Chapter 5

5.1 The credit analyst is concerned with the ability of the borrower to

repay interest and principal on loans. Questions raised in a credit analysis

5.2 Financial ratios can serve as screening devices, indicate areas of

potential strength or weakness, and reveal matters that need further

investigation. But financial ratios do not provide answers in and of

5.3 Liquidity ratios measure a firm’s ability to meet cash needs as they

arise. Activity ratios measure the liquidity of specific assets and the

5.4 The Du Pont System helps the analyst see how the firm’s decisions

and activities over the course of an accounting period interact to produce an

overall return to the firm’s shareholders. By reviewing the relationships of a

series of financial ratios, the analyst can identify strengths and weaknesses

5.5

Current Ratio

725,000

475,000

1.53 times

Quick Ratio

400,000

475,000

0.84 times

Average Collection Period

275,000

Inventory Turnover

1,200,000

325,000

3.69 times

Fixed Asset Turnover

1,500,000

420,000

3.57 times

Total Asset Turnover

1,500,000

1,145,000

1.31 times

Debt Ratio

875,000

1,145,000

76.4 %

Times Interest Earned

200,000

2.78 times

Gross Profit Margin

300,000

Net Profit Margin

76,800

1,500,000

5.1 %

Return on Total Assets

76,800

1,145,000

6.7 %

Return on Equity

76,800

270,000

28.4 %

Capital asset efficiency is in good shape, as evidenced by an improving and

above average fixed asset turnover. The efficient management of fixed assets

approximately offsets the poor inventory turnover, and the total asset

turnover is only slightly weaker than the industry.

The return on investment, which has declined and is below the industry

average, reflects decreasing profitability and the overstocking of inventory.

Return on equity is above the industry average and is trending upward.

Although the high debt ratio improves the return on equity, it also increases

risk. The increased use of financial leverage has more than offset the

decrease in profitability:

Net Profit

Margin

x

Total Asset

Turnover

=

Return on

Investment

5.6 Luna’s current ratio has increased and is above the industry average,

the average collection period has shortened and is less than the industry

average, and the inventory turnover ratio has improved; the ratios indicate

that Luna has no obvious problems with liquidity or the management of

5.7

(a) FIFO

(b) LIFO

Gross profit margin

53.3

3

%

25.8

3

%

Operating profit margin

33.3

3

%

5.8

3

%

Net profit margin

19.9

3

%

2.0

6

%

Current ratio

1.6

1

1.1

0

Quick ratio

0.7

7

0.7

7

4

the future. The difference in profit margins has resulted from a “paper”

profit recorded under the FIFO method.

Ending inventory is undervalued when LIFO is used during inflation. The

FIFO valuation is a better reflection of the current market price of Rare

Metals, Inc.’s inventory. As a result the current ratio of 1.61 is a more

accurate representation than 1.10. The quick ratios are identical because

inventory has been eliminated from the calculation, and inventory is the only

difference in the numbers being compared.

(d) Yes, cash flow from operating activities will differ due to the

difference in taxes paid. Assuming that the inventory method is the only

5.8

(a) XYZ is more liquid than ABC. XYZ’s current and quick ratios are

both above one and the cash-flow liquidity ratio is close to one, indicating

the company should be able to pay current liabilities as they come due.

ABC’s liquidity ratios are all below one. It appears that ABC must find

ABC generates higher operating and net profits than XYZ, and therefore has

higher return on assets and equity ratios. The return on equity ratio is

extremely high due to the fact that ABC uses a significant amount of debt

(76%) and is generating sufficient returns to cover the cost of the debt.

XYZ, while not as profitable, is translating their profits into cash much

better than ABC.

(b)

ABC

XYZ

Stock Price

EPS

$41

$4.59

$35

$1.19

PE Ratio

8.9

29.4

The PE ratio indicates the value being placed by the stock market on a

5.9

Current

Quick

Net Wk. Capital

Debt

(a)

D

N

N

I

(b)

N

N

N

N

(c)

I

I

I

D

D

D

D

N

(e)

D

N

D

I

(f)

N

N

N

N

(g)

I

I

I

I

(h)

I

I

I

D

(i)

N

N

N

D

(j)

N

D

N

N

(k)

D

D

N

I

(l)

I

N

N

D

The instructor might want to discuss why a firm would make a specific

5.10

(a)

