CHAPTER 4

Reporting Earnings and Financial Position

THINKING BEYOND THE QUESTION

How do we report earnings and financial position to stockholders?

Using common rules and formats is important so that decision makers

can compare results across companies and so they will have faith in the

QUESTIONS

Q4-1 Dividends are NEVER an expense. Dividends are a distribution of income,

not a component of it.

Q4-2 Students will have many responses but among them might be the follow-

ing:

a. What was the total selling price of goods and services sold this peri-

od?

b. What was the amount of gross profit this period?

92 Chapter 4

Q4-3 Students will have many responses but among them might be the follow-

ing:

a. What amount of cash did the firm have on hand at the end of the pe-

Q4-4 The primary reason is to maximize the amount of profit-related infor-

mation conveyed to users. By breaking the information into separate and

distinct categories, additional information is conveyed. Consider the op-

posite situation. At the extreme, one could report a one-section or even a

Q4-5 The purpose of consolidated financial statements is to report combined

financial information of the parent and its subsidiaries as if they were all

the same organization. Legally, they are separate corporations. But, be-

Reporting Earnings and Financial Position 93

Q4-6 In general, this statement is true. Income statement information is devel-

oped using accrual basis accounting. This means that sales revenue is

Q4-7 A classified balance sheet is one in which assets and liabilities are both

divided into subcategories. For example, a classified balance sheet might

Q4-8 The left side of a balance sheet reveals how an organization’s managers

have used investors’ capital. That is, what does the organization own? Or,

what amount of capital has been committed to which assets? The right

Q4-9 Only the ending balances of the stockholders’ equity accounts are re-

ported on the balance sheet. If the only information of interest was the

Q4-10 Preparation of the income statement, statement of stockholders’ equity,

and balance sheet occurs sequentially. This is because the results of

each statement are reported as components of the next statement. For

example, the income statement must be prepared before the statement of

94 Chapter 4

Q4-11 Articulation refers to the process by which information on one financial

Q4-12 Each of the three financial statements has a different purpose. The pur-

pose of the income statement is to report accrual-basis profitability in-

formation that covers a period of time. It does so by reporting revenues

Q4-13 When historical cost information is relatively recent, there is no meaning-

ful limitation. Over time, however, the cost of assets and liabilities tends

to lose relevance as the value of these items change. As an extreme ex-

Q4-14 Periodic measurement requires that financial reports be prepared for arbi-

trarily short time periods such as a quarter or a year. Transformation pro-

EXERCISES

E4-1 Definitions of all terms are listed in the glossary.

Reporting Earnings and Financial Position 95

E4-2

a.

Changes in a corporation’s

stockholders’ equity for a

fiscal period

Statement of stockholders’ equity

b.

The dollar amount of

resources available at a

Balance sheet

E4-3 1. I 9. I and SE

particular date

The amount of credit sales

Balance sheet

Accrual-based operating

results for a fiscal period

Income statement

The sources of finances

used to acquire resources

Balance sheet

stock on the amount of

contributed capital during

a period

The amount of profit

earned during a period

Income statement

96 Chapter 4

E4-4 Valentine Company

Income Statement

For the Month of September 2007

Sales revenue $48,500

E4-5 a. Gross profit:

Sales revenue $81,000

d. Pretax income:

Income from operations $78,000

Interest expense 7,500

Pretax income $70,500

Reporting Earnings and Financial Position 97

E4-6 a. Sales revenue (item 1) arises from the primary operating activities of

b. Gross profit (item 3) is the difference between the prices at which

c. Cost of goods sold (item 2), operating expenses (item 4), and other

expenses (item 7) are all categories of expense. Each represents re-

sources that were consumed to produce revenue.

d. Each of the items represents a different type of expense. Cost of

e. Income taxes (item 9) are an expense, as are cost of goods sold, op-

erating expenses, and other expenses. Businesses could not exist

E4-7 a. Primary source of revenue: transporting passengers.

98 Chapter 4

E4-8 a. Harley-Davidson earned $5,015,190,000 in revenues from selling

motorcycles in 2004.

b. Harley-Davidson earned $305,262,000 in revenues from providing

financial services in 2004.

