Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 05 - Receivables and Sales

5-1

Chapter 5

Receivables and Sales

INSTRUCTOR’S MANUAL

Learning Objectives

LO5-1 Recognize accounts receivable.

LO5-2 Calculate net revenues using discounts, returns, and allowances.

LO5-3 Record an allowance for future uncollectible accounts.

LO5-4 Use the aging method to estimate future uncollectible accounts.

LO5-5 Apply the procedure to write off accounts receivable as uncollectible.

LO5-6 Contrast the allowance method and direct write-off method when accounting

for uncollectible accounts.

LO5-7 Account for notes receivable and interest revenue.

Analysis

LO5-8 Calculate key ratios investors use to monitor a company’s effectiveness in managing

receivables.

Appendix

LO5-9 Estimate uncollectible accounts using the percentage-of-credit-sales method.

Chapter 05 - Receivables and Sales

5-2

Teaching Suggestions

Chapter 5 uses a hospital theme because of the high amounts of receivables and uncollectible

accounts in the industry.

Part A begins with the concept of credit sales (or sales on account). Students should become

familiar with the idea that selling products or services on account results in revenue being

recorded even though no cash is yet received. Credit sales also create the right to collect cash

from customers, or an asset, referred to as accounts receivable. Related to credit sales, students

are introduced to recording sales discounts. Other sales-related activities are also covered (trade

discounts, sales returns, and sales allowances).

Part B addresses the main issue of the chapter, allowance for uncollectible accounts. Students

are asked to focus on the concept that accounts receivable are recorded at their net realizable

value. Consistent with this, the allowance method is covered using the percentage-of-receivables

method. It’s useful for the instructor to focus on the fact that at the time of estimating

uncollectible accounts, assets are reduced (through the allowance account) and expenses are

recorded. When the actual bad debts occur, the accounting equation remains unaffected because

the negative effects of bad debts have already been recorded. This is illustrated by walking

students through writing off an actual bad debt and then subsequently collecting on an account

previously written off. Students are also introduced to the aging method, which explains that the

collectability of a receivable is inherently linked to its age (or number of days past due).

Part C deals with notes receivable. Students are reminded that accounting for notes

receivable is similar to accounts receivable, except for interest collection, which usually

accompanies notes receivable.

The analysis section discusses the receivables turnover ratio and the average collection

period to help students understand how decision makers use receivables information. The

analysis is performed for Tenet Healthcare and LifePoint Hospitals. The analysis demonstrates

that the lower profit performance of Tenet may be linked to the company’s higher uncollectible

accounts.

For those interested in comparing the balance sheet method (percentage-of-receivables) to

the income statement method (percentage-of-credit-sales), the appendix provides an analysis.

Understanding this comparison may be helpful from a conceptual understanding that accounting

choices have real effects on amounts reported in the financial statements. However, students are

reminded that the percentage-of-credit-sales method is allowed only if the ending balance of the

allowance account is not materially different than that under the percentage-of-receivables

method. Accounts receivable must be recorded at their net realizable value, which is a balance

sheet focus.

Chapter 05 - Receivables and Sales

5-3

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

ts

s

Questions

Learning

Objective(s)

Topic

Time

(Min.)

