5–21 Ch. 5—Problems

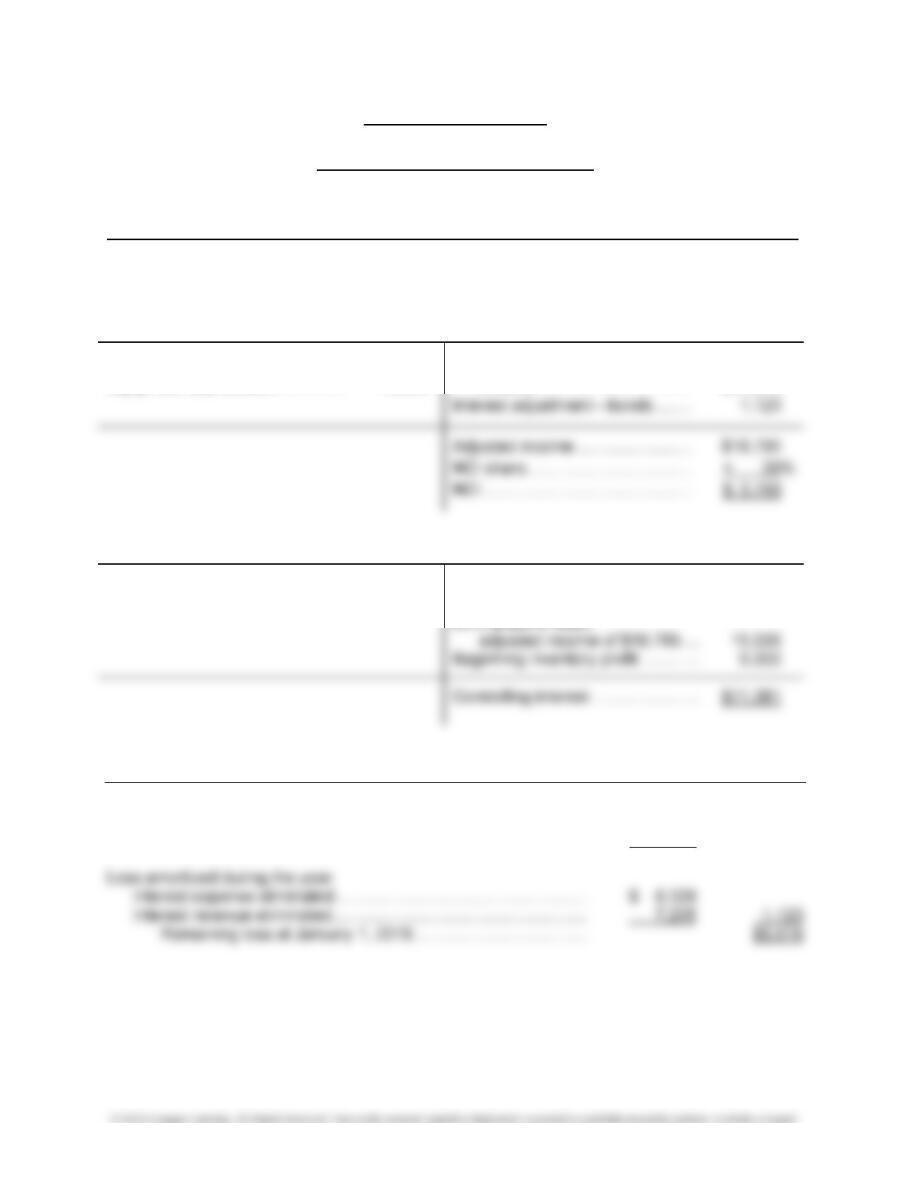

Problem 5-5, Continued

Intercompany Inventory Profit Deferral

Parent Parent Parent Sub Sub Sub

Amount Percent Profit Amount Percent Profit

Beginning ………………………… $20,000 30% $6,000 — 0% —

Ending …………………………….. 25,000 30 7,500 — 0 —

Subsidiary Stark Company Income Distribution

Buildings depreciation …………….. $ 4,000 Internally generated net

Equipment depreciation ………….. 10,000 income …………………………….. $31,672

Parent Pontiac Company Income Distribution

Ending inventory profit ……………. $7,500 Internally generated net

income ………………………………. $57,845

Proof for Bond Retirement

Loss remaining at year-end:

Investment in bonds at December 31, 2016 ………………………… $103,180

Carrying value at December 31, 2016 ………………………………… 98,687 $4,493

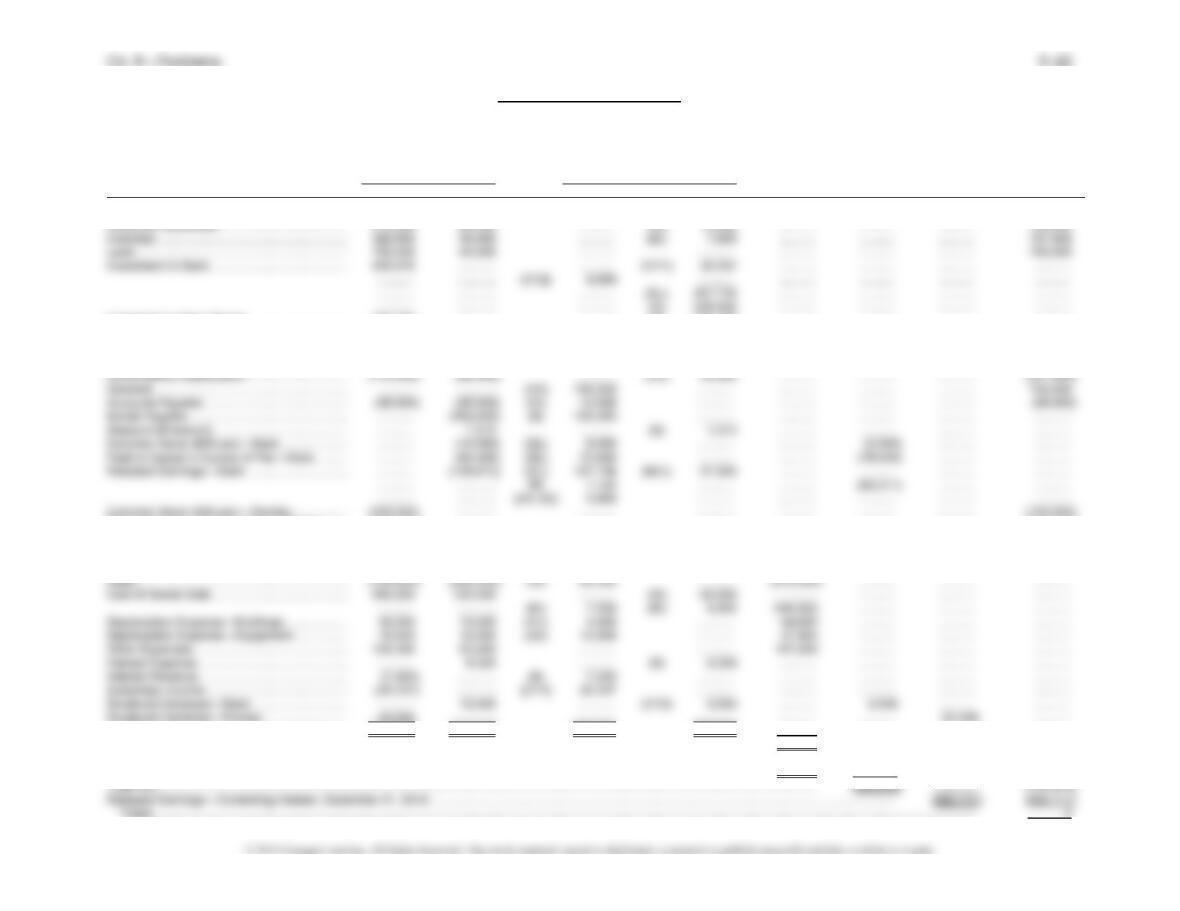

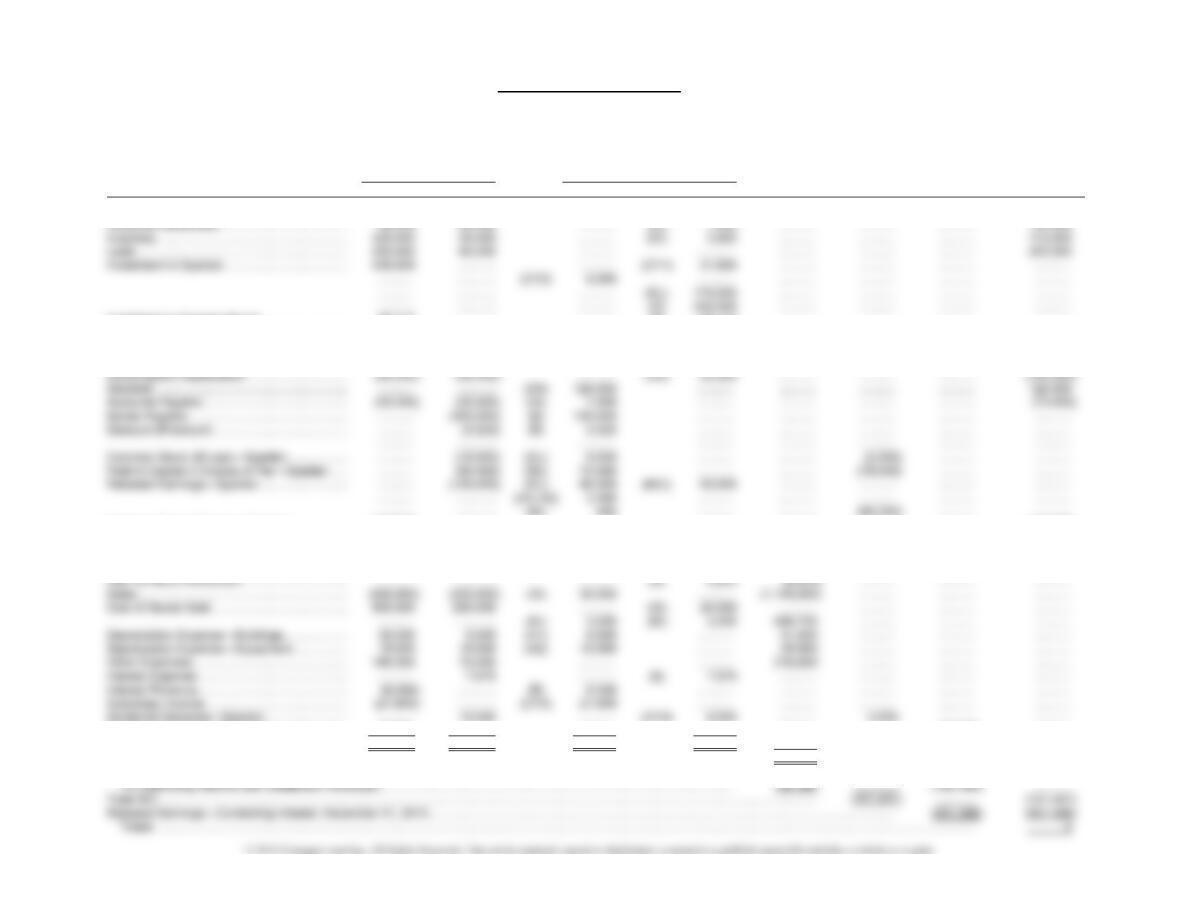

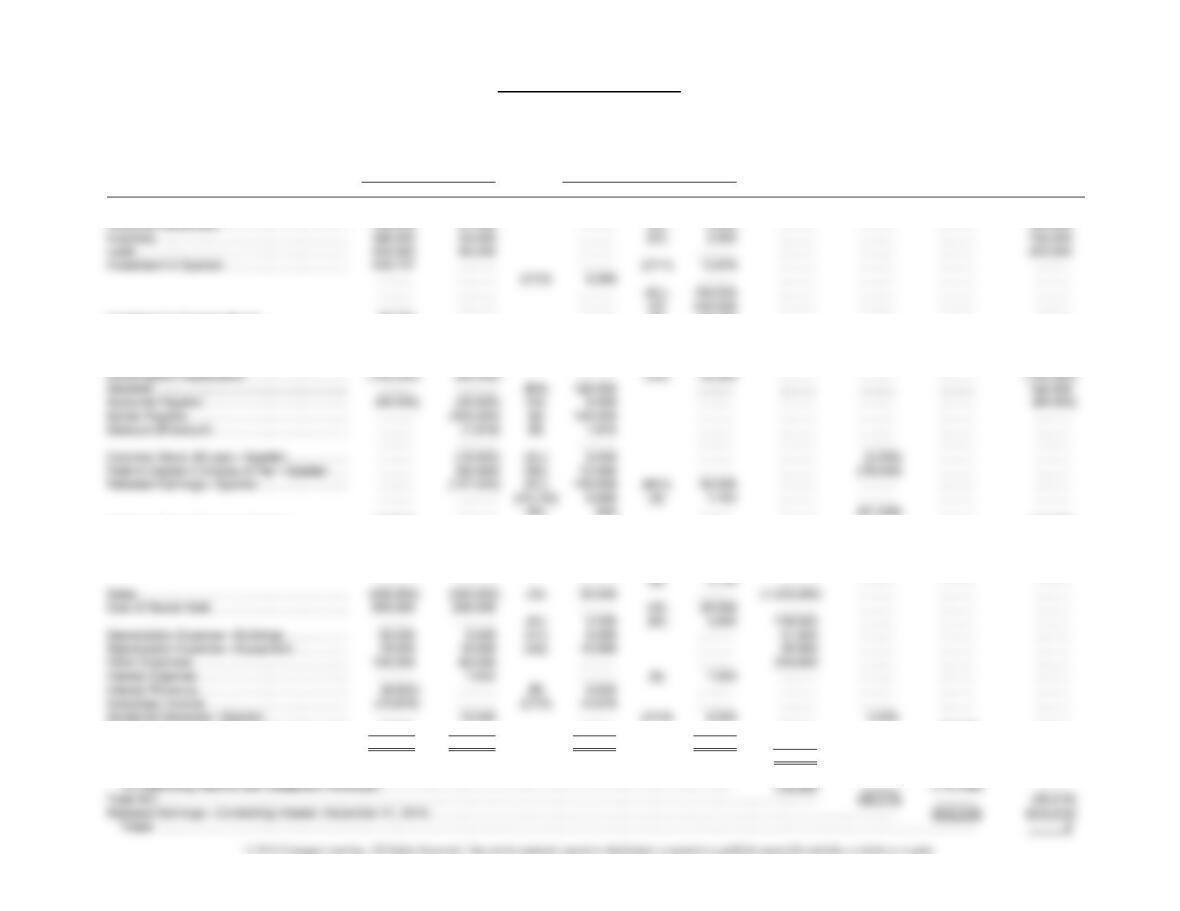

Problem 5-5, Continued

Pontiac Company and Subsidiary Stark Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Pontiac Stark Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 49,150 61,031 ……….. ……….. ……….. ……….. ……….. 110,181

Investment in Stark Bonds ………………………… 103,180 ………… ……….. (B) 103,180 ……….. …..…… ……….. ………..

Buildings ………………………………………………… 500,000 250,000 (D1) 80,000 ……….. ……….. ……….. ……….. 830,000

Accumulated Depreciation ………………………… (330,000) (80,000) ……….. (A1) 12,000 ……….. ……….. ……….. (422,000)

Equipment ………………………………………………. 200,000 120,000 (D2) 50,000 ……….. ……….. ..……… ……….. 370,000

Paid-In Capital in Excess of Par—Pontiac …… (600,000) ………… ……….. ……….. ……….. ……….. ……….. (600,000)

Retained Earnings—Pontiac ……………………… (442,223) ………… (A1–A2) 22,400 ……….. ……….. ……….. ……….. ………..

……….. ………… (BI) 6,000 ……….. ……….. ……….. (409,330) ………..

……….. ………… (B) 4,493 ……….. ……….. ……….. ……….. ………..

Totals …………………………………………………. 0 0 766,396 766,396 ……….. ……….. ……….. ………..

Consolidated Net Income ………………………………………………………………………………………….………………………………………. (75,140) ……….. ……….. ………..

To NCI (see distribution schedule) ……………………………………………………………………………………………………………….…. 3,759 (3,759) ……….. ………..

To Controlling Interest (see distribution schedule)…………………………………………………………………………………………….. 71,381 ………… (71,381) ………..