Debt

Equity

Debt Ratio*

40+10

90+10

= 50%

40

90+10

= 40%

4.8+1.5

= 2.86 x

18

= 3.75x

Operating Profit

Interest Expense

Earnings before tax

Net Income

Shares Outstanding

800,000

1,000,000

Earnings per share

$8.78

$7.92

Return on Equity

7,020

50,000

= 14.04%

7,920

60,000

= 13.20%

100,000

14.04

10.80

= 1.3

13.20

10.80

= 1.2

7

(b) Use of debt would increase the debt ratios from 44% to 50%, while

equity financing would reduce the debt ratio to 40%. Interest coverage

would decline from 3.1 times to 2.86 times if debt is employed; times

interest earned would increase to 3.75 times with stock financing. Earnings

per share would be higher with the debt financing. The financial leverage

index is greater than 1, indicating the successful use of financial leverage

under either alternative, but is higher with debt financing.

5.11 At first glance, it appears that Walmart has poor short-term liquidity.

The current, quick and cash flow liquidity ratios are all below 1.0. This

means the firm does not have as many current assets or liquid items to cover

current liabilities. The quick ratio is especially low due to the large amount

of inventories Walmart must have to stock its stores. The cash flow liquidity

ratio is decreasing as a result of cash flow from operations decreasing from

2013 to 2014.

5.12 Republic Airways has a risky capital structure. The overall debt has

decreased slightly to 83.2% and long-term debt remains stable at 77%. The

interest (accrual-based and cash-based) and fixed charge coverage ratios are

low, but have improved from 2012 to 2013. An increase in operating profit

may have contributed to an increase in cash flow from operations. Cash flow

Operating profit has improved, but net profit has declined. Since revenues

have decreased, the company has been more efficient in managing their

operating expenses. The lower net profit could be caused by large interest

expense. Cash flow margin and cash return on assets have improved over the

past year which is positive and a result of the increasing cash flow from

5.13 Writers of the 2016 annual report will probably want to emphasize

rebounding in 2016 from an abnormal year in 2015. They will want to point

out reasons for the improvement in 2016, showing how the company is

5.14 There is no solution presented for this problem since students will

choose different industries. Having students share what they have learned

from their research can lead to interesting discussions.