1

LO5-1

Describe recording of a credit sale

5

2

LO5-1

Explain the difference between a trade receivable

and a nontrade receivable

5

3

LO5-2

Explain the difference between a trade discount and

a sales discount

5

4

LO5-2

Explain the accounting treatment for sales returns

and allowances

5

5

LO5-2

Provide an example of revenue earned at one point

or over time

5

6

LO5-3

Explain how companies account for uncollectible

accounts receivable

5

7

LO5-3

Understand the purposes of estimating future

uncollectible accounts

5

8

LO5-3

Relate accounting for uncollectible accounts to the

matching principle

5

9

LO5-3

Identify the financial statement effects of

accounting for uncollectible accounts

5

10

LO5-3

Describe the year-end adjustment for the allowance

for uncollectible accounts

5

11

LO5-3

Explain a debit balance in the allowance for

uncollectible accounts

5

12

LO5-3

Explain net realizable value

5

13

LO5-4

Explain the age of accounts receivable

5

14

LO5-5

Describe the entry to write off an account

5

15

LO5-5

Explain a credit balance in the allowance for

uncollectible accounts

5

16

LO5-6

Discuss the differences between the allowance

method and direct write-off method

5

17

LO5-7

Describe notes receivable

5

18

LO5-7

Explain terms related to notes receivable

5

19

LO5-7

Understand interest calculation on a note receivable

5

20

LO5-7

Describe the entry to accrue interest revenue

5

21

LO5-8

Explain the receivables turnover ratio

5

22

LO5-8

Identify the average collection period

5

23

LO5-8

Discuss the benefits of effectively managing

receivables

5

24

LO5-9

Discuss the use of the percentage-of-credit-sales

method

5

25

LO5-9

Explain the balance sheet method and income

statement method of accounting for uncollectible

accounts

5

Chapter 05 - Receivables and Sales

5-4

Brief

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

BE5-1

LO5-2

Record accounts receivable and trade discount

5

BE5-2

LO5-2

Calculate net sales

5

BE5-3

LO5-3

Record the adjustment for uncollectible accounts

BE5-4

LO5-3

Record the adjustment for uncollectible accounts

5

BE5-5

LO5-3

Record the adjustment for uncollectible accounts

5

BE5-6

LO5-3

Record the adjustment for uncollectible accounts

BE5-7

LO5-3

Record the adjustment for uncollectible accounts

10

BE5-8

LO5-4

Calculate uncollectible accounts using the aging

method

5

BE5-9

LO5-4

Calculate uncollectible accounts using the aging

method

5

BE5-10

LO5-5

Record the write-off of uncollectible accounts

5

BE5-11

LO5-5

Record collection of account previously written off

5

BE5-12

LO5-6

Use the direct write-off method to account for

uncollectible accounts

10

BE5-13

LO5-6

Use the direct write-off method to account for

uncollectible accounts

10

BE5-14

LO5-6

Use the direct write-off method to account for

uncollectible accounts

10

BE5-15

LO5-7

Calculate amounts related to interest

10

BE5-16

LO5-7

Calculate interest revenue on notes receivable

5

BE5-17

LO5-9

Use the percentage-of-credit-sales method to adjust

for uncollectible accounts

5

BE5-18

LO5-9

Use the percentage-of–credit-sales method to adjust

for uncollectible accounts

5

BE5-19

LO5-1, 5-2,

5-3, 5-4, 5-5,

5-6, 5-7

Define terms related to receivables

15

Chapter 05 - Receivables and Sales

5-5

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

E5-1

LO5-1

Record credit sale

5

E5-2

LO5-2

Record cash sales with a trade discount

5

E5-3

LO5-1, 5-2

Record credit sale and cash collection with a sales

discount

5

E5-4

LO5-1, 5-2

Record credit sale and cash collection

5

E5-5

LO5-1, 5-2

Record credit purchase and cash payment

5

E5-6

LO5-1, 5-2

Record credit sales with a sales allowance

10

E5-7

LO5-3

Record the adjustment for uncollectible accounts

and calculate net realizable value

10

E5-8

LO5-3

Record the adjustment for uncollectible accounts

and calculate net realizable value

10

E5-9

LO5-3

Record the adjustment for uncollectible accounts

and calculate net realizable value

10

E5-10

LO5-4

Record the adjustment for uncollectible accounts

using the aging method

10

E5-11

LO5-4

Record the adjustment for uncollectible accounts

using the aging method

10

E5-12

LO5-3, 5-5

Identify the financial statement effects of

transactions related to accounts receivable and

allowance for uncollectible accounts

10

E5-13

LO5-6

Compare the allowance method and the direct write-

off method

20

E5-14

LO5-7

Record notes receivable

5

E5-15

LO5-7

Record notes receivable and interest revenue

5

E5-16

LO5-7

Record notes payable and interest expense

5

E5-17

LO5-7

Record notes receivable and interest revenue

10

E5-18

LO5-8

Calculate receivables ratios

10

E5-19

LO5-9

Compare the percentage-of-receivables method and

the percentage-of-credit-sales method

10

E5-20

LO5-9

Compare the percentage-of-receivables method and

the percentage-of-credit-sales method

10

E5-21

LO5-1, 5-3,

5-4, 5-5, 5-7,

5-8

Complete the accounting cycle using receivable

transactions

60

Chapter 05 - Receivables and Sales

5-6

Problems

Learning

Objective(s)

Topic

Time

(Min.)

