PROBLEM 5-7A

ERMLER DEPARTMENT STORE

Income Statement (Partial)

For the Year Ended November 30, 2014

Sales

Sales revenue …………………….. $902,000

Less: Sales returns and

allowances ……………….. 20,000

Net sales …………………………………… 882,000

Cost of goods sold

Inventory, Dec. 1, 2013 ………… $ 41,300

PROBLEM 5-8A

(a)

(a) Cost of goods sold = Sales revenue – Gross profit

(c) Merchandise inventory = 2012 Inventory + Purchases – CGS

= $13,000 + $25,890 – $29,090 = $9,800

(d) Cash payments to suppliers = 2012 Accounts payable + Purchases

(f) Operating expenses = Gross profit – Net income

= $59,620 – $3,510 = $56,110

(g) 2013 Inventory + Purchases – 2014 Inventory = CGS

Purchases = CGS – 2013 Inventory + 2014 Inventory

(h) Cash payments to suppliers = 2013 Accounts payable + Purchases –

2014 Accounts Payable

(i) Gross profit = Sales revenue – CGS

PROBLEM 5-8A (Continued)

(k) 2014 Inventory + Purchases – 2015 Inventory = CGS

Inventory = 2014 Inventory + Purchases – CGS

(b) No. A decline in sales does not necessarily mean that profitability

declined. Profitability is affected by sales, cost of goods sold and

operating expenses. If cost of goods sold or operating expenses decline

more than sales, profitability can increase even when sales decline.

*PROBLEM 5-9A

(a)

General Journal

Date Account Titles and Explanation Debit Credit

Apr. 5 Purchases ………………………………………………. 1,500

Accounts Payable ………………………….. 1,500

10 Accounts Receivable ………………………………. 1,340

Sales Revenue ……………………………….. 1,340

12 Purchases ………………………………………………. 830

Accounts Payable ………………………….. 830

17 Accounts Payable …………………………………… 30

Purchase Returns and

Allowances …………………………….

30

20 Accounts Receivable ………………………………. 810

Sales Revenue ……………………………….. 810

*PROBLEM 5-9A (Continued)

Date

A

ccount Titles and Explanation Debit Credit

Apr. 27 Sales Returns and Allowances……………….. 80

(b)

Cash

4/1 Bal. 2,500

4/7 80

Inventory

4/1 Bal. 3,500

Common Stock

4/1 Bal. 6,000

4/27 80

4/30 Bal. 80

*PROBLEM 5-9A (Continued)

Purchase

Returns and Allowances

4/9 200

Purchase Discounts

4/14 39

(c)

FLINT HILLS PRO SHOP

Trial Balance

April 30, 2014

Debit Credit

Cash ………………………………………………………….. $1,587

Accounts Receivable ………………………………….. 850

Inventory ……………………………………………………. 3,500

*PROBLEM 5-9A (Continued)

(d)

FLINT HILLS PRO SHOP

Income Statement (Partial)

For the Month Ended April 30, 2014

____________________________________________________________

Sales

Sales revenue …………………….. $2,150

Less: Sales returns and

allowances ……………….. 80

Net sales …………………………….. 2,070

Cost of goods sold

Inventory, April 1 ………………… $3,500

Purchases ………………………….. $2,330

Less: Purchase returns

and allowances ………… $230

Purchase discounts. …. 47 277

PROBLEM 5-1B

(a)

General Journal

Date Account Titles Debit Credit

Apr. 2 Inventory ………………………………………………….

Accounts Payable ……………………………..

8,700

8,700

4 Accounts Receivable ………………………………..

6,000

13 Cash ………………………………………………………..

Sales Discounts ($6,000 X 2%) ………………….

Accounts Receivable …………………………

5,880

120

6,000

14 Inventory ………………………………………………….

Cash …………………………………………………

4,700

4,700

PROBLEM 5-1B (Continued)

General Journal

Date Account Titles Debit Credit

Apr. 23 Cash ……………………………………………………….

Sales Revenue …………………………………

8,300

8,300

27 Accounts Payable……………………………………

Cash ………………………………………………..

