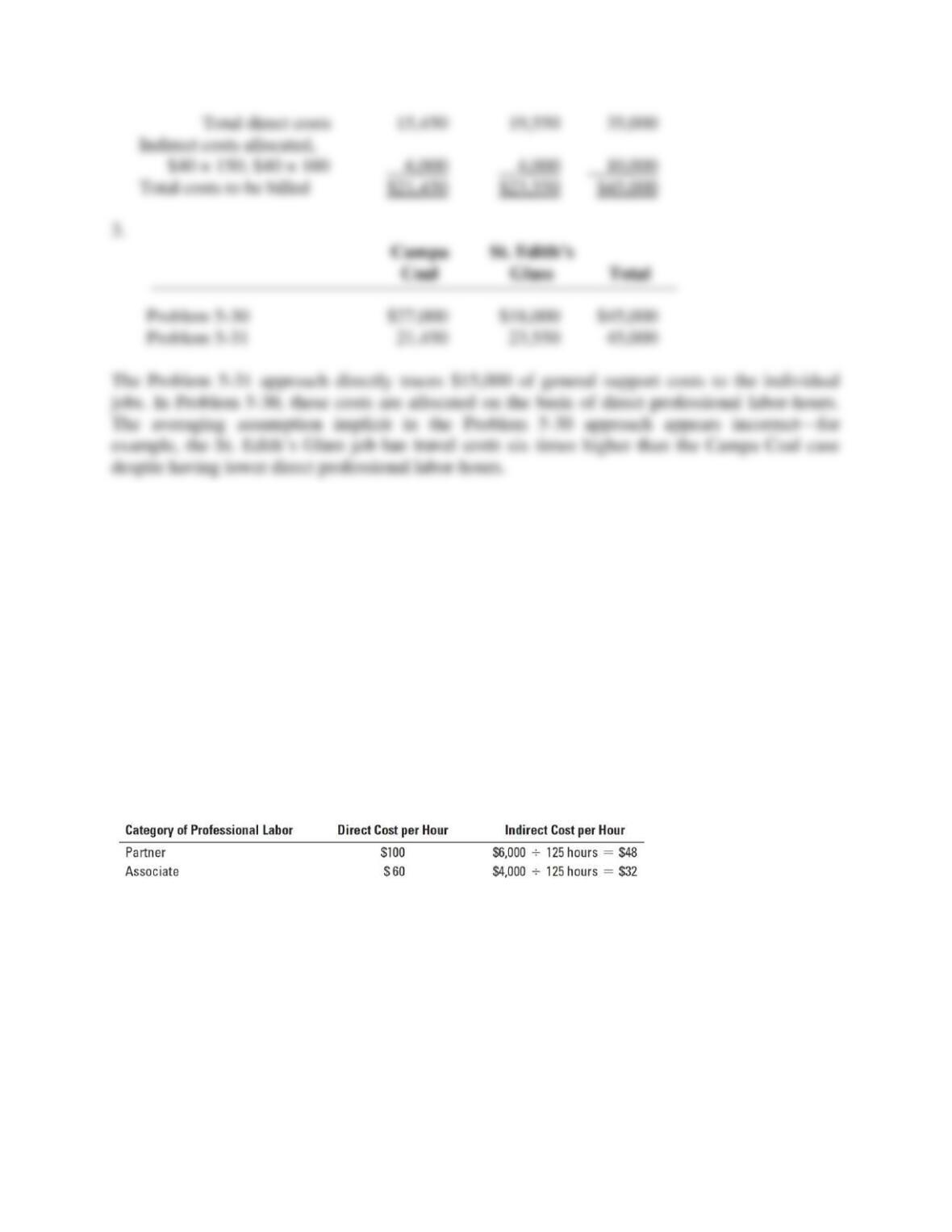

5-41

5-32 (30 min.) Job costing with multiple direct-cost categories, multiple indirect-cost

pools, law firm (continuation of 5-30 and 5-31).

Bradley has two classifications of professional staff: partners and associates. Harrington asks his

assistant to examine the relative use of partners and associates on the recent Campa Coal and St.

Edith’s jobs. The Campa job used 50 partner-hours and 100 associate-hours. The St. Edith’s job

used 75 partner-hours and 25 associate-hours. Therefore, totals of the two jobs together were 125

partner-hours and 125 associate-hours. Harrington decides to examine how using separate direct-

cost rates for partners and associates and using separate indirect-cost pools for partners and

associates would have affected the costs of the Campa and St. Edith’s jobs. Indirect costs in each

indirect-cost pool would be allocated on the basis of total hours of that category of professional

labor. From the total indirect cost-pool of $10,000, $6,000 is attributable to the activities of

partners and $4,000 is attributable to the activities of associates.