P5-1A

LO5-1

Calculate the amount of revenue to recognize

10

P5-2A

LO5-1, 5-2

Record transactions related to credit sales and contra

revenues

20

P5-3A

LO5-3, 5-5

Record transactions related to accounts receivable

25

P5-4A

LO5-4, 5-5

Record transactions related to uncollectible accounts

15

P5-5A

LO5-3, 5-6

Compare the direct write-off method to the

allowance method

20

P5-6A

LO5-3

Use estimates of uncollectible accounts to overstate

income

20

P5-7A

LO5-3, 5-5

Overestimate future uncollectible accounts

20

P5-8A

LO5-7

Record long-term notes receivable and interest

revenue

10

P5-9A

LO5-8

Calculate and analyze ratios

15

P5-1B

LO5-1

Calculate the amount of revenue to recognize

10

P5-2B

LO5-1, 5-2

Record transactions related to credit sales and contra

revenues

20

P5-3B

LO5-3, 5-5

Record transactions related to accounts receivable

25

P5-4B

LO5-4, 5-5

Record transactions related to uncollectible accounts

15

P5-5B

LO5-3, 5-6

Compare the direct write-off method to the

allowance method

20

P5-6B

LO5-3

Use estimates of uncollectible accounts to

understate income

20

P5-7B

LO5-3, 5-5

Underestimate future uncollectible accounts

20

P5-8B

LO5-7

Record long-term notes receivable and interest

revenue

10

P5-9B

LO5-8

Calculate and analyze ratios

15

Additional

Perspectives

Topic

Time

(Min.)

AP5-1

Continuing Problem: Great Adventures

30

AP5-2

Financial Analysis: American Eagle Outfitters, Inc.

15

AP5-3

Financial Analysis: The Buckle, Inc.

15

AP5-4

Comparative Analysis: American Eagle Outfitters, Inc. vs. The

Buckle, Inc.

10

AP5-5

Ethics

20

AP5-6

Internet Research

30

AP5-7

Written Communication

25

AP5-8

Earnings Management

20

Chapter 05 - Receivables and Sales

5-7

Chapter Quiz Questions

The following multiple-choice questions are 10 unique quiz questions that correspond to the 10

questions at the end of each chapter. Each question covers the same learning objective but with a

little different twist. The correct answer is highlighted in bold for each item.

LO5-1

1. Which of the following transactions would result in an account receivable?

LO5-2

2. On August 4, Sanders provides services to Frederickson for $5,000, terms 3/10, n/30.

Frederickson pays for the services on August 12. What amount would Sanders record as

revenue on August 4?

LO5-2

3. Refer to the information in the previous question. What is the amount of net revenues (total

revenue minus sales discounts) as of August 12?

LO5-3

4. Suppose the balance of the allowance for uncollectible accounts at the end of the current year

is $800 (debit) before any adjustment. The company estimates future uncollectible accounts

to be $5,600. At what amount would bad debt expense be reported in the current year’s

income statement?

5-8

LO5-3

5. Suppose the balance of the allowance for uncollectible accounts at the end of the current year

is $800 (credit) before any adjustment entry. The company estimates future uncollectible

accounts to be $5,600. At what amount would bad debt expense be reported in the current

year’s income statement?

a. $800

LO5-4

6. Nija Incorporated reports the following aging schedule of its accounts receivable with the

estimated percent uncollectible. What is the total estimate of uncollectible accounts using the

aging method?