Inventory ($5,500 X 2%) …………………….

5,500

5,390

110

PROBLEM 5-1B (Continued)

(b)

Cash

4/1 Bal. 10,000

4/5 200

Accounts Receivable

4/4 6,000

4/30 3,980

4/13 6,000

4/30 Bal. 3,980

Inventory

4/2 8,700

4/4 3,700

Accounts Payable

4/6 400

4/2 8,700

Sales Revenue

4

/

4 6,000

Sales Discounts

4/13 120

4/30 Bal. 120

Freight-Out

4/5 200

4/30 Bal. 200

PROBLEM 5-1B (Continued)

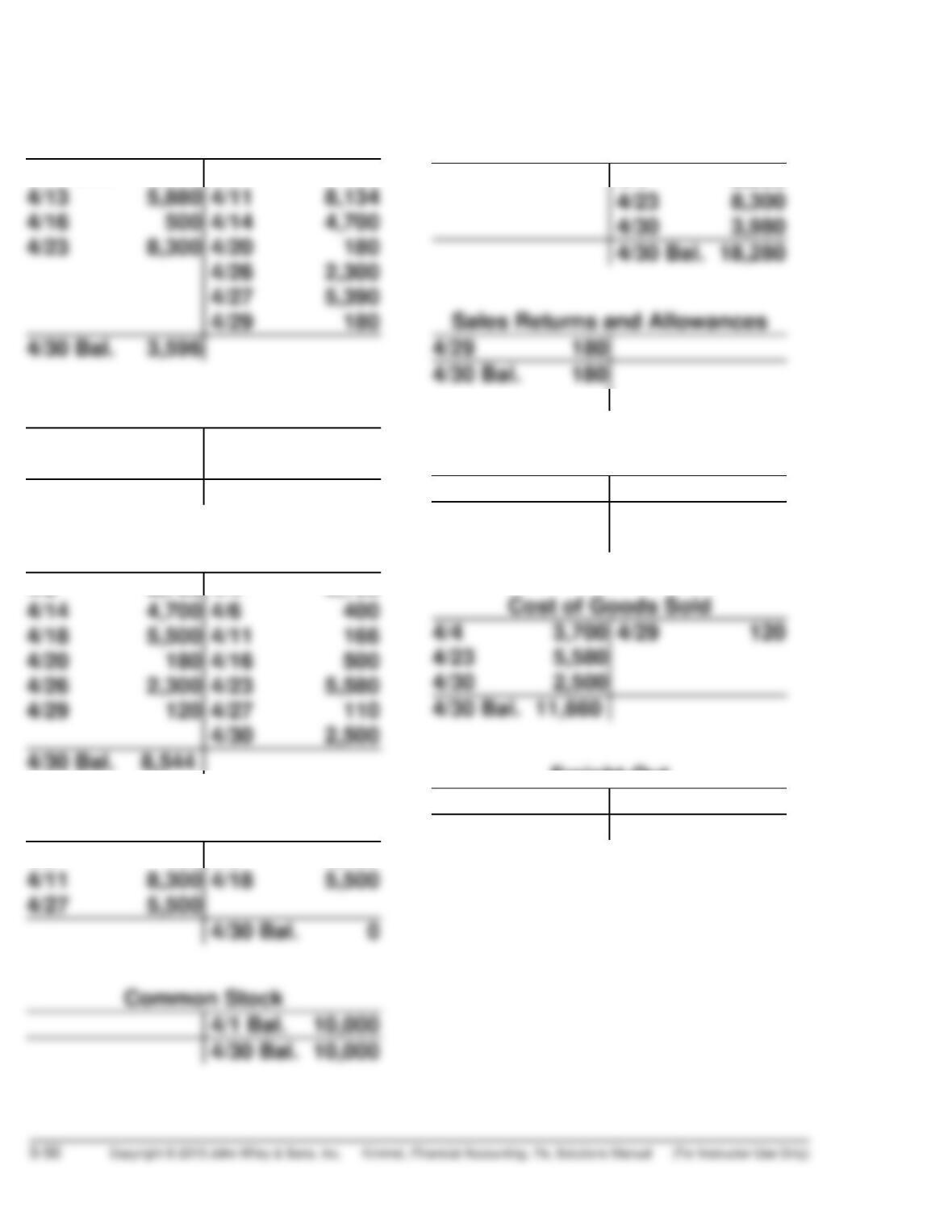

(c) KREY DISTRIBUTING COMPANY

Income Statement (Partial)