The rates per category of professional labor are as follows:

Required:

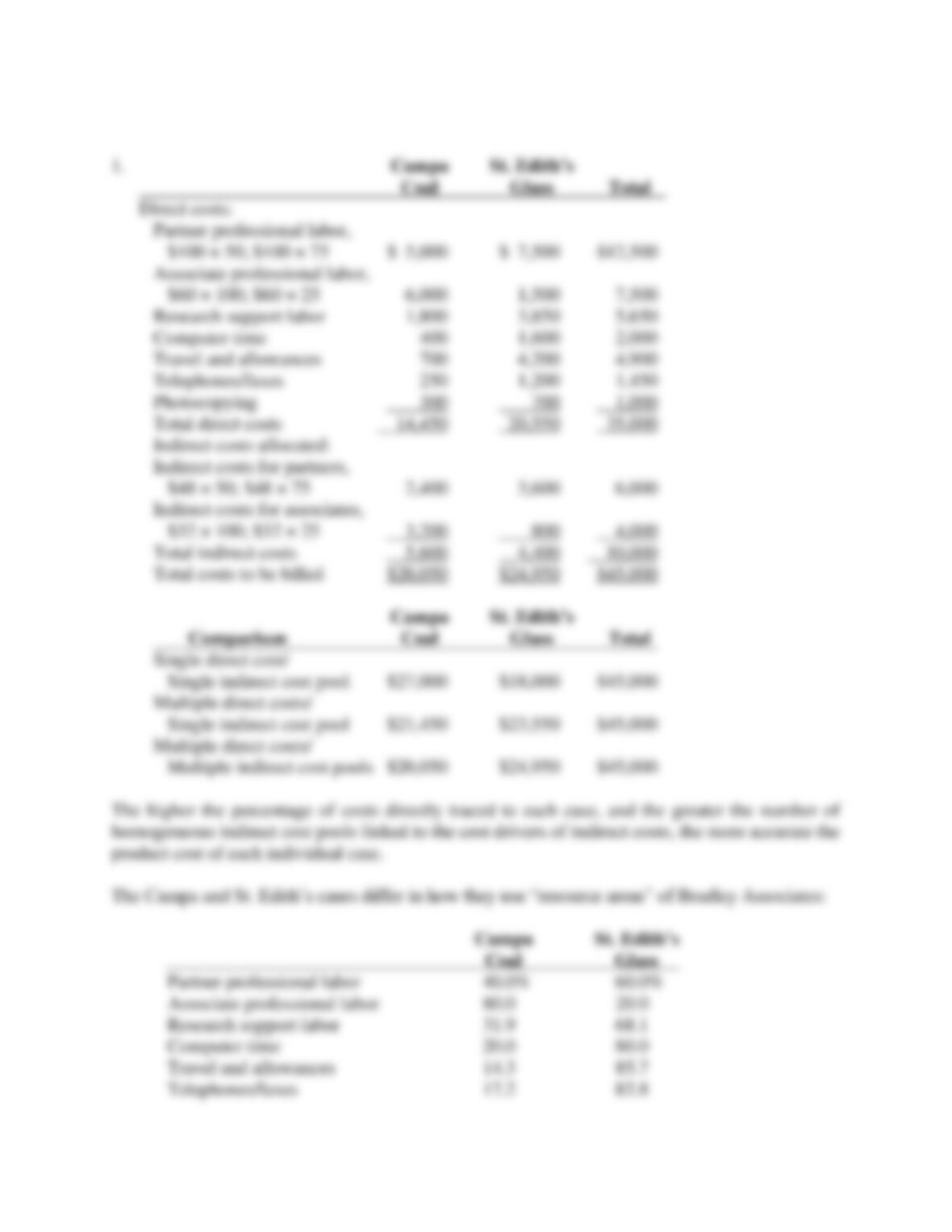

1. Compute the costs of the Campa and St. Edith’s cases using Bradley’s further refined system,

with multiple direct-cost categories and multiple indirect-cost pools.

2. For what decisions might Bradley Associates find it more useful to use this job-costing

approach rather than the approaches in Problem 5-30 or 5-31?

