5–1

CHAPTER 5

Learning Objectives

After studying this chapter, students should be able to:

1. Describe the basic requirements for an individual to be classified as an employer or

an employee under the Federal Unemployment Tax Act.

2. Identify generally what is defined as taxable wages by the Federal Unemployment

Tax Act.

3. Compute the federal unemployment tax, the credit against the tax, and any credit

reductions that might apply.

4. Describe how an experience-rating system is used in determining employers’

contributions to state unemployment compensation funds.

5. Complete the reports required by the Federal Unemployment Tax Act.

6. Describe the types of information reports under the various state unemployment

compensation laws.

Contents

Chapter 5 outline:

LEARNING OBJECTIVES

COVERAGE UNDER FUTA AND SUTA

Employers—FUTA

Employers—SUTA

Employees—FUTA

Employees—SUTA

Coverage of Interstate Employees

Place Where the Work Is Localized

Location of Base of Operations

Location of Place from Which Operations Are Directed or Controlled

Location of Employee’s Residence

Reciprocal Arrangements and Transfers of Employment

Coverage of Americans Working Overseas

5–2 Payroll Accounting

UNEMPLOYMENT COMPENSATION TAXES AND CREDITS

Tax Rate—FUTA

Credits Against FUTA Tax

Experience Rating

Title XII Advances

Tax Rates—SUTA

UNEMPLOYMENT COMPENSATION REPORTS REQUIRED OF THE EMPLOYER

Annual FUTA Return—Form 940

Electronic Filing

Completing the Return

Part 1

Part 2

Part 3

Part 4

Part 5

Part 6

Part 7

Schedule A

Filing the Return

Amending the Return

Final Return

Quarterly Deposit—FUTA

Taxes—Household Employers

Penalties—FUTA

Information Reports—SUTA

Status Reports

Contribution Reports

Wage Information Reports

Separation Reports

Partial Unemployment Notices

Record Retention

Penalties—SUTA

KEY TERMS

ANSWERS TO SELF-STUDY QUIZZES

KEY POINTS SUMMARY

Chapter 5 5–3

Matching Quiz (p. 5–32)

Questions for Review (p. 5–32)

1. Under FUTA, a person or a business is considered an employer if either of the

following two tests applies:

2. If during the present or previous year, the household employer paid $1,000 or more

4. The three conditions are (1) the employee performs work in that state, (2) the

5. FUTA coverage includes service of any nature performed outside the United States

7. To obtain the maximum credit of 5.4 percent, the employer must make the state

8. State contribution ……………………………………………………………………….. 1.5%

5–4 Payroll Accounting

9. Two situations that could result in a net FUTA tax greater than 0.6 percent are:

10. The purpose of Title XII advances is to provide funds to states that cannot pay

12. Each state sets an initial contribution rate (not less than 1%) for new employers

15. The employer must complete a new Form 940 for the year being amended. The

16. A final Form 940 is completed (a box on Form 940 is checked to indicate a final

Chapter 5 5–5

17. If the employer’s FUTA tax liability exceeds $500 at the end of a calendar quarter,

18. A check or money order can be remitted with Form 940, or an electronic payment

20. A separation report provides a wage and employment record of an employee and

Questions for Discussion (p. 5–33)

1. Benefits cannot be paid to self-employed persons because persons in business

for themselves on a full-time basis are not considered unemployed for

2. Stable employers should not be penalized with high minimum rates in order to

keep a cap on the upper tax limits. Employers responsible for layoffs should pay

3. Students’ answers to this question will vary, depending upon the state under

5–6 Payroll Accounting

4. a. Benefits for the employer include:

Benefits for the employees include:

(1) The hardship is spread out over the entire workforce. And with partial

(2) Workers in the lower-paying, more junior jobs stand to gain the most.

(3) Often, while on a reduced workweek, workers do not lose their health and

b. Because of the continuation of health and welfare benefits to the partially unem-

ployed, the cost of the program may be a little more than under a companywide

Chapter 5 5–7

Problem Sets (p. 5–35)

The principles and practices of payroll accounting discussed in Chapter 5 are applied in

the Problem Sets as shown below.

Principle or Practice Problem Set No. (A and B)

1. Calculating the net FUTA and SUTA taxes. 5–1 through 5–9, 5–11, 5-14

2. Determining taxable wages for FUTA and SUTA. 5–6 through 5–9, 5–14

3. Transfer of employment. 5–7

4. The amount of credit against the FUTA tax 5–10

based on late payments of SUTA tax.