For the Month Ended April 30, 2014

Sales

Sales revenue …………………………………………….. $18,280

Less: Sales returns and allowances …………… $180

Sales discounts ……………………………….. 120 300

PROBLEM 5-2B

April 1 Inventory (190 X $6) ………………………………………. 1,140

Accounts Payable ………………………………….. 1,140

3 Accounts Receivable (40 X $10) …………………….. 400

13 Accounts Receivable (25 X $12) …………………….. 300

Sales Revenue ………………………………………. 300

Cost of Goods Sold (25 X $6) ………………………… 150

Inventory ……………………………………………….. 150

20 Inventory (200 X $6) ………………………………………. 1,200

Accounts Payable ………………………………….. 1,200

24 Cash …………………………………………………………….. 300

PROBLEM 5-3B

(a)

General Journal

Date Account Titles Debit Credit

Apr. 4 Inventory ………………………………………………….

.

Accounts Payable ……………………………..

.

980

980

6 Inventory ………………………………………………….

.

.

.

.

60

13 Accounts Payable ($980

–

$130) ……………….

.

Cash …………………………………………………

.

Inventory ($850 X 2%) ………………………..

.

850

833

17

14 Inventory ………………………………………………….

.

Accounts Payable ……………………………..

.

1,300

1,300

15 Cash ………………………………………………………..

.

.

.

50

PROBLEM 5-3B (Continued)

