Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 5

Chapter 5

Accounting for Merchandising

Operations

QUESTIONS

1. Merchandising companies report Merchandise Inventory on the balance sheet,

2. Additional accounts of a merchandising company likely include Merchandise

3. A company can have a net loss if its expenses (absent cost of goods sold) are

4. A cash discount can be offered to encourage customers to promptly pay. This

5. For a perpetual inventory system, inventory shrinkage is determined by taking a

6. Cash discounts are granted in return for early payment and reduce the amount paid

below the negotiated price. Cash discounts are recorded in the accounting records

7. Sales discount is a term used by a seller to describe a cash discount granted to a

8. A manager is concerned about the quantity of its purchase returns because the

9. The sender (maker) of a debit memorandum records a debit in an account of the

292

10. The single-step income statement format presents cost of goods sold and expenses

in one list, totals the list, and subtracts the total from net sales in one step. The

12. Google titles its cost of goods sold account as “Cost of revenues.”

QUICK STUDIES

Quick Study 5-1 (10 minutes)

1. G. 6. H.

Quick Study 5-2 (5 minutes)

293

Quick Study 5-3 (15 minutes)

a. (i) Computation of goods available for sale

Beginning inventory ……………………………………………. $5,000

Quick Study 5-4 (15 minutes)

Payment Computations

Quick Study 5-5 (15 minutes)

Nov. 5 Merchandise Inventory ………………………………. 6,000

Accounts Payable ………………………………. 6,000

Quick Study 5-6 (10 minutes)

a)

Aug. 1 Merchandise Inventory ………………………………………. 60,000

Quick Study 5-7 (10 minutes)

a)

Sep. 15 Merchandise Inventory ………………………………………. 35,000

Quick Study 5-8 (15 minutes)

Apr. 1 Accounts Receivable ………………………………………… 3,000

Quick Study 5-9 (10 minutes)

July 31 Cost of Goods Sold ……………………………… 1,900

296

Quick Study 5-10 (10 minutes)

July 31 Sales …………………………………………………….. 160,200

Income Summary …………………………... 160,200

Quick Study 5-11 (10 minutes)

1. a

Quick Study 5-12 (10 minutes)

297

Quick Study 5-13 (10 minutes)

Similarities: Both the acid-test ratio and current ratio are used to assess

liquidity. Both ratios are computed with current liabilities as the denominator.

Quick Study 5-14 (10 minutes)

(a)

(b)

(c)

(d)

Sales ……………………………………..

$150,000

$550,000

$38,700

$255,700

Sales discounts ……………………..

298

Quick Study 5-15 (20 minutes)

1. Multiple-step income statement

adidas Group

Income Statement (€ millions)

For Year Ended December 31, 2014

Net sales ……………………………………………………………. €14,534

2. Single-step income statement

adidas Group

Income Statement (€ millions)

For Year Ended December 31, 2014

Revenues

Net sales ………………………………………………………… €14,534

299

Quick Study 5-16A (5 minutes)

a. Periodic inventory system

Quick Study 5-17A (10 minutes) PERIODIC & GROSS

Nov. 5 Purchases ………………………………………………………….. 6,000

Accounts Payable ……………………………………….. 6,000

Quick Study 5-18A (10 minutes) PERIODIC & GROSS

Apr. 1 Accounts Receivable …………………………………………. 3,000

300

Quick Study 5-19 C (10 minutes)

a.

June 30 Sales Discounts …………………………………………………. 60

Quick Study 5-20C (10 minutes)

a.

June 30 Sales Returns and Allowances …………………………... 1,000

Quick Study 5-21D (10 minutes) NET & PERPETUAL

Nov. 5 Merchandise Inventory ………………………………………. 5,880

Quick Study 5-22D (10 minutes) NET & PERPETUAL

Apr. 1 Accounts Receivable ………………………………. 3,000

Sales ……………………………………………….. 3,000

Record sale of goods.

Quick Study 5-23 (10 minutes)