5-42

SOLUTION

5-43

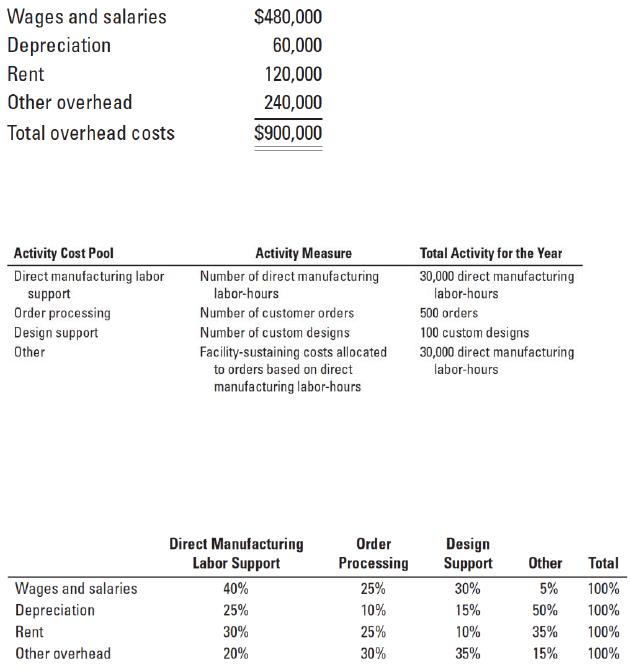

5-33 (30 min.) First stage allocation, activity-based costing, manufacturing sector.

Thurgood Devices uses activity-based costing to allocate overhead costs to customer orders for

pricing purposes. Many customer orders are won through competitive bidding. Direct material

and direct manufacturing labor costs are traced directly to each order. Thurgood’s direct

5-44

manufacturing labor rate is $20 per hour. The company reports the following yearly overhead

costs:

Thurgood has established four activity cost pools:

Only about 20% of Thurgood’s yearly orders require custom designs.

Paul Moeller, Thurgood’s controller, has prepared the following estimates for distribution of

the over- head costs across the four activity cost pools:

Order 448200 required $4,550 of direct materials, 80 direct manufacturing labor-hours, and one

custom design.

Required:

1. Allocate the overhead costs to each activity cost pool. Calculate the activity rate for each

pool.

2. Determine the cost of Order 448200.

3. How does activity-based costing enhance Thurgood’s ability to price its orders? Suppose

Thurgood used a traditional costing system to allocate all overhead costs to orders on the

basis of direct manufacturing labor-hours. How might this have affected Thurgood’s pricing

decisions?

5-45

SOLUTION

5-46

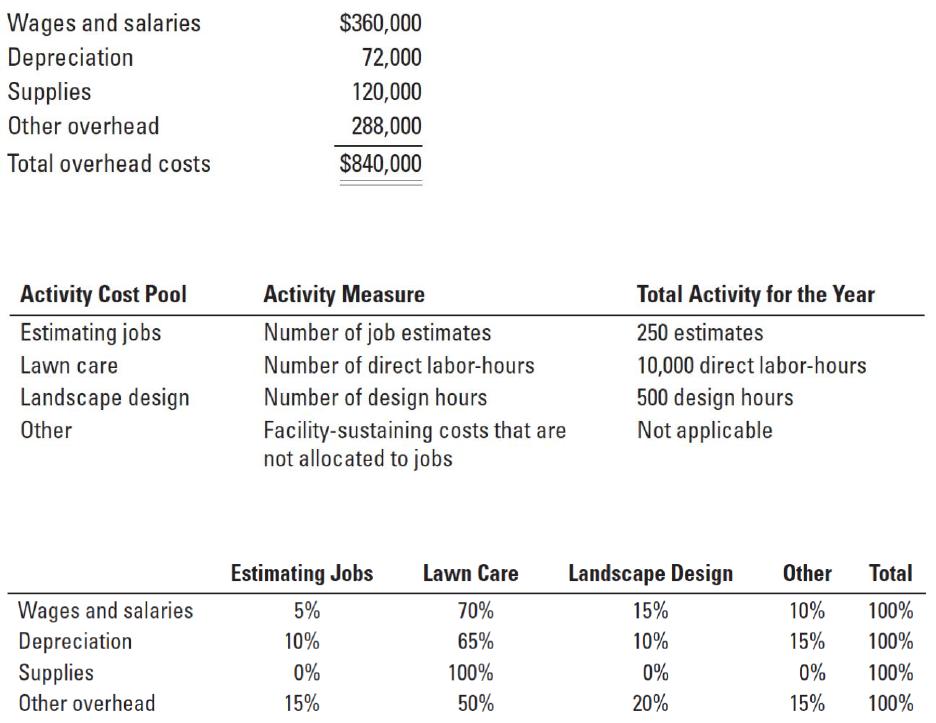

5-34 (30 min.) First stage allocation, activity-based costing, service sector.

