CHAPTER 5

SOLUTIONS TO EXERCISES—SET B

EXERCISE 5-1 B

(a)

(b) The relevant range is 4,000 – 9,000 units of output since a straight-line

relationship exists for both direct materials and rent within this range.

(c)

Variable cost per unit

Within the relevant range

=

Difference in cost

Difference in units

9,000 – 4,000

$15,000*

5,000*

(d) Fixed cost within the

relevant range = $8,000

EXERCISE 5-2B

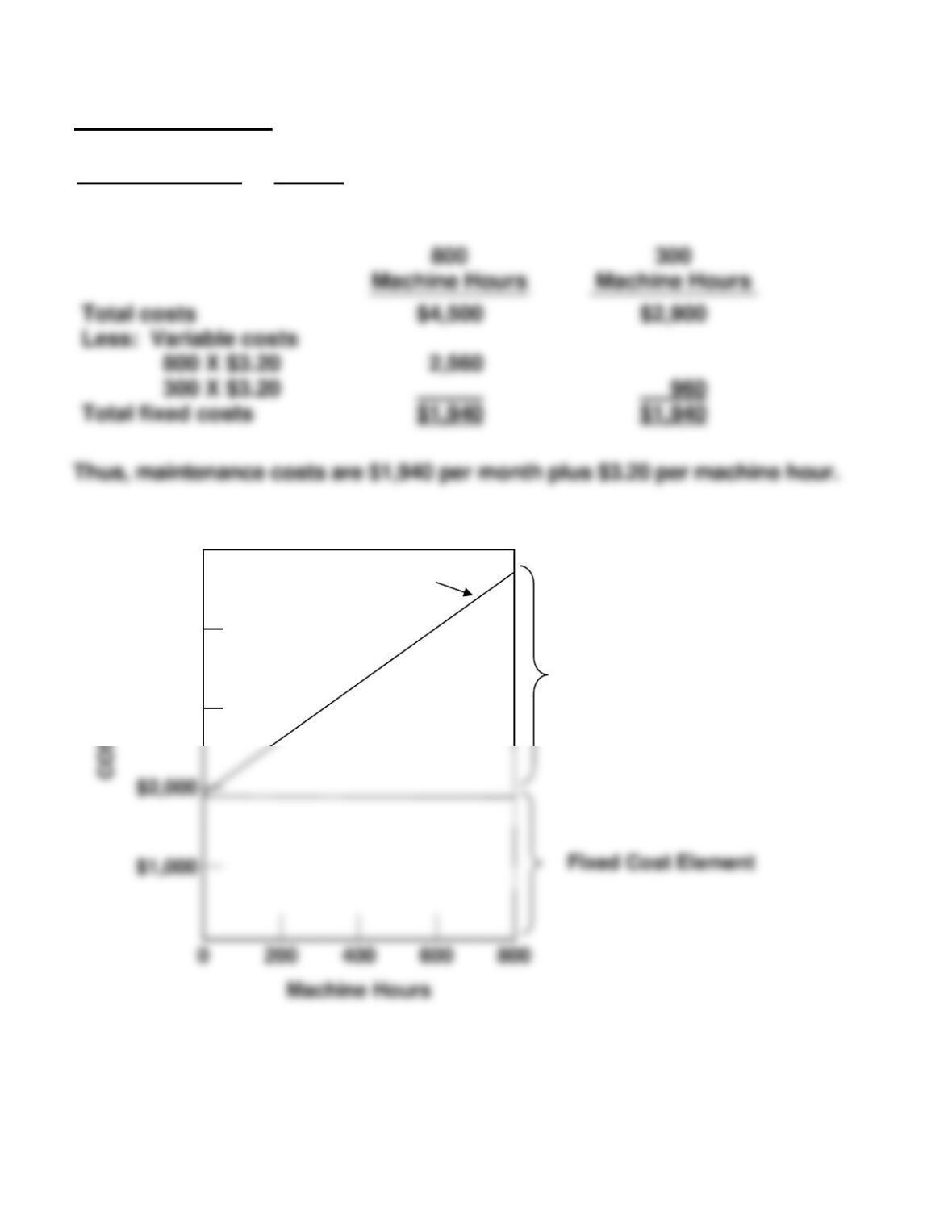

(a) Maintenance Costs:

= = $3.20 variable cost per machine hour

(b)

$5,000

$2,000

Total Cost Line

$4,400

$4,000

$3,000

Variable Cost Element

$4,500–$2,900

800–300

$1,600

500

EXERCISE 5-3B

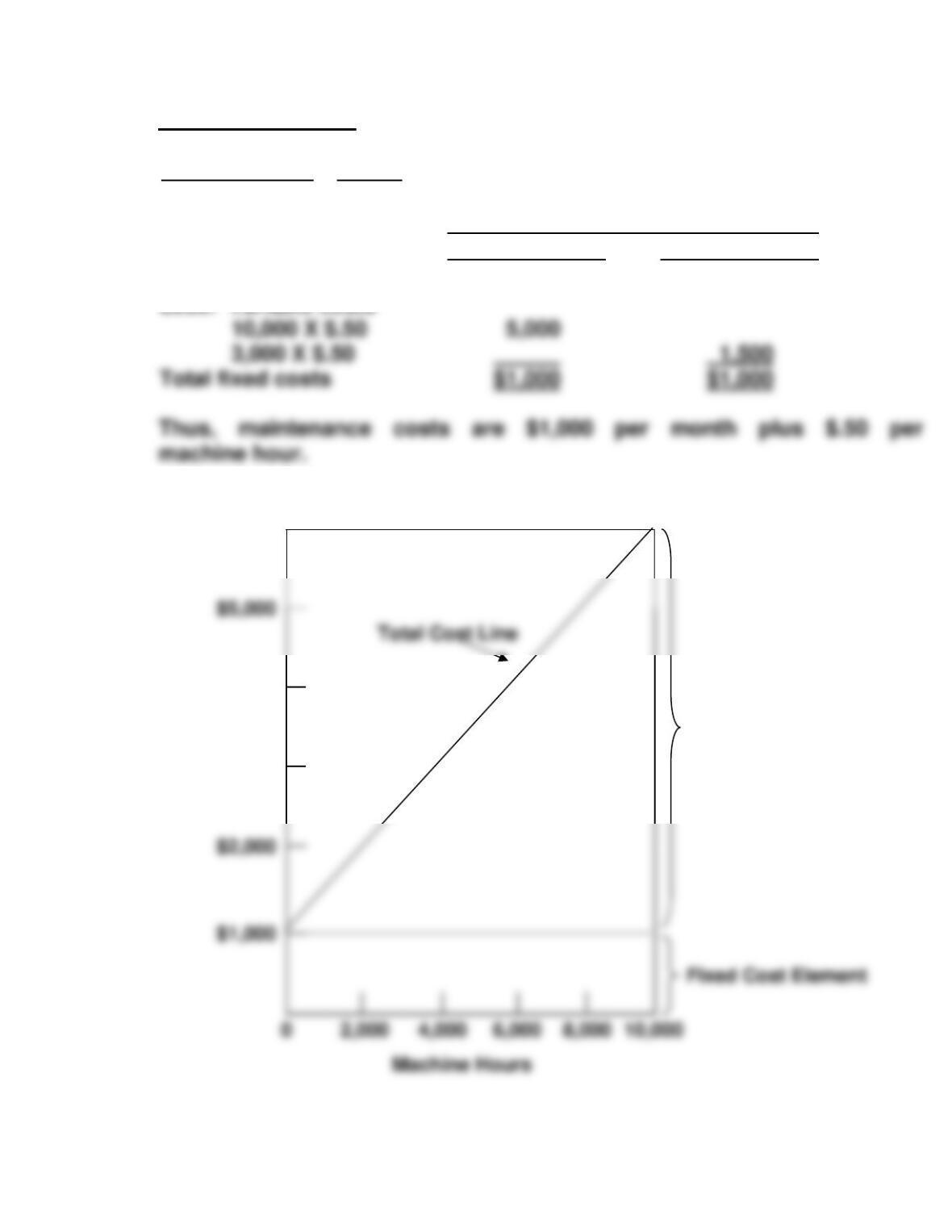

(a) Maintenance Costs:

= $.50 variable cost per machine hour

Activity Level

High

Low

Total cost

Less: Variable costs

$6,000

$2,500

(b)

$5,000

$6,000

$4,000

Variable Cost Element

$3,000

$6,000 – $2,500

10,000 – 3,000 =$3,500

7,000

Total fixed costs

EXERCISE 5-4B

(a)

Cost

Fixed

Variable

Mixed

Direct materials

X

Direct labor

X

Utilities

X

(b) Fixed costs = $1,000 + $1,800 + $2,400

= $5,200

Variable costs to produce 4,000 units = $7,500 + $15,000 + $5,500

= $28,000

Maintenance:

Variable cost to produce 4,000 units = $1,400 – $200

= $1,200

Variable cost per unit = $1,200/4,000 units

= $.30 per unit

Property taxes

X

Indirect labor

X

Supervisory salaries

X

Maintenance

X

Depreciation

X

EXERCISE 5-5B

(a)

Contribution margin per lawn

Contribution margin per lawn

=

=

$70 – ($15 + $7 + $6)

$42

(b) Break-even point in dollars = 120 lawns X $70 per lawn

= $8,400 per month

OR

EXERCISE 5-6B

(1)

Contribution margin per room

Contribution margin per room

=

=

$120 – ($32 + $40)

$48

(2) Break-even point in dollars = 375 rooms X $120 per room

= $45,000 per month

EXERCISE 5-7B

(a) Contribution margin in dollars: Sales = 600 X $90 = $54,000

Variable costs = $54,000 X .60 = 32,400

Contribution margin $21,600

(b) Breakeven sales (in dollars):

$18,000

= $45,000

40%

$18,000

EXERCISE 5-8B

(a)

(1) Contribution margin ratio is:

$43,200

= 75%

$57,600

Break-even point in dollars =

= $24,000

(2) Round-trip fare =

$57,600

= $40

1,440 fares

(b) At the break-even point fixed costs and contribution margin are equal.

EXERCISE 5-9B

(a) Unit contribution margin =

=

$105,000

(420,000 ÷ $8)

(b) Fixed costs = Breakeven sales in units X Unit contribution

margin

= ($450,000 ÷ $8.00) X $2

= $112,500

OR

units in sales Breakeven

costs Fixed

EXERCISE 5-10B

(a) AMBER COMPANY

CVP Income Statement

For the Month Ended September 30, 2017

Total

Per Unit

Sales (720 video game consoles) ……………… $360,000 $500

Variable costs …………………………………………. 252,000 350

(b) Sales = Variable costs + Fixed costs

$500X = $350X + $72,000

(c) AMBER COMPANY

CVP Income Statement

For the Month Ended September 30, 2017

Total

Per Unit

Sales (480 video game consoles)………………. $240,000 $500

EXERCISE 5-11B

(a) Sales = Variable cost + Fixed cost + Target net income

$180X = $90X + $540,000 + $90,000

EXERCISE 5-11B (Continued)

OR

Units sold in 2016 =

$540,000 + $90,000

= 7,000 units

$180 − $90

(c)