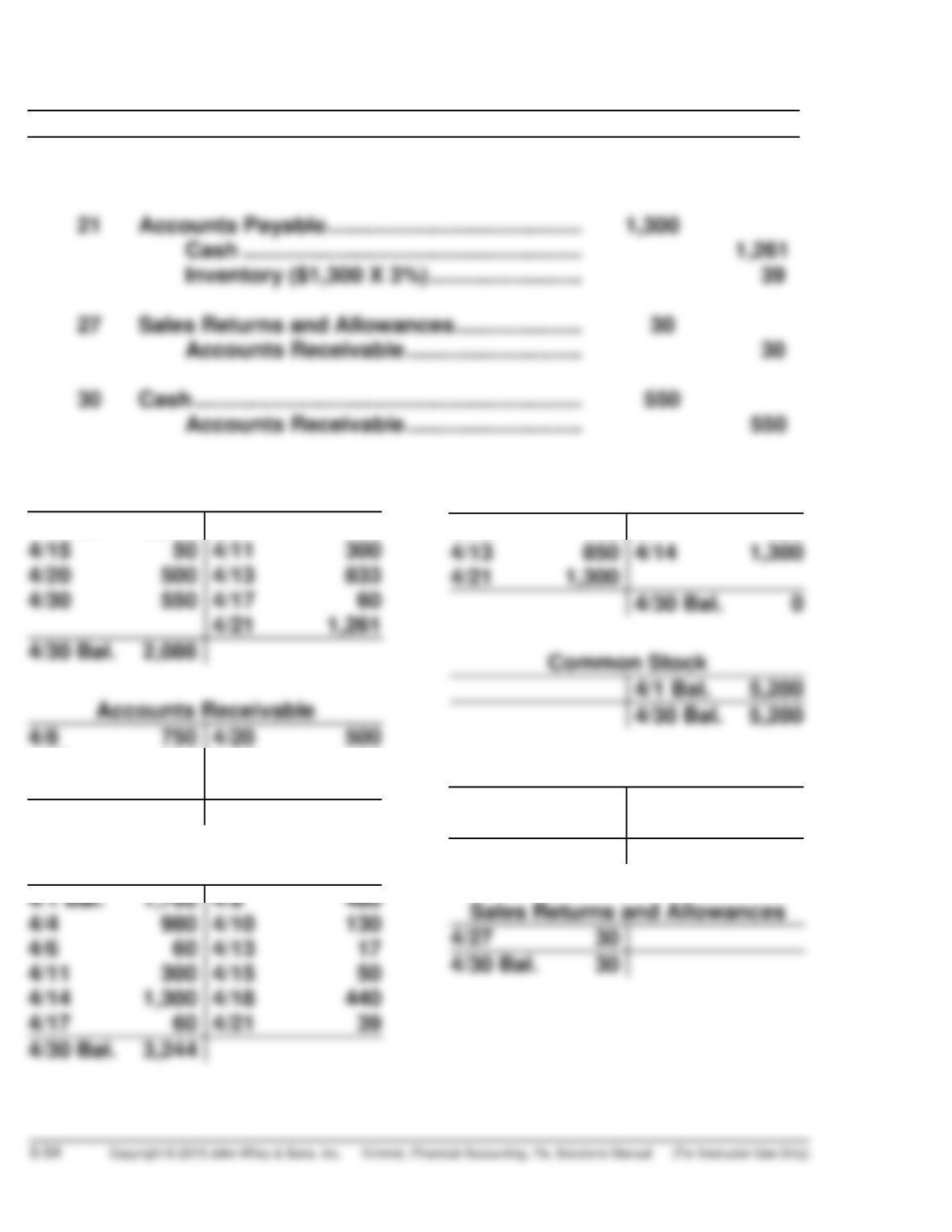

Date Account Titles Debit Credit

Apr. 20 Cash ……………………………………………………….

Accounts Receivable ………………………..

500

500

(b)

Cash

4/1 Bal. 3,500

4/6 60

4/18 660

4/27 30

4/30 550

4/30 Bal. 330

Inventory

A

ccounts Payable

4/10 130

4/4 980

Sales Revenue

4/8 750

4/18 660

4/30 Bal. 1,410

PROBLEM 5-3B (Continued)

Cost of Goods Sold

(c) CONNORS’ TENNIS SHOP

Trial Balance

April 30, 2014

Debit Credit

Cash ……………………………………………………………….

$2,086

(d) CONNORS’ TENNIS SHOP

Income Statement (Partial)

For the Month Ended April 30, 2014

PROBLEM 5-4B

(a) PARKER DEPARTMENT STORE

Income Statement

For the Year Ended December 31, 2014

Sales

Sales revenue ………………………………… $626,000

Less: Sales returns and

Operating expenses

Salaries and wages expense …………… $111,000

Depreciation expense …………………….. 23,400

Utilities expense …………………………….. 11,000

Insurance expense …………………………. 8,400

Maintenance and repairs expense …… 6,200

Total operating expenses ………… 160,000

PARKER DEPARTMENT STORE

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, January 1 …………………………………………………. $19,200

Add: Net income ………………………………………………………………….. 28,300

PROBLEM 5-4B (Continued)