LawnCare USA provides lawn care and landscaping services to commercial clients. LawnCare

USA uses activity-based costing to bid on jobs and to evaluate their profitability. LawnCare

USA reports the following annual costs:

John Gilroy, controller of LawnCare USA, has established four activity cost pools:

Gilroy estimates that LawnCare USA’s costs are distributed to the activity-cost pools as follows:

Sunset Office Park, a new development in a nearby community, has contacted LawnCare USA to

provide an estimate on landscape design and annual lawn maintenance. The job is estimated to

require a single landscape design requiring 40 design hours in total and 250 direct labor-hours

annually. LawnCare USA has a policy of pricing estimates at 150% of cost.

Required:

1. Allocate LawnCare USA’s costs to the activity-cost pools and determine the activity rate for

each pool.

2. Estimate total cost for the Sunset Office Park job.

3. How much should LawnCare USA bid to perform the job?

4. Sunset Office Park asks LawnCare USA to give an estimate for providing its services for a 2-

year period. What are the advantages and disadvantages for LawnCare USA to provide a 2-

year estimate?

5-47

SOLUTION

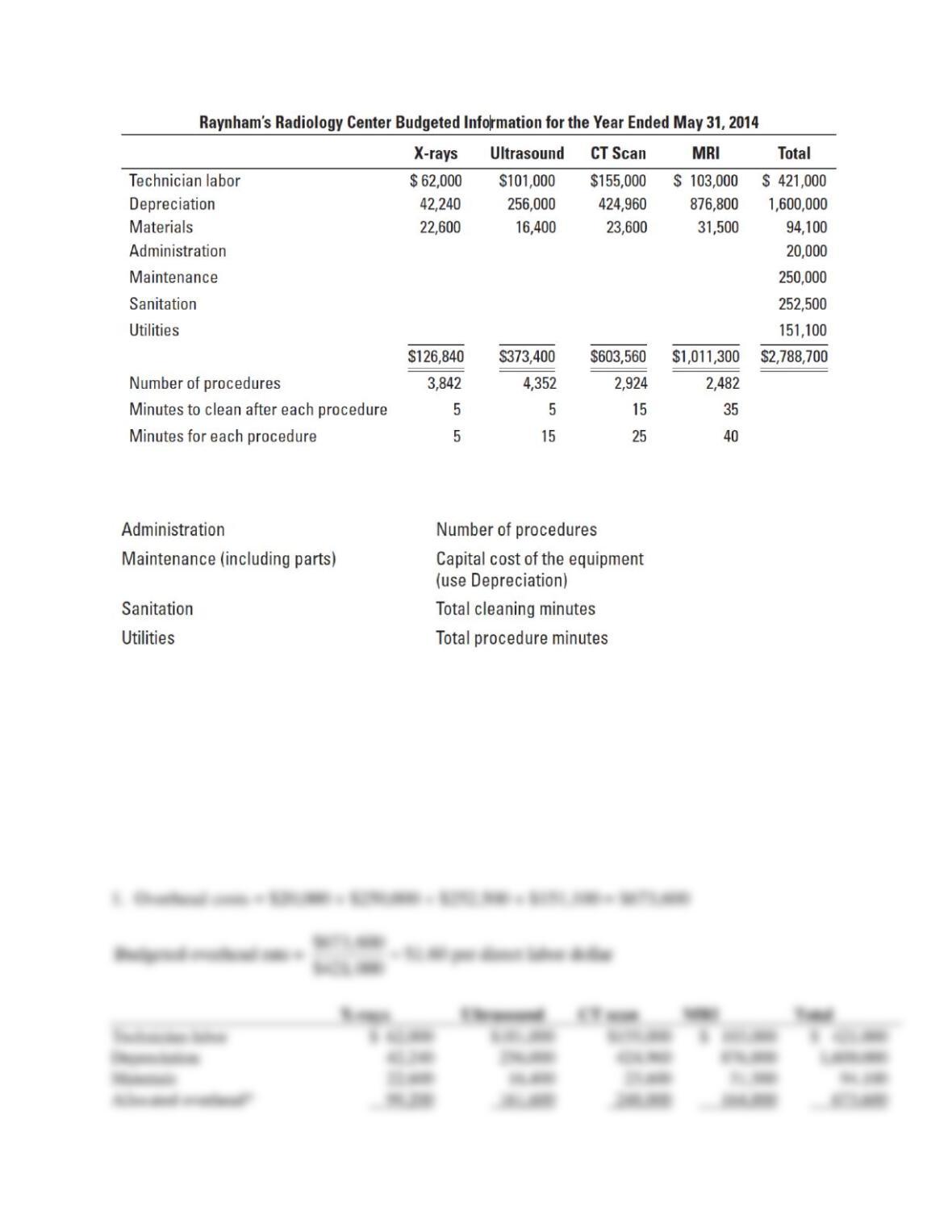

5-35 (30-40 min.) Department and activity-cost rates service sector.