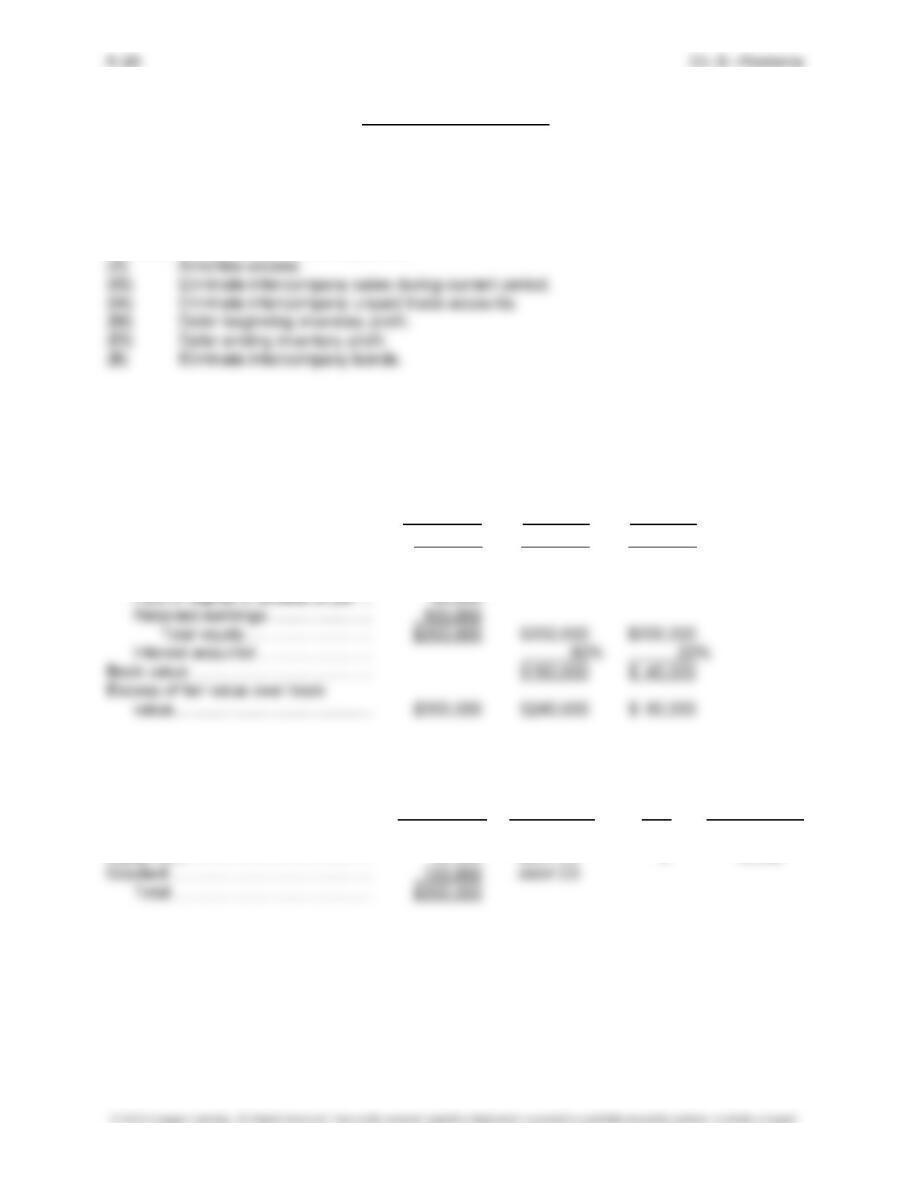

Problem 5-5, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

(EL) Eliminate controlling interest in subsidiary equity.

(D)/(NCI) Distribute excess and adjust NCI.

