CHAPTER 5

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 5-1C

(a)

General Journal

Date

Account Titles

Debit

Credit

Apr. 2

Inventory ……………………………………………………

Accounts Payable ………………………………..

8,700

8,700

Cost of Goods Sold …………………………………….

Inventory ……………………………………………..

3,700

3,700

5

Freight-out …………………………………………………

Cash ……………………………………………………

200

200

6

Accounts Payable ………………………………………

Inventory ……………………………………………..

400

400

11

Accounts Payable ($8,700 – $400) ……………….

Cash ……………………………………………………

Inventory ($8,300 X 2%) ………………………..

8,300

8,134

166

13

Cash ……………………………………………………….….

Sales Discounts ($6,000 X 2%) …………………….

Accounts Receivable …………………………..

5,880

14

Inventory ……………………………………………………

Cash ……………………………………………………

4,700

4,700

16

Cash ……………………………………………………….….

500

18

Inventory ……………………………………………………

Accounts Payable ………………………………..

5,500

5,500

20

Inventory ……………………………………………………

Cash ……………………………………………………

180

180

PROBLEM 5-1C (Continued)

General Journal

Date

Account Titles

Debit

Credit

Apr. 23

Inventory ……………………………………………..

Cash ……………………………………………………….

Sales Revenue ……………………………………..

8,300

8,300

27

Accounts Payable ……………………………………….

Cash ……………………………………………………

Inventory ($5,500 X 2%) ………………………..

5,500

5,390

110

29

30

Accounts Receivable …………………………………..

Sales Returns and Allowances …………………….

Cash ……………………………………………………

180

180

PROBLEM 5-1C (Continued)

(b)