PARKER DEPARTMENT STORE

Balance Sheet

December 31, 2014

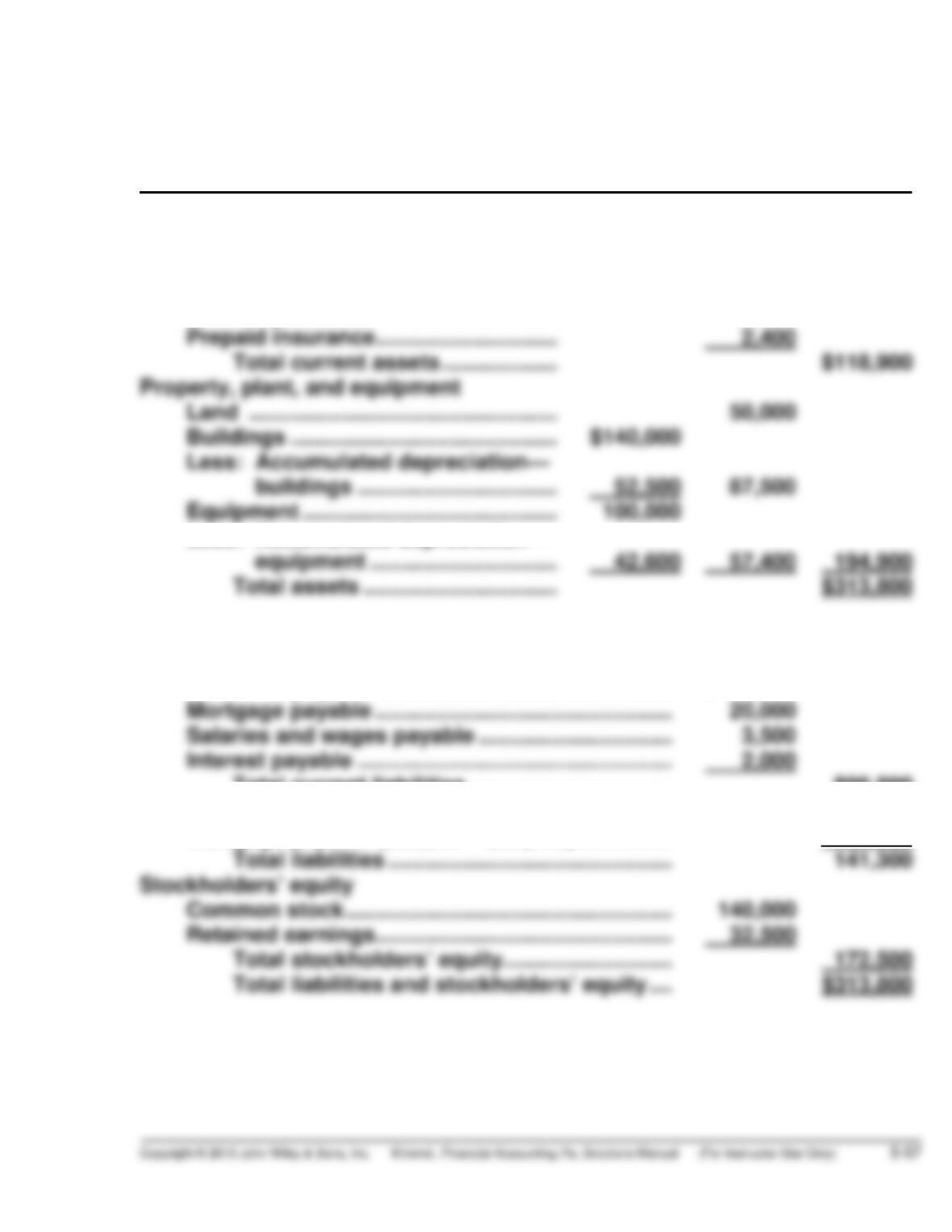

Assets

Current assets

Cash ……………………………………………. $ 30,000

Accounts receivable …………………….. 43,500

Inventory ……………………………………… 43,000

Less: Accumulated depreciation—

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………………………. $ 73,300

Total current liabilities ……………………………. $98,800

Long-term liabilities

Mortgage payable ($62,500 – $20,000) ……………. 42,500

PROBLEM 5-4B (Continued)