5.15 There is no solution presented for this problem since students will

Case 5.1

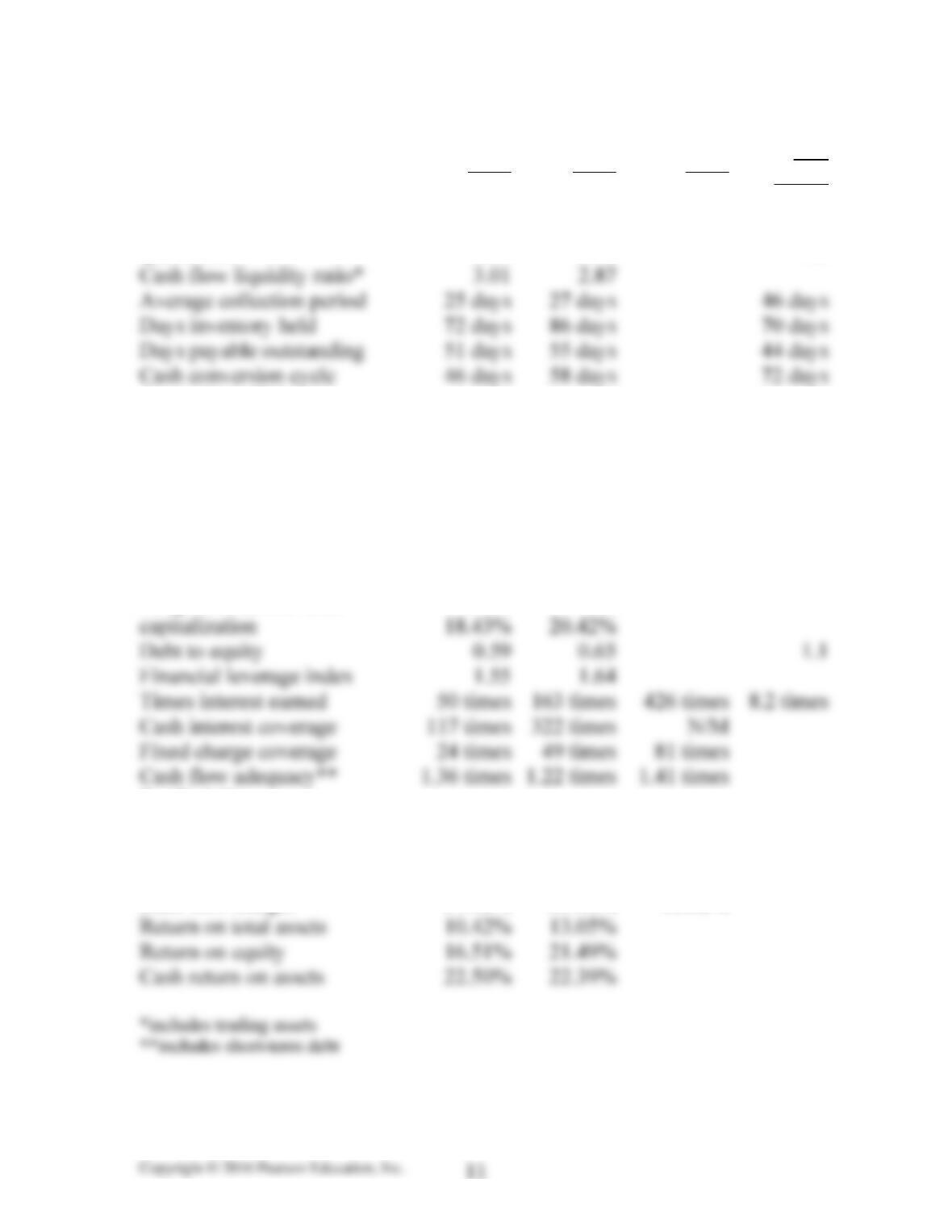

(a) and (b)

2013

2012

2011

Ind.

Avg.*

Short-term liquidity

Current ratio

2.36

2.43

2.2

Quick ratio

2.06

2.06

1.2

Cash flow liquidity ratio*

3.01

2.87

Average collection period

25 days

Days inventory held

Days payable outstanding

Cash conversion cycle

58 days

Operating efficiency

Accounts receivable turnover

14.71

13.92

8.0

Inventory turnover

5.08

4.26

5.2

Accounts payable turnover

7.14

6.68

8.3

Fixed asset turnover

1.68

1.91

15.2

Total asset turnover

.57

.63

1.5

Leverage

Debt ratio

36.92%

39.30%

49.7%

18.43%

20.42%

Debt to equity

1.1

Financial leverage index

Times interest earned

Cash interest coverage

N/M

Fixed charge coverage

Cash flow adequacy**

Long-term debt to total

Profitability

Gross profit margin

59.80%

62.15%

62.51%

28.7%

Operating profit margin

23.32%

27.44%

32.37%

1.6%

Net profit margin

18.25%

20.63%

23.97%

Cash flow margin

39.42%

35.40%

38.82%

Return on total assets

10.42%

13.05%

Return on equity

16.51%

21.49%

Cash return on assets

22.50%

22.39%

2013

2012

2011

Ind.

Avg.

Market measures

Earnings per share

$1.94

$2.20

$2.46

Closing price

$25.60

$20.23

$24.25

* Industry average is from The Risk Management Association, Annual

Statement Studies, 2013; NAICS 334413

(c) As requested, an evaluation of Intel has been completed. The following

Short-term Liquidity

Intel’s short-term liquidity is impressive. The current and quick ratios are

both above two and higher than the industry average. The cash-flow

liquidity ratio increased due to the increases in liquid assets and increasing

cash from operations. Intel has a significant amount of cash and short-term

investments and, therefore, should not have problems paying debt as it

comes due. This company has no problem generating cash from operations

as evidenced by the statement of cash flows.

Days inventory held has decreased significantly and is now just two days

above the industry average. It is important for Intel to decrease inventory

days because of the rapid obsolescence of products in the high technology

industry.

Days payable outstanding has decreased indicating Intel is paying suppliers

faster, but still takes longer than the competition. It is possible that Intel, due

to its excellent short-term liquidity, is better able than its competitors to

obtain more favorable credit terms from its suppliers.

Operating Efficiency

As discussed under short-term liquidity, Intel’s inventory turnover is better

in 2013 compared to 2012 and the firm is paying accounts payable faster.

new facility in Arizona which is currently not being used. The lack of

generation of sales after such a large investment is of concern.

Capital structure and long-term solvency

Intel has less debt than the competition. Cash and short-term investments

can easily cover all of Intel’s current liabilities and current assets cover 94%

of total liabilities.

Profitability

Revenues for Intel decreased in both 2013 and 2012 by 1.2%. Operating

costs increased in both years resulting in decreasing operating profit. Intel

has four segments for reporting purposes: the PC Client Group (PCCG), the

Data Center Group (DCG), the Other Intel Architecture segment (OIA) and

the Software and Services segment (SSG).