Raynham’s Radiology Center (RRC) performs X-rays, ultrasounds, computer tomography (CT)

scans, and magnetic resonance imaging (MRI). RRC has developed a reputation as a top

radiology center in the state. RRC has achieved this status because it constantly reexamines its

processes and procedures. RRC has been using a single, facility-wide overhead allocation rate.

The vice president of finance believes that RRC can make better process improvements

if it uses more disaggregated cost information. She says, “We have state-of-the-art medical

imaging technology. Can’t we have state-of-the-art accounting technology?”

5-48

RRC operates at capacity. The proposed allocation bases for overhead are:

Required:

1. Calculate the budgeted cost per service for X-rays, ultrasounds, CT scans, and MRI using

direct technician labor costs as the allocation basis.

2. Calculate the budgeted cost per service of X-rays, ultrasounds, CT scans, and MRI if RRC

allocated overhead costs using activity-based costing.

3. Explain how the disaggregation of information could be helpful to RRC’s intention to

continuously improve its services.

SOLUTION

5-49

5-50

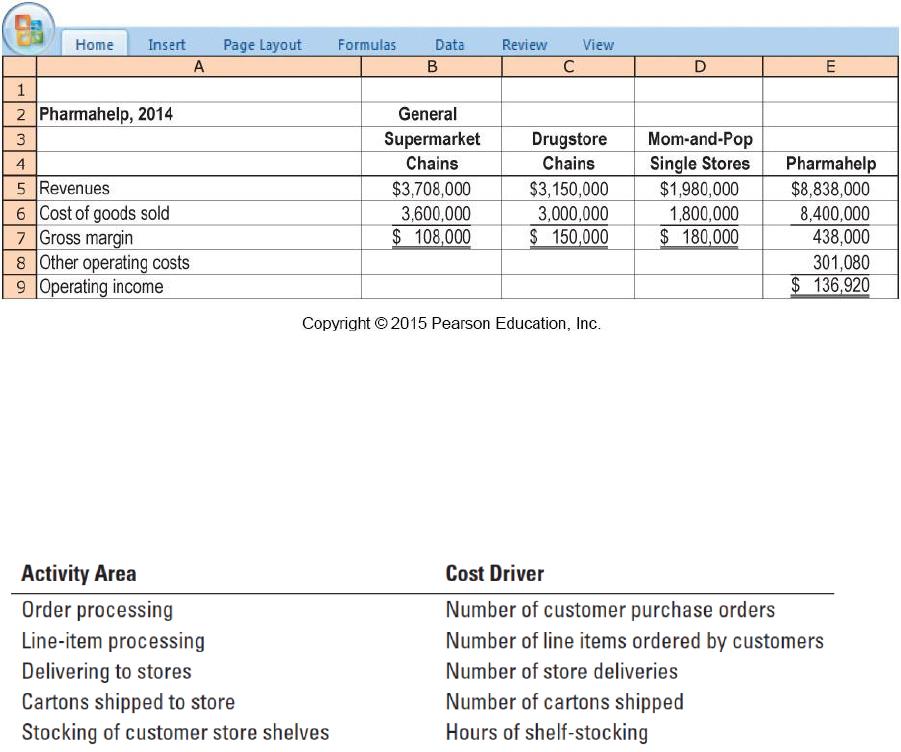

5-36 (30–40 min.) Activity-based costing, merchandising.