(b) Profit margin: $28,300 ÷ $618,000 = 4.6%

(c) Revised net income = Current net income + increase in gross profit –

increase in operating expenses

Revised gross profit rate: $256,500 ÷ $772,500 = 33.2%

This plan increases net sales and gross profit but barely changes the

gross profit rate. This is not surprising since the proposed change

affects selling expenses rather than cost of goods sold. An increase in

PROBLEM 5-5B

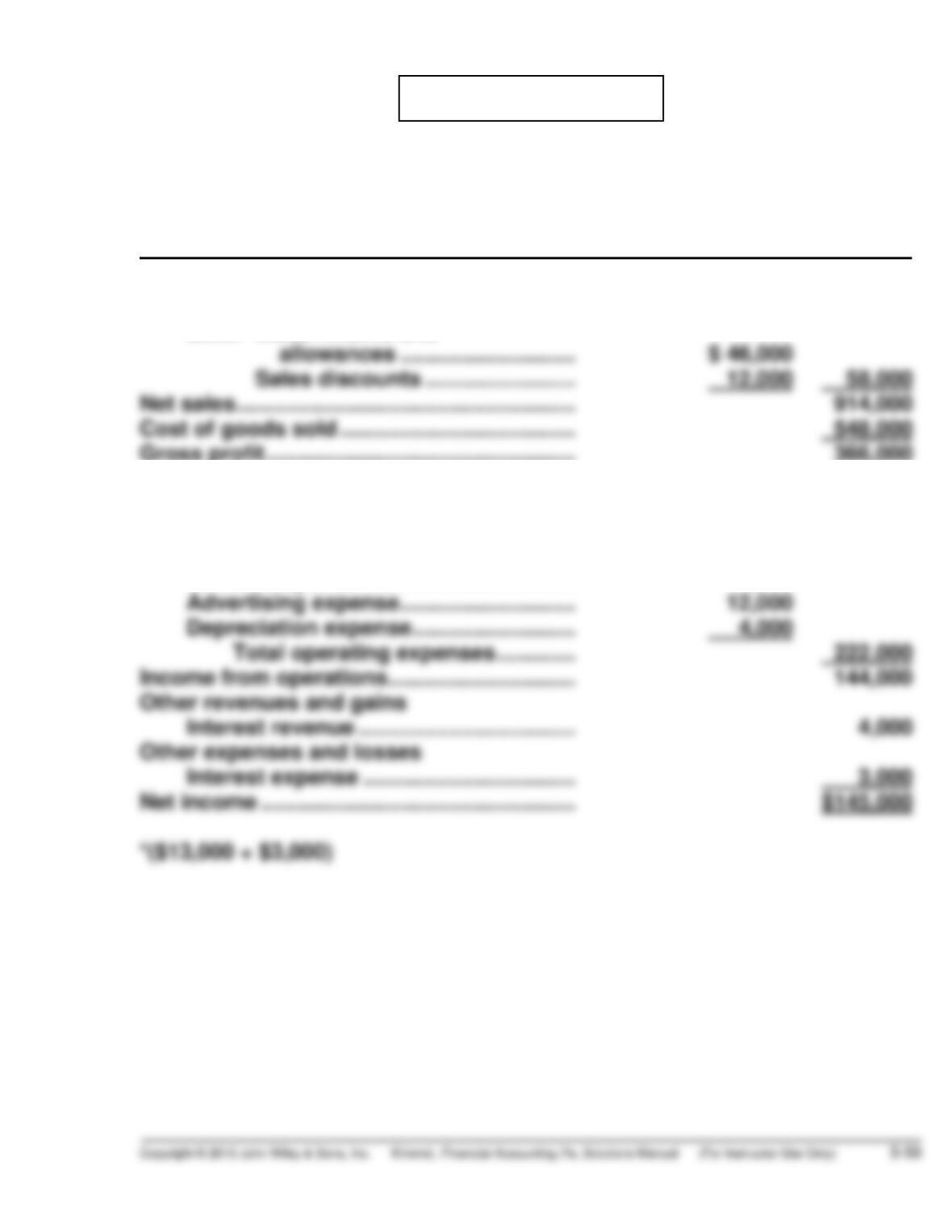

WRIGHT COMPANY

Income Statement

For the Year Ended December 31, 2014

Sales

Sales revenue …………………………………. $972,000

Less: Sales returns and