The decrease in revenues in 2012 was partially due to the fact that 2012 was

a 52 week year and 2011 was a 53 week year. In addition, volume was

decreasing due to the shift away from PCs to consumer demand for tablets.

The gross profit margin, stable in 2011 and 2012, decreased in 2013. The

Management Discussion and Analysis (MDA) explains that the decrease in

gross profit margin was a result of higher factory start-up costs primarily for

the next-generation 14nm process technology. To a lesser extent, lower

overall revenue from the OIA segment, primarily in the phone and mobile

component businesses and netbook group, as well as lower PCCG and DCG

platform revenue contributed to the decrease. These decreases were partially

offset by higher ISG platform revenue, lower PCCG and DCG platform unit

costs, and lower excess capacity charges. Higher (or lower) revenues caused

by volume increases (or decreases) result in higher (lower) gross profit

margins when firms have fixed costs. As a manufacturer Intel would have

significant fixed costs included in their cost of sales.

Intel is spending more on research and development costs (R&D) in 2012

and 2013 as they transition to new markets. Investments are being made

primarily in smartphones and tablets, as well as rewarding employees with

higher salaries in 2013, while in 2012 investments focused on not only

smartphones and tablets, but also, Ultrabook devices, and data centers.

Higher process development costs for 14nm process technology, higher

compensation expenses, costs of acquisitions, and higher costs related to the

development of 450mm wafer technology contributed to the 2012 R&D

increases. (pg. 37 of Form 10-K)

Intel has net overall gains from equity investments in all three years.

Although the amounts are insignificant they are growing each year as market

conditions improve. Interest and other, net, is a combination of

miscellaneous items including interest income and interest expense. Interest

income is stable year to year, however, interest expense has increased all

years as a result of the long-term debt taken out to repurchase the firm’s

common stock. (See Note 22, pg. 94 of the Form 10-K for detail of this

account.)

Net profit margin followed the downward trend of operating profit margin.

Return on assets and return on equity have declined due to the decreasing

profits and increasing assets and equity. To continue to be successful, Intel

must maintain good control of expenses, while continuing to develop cutting

edge products. In addition, Intel must be prepared to transition quickly when

changes in the technology market occur. With PCs and older technology

Market Measures

Earnings per share decreased all three years due to declining revenues and

increasing operating expenses. The stock price which dropped in 2012 has

rebounded in 2013. The PE ratio indicates investors are viewing Intel more

favorably in 2013.

Quality of Financial Reporting

Intel has disclosed key information as required in their annual report and

Form 10-K. Overall, the quality of financial reporting is good.

Strengths

Strong cash flow from operations

Solid short-term liquidity

Weaknesses

Reliance on three customers

Investment potential

Intel generates excellent cash flow, but needs to work on increasing

Creditworthiness

Intel’s solid short-term and long-term solvency combined with strong cash

flow from operations and an average debt ratio make this company a good

credit risk.