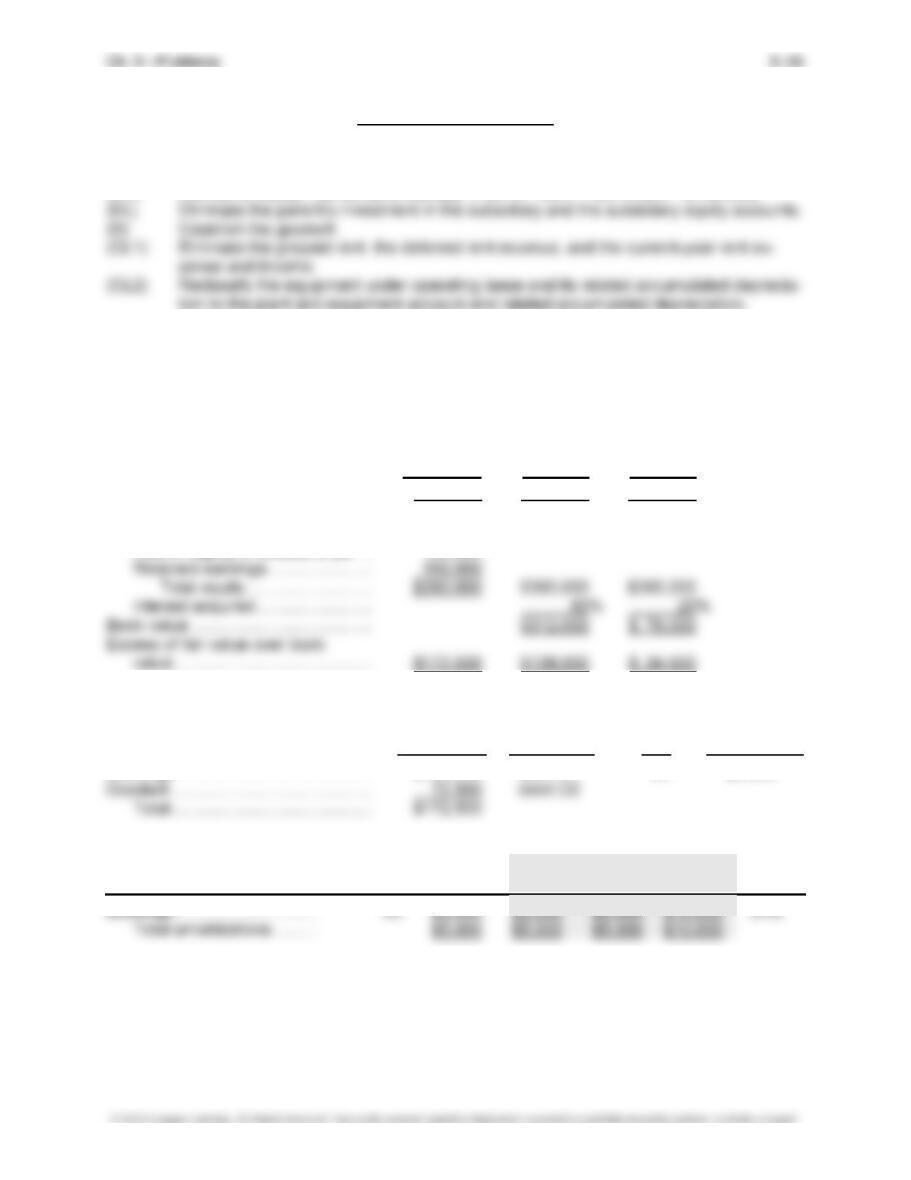

PROBLEM 5-6

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $500,000 $400,000 $100,000

Less book value of interest acquired:

Common stock ($1 par) …………… $ 10,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Buildings ……………………………………. $130,000 debit D1 20 $ 6,500

Equipment ………………………………….. 50,000 debit D2 5 10,000

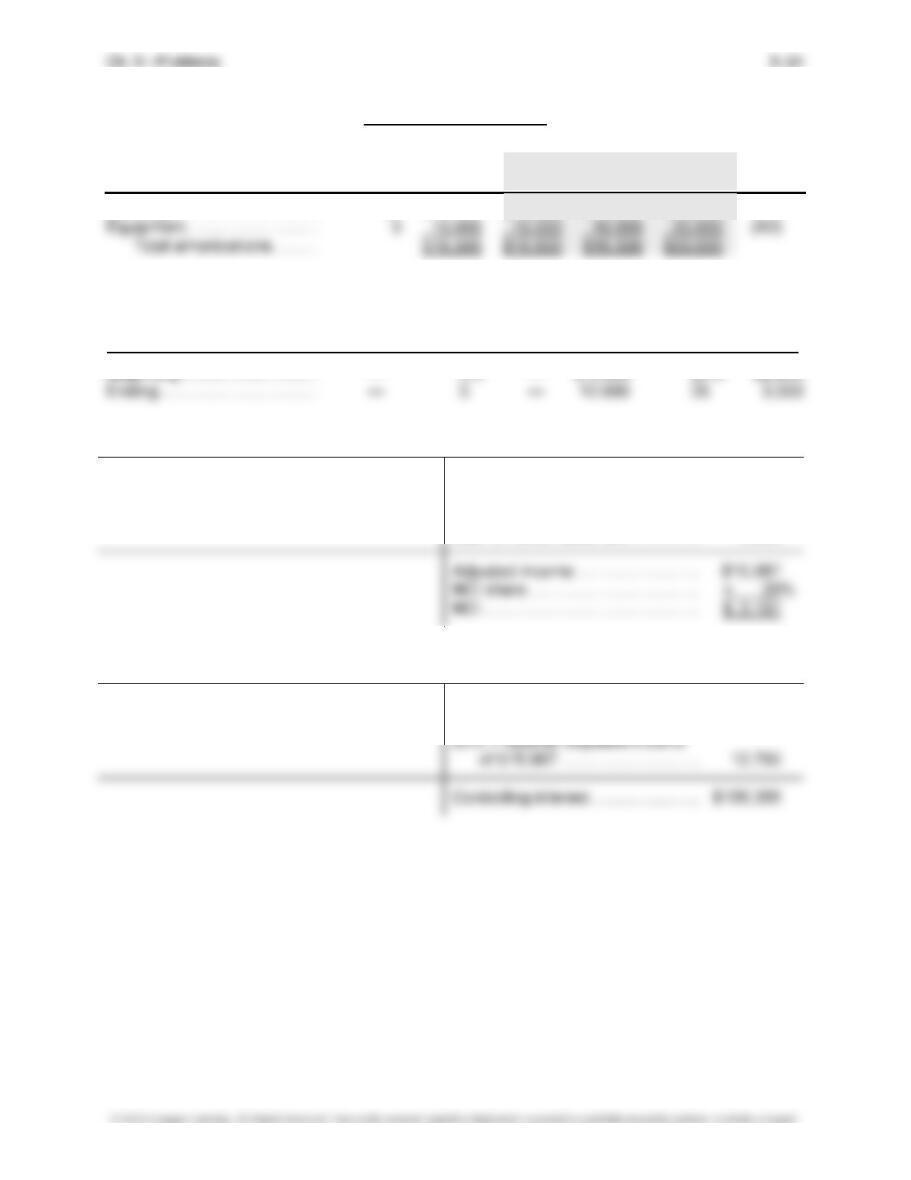

Problem 5-6, Continued

Account Adjustments Annual Current Prior

to Be Amortized Life Amount Year Years Total Key

Buildings …………………………. 20 $ 6,500 $ 6,500 $ 6,500 $13,000 (A1)