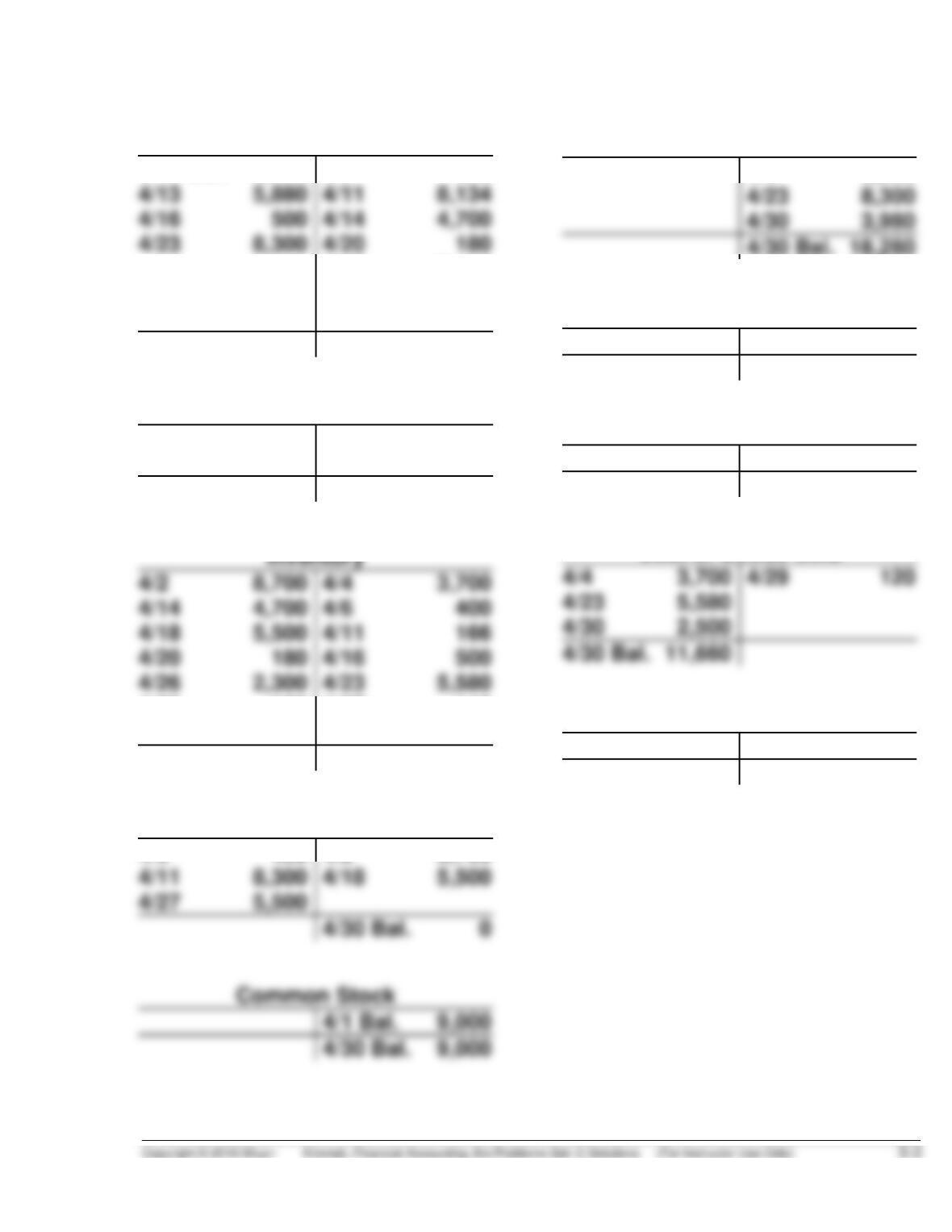

Cash

4/30 3,980

4/1 Bal. 9,000

4/5 200

4/26 2,300

4/27 5,390

4/29 180

4/30 Bal. 2,596

Accounts Receivable

4/4 6,000

4/30 3,980

4/13 6,000

4/30 Bal. 3,980

4/2 8,700

4/26 2,300

4/4 3,700

4/4 3,700

4/29 120

4/30 Bal. 11,660

4/29 120

4/27 110

4/30 2,500

4/30 Bal. 8,544

Accounts Payable

4/30 Bal. 0

4/1 Bal. 9,000

4/30 Bal. 9,000

4/6 400

4/2 8,700

Sales Revenue

4/4 6,000

4/30 Bal. 18,280

Sales Returns and Allowances

4/29 180

4/30 Bal. 180

Sales Discounts

4/13 120

4/30 Bal. 120

Cost of Goods Sold

Freight-Out

4/5 200

4/30 Bal. 200

PROBLEM 5-1C (Continued)

(c) CURTAIN DISTRIBUTING COMPANY

Income Statement (Partial)

For the Month Ended April 30, 2014

Sales

Sales revenue …………………………………………….. $18,280

Less: Sales returns and allowances ……………. $180

(d) Profit margin: ($6,320 – $2,050) ÷ $17,980 = 24%

PROBLEM 5-2C

July 1 Inventory ……………………………………………………… 2,700

Accounts Payable ………………………………….. 2,700

9 Accounts Payable ………………………………………… 2,700

Cash ……………………………………………………… 2,646

Inventory ($2,700 X .02) ………………………….. 54

12 Cash ……………………………………………………………. 2,871

Sales Discounts ($2,900 X .01) ………………………. 29

Accounts Receivable …………………………….. 2,900

17 Accounts Receivable ……………………………………. 2,000

Sales Revenue ………………………………………. 2,000

PROBLEM 5-2C (Continued)

July 22 Cost of Goods Sold ……………………………………….. 1,800

Inventory ………………………………………………… 1,800

PROBLEM 5-3C

(a)

General Journal

Date

Account Titles

Debit

Credit

Apr. 4

Inventory …………………………………………………….

Accounts Payable ………………………………..

980

980

6

Inventory …………………………………………………….

Cash ……………………………………………………

60

60

Cost of Goods Sold …………………………………….

Inventory ……………………………………………..

480

480

10

Accounts Payable ……………………………………….

Inventory ……………………………………………..

130

11

Inventory …………………………………………………….

Cash ……………………………………………………

300

300

13

Accounts Payable ($980 – $130) ………………….

Cash ……………………………………………………

Inventory ($850 X 2%) …………………………..

850

833

17

14

Inventory …………………………………………………….

Accounts Payable ………………………………..

1,300

1,300

15

Cash …………………………………………………………..

Inventory ……………………………………………..

17

Inventory …………………………………………………….

Cash ……………………………………………………

Cost of Goods Sold …………………………………….

Inventory ……………………………………………..