Age Group

Amount

Receivable

Estimated

Percent

Uncollectible

0-60 days

$40,000

1%

61-90 days

15,000

20%

More than 90 days past due

5,000

60%

Total

$60,000

a. $400

LO5-5

7. The effect of writing off a specific account receivable is:

LO5-6

8. Under the direct write-off method, bad debt expense is reported:

a. When an account receivable is estimated to be uncollectible.

5-9

LO5-7

9. At the beginning of the year, Dawnetta Fashions has total accounts receivable of $300,000.

By the end of the year, Dawnetta reports total credit sales of $1,500,000 and total accounts

receivable of $200,000. What is the receivables turnover ratio for Dawnetta Fashions?

LO5-8

10. On September 1, Bates Supplies borrows $30,000 from Vines Incorporated by signing an 8%

note due in 12 months. Calculate the amount of interest revenue Vines will record on

December 31, four months after the note is issued.

Chapter 05 - Receivables and Sales

5-10

Alternate Let’s Review

Problem #1

Mercy Care normally charges $200 for an annual physical exam. Currently, the company is

offering a $50 discount to expectant mothers. In addition, Mercy offers terms 2/10, n/30 to all

customers receiving services on account. The following events occur.

June 16 Mary, an expectant mother, calls to set up an appointment.

June 21 Mary visits Mercy and receives a physical exam for the discounted price.

June 27 Mary pays for her physical exam.

Required:

1. On what date should Mercy record patient revenue?

2. Record service revenue for Mercy.

3. Mercy receives Mary’s payment in full on June 27 (within the discount period). Record the

cash collection for Mercy.

4. Calculate the balance of accounts receivable and net revenue after the cash payment is

received.