Intercompany Inventory Profit Deferral

Parent Parent Parent Sub Sub Sub

Amount Percent Profit Amount Percent Profit

Beginning ………………………… — 0% — $ 9,000 25% $2,250

Subsidiary Spartan Company Income Distribution

Amortizations ………………………… $16,500 Internally generated net

Ending inventory profit ……………. 3,000 income ………………………………. $27,324

Interest adjustment, bonds ………. 920 Beginning inventory profit …………. 2,250

Gain on bond retirement …………… 6,833

Parent Postman Company Income Distribution

Internally generated net

income ………………………………. $173,596

5–25 Ch. 5—Problems

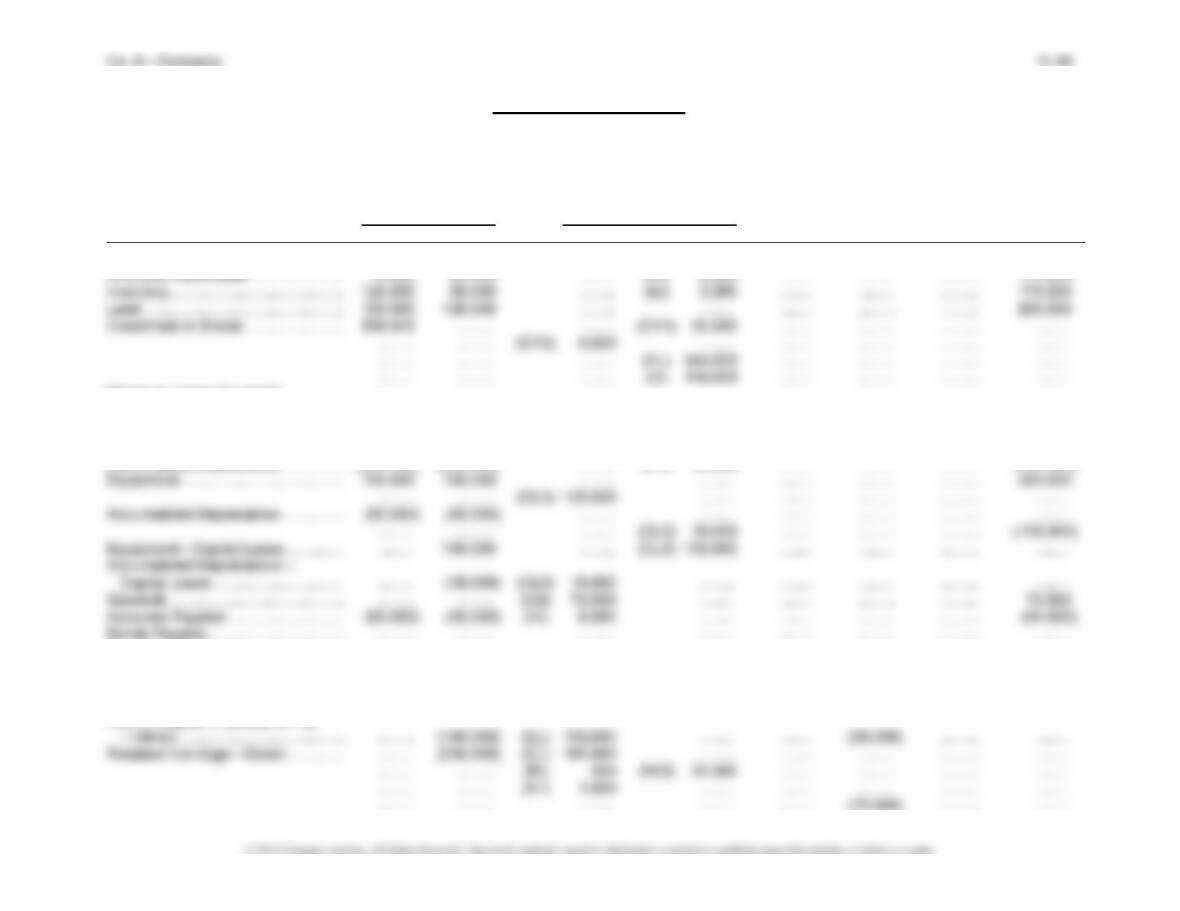

Problem 5-6, Continued

Postman Company and Subsidiary Spartan Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2015

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Postman Spartan Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 144,486 99,347 ……….. ……….. ……….. ……….. ……….. 243,833

Investment in Spartan Bonds …………………….. 96,110 ………… ……….. (B) 96,110 ……….. ……….. ……….. ………..

Buildings ………………………………………………… 600,000 100,000 (D1) 130,000 ……….. ……….. ……….. ……….. 830,000

Accumulated Depreciation ………………………… (310,000) (40,000) ……….. (A1) 13,000 ……….. ……….. ……….. (363,000)

Equipment ………………………………………………. 150,000 80,000 (D2) 50,000 ……….. ……….. ……….. ……….. 280,000

Common Stock ($1 par)—Postman ……………. (100,000) ………… ……….. ……….. ……….. ……….. ……….. (100,000)

Paid-In Capital in Excess of Par—Postman …. (800,000) ………… ……….. ……….. ……….. ……….. ……….. (800,000)

Retained Earnings—Postman ……………………. (300,000) ………… (A1–A2) 13,200 ……….. ……….. …..…… ……….. ………..

……….. ………… (BI) 1,800 ……….. ……….. ……….. (285,000) ………..

Dividends Declared—Postman ………………….. 20,000 ………… ………… ………… ……….. ……….. 20,000 ………..

Totals …………………………………………………. 0 0 681,728 681,728 ………… ……….. ……….. ………..

Consolidated Net Income ………………………………………………………………………………………….………………………………………. (189,583) ……….. ……….. ………..