a. Both U.S. GAAP and IFRS include broad and similar guidance for the

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 5

EXERCISES

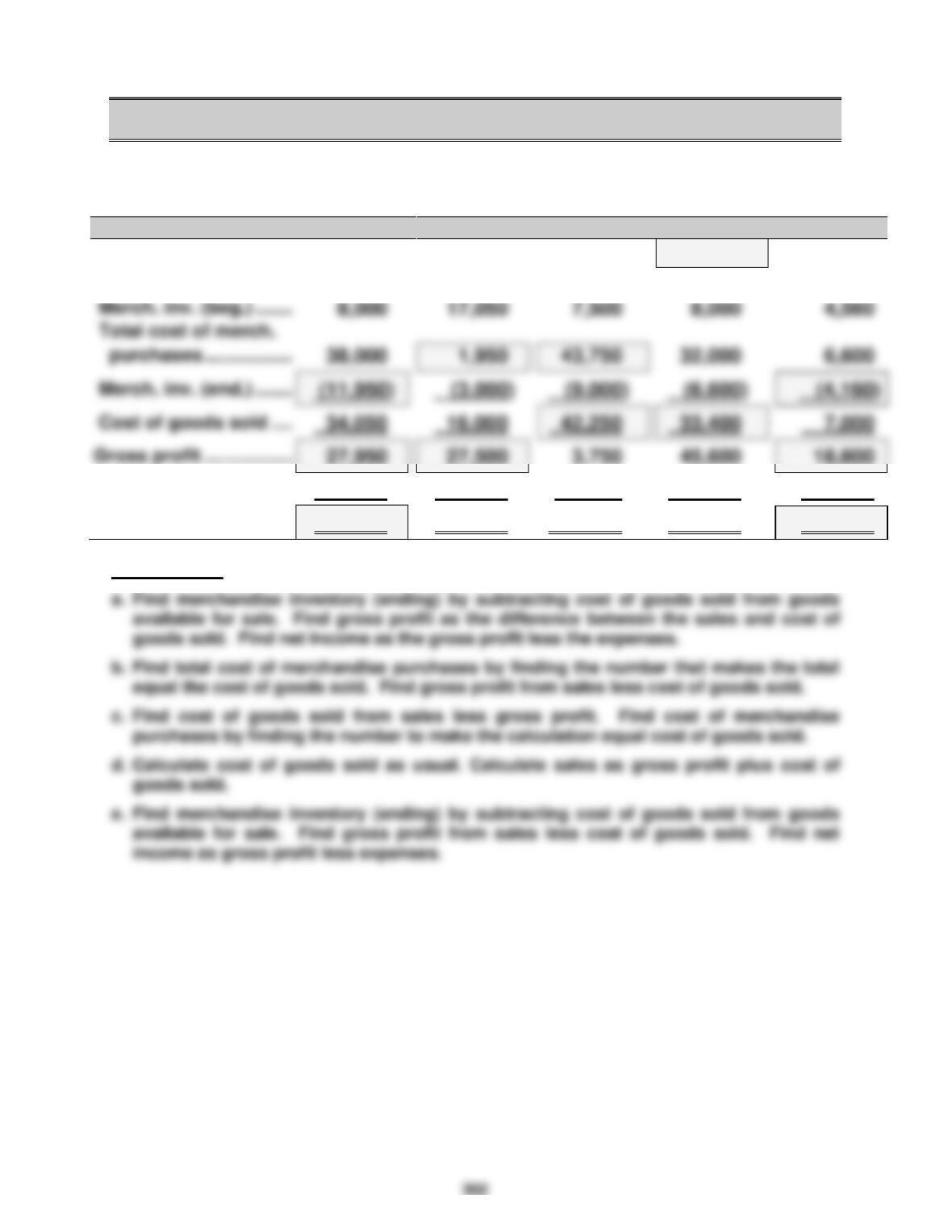

Exercise 5-1 (30 minutes)

Note: The original missing numbers are blocked.

(a)

(b)

(c)

(d)

(e)

Sales ……………………….

$62,000

$43,500

$46,000

$79,000

$25,600

Cost of goods sold

Merch. inv. (beg.) …….

Total cost of merch.

Merch. inv. (end.) …….

(11,950)

(9,000)

(6,600)

Expenses …………………

10,000

10,650

12,150

3,600

6,000

Net income (loss) ……..

$17,950

$16,850

$ (8,400)

$42,000

$12,600

Explanations:

303

Exercise 5-2 (10 minutes)

Operating cycle of a merchandiser with credit sales follows (chronological):

2 (a) prepare merchandise for sale

Exercise 5-3 (30 minutes)

Apr. 2 Merchandise Inventory …………………………..….. 4,600

Accounts Payable—Lyon …………………….. 4,600

Purchased merchandise on credit.

304

Exercise 5-4 (30 minutes)

SELLER—Allied

May 3 Merchandise Inventory …………………………..….. 20,000

305

Exercise 5-5 (15 minutes)

BUYER—Macy

May 3 No entry for buyer.

May 5 Merchandise Inventory …………………………..…. 21,000

Accounts Payable ………………………………. 21,000

Exercise 5-6 (30 minutes)

1. BUYER– Santa Fe

a) Credit Purchase

Merchandise Inventory …………………………..…. 24,000

Accounts Payable ………………………………. 24,000

2. SELLER – Mesa

a) Credit Sale

Accounts Receivable …………………………..……. 24,000

Sales ………………………………………………….. 24,000

Exercise 5-7 (25 minutes)

1. Entries for Sydney (BUYER):

May 11 Merchandise Inventory ………………………….... 40,000

Accounts Payable ……………………………… 40,000

Purchased goods.

2. Entries for Troy (SELLER):

May 11 Accounts Receivable ……………………………….. 40,000

Sales …………………………………………………. 40,000

Sold goods.

