ATS–11

2018

e

d

i

t

i

o

n

PAYROLL

ACCOUNTING

Bie

g

/Toland

TEST 5

Student INSTRUCTOR’S COPY

Chapter 5 Date

SCORING RECORD

Section Total Points Deductions Score

A 40

B 30

C 30

Total 100

Section A—DIRECTIONS: Each of the following statements is either true or false. Unless directed otherwise by

your instructor, indicate your choice in the Answers column by writing “T” for a true answer or “F” for a false answer.

(2 points for each correct answer)

For

Answers Scoring

1. The federal unemployment tax is imposed on employers, and thus, is not deducted from

2. Educational assistance payments to workers are considered nontaxable wages for unemployment

5. The location of the employee’s residence is the primary factor to be considered in determining

6. A bonus paid as remuneration for services is not considered taxable wages for unemployment tax

7. In the case of an employee who changes jobs during the year, only the first employer must pay

9. If an employer pays a SUTA tax of 2.0%, the total credit that can be claimed against the FUTA

11. Employer contributions made to employees’ 401(k) plans that are included in total payments on

12. The payments of FUTA taxes are included with the payments of FICA and FIT taxes and are

14. If a business has ceased operations during the year, as long as the payments of the FUTA taxes

17. All of the states allow employers to make voluntary contributions into their state unemployment

18. Employers have to pay a FUTA tax on only the first $3,500 of each part-time employee’s earnings

19. Only employers who paid state unemployment taxes in more than one state or paid wages in a

ATS–12 Chapter 5/Achievement Test Solutions

Section B—DIRECTIONS: Determine the correct answer for each of the following problems. (5 points for

each correct answer)

Answers

For

Scoring

1. Truson Company paid a 4% SUTA tax on taxable wages of $108,500. The taxable wages

2. Jason Jeffries earned $10,200 while working for Brown Company. The company’s

SUTA tax rate is 2.9% of the first $7,000 of each employee’s earnings. Compute the

3. Caruso Company’s SUTA rate for next year is 2.9% because its reserve ratio falls in its

state’s 8% to less than 10% category [(contributions – benefits paid) ÷ average payroll =

4. Fred Stone is an employee of Henrock Company. During the first part of the year, Stone

earned $4,340 while working in State Q. For the remainder of the year, the company

transferred him to State S where he earned $27,000. Henrock Company’s tax rate in

5. Leinart Company had taxable wages (SUTA and FUTA) totaling $175,000. During the

6. Englesbe Company’s FUTA tax liability was $289.50 FUTA tax for the 1st quarter;

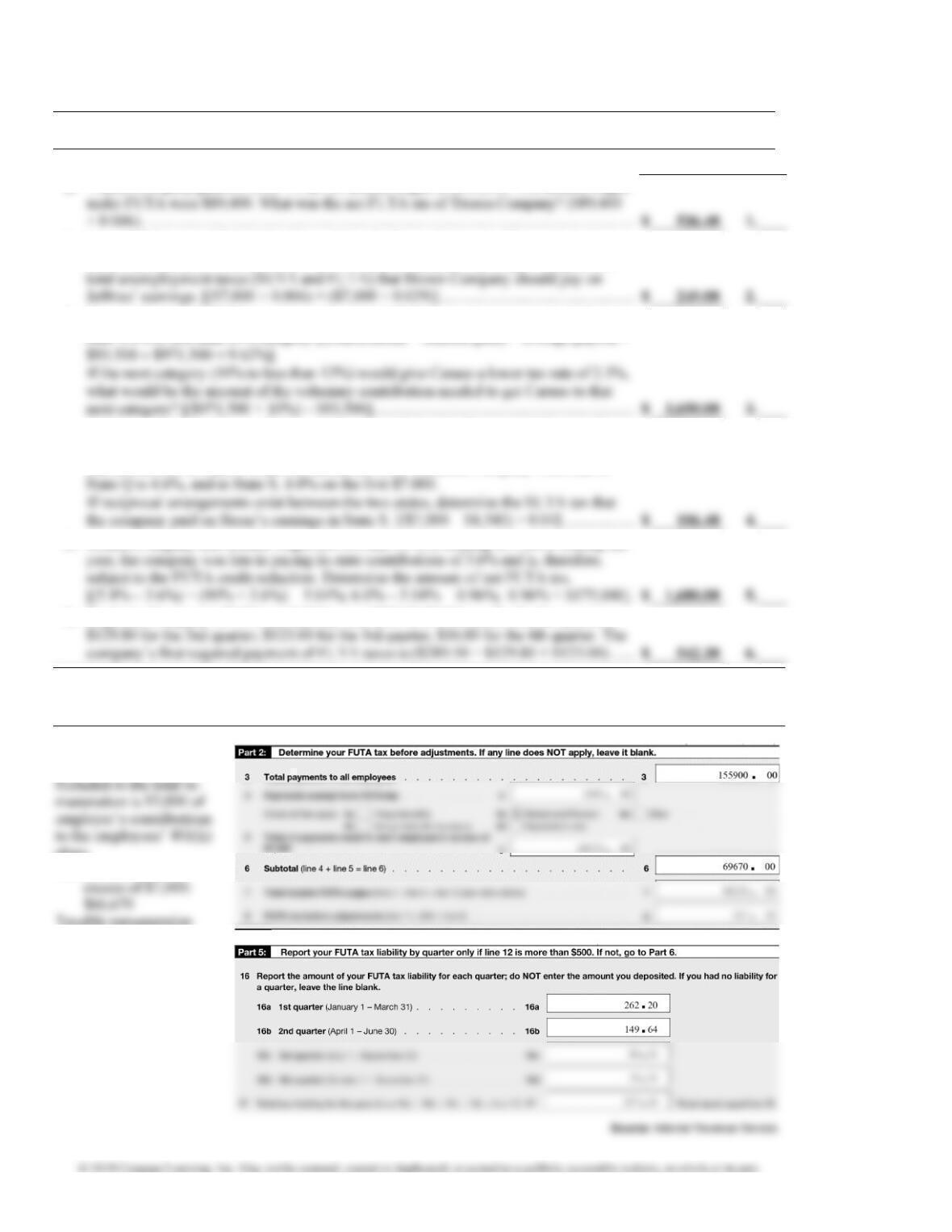

Section C—DIRECTIONS: The information given below was taken from the payroll records of Clegg Compa-

ny (Oregon employer) for 20–. Use the information to complete the partially illustrated Form 940 shown below. As-

sume that all taxes were deposited timely. (2½ points for each correct answer)

Total remuneration:

$155,900

plans.

Remuneration in

Taxable remuneration

by quarters:

1st quarter …….. $43,700

2nd quarter ……. $24,940

3rd quarter …….. $14,360

4th quarter …….. $ 3,230