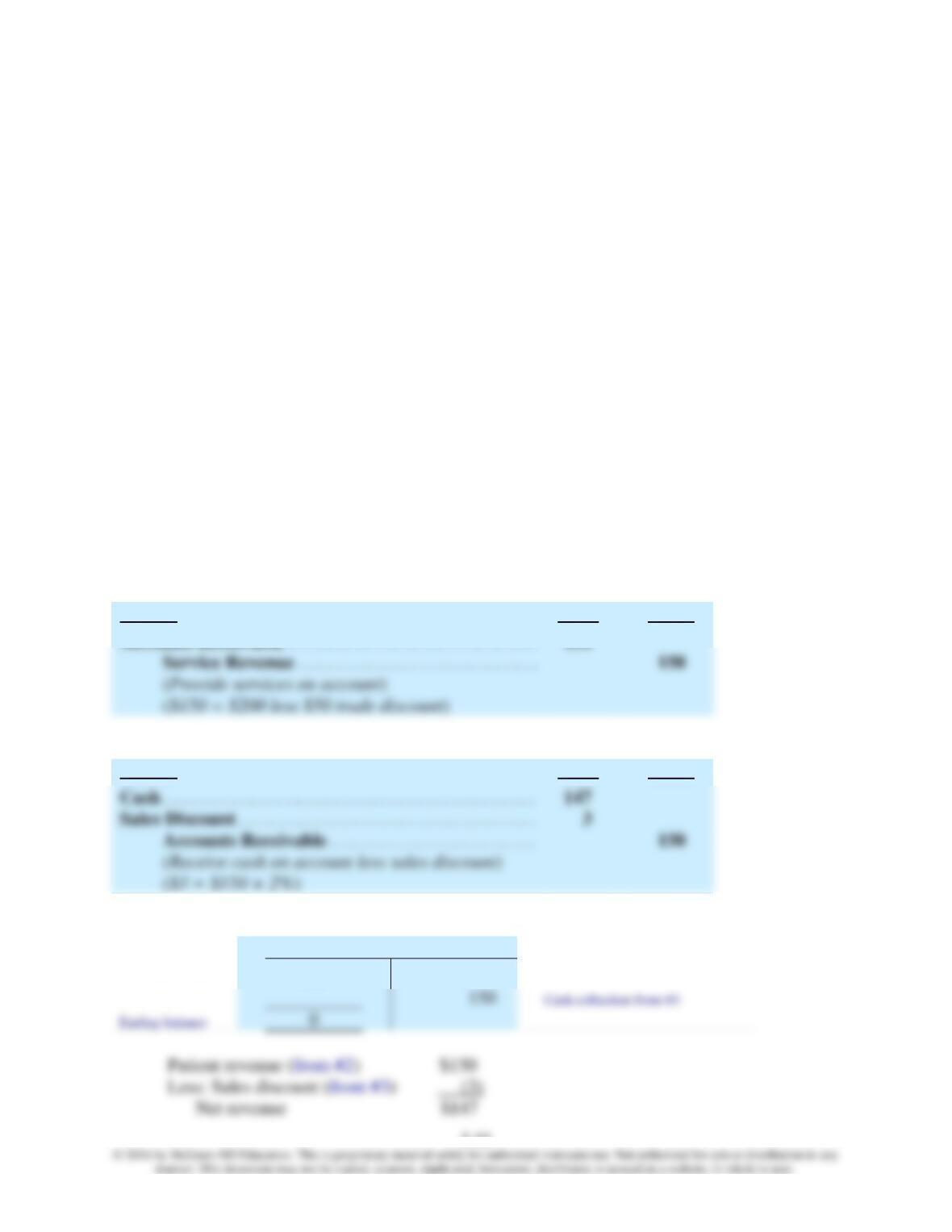

Solution:

1. June 21 – the date the service is provided.

2.

June 21

Debit

Credit

Accounts Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . .

150

3.

June 27

Debit

Credit

4.