To NCI (see distribution schedule) ……………………………………………………………………………………………………………….…. 3,197 (3,197) ……….. ………..

Problem 5-6, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

(EL) Eliminate controlling interest in subsidiary equity.

Proof for Bond Retirement

Gain remaining at year-end:

Carrying value at December 31, 2015 ………………………………… $102,023

Investment in bonds at December 31, 2015 ………………………… 96,110 $5,913

PROBLEM 5-7

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $500,000 $400,000 $100,000

Less book value of interest acquired:

Common stock ($1 par) …………… $ 10,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Buildings ……………………………………. $130,000 debit D1 20 $ 6,500

Equipment ………………………………….. 50,000 debit D2 5 10,000

Account Adjustments Annual Current Prior

to Be Amortized Life Amount Year Years Total Key

Buildings …………………………. 20 $ 6,500 $ 6,500 $13,000 $19,500 (A1)

Problem 5-7, Continued

Intercompany Inventory Profit Deferral

Parent Parent Parent Sub Sub Sub

Amount Percent Profit Amount Percent Profit

Subsidiary Spartan Company Income Distribution

Amortizations ………………………… $16,500 Internally generated net

Ending inventory profit ……………. 2,500 income ………………………………. $17,348

Interest adjustment, bonds ………. 998 Beginning inventory profit …………. 3,000

Parent Postman Company Income Distribution

Internally generated net

income ………………………………. $178,650

5–29 Ch. 5—Problems

Problem 5-7, Continued

Postman Company and Subsidiary Spartan Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Postman Spartan Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 290,486 99,347 ……….. ……….. ……….. ……….. ……….. 389,833

Investment in Spartan Bonds …………………….. 96,760 ………… ……….. (B) 96,760 ……….. ……….. ……….. ………..

Buildings ……………………………………………….. 600,000 100,000 (D1) 130,000 ……….. ……….. ……….. ……….. 830,000

Accumulated Depreciation ………………………… (340,000) (45,000) ……….. (A1) 19,500 ……….. ……….. ……….. (404,500)

Equipment ………………………………………………. 150,000 80,000 (D2) 50,000 ……….. ……….. ……….. ……….. 280,000

Common Stock ($1 par)—Postman ……………. (100,000) ………… ……….. ……….. ……….. ……….. ……….. (100,000)

Paid-In Capital in Excess of Par—Postman …. (800,000) ………… ……….. ……….. ……….. ……….. ……….. (800,000)

Retained Earnings—Postman ……………………. (475,455) ………… (A1–A2) 26,400 ……….. ……….. …..…… ……….. ………..

……….. ………… (BI) 2,400 ……….. ……….. ……….. (451,385) ………..

Dividends Declared—Postman ………………….. 20,000 ………… ……….. ……….. ……….. ……….. 20,000 ………..

Totals …………………………………………………. 0 0 708,062 708,062 ……….. ……….. ……….. ………..

Consolidated Net Income ………………………………………………………………………………………….………………………………………. (179,000) ……….. ……….. ………..

To NCI (see distribution schedule) ……………………………………………………………………………………………………………….…. 70 (70) ……….. ………..

Problem 5-7, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

(EL) Eliminate controlling interest in subsidiary equity.

(D)/(NCI) Distribute excess and adjust NCI.

Proof:

Gain remaining at year-end:

Carrying value at December 31, 2016 ………………………………… $101,675

Investment in bonds at December 31, 2016 ………………………… 96,760 $4,915

PROBLEM 5-8

(1) (a) $10,000 decrease in income. The $15,000 gain is eliminated. Depreciation expense is

reduced by ⅓ of the gain, $5,000.

(2) a – 1

b – 2 Elimination of the intercompany sale reduces cost of that asset.

c – 5

d – 2 50% of the bonds are treated as retired when consolidating.

PROBLEM 5-9

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (90%) (10%)

Fair value of subsidiary ………………… $750,000 $675,000 $ 75,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Goodwill …………………………………….. $150,000 debit D

Subsidiary Sundown Company Income Distribution

Interest adjustment Internally generated net

($10,702 – $9,621) ……………. $1,081 income …………………………….. $8,758

Realized equipment gain ………… 2,000

Problem 5-9, Continued

Princess Company and Subsidiary Sundown Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Princess Sundown Dr. Cr. Statement NCI Earnings Sheet

Inventory ………………………………………… 25,000 80,000 ………. (EI) 6,000 ……… ………. ………. 99,000

Equipment ………………………………………. 371,190 1,522,413 ………. (F1) 10,000 ……… ………. ………. 1,883,603

Bonds Payable (9%) ………………………… ………. (200,000) (B) 100,000 ………. ……… ………. ………. (100,000)

Discount on Bonds Payable ………………. ………. 6,345 ………. (B) 3,173 ……… ………. ………. 3,172

Common Stock ($10 par)—

Princess ………………………………………. (200,000) ………. ………. ………. ……… …..….. ………. (200,000)

Paid-In Capital in Excess of Par—

………. ………. (F1) 600 (NCI) 15,000 ……… (65,102) ………. ……….

Sales ……………………………………………… (300,000) (260,000) (IS) 50,000 ………. (510,000) …….... ………. ……….

Cost of Goods Sold ………………………….. 100,000 72,000 (EI) 6,000 (IS) 50,000 128,000 ………. ………. ……….

Interest Income ……………………………….. (10,702) ………. (B) 10,702 ………. ……… ………. ………. ……….

Other Expenses ………………………………. 150,000 160,000 ………. (F2) 2,000 308,000 ………. ………. ……….