Pharmahelp, Inc., a distributor of special pharmaceutical products, operates at capacity and has

three main market segments:

a. General supermarket chains

b. Drugstore chains

c. Mom-and-pop single-store pharmacies

Rick Flair, the new controller of Pharmahelp, reported the following data for 2014

5-51

For many years, Pharmahelp has used gross margin percentage [(Revenue – Cost of goods sold)

÷ Revenue] to evaluate the relative profitability of its market segments. But Flair recently

attended a seminar on activity- based costing and is considering using it at Pharmahelp to

analyze and allocate “other operating costs.” He meets with all the key managers and several of

his operations and sales staff, and they agree that there are five key activities that drive other

operating costs at Pharmahelp:

Each customer order consists of one or more line items. A line item represents a single product

(such as Extra-Strength Tylenol Tablets). Each product line item is delivered in one or more

separate cartons. Each store delivery entails the delivery of one or more cartons of products to a

customer. Pharmahelp’s staff stacks cartons directly onto display shelves in customers’ stores.

Currently, there is no additional charge to the customer for shelf-stocking and not all customers

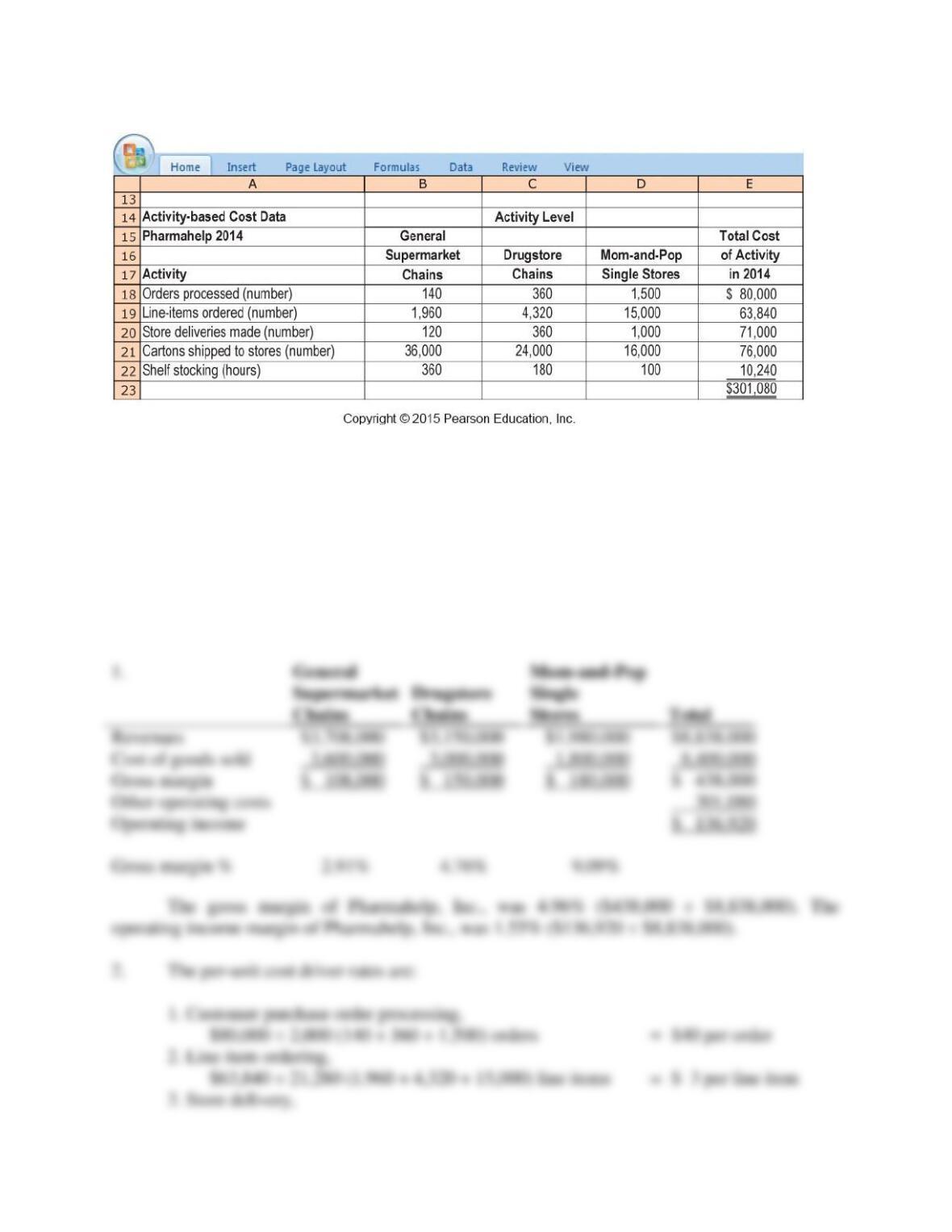

use Pharmahelp for this activity. The level of each activity in the three market segments and the

total cost incurred for each activity in 2014 is as follows:

5-52

Required:

1. Compute the 2014 gross-margin percentage for each of Pharmahelp’s three market segments.

2. Compute the cost driver rates for each of the five activity areas.

3. Use the activity-based costing information to allocate the $301,080 of “other operating costs”

to each of the market segments. Compute the operating income for each market segment.