$540,000 + $162,000

= 7,000 units, where X = new selling price

X − $90

EXERCISE 5-12B

1. Unit sales price = $350,000 ÷ 5,000 units = $70

2. Reduce variable costs to 70% of sales.

$540,000 + $162,000*

EXERCISE 5-13B

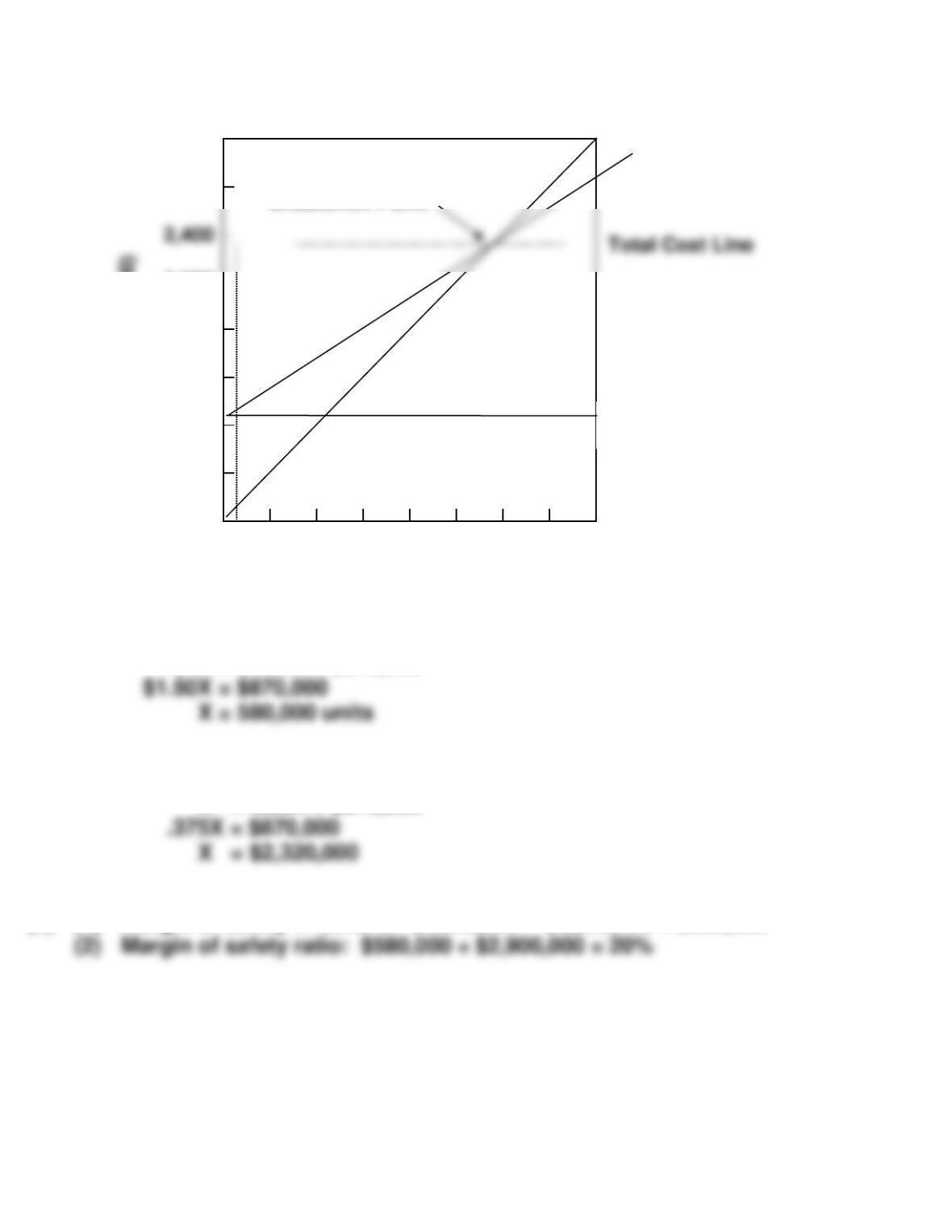

(a)

$3,200

Sales Line

DOLLARS (000)

2,800

Breakeven Point

2,000

1,600

1,200

800

Fixed Cost Line

400

100

200

300

400

500

600

700

800

Number of Units (in thousands)

(b) (1) Breakeven sales in units:

$4X = $2.50X + $870,000

(2) Breakeven sales in dollars:

X = .625X + $870,000

(c) (1) Margin of safety in dollars: $2,900,000 – $2,320,000 = $580,000

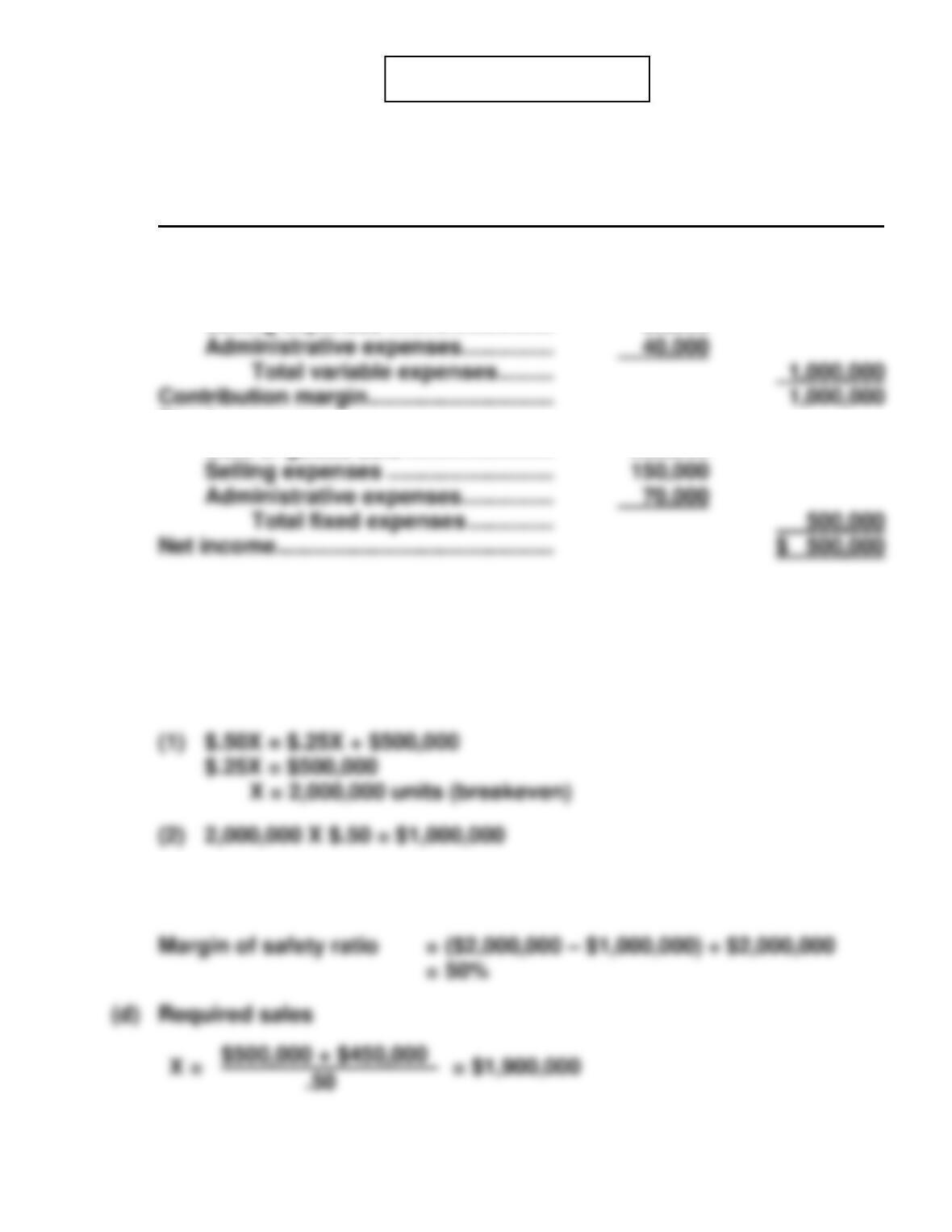

EXERCISE 5-14B