Accounts Receivable

Credit sale from #2

150

5-11

Problem #2

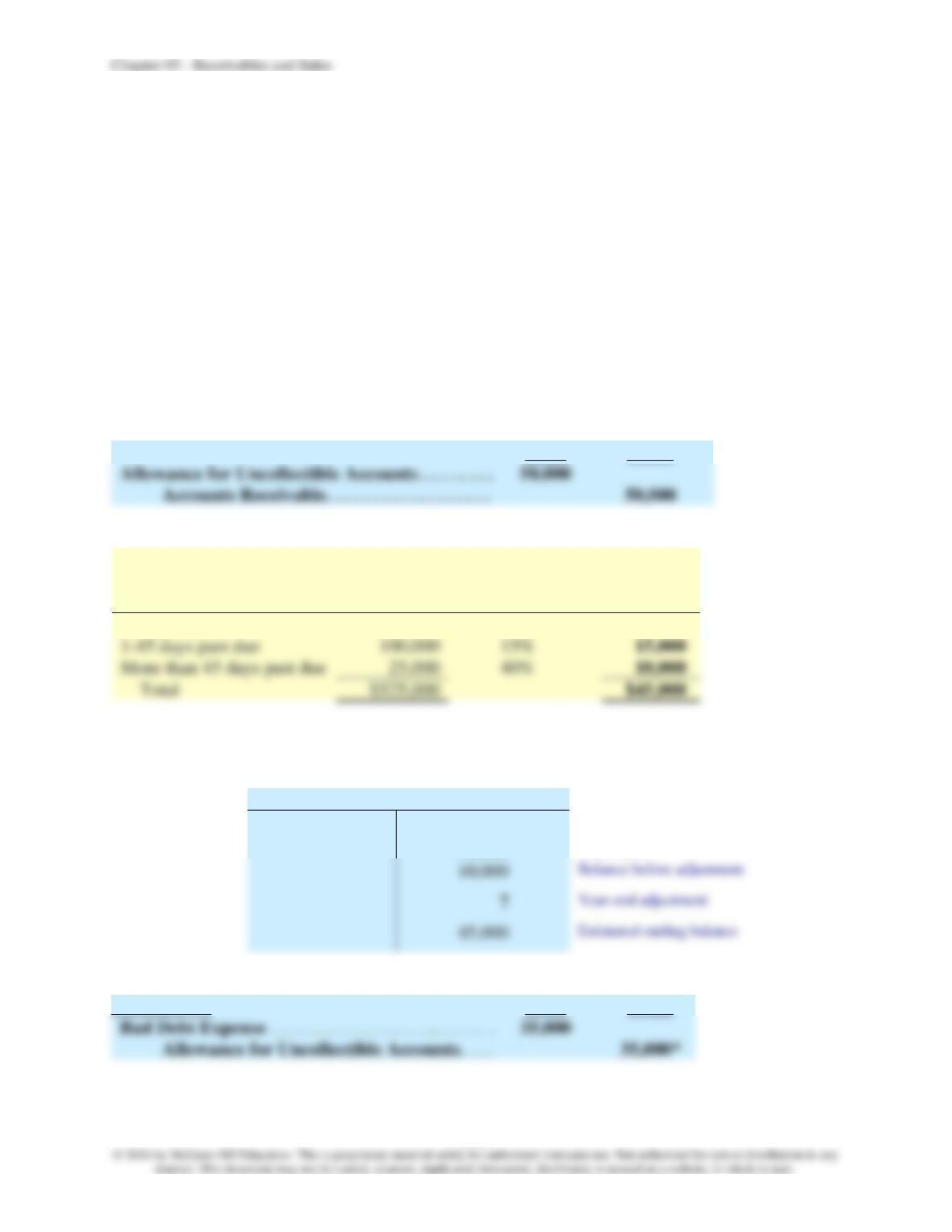

At the beginning of the year, Compassion Clinic’s allowance for uncollectible accounts has a

balance of $60,000 credit.

Required:

1. Record the write-off of $50,000 of accounts receivable during the year.

2. Estimate the allowance for future uncollectible accounts using the following ages and

estimated percentage uncollectibles at the end of the year.

3. Use a T-account to determine the year-end adjustment to the allowance account.

4. Record the year-end adjusting entry for bad debts expense.

5. Prepare a partial balance sheet showing accounts receivable and the allowance for

uncollectible accounts.

Solution:

1.

Debit

Credit

2.

Age Group

Amount

Receivable

Estimated

Percent

Uncollectible

Estimated

Amount

Uncollectible

Not yet due

$400,000

5%

$20,000

3.

Allowance for Uncollectible Accounts

60,000

Beginning balance

50,000

Write-offs

4.

December 31

Debit

Credit

Chapter 05 - Receivables and Sales

5-12

* Notice from #3 that the balance of the allowance account before adjustment is $10,000

credit. Based on the estimated allowance of $45,000 credit from #2, we need a credit

adjustment of $35,000.