Problem 5-9, Concluded

Eliminations and Adjustments:

(F1) Reduce machine to cost to consolidated entity. Unrecognized gain of $6,000 remain-

ing at beginning of year is split 90% to controlling retained earnings and 10% to NCI

retained earnings.

(F2) Reduce current-year depreciation expense due to sale of machine, $10,000 ÷ 5 years

= $2,000.

(B) Eliminate intercompany interest revenue and expense. Eliminate the balance in the

investment in bonds against the bonds payable. The gain on retirement at the start of

5–35 Ch. 5—Problems

PROBLEM 5-10

Paratec Corporation and Subsidiary Sym Corporation

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2018

Consolidated Controlling Consolidated

Trial Balance

Eliminations and Adjustments Income Retained Balance

Paratec Sym Dr. Cr. Statement Earnings Sheet

Cash …………………………………………. 190,000 40,000 …………. …………. …………. ………… 230,000

Accounts Receivable (net) …………… 738,350 142,000 …………. …………. …………. ………… 880,350

…………. ………… …………. (D) 50,000 …………. ………… …………

Land …………………………………………. 250,000 85,000 …………. …………. …………. ………… 335,000

Plant and Equipment …………………… 1,950,000 295,000 (CL2) 120,000 …………. …………. ………… 2,365,000

Accumulated Depreciation—

Plant and Equipment ……………….. (250,000) (60,000) …………. (CL2) 36,000 …………. ………… (346,000)

Equipment Under Operating Lease .. 120,000 ………… …………. (CL2) 120,000 …………. ………… …………

—Sym ……………………………………. …………. (310,000) (EL) 310,000 …………. …………. ………… …………

Sales ………………………………………… (4,720,000) (500,000) …………. …………. (5,220,000) ………… …………

Rental Income ……………………………. (12,000) ………… (CL1) 12,000 …………. …………. …….….. …………

Cost of Goods Sold …………………….. 3,068,000 300,000 …………. …………. 3,368,000 ………… …………

Rent Expense …………………………….. …………. 12,000 …………. (CL1) 12,000 …………. ………… …………

Problem 5-10, Concluded

Eliminations and Adjustments:

(CV) Convert to equity method as of January 1, 2018, 100% × ($310,000 – $150,000).

PROBLEM 5-11

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $562,500 $450,000 $112,500

Less book value of interest acquired:

Common stock ($1 par) …………… $ 10,000

Paid-in capital in excess of par … 190,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Buildings ……………………………………. $100,000 debit D1 20 $5,000

Account Adjustments Annual Current Prior

to Be Amortized Life Amount Year Years Total Key

Problem 5-11, Continued

Intercompany Inventory Profit Deferral

Parent Parent Parent Sub Sub Sub

Amount Percent Profit Amount Percent Profit

Beginning ………………………… — 0% — $10,000 25% $2,500

Ending …………………………….. — 0 — 12,000 25 3,000

Subsidiary Simon Company Income Distribution

Ending inventory profit ……………. $3,000 Internally generated net

Amortization ………………………….. 5,000 income ………………………………. $40,804

Beginning inventory profit …………. 2,500

Problem 5-11, Continued

Press Company and Subsidiary Simon Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Press Simon Dr. Cr. Statement NCI Earnings Sheet

Cash …………………………………………. 72,363 73,637 ……… ……… …….. ……… ……... 146,000

Minimum Lease Payments

Receivable ……………………………… 103,452 ……… ……… (CL2) 103,452 …….. ……… ……... ……..

Unearned Interest ………………………. (17,619) ……… (CL2) 17,619 ……… …….. ……… ……... ……..

Buildings …………………………………… 800,000 400,000 (D1) 100,000 ……… …….. ……… ……… 1,300,000

Accumulated Depreciation …………… (220,000) (220,000) ……… (A1) 10,000 …….. ……… ……… (450,000)

Discount (Premium) ……………………. ……… ……… ……… ……… …….. ……… ……… ……..

Obligation Under Capital Lease ……. ……… (76,637) (CL2) 76,637 ……… …….. ……… ……… ……..

Accrued Interest—Capital Lease ….. ……… (9,196) (CL2) 9,196 ……… …….. ……… ……… ……..

Common Stock ($1 par)—Simon ….. ……… (10,000) (EL) 8,000 ……… …….. (2,000) ……… ……..

Paid-In Capital in Excess of Par

5–39 Ch. 5—Problems

Problem 5-11, Continued

Press Company and Subsidiary Simon Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

(Concluded)

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Press Simon Dr. Cr. Statement NCI Earnings Sheet

Common Stock ($1 par)—Press …… (100,000) ……… ……… ……… …….. ……… ……… (100,000)

Paid-In Capital in Excess of Par

Cost of Goods Sold …………………….. 450,000 240,000 ……… (IS) 40,000 …….. ……… ……… ……..

……… ……… (EI) 3,000 (BI) 2,500 650,500 ……… ……… ……..

Depreciation Expense—Buildings …. 30,000 10,000 (A1) 5,000 ……… 45,000 ……… ……… ……..

Depreciation Expense—Equipment 15,000 28,000 ……… ……… …….. ……… ……… ……..

……… ……… ……… ……… 43,000 ……… ……… ……..

Other Expenses …………………………. 140,000 72,000 ……… ……… 212,000 ……… ……… ……..

Interest Expense ………………………… ……… 9,196 ……… (CL1) 9,196 …….. ……… ……… ……..

Interest Revenue ………………………… (9,196) ……… (CL1) 9,196 ……… …….. ……… ……… ……..

Ch. 5—Problems 5–40

Problem 5-11, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

(EL) Eliminate controlling interest in subsidiary equity.

(D)/(NCI) Distribute excess.

(A) Amortize excess.