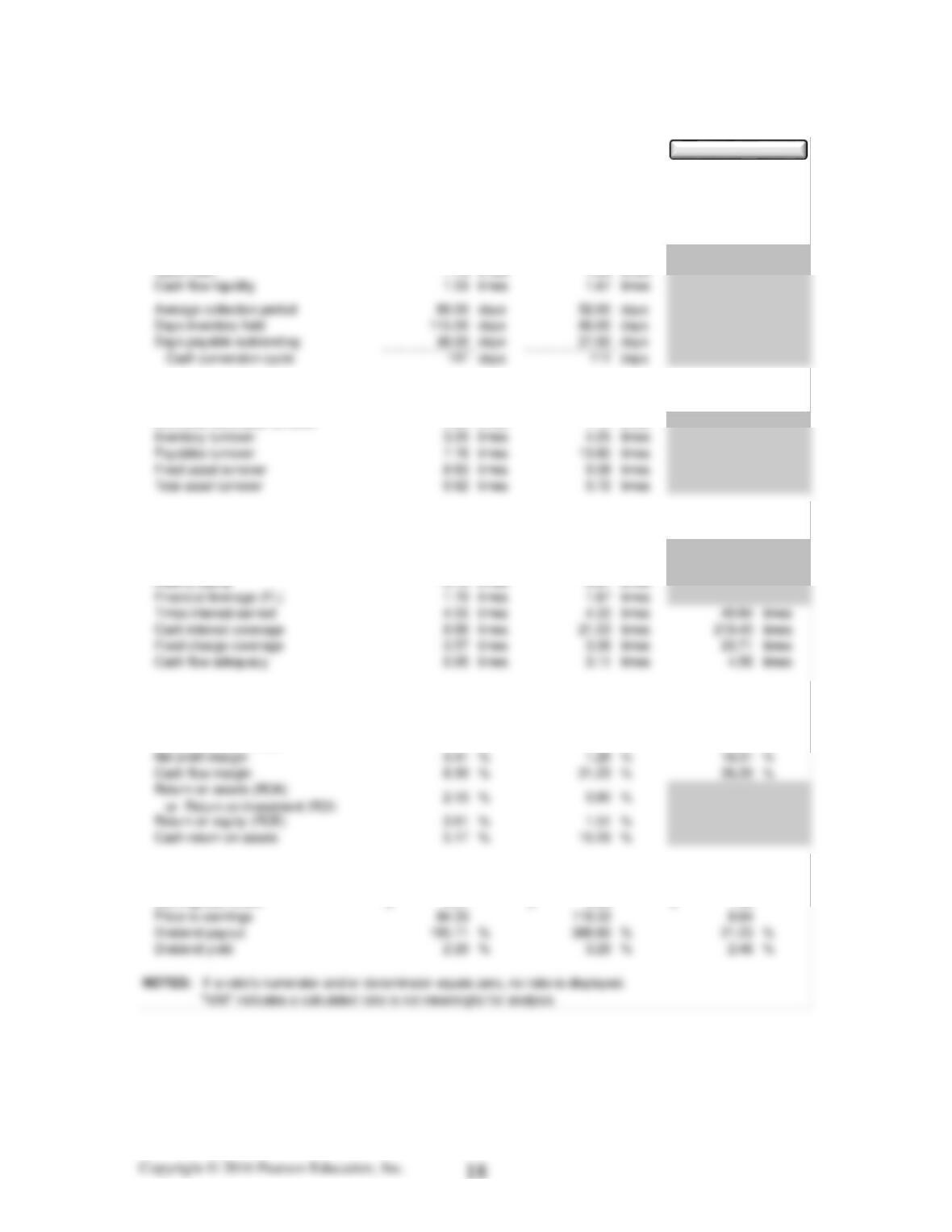

Case 5.2 (a)

Liquidity Ratios:

Current ratio 2.31 times 2.25 times

Activity Ratios:

Accounts receivable turnover 4.60 times 7.15 times

Leverage Ratios:

Debt ratio 41.14 % 40.22 %

Long–term debt to total capitalization 21.54 % 21.20 %

Profitability Ratios:

Gross profit margin 39.83 % 38.00 % 41.46 %

Operating profit margin 5.75 % 4.71 % 22.80 %

Market Ratios:

Earnings per share 0.21$ 0.09$ 1.46$

Applied Materials (AMAT / NASDAQ)

Summary of Financial Statement Ratios

Results for the Years Ending

Oct 27, 2013

Oct 28, 2012

Oct 30, 2011

Show Formulas

(b) Analysis of Applied Materials – 2013

Applied Materials (AMAT) manufactures equipment, and provides services

and software to the global semiconductor, flat panel display, solar

Short-term liquidity

AMAT’s current and quick ratios are above two and increasing. The cash

flow liquidity ratio decreased in 2013 due to a decrease in cash from

operating activities (CFO) caused by increasing accounts receivable and

Selected Income Statement Growth Rates:

Sales growth rate (13.88) %(17.10) %

Gross profit growth rate (9.72) %(24.01) %

NOTES: “N/M” indicates a calculated rate is not meaningful for analysis

2013 vs. 2012

2012 vs. 2011

Applied Materials (AMAT / NASDAQ)

Additional Ratio Analysis

Growth Rate Comparisons Between

Inventory days held increased twenty-nine days and at 115 days, seems high.

If this is a temporary increase due to demand and not stockpiling that may

result in obsolete products, the ratio should decrease in 2014. AMAT is

taking 21 days longer to pay suppliers. At 48 days this is not a problem and

is a good way for AMAT to keep money earning a return until absolutely

needed for paying bills. The cash conversion cycle is high at 147 days as a

result of increases in average collection period and days inventory held,

offset by the longer days payable.

Operating efficiency

The accounts receivable, inventory and accounts payable turnovers were

discussed under short-term liquidity. Fixed asset turnover has decreased due

Capital structure and long-term solvency

AMAT’s debt structure is good and ratios are stable with approximately half

of the debt short-term and half of the debt long-term. The only significant

borrowing was in 2011 to support the acquisition of Varian. Most cash

inflows are obtained from operations and short-term investments each year;

however, both of these sources have decreased in dollar amount from 2011

to 2013.