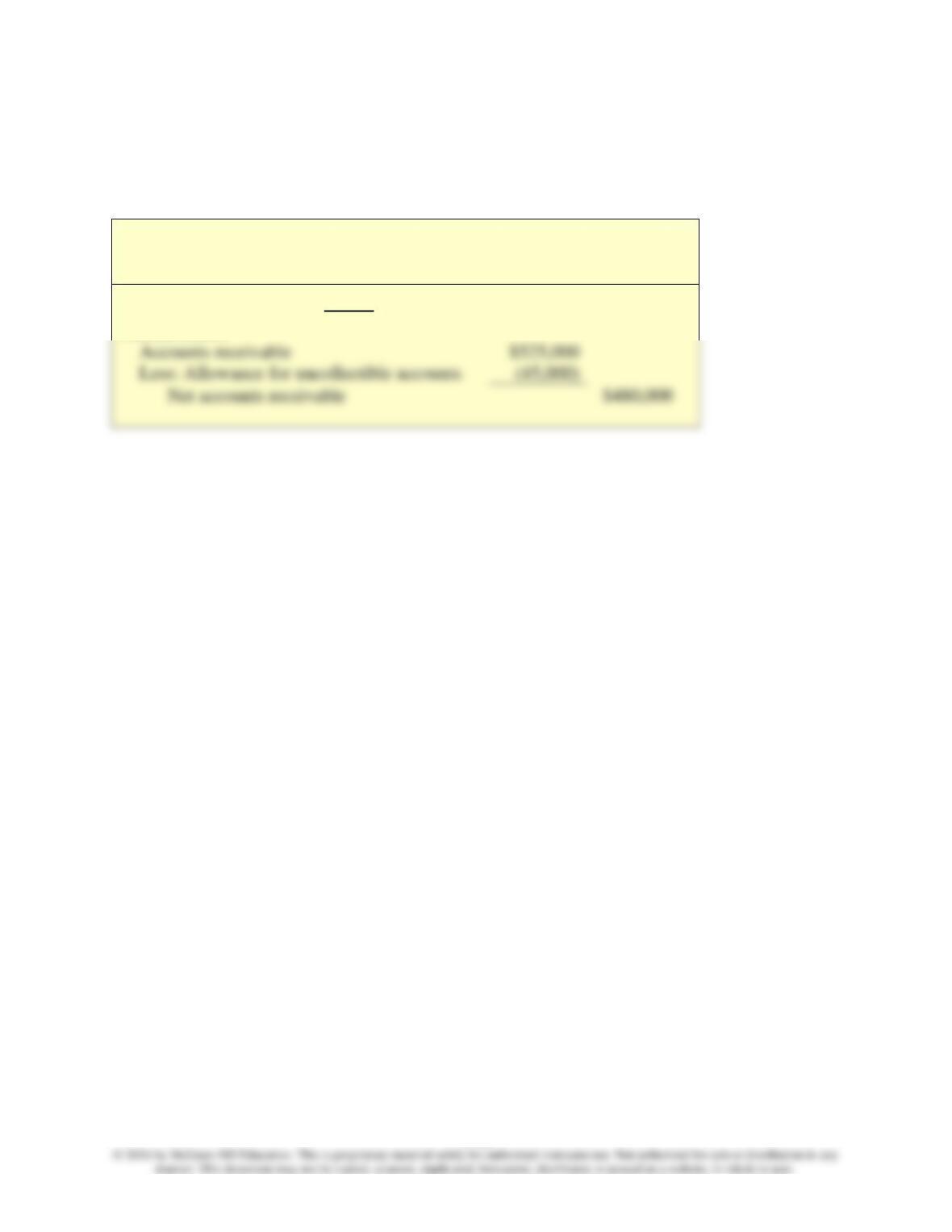

5.

Compassion Clinic

Partial Balance Sheet

December 31

Assets

Current assets:

Chapter 05 - Receivables and Sales

5-13

Problem #3

Northwest Hospital has a policy of loaning any employee up to $5,000 for a period of up to 12

months at a fixed interest rate of 12%. Clark Lewis has worked for Northwest for more than 10

years and wishes to take his family on a winter vacation to the Pacific Coast. On November 1,

2018, he borrows $5,000 from Northwest by issuing a note to be repaid in six months.

Required:

1. Record the acceptance of the note receivable by Northwest Hospital.

2. Record Northwest Hospital’s year-end adjusting entry to accrue interest revenue.

3. Record the collection of the note with interest from Clark Lewis on May 1, 2019.

Solution:

1.

November 1, 2018

Debit

Credit

2.

December 31, 2018

Debit

Credit

Interest Receivable. . . . . . . . . . . . . . . . . . . . . . . . .

100

3.

May 1, 2019

Debit

Credit

Cash. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5,300

Notes Receivable. . . . . . . . . . . . . . . . . . . . . . .

5,000

Chapter 05 - Receivables and Sales

5-14

Key Points by Learning Objective

LO5-1 Recognize accounts receivable.

LO5-2 Calculate net revenues using discounts, returns, and allowances.

LO5-3 Record an allowance for future uncollectible accounts.

We recognize accounts receivable as assets in the balance sheet and record them at

their net realizable values, that is, the amount of cash we expect to collect.

Under the allowance method, companies are required to estimate future uncollectible accounts

LO5-4 Use the aging method to estimate future uncollectible accounts.

LO5-5 Apply the procedure to write off accounts receivable as uncollectible.

Writing off a customer’s account as uncollectible reduces the balance of accounts receivable but

also reduces the contra asset—allowance for uncollectible accounts. The net effect is that there is

Chapter 05 - Receivables and Sales

5-15

LO5-6 Contrast the allowance method and direct write-off method when accounting for

uncollectible accounts.