4. Comment on the results. What new insights are available with the activity-based costing

information?

SOLUTION

5-53

5-54

5-55

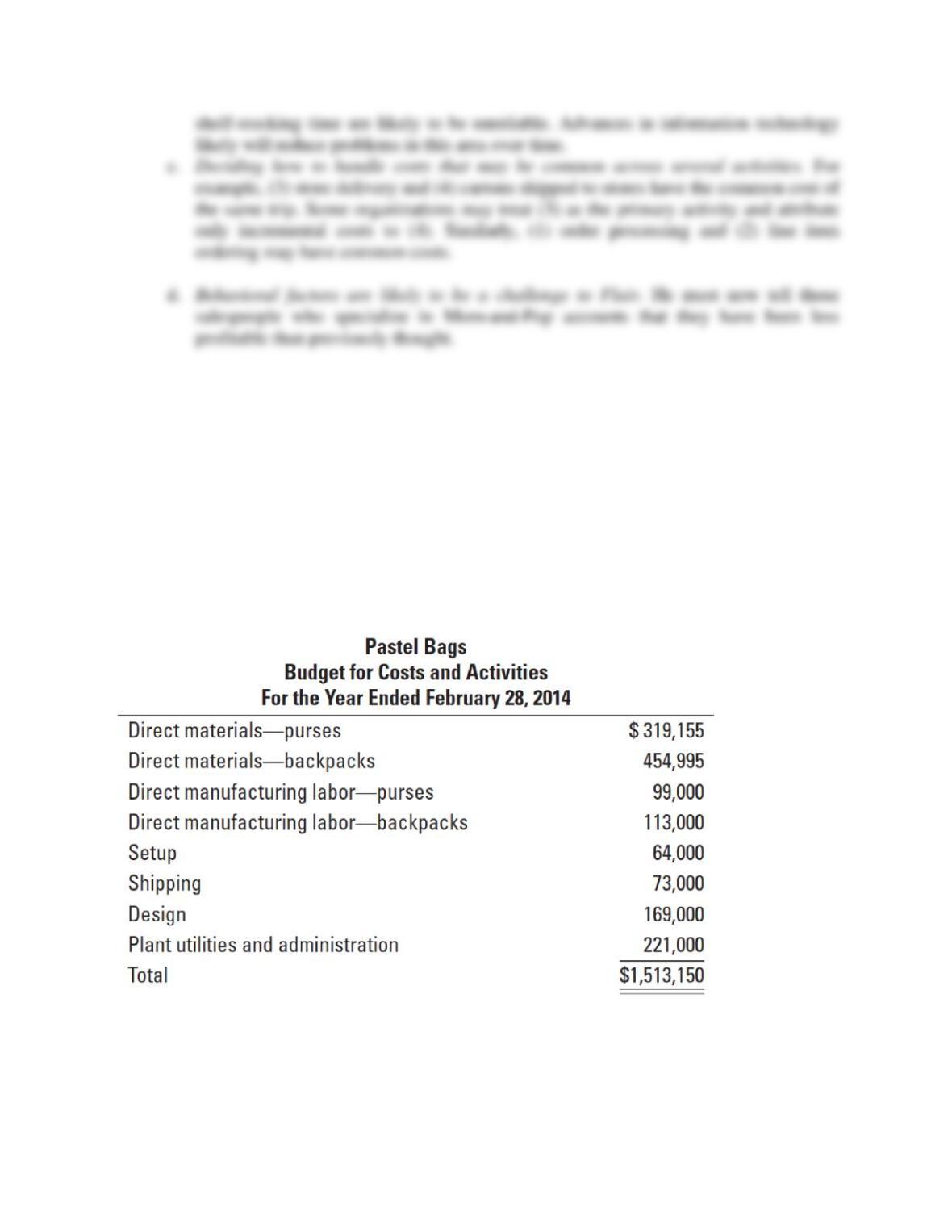

5-37 (30-40 min.) Choosing cost drivers, activity-based costing, activity-based

management.