Gross profit …………………………………………… 366,000

Operating expenses

Salaries and wages expense …………… 152,000

Freight-out ……………………………………… 20,000

Rent expense ($20,000 – $2,000) ……… 18,000

Utilities expense …………………………….. 16,000*

PROBLEM 5-6B

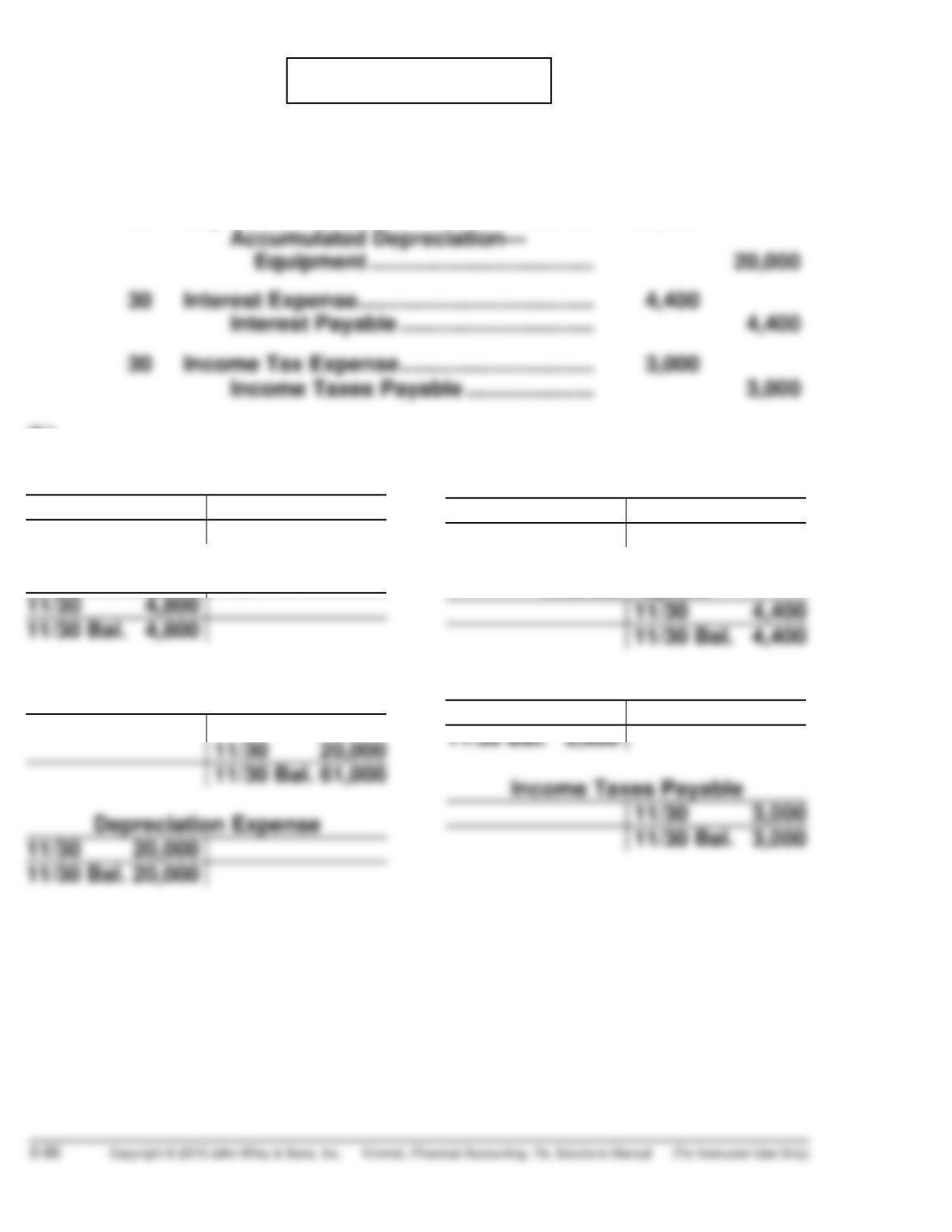

(a) Nov. 30 Supplies Expense ………………………………. 4,800

Supplies ($8,800 – $4,000) …………… 4,800

30 Depreciation Expense ………………………… 20,000

(b)

Supplies

11/30 Bal. 8,800 11/30 4,800

11/30 Bal. 4,000

Supplies Expense

Accumulated Depreciation

—

Equipment

11/30 Bal. 41,000

Interest Expense

11/30 4,400

11/30 Bal. 4,400

Interest Payable

Income Tax Expense

11/30 3,000