(a) Contribution ratio = Contribution margin ÷ Sales

($50 – $10) ÷ $50 = 80%

SOLUTIONS TO PROBLEMS—SET C

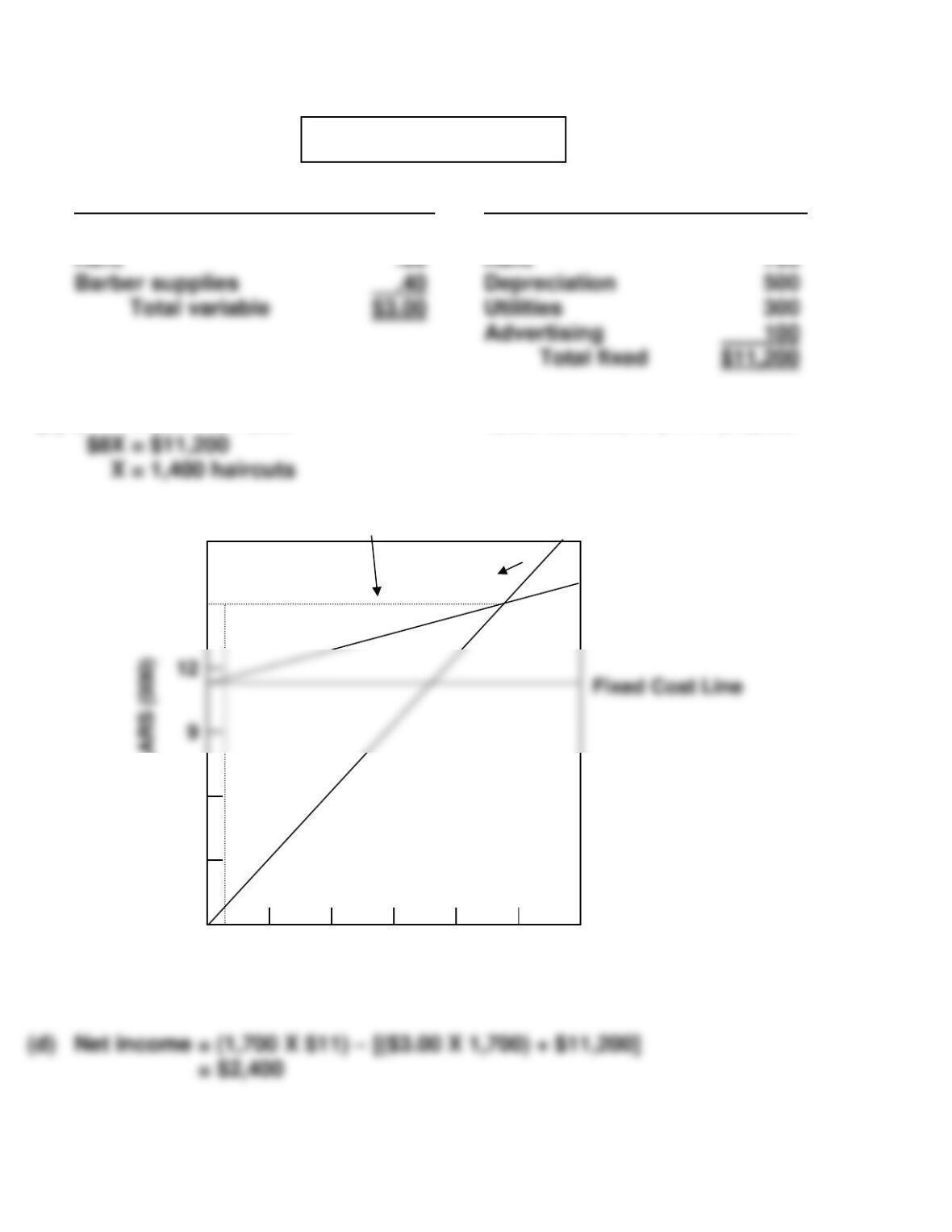

PROBLEM 5-1C

(a)

Variable costs (per haircut)