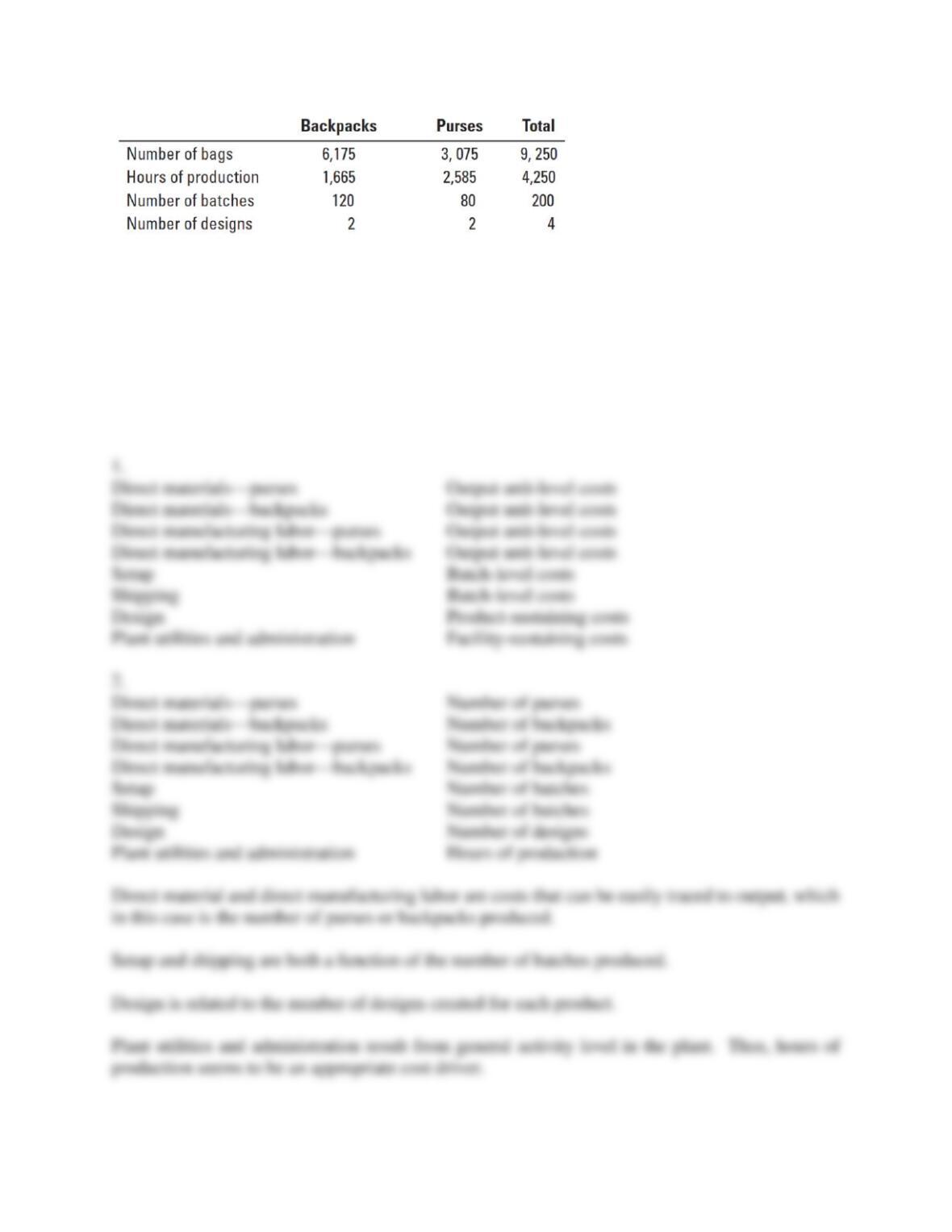

Pastel Bags (PB) is a designer of high-quality backpacks and purses. Each design is made in

small batches. Each spring, PB comes out with new designs for the backpack and for the purse.

The company uses these designs for a year and then moves on to the next trend. The bags are all

made on the same fabrication equipment that is expected to operate at capacity. The equipment

must be switched over to a new design and set up to prepare for the production of each new

batch of products. When completed, each batch of products is immediately shipped to a

wholesaler. Shipping costs vary with the number of shipments. Budgeted information for the

year is as follows:

Other budget information follows:

5-56

Required:

1. Identify the cost hierarchy level for each cost category.

2. Identify the most appropriate cost driver for each cost category. Explain briefly your choice

of cost driver.

3. Calculate the budgeted cost per unit of cost driver for each cost category.

4. Calculate the budgeted total costs and cost per unit for each product line.

5. Explain how you could use the information in requirement 4 to reduce costs.

SOLUTION