsoft Excel was used. Data on overhead costs were treated as Y, or the dependent variable.

Data on machine hours were treated as X, or the independent variable.

The regression results are as follows:

Part 2

Demonstration Problem 3 – Solution, continued

Part 3