Fixed costs (per month)

Barbers’ commission $2.00

Barbers’ salaries $ 9,600

(b)

$11X = $3X + $11,200

1,400 haircuts X $11 = $15,400

(c)

18

Breakeven Point

Sales Line

DOLLARS (000)

15

Total Cost Line

12

Fixed Cost Line

6

3

300

600

900

1,200

1,500

1,800

Number of Haircuts

Total variable $3.00

Utilities 300

PROBLEM 5-2C

(a) HAWKINS COMPANY

CVP Income Statement (Estimated)

For the Year Ending December 31, 2017

Net sales ………………………………………… $2,000,000

Variable expenses

Cost of goods sold …………………… $880,000 (1)

Selling expenses ……………………… 80,000

Fixed expenses

Cost of goods sold …………………… 280,000

(1) Direct materials $290,000 + direct labor $370,000 + variable manufacturing

overhead $220,000.

(b) Variable costs = 50% of sales ($1,000,000 ÷ $2,000,000) or $.25 per bottle

($.50 X 50%). Total fixed costs = $500,000.

(c) Contribution margin ratio = ($.50 – $.25) ÷ $.50

= 50%

PROBLEM 5-3C

(a) Sales were $1,600,000 and variable expenses were $1,040,000, which

means contribution margin was $560,000 and CM ratio was 35%. Fixed

expenses were $840,000. Therefore, the breakeven point in dollars is:

(b) 1. The effect of this alternative is to increase the selling price per unit to

$35 ($1,600,000 ÷ 64,000) X 140%). Total sales become $2,240,000

2. The effects of this alternative are to change total fixed costs to $670,000

($840,000 – $170,000) and to change the contribution margin ratio to .30

[($1,600,000 – $1,040,000 – $80,000) ÷ $1,600,000]. The new breakeven

point is:

(

1

8

,

0

0

0

X

$

3

0

)

–

(

1

3

,

5

0

0

X

$

3

0

)

(

1

8

,

0

0

0

X

$

3

0

)