5. Calculating the net SUTA and FUTA taxes and 5–11

the amount of the employees’ unemployment

compensation tax.

6. Determining the SUTA contribution rate based 5–12, 5–13, 5–15

on a reserve ratio.

7. Voluntary contributions. 5–12, 5–13

8. Employees’ FICA taxes and the employer’s 5–14

payroll taxes for one payroll period.

9. Form 940 [Employer’s Annual Federal 5–16, 5–17

Unemployment (FUTA) Tax Return].

10. State Quarterly Unemployment Compensation 5–17

Tax Form.

Solutions—Problem Set A

5–8 Payroll Accounting

5–2A. Earnings subject to FUTA and SUTA:

5–6A. (a) FUTA taxable wages:

(b) SUTA taxable wages:

Chapter 5 5–9

5–8A. (a) FUTA tax ………………………………………………… $7,000 × 0.006 = $ 42.00

Total = $ 756.00

5–10A. (a) $114,000 × 0.031 × 90% …………………………………………… $3,180.60

5–10 Payroll Accounting

5–13A. (a) $1,190

5–14A. (a) Taxable OASDI HI

Earnings (6.2%) (1.45%)

V. Hoffman…………………………….. $392.31 $24.32 $5.69

A. Drugan ……………………………… 288.46 17.88 4.18

Chapter 5 5–11

5–15A. (a) State contributions:

2004 to 2013 inclusive ……………………………………………… $14,695.00

Average annual payroll:

Total payroll for last three years, $141,350, divided by 3 equals

$47,116.67, the average annual payroll.

Computation of the rate for 2018:

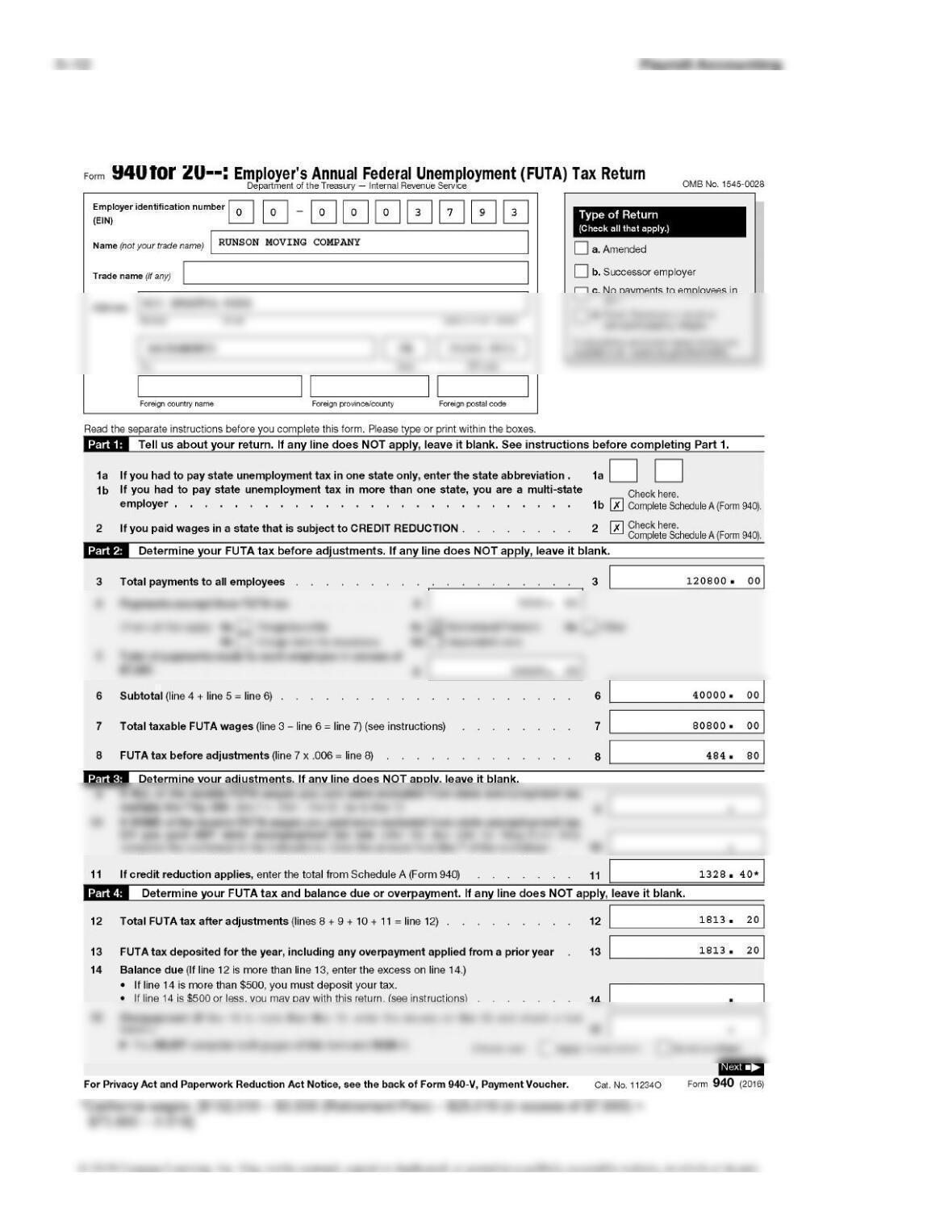

5–16A. Form 940

Chapter 5 5–13

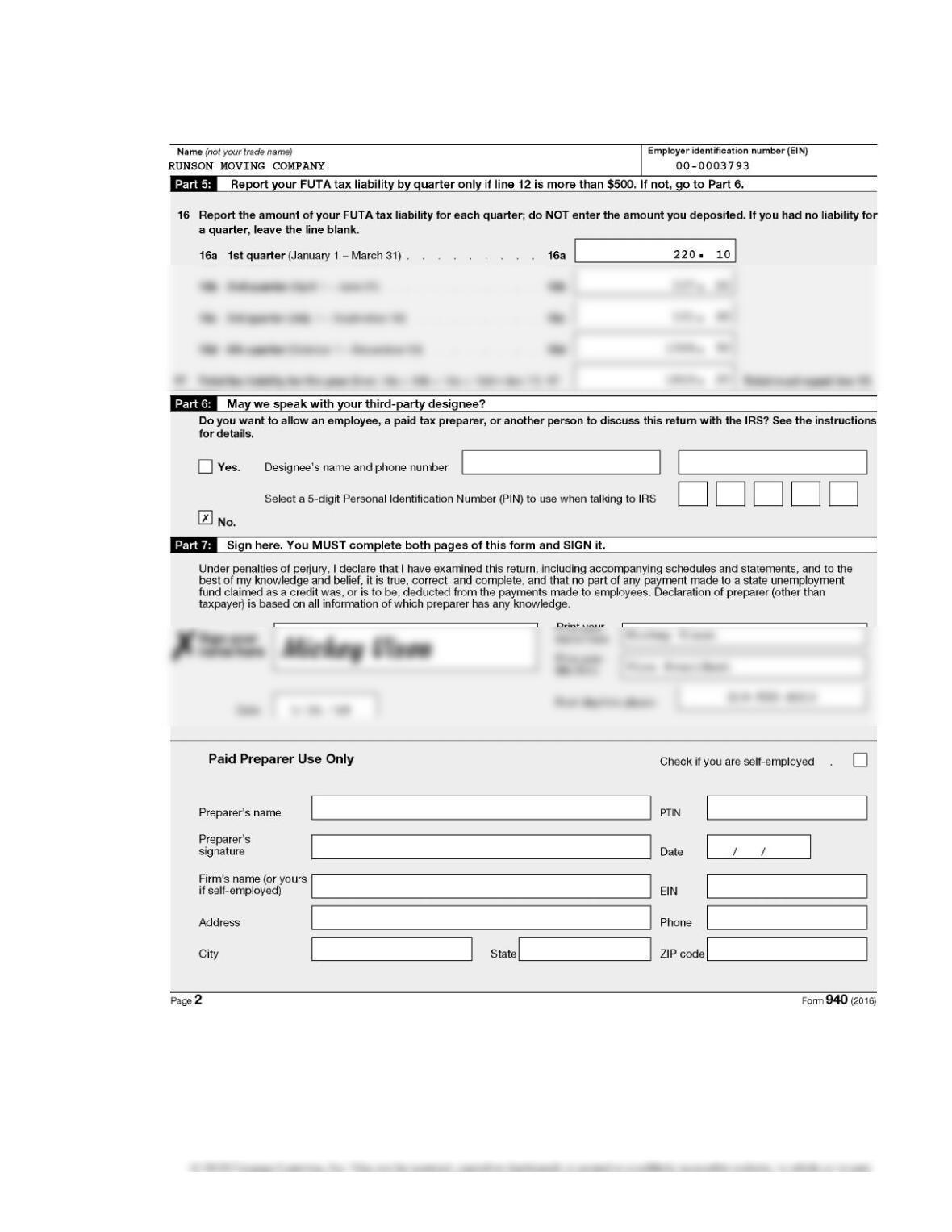

5–16A. Form 940 (Continued)

Source: Internal Revenue Service.