11 Cost of Goods Sold ………………………………….. 30,000

308

Exercise 5-8 (30 minutes)

Merchandise Inventory

Balance, Dec. 31, 2016 …………..

25,000

Purchase discounts received …………………………..

1,700

Shrinkage ……………………………………………………….

Exercise 5-9 (20 minutes)

PERPETUAL

Nov. 1 Merchandise Inventory ………………………………. 1,500

Accounts Payable ……………………………….. 1,500

Record purchases, terms 2/5, n/30.

Nov. 13 Accounts Receivable …………………………………. 1,600

Sales …………………………………………………… 1,600

Record sale of goods, terms n/30.

Cost of Goods Sold ……………………………………. 800

Merchandise Inventory ………………………… 800

310

Exercise 5-10 (25 minutes)

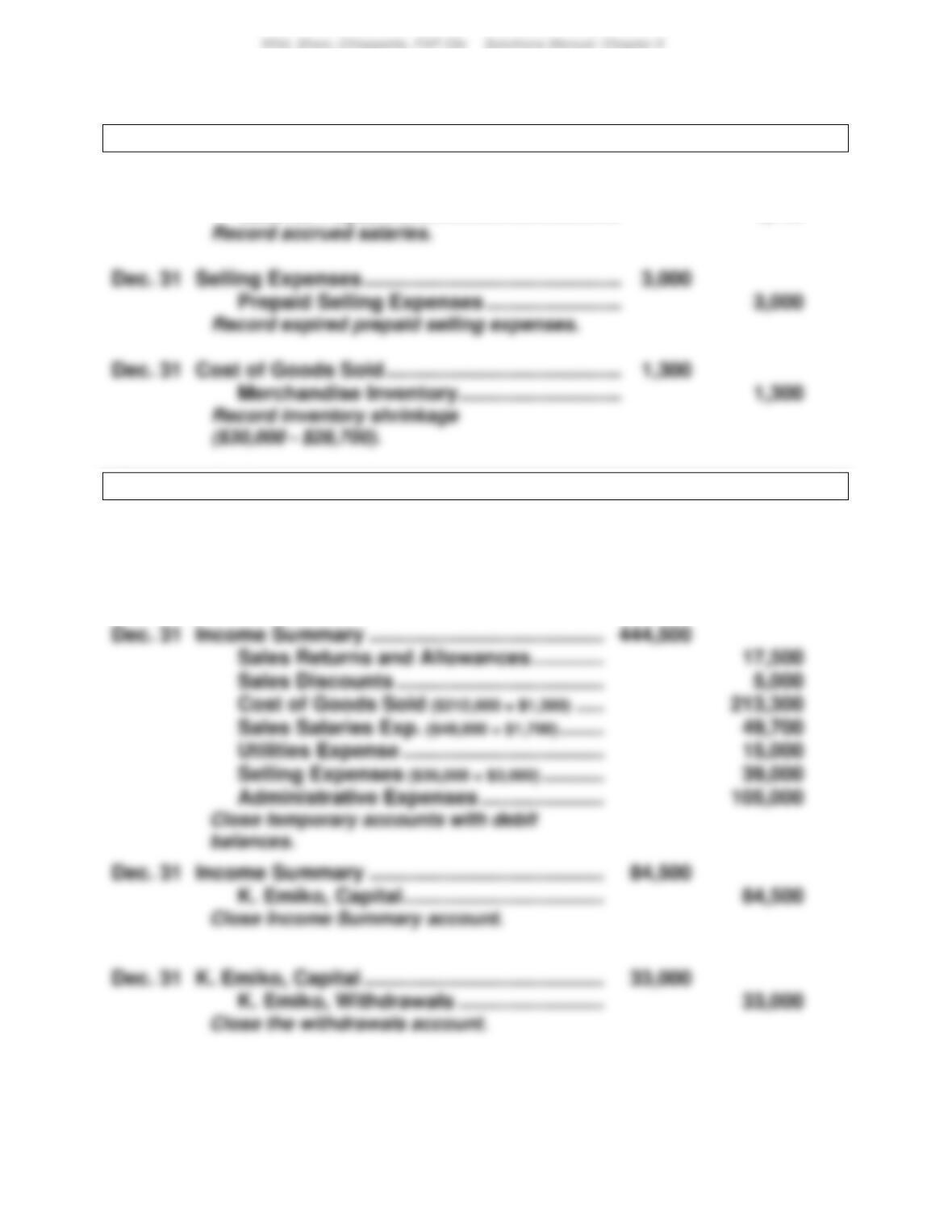

Adjusting entries

Dec. 31 Sales Salaries Expense …………………………….. 1,700

Salaries Payable…………………………………. 1,700

Closing entries

Dec. 31 Sales …………………………………………………….. 529,000

Income Summary …………………………….. 529,000

Close temporary accounts with credit

balances.