PROBLEM 5-4C

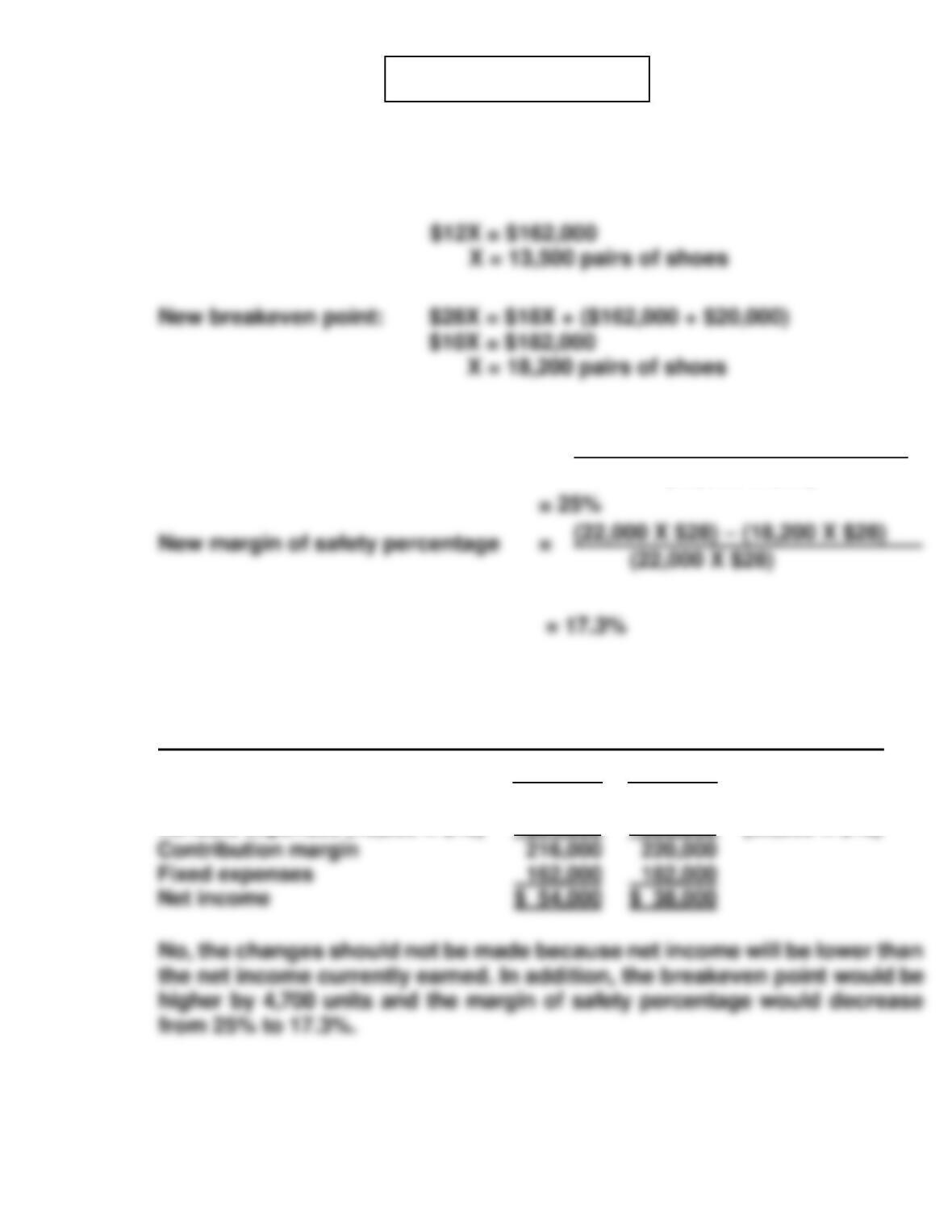

(a) Current breakeven point: $30X = $18X + $162,000

(where X = pairs of shoes)

(b) Current margin of safety percentage =

(c) EASY-FIT SHOE STORE

CVP Income Statement

Current

New

Net income

Sales (18,000 X $30)

Variable expenses (18,000 X $18)

$540,000

324,000

$616,000

396,000

(22,000 X $28)

(22,000 X $18)

PROBLEM 5-5C

(a)

(1)

Current Year

Net sales

Variable costs

Direct materials

$2,500,000

600,000

Current Year

Projected Year

Contribution margin

Sales

Variable costs

Direct materials

Direct labor

$2,500,000

600,000

425,000

X 1.2

X 1.2

X 1.2

$3,000,000

720,000

510,000

(2)

Fixed Costs

Current Year

Projected Year

Total fixed costs

Manufacturing overhead ($525,000 X .80)

$ 420,000

$ 420,000

Contribution margin

PROBLEM 5-5C (Continued)

(b) Unit selling price = $2,500,000 ÷ 100,000 = $25

Unit variable cost = $1,400,000 ÷ 100,000 = $14

(c) Sales dollars

required for

=

(Fixed costs

+

Target net income)

÷

Contribution margin ratio

income

=

+

÷

(d) Margin of safety

ratio

=

(Expected sales

–

Break-even

sales)

÷

Expected sales

Break-even point in units

=

Fixed costs

÷

Unit contribution margin

Break-even point in dollars

Fixed costs

÷

Contribution margin ratio

PROBLEM 5-6C

(a) (1) Let variable selling and administrative expenses = VSA

Sales – Variable cost of goods sold – VSA = Contribution Margin

(2) Let fixed manufacturing overhead = FMO

Sales – Variable cost of goods sold – FMO = Gross profit

(3) Let fixed selling and administrative expenses = FSA

Contribution margin ratio = $117,000 ÷ $1,300,000 = 9%

Contribution margin at break-even = $1,350,000 X 9% = $121,500

(b) Incremental sales = $1,300,000 X 15% = $195,000

Incremental contribution margin = $195,000 X 9% = $17,550