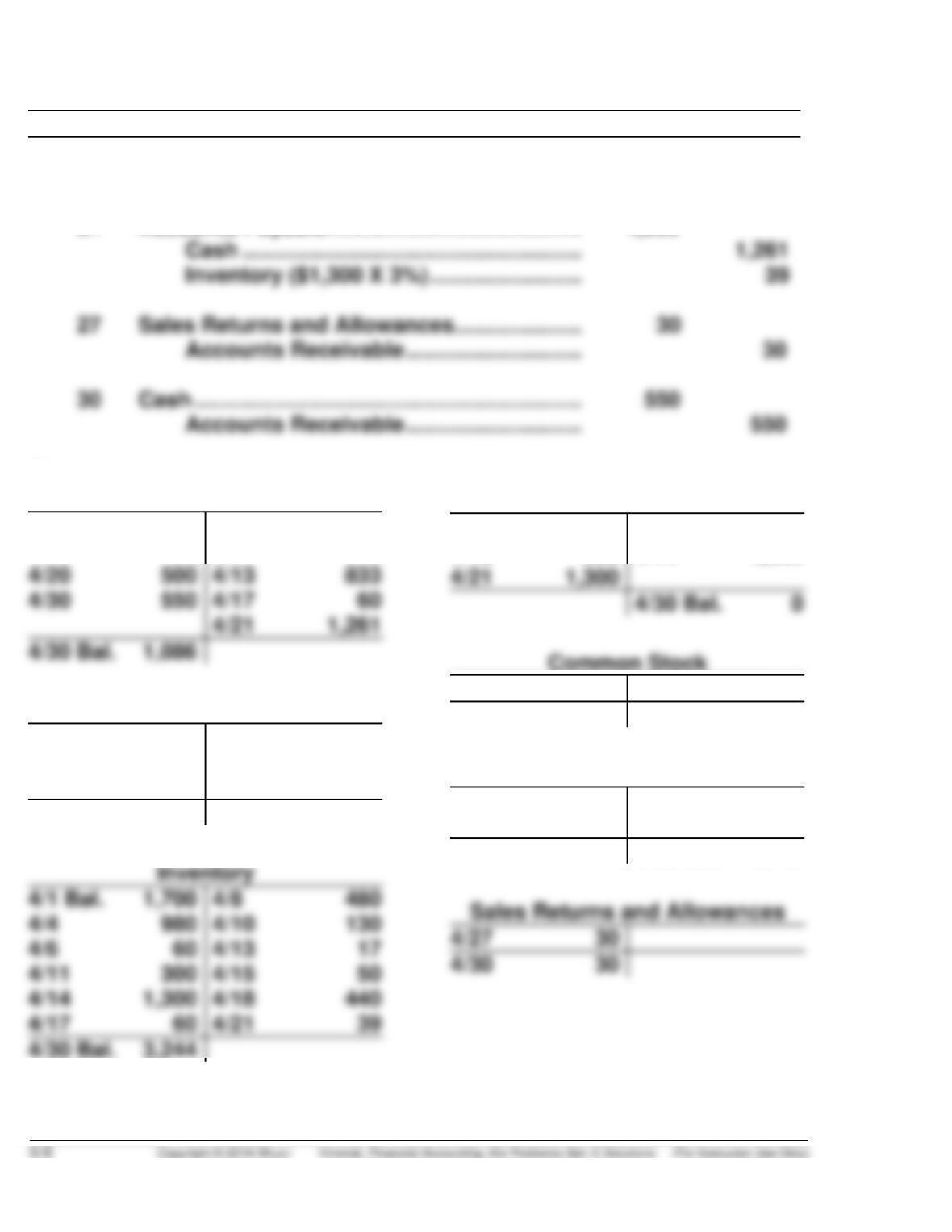

PROBLEM 5-3C (Continued)

Date

Account Titles

Debit

Credit

Apr. 20

Cash ……………………………………………………….

Accounts Receivable …………………………..

500

500

21

Accounts Receivable …………………………..

Accounts Receivable …………………………..

Accounts Payable ……………………………………….

1,300

(b)

Cash

4/21 1,261

4/30 Bal. 1,086

4/30 Bal. 0

4/1 Bal. 2,500

4/15 50

4/6 60

4/11 300

Accounts Receivable

4/8 750

4/18 660

4/20 500

4/27 30

4/30 550

4/30 Bal. 330

4/11 300

4/15 50

4/30 Bal. 3,244

4/27 30

4/30 30

Accounts Payable

4/10 130

4/13 850

4/4 980

4/14 1,300

4/1 Bal. 4,200

4/30 Bal. 4,200

Sales Revenue

4/8 750

4/18 660

4/30 Bal. 1,410

PROBLEM 5-3C (Continued)

Cost of Goods Sold

4/30 Bal. 920

4/8 480

(c) HIGHLAND TENNIS SHOP

Trial Balance

April 30, 2014

Debit

Credit

Cost of Goods Sold …………………………………………

$5,610

Cash ……………………………………………………………….

Accounts Receivable ……………………………………….

$1,086

330

(d) HIGHLAND TENNIS SHOP

Income Statement (Partial)

For the Month Ended April 30, 2014

Sales

Sales revenues ………………………………………………………….. $1,410

PROBLEM 5-4C

(a) PARKLAND DEPARTMENT STORE

Income Statement

For the Year Ended December 31, 2014

Sales

Sales revenue ………………………………… $626,000

Less: Sales returns and

Depreciation expense …………………….. 23,400

Utilities expense …………………………….. 11,000

Insurance expense …………………………. 8,400

Maintenance and repairs expense …… 6,200

Total operating expenses ………… 160,000

Income from operations ………………………… 46,000

PARKLAND DEPARTMENT STORE

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, January 1 …………………………………………………. $19,200

Add: Net income ………………………………………………………………….. 28,300

PROBLEM 5-4C (Continued)

PARKLAND DEPARTMENT STORE

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ……………………………………………. $ 28,000

Accounts receivable …………………….. 45,500

Inventory ……………………………………… 43,000

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………………………. $ 73,300

Mortgage payable …………………………………………. 20,000

Salaries and wages payable ………………………….. 3,500

PROBLEM 5-4C (Continued)

(b) Profit margin: $28,300 ÷ $618,000 = 4.6%

(c) Revised net income = Current net income + increase in gross profit –

increase in operating expenses

$51,000 = $28,300 + $50,500 – $27,800

Revised net sales = Current net sales + .25 (current net sales)

$772,500 = $618,000 + $154,500