LO5-7 Account for notes receivable and interest revenue.

Notes receivable are similar to accounts receivable except that notes receivable are formal credit

arrangements made with a written debt instrument, or note.

Analysis

LO5-8 Calculate key ratios investors use to monitor a company’s effectiveness in managing

receivables.

Appendix

LO5-9 Estimate uncollectible accounts using the percentage-of-credit-sales method.

Chapter 05 - Receivables and Sales

5-16

Common Mistakes

Common Mistake

Students sometimes misclassify contra revenue accounts—sales returns and sales allowances—

as expenses. Like expenses, contra revenues have normal debit balances and reduce the reported

amount of net income. However, contra revenues represent reductions of revenues, whereas

expenses represent the separate costs of generating revenues.

Common Mistake

Because Allowance for Uncollectible Accounts has a normal credit balance, students sometimes

Chapter 05 - Receivables and Sales

5-17

Decision Points

Question

Accounting Information

Analysis

Does a company have

a recurring problem

with customer

satisfaction?

Total sales and sales returns

and allowances

If sales returns and allowances are

routinely high relative to total sales,

this might indicate that customers are

not satisfied with the company’s

products or services.

Question

Accounting Information

Analysis

Are the company’s

credit sales policies

Accounts receivable and

the allowance for

A high ratio of the allowance for

uncollectible accounts to total

Question

Accounting Information

Analysis

How likely is it that

the company’s

accounts receivable

will be collected?

Notes to the financial

statements detailing the

age of individual accounts

receivable

Older accounts are less likely to be

collected.

Question

Accounting Information

Analysis

Is the company

effectively managing

Receivables turnover ratio and

average collection period

A high receivables turnover ratio (or

low average collection period)

Chapter 05 - Receivables and Sales

5-18

Career Corner

Career Corner

Companies that make large amounts of credit sales often employ credit analysts. These analysts

are responsible for deciding whether to extend credit to potential customers. To make this

decision, credit analysts focus on the customer’s credit history (such as delinquency in paying

bills) and information about current financial position, generally found using amounts in the

Chapter 05 - Receivables and Sales

5-19

Ethical Dilemma

Ethical Dilemma

Philip Stanton, the executive manager of Thomson Pharmaceutical, receives a bonus if the

company’s net income in the current year exceeds net income in the past year. By the end of

2018, it appears that net income for 2018 will easily exceed net income for 2017. Philip has

asked Mary Beth Williams, the company’s controller, to try to reduce this year’s income and

“bank” some of the profits for future years. Mary Beth suggests that the company’s bad debt

expense as a percentage of accounts receivable for 2018 be increased from 10% to 15%. She

believes 10% is the more accurate estimate but knows that both the corporation’s internal and

external auditors allow some flexibility in estimates. What is the effect of increasing the estimate

of bad debts from 10% to 15% of accounts receivable? How does this "bank" income for future

years? Why does Mary Beth’s proposal present an ethical dilemma?

Key Issues

• Increasing the bad debt estimate from 10% to 15% of accounts receivable increases bad

debt expense in the current year, reducing net income. If 10% ends up being the correct

estimate of future bad debts, then the company will be able to report less bad debt

expense in the following year, increasing net income in the following year. The effect of

this change in estimate is to shift profits from this year to next year.

• How do you define “accurate” reporting?

Option 1: Record the estimate of bad debts for 10% of accounts receivable

• An assumption of financial reporting is that accountants present financial information

that is reliable and accurate. Knowing that 10% is the correct percentage for bad debt

Option 2: Record the estimate of bad debts for 15% of accounts receivable

• In the long run, it is likely that the bad debt expense will smooth itself out, so a temporary

adjustment is not going to change investors’ decisions.

Chapter 05 - Receivables and Sales

5-20

• Ultimately, Mary Beth should not feel responsible for this decision to change the

percentage. Her boss is advising her on what to do, so is it worth her job to

oppose/confront him on this decision?

• We have extra profits this year, so why not hang onto them? We may need some in future