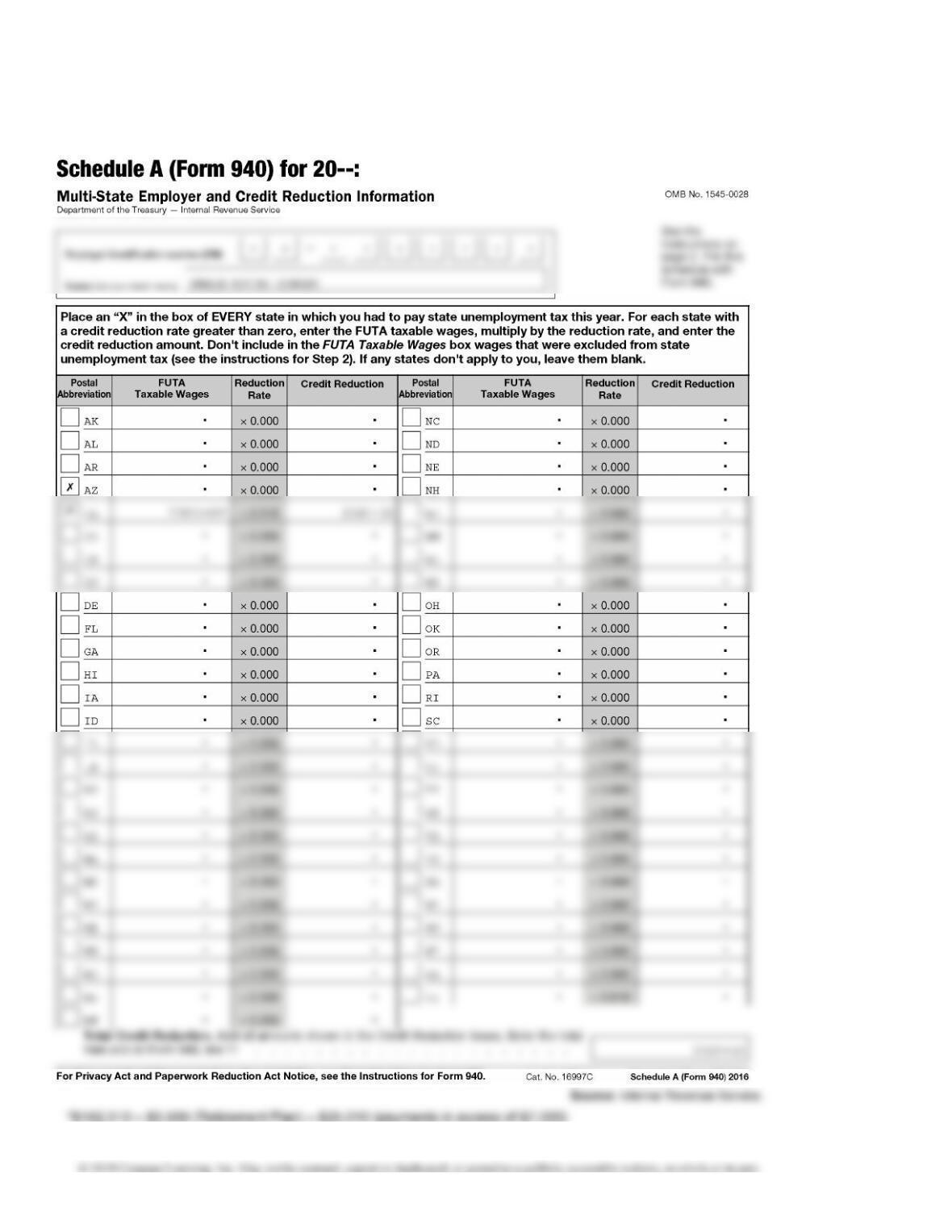

5–14 Payroll Accounting

5–16A. Form 940 (Concluded)