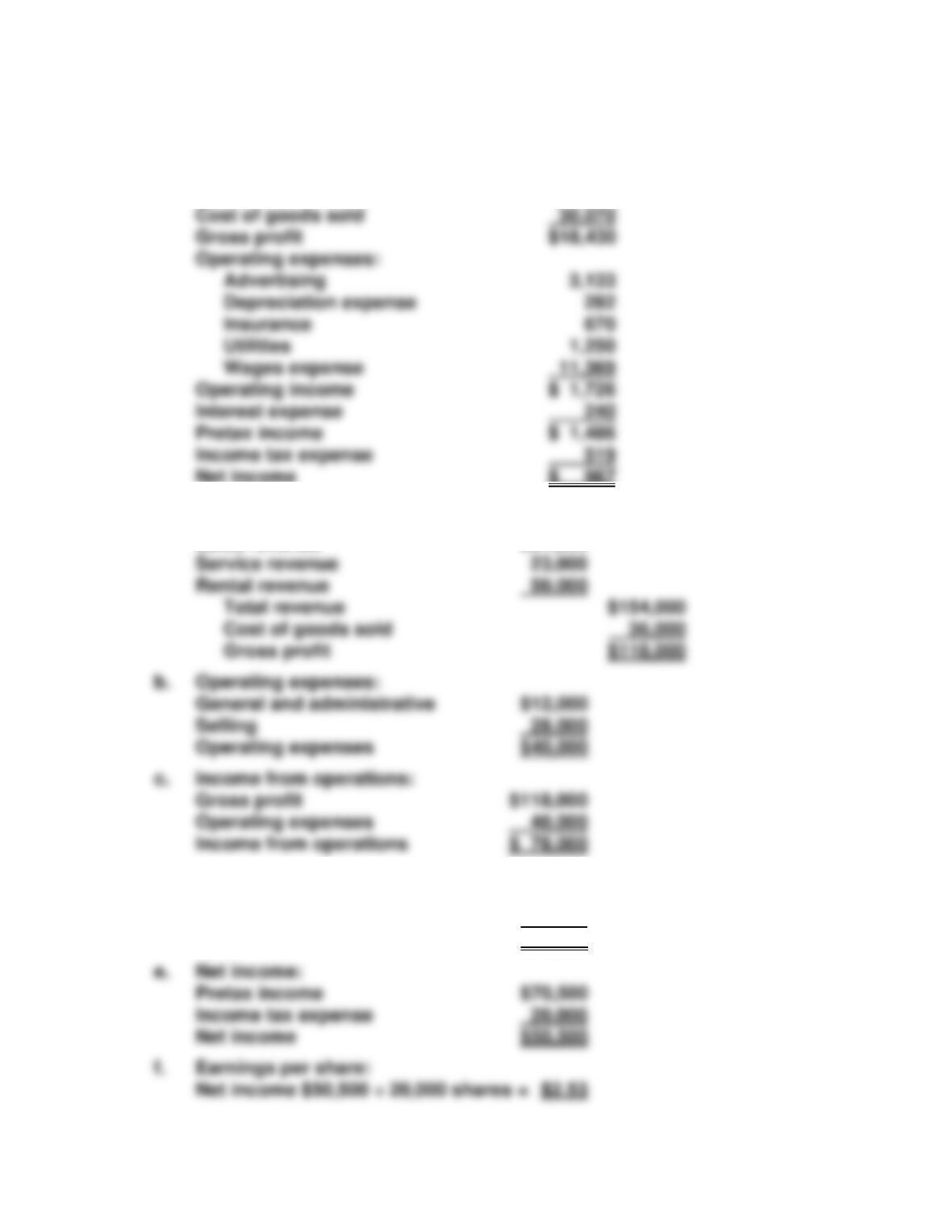

E4-9 a. Gross profit: $169,837

b. Product costs expensed = cost of sales: $549,313

E4–10 a. Ratio of net income to net revenues

b. Ratio of cost of revenues to net revenues

c. Ratio of operating expenses to net revenues

Reporting Earnings and Financial Position 99

e. Bio–Tek’s operating results improved between 2005 and 2006. Net in-

come increased by 57.4%. Revenues and earnings per share in-

E4–11 a. Current assets:

Cash $ 34,500

b. Current liabilities:

c. Property, plant, and equipment:

d. Total assets:

Current assets $ 592,600

100 Chapter 4

Total liabilities $790,600

g. Stockholders’ equity:

Contributed capital $ 700,000

Retained earnings 279,000

Stockholders’ equity $ 979,000

E4–12 Advances Unlimited

Balance Sheet

January 31

Assets

Current assets:

Accounts payable $ 275

Accrued expenses 348

Income taxes payable 93

Other current liabilities 46

Total current liabilities $ 762

Reporting Earnings and Financial Position 101

E4–13 Marvelous Enterprises

Balance Sheet

April 30

Assets

Current assets:

Cash $ 10,360

Accounts receivable 14,700

Other assets:

Copyrights and trademarks $ 5,000

Patents 3,300

Total liabilities $ 81,900

Stockholders’ Equity:

Contributed capital $ 38,770

Retained earnings* 11,740

Total stockholders’ equity $ 50,510

102 Chapter 4

E4–14 a. Current assets Current liabilities

Cash Accounts payable

Accounts receivable Interest payable

b. 1. Total current assets $1,936

E4–15

1. Gross profit:

2. Operating income:

Gross profit $243,000

3. Net income:

Operating income $111,000

5. Current assets:

Cash $ 35,000

Reporting Earnings and Financial Position 103

6. Property, plant and equipment:

Land $ 65,000

7. Other assets:

8. Total assets:

Current assets $190,000

9. Current liabilities:

Accounts payable $ 41,000

10. Working capital and working capital ratio:

Current assets $190,000

11. Total liabilities:

12. Retained earnings, December 31, 2007:

Retained earnings, December 31, 2006 $ 19,000

13. Total stockholders’ equity:

14. Total liabilities and stockholders’ equity:

Total liabilities $462,000

104 Chapter 4

E4–16

a.

Loss on sale of equip-

ment

Income statement

b.

Taxes payable

Balance sheet

c.

Trademark

Balance sheet

E4–17

Item

Financial Statement

Information Provided

1.

Accounts

receivable

Balance sheet

Cash to be received in the future

from prior sales

2.

Rent payable

Balance sheet

Cash to be paid in the future for

past usage of rental space

Retained earnings

Balance sheet and

Profits earned from past opera-

tions that have been reinvested

in the company

4.

Cost of sales

Income statement

Cost of resources consumed in

operations in the generation of

sales revenue during the operat-

ing period just ended

Prepaid rent

Balance sheet

Cost of rental resources paid for

in the past to be used in future

operations

Supplies expense

Income statement

Cost of supplies used in opera-

tions during the operating period

just ended

Accumulated other

comprehensive income

Statement of stockholders’ equity

e.

Current assets

Balance sheet

Investments

Balance sheet

g.

Rental revenue

Income statement

h.

Gross profit

Income statement

Earnings per share

Income statement

Accumulated deprecia-

tion

Balance sheet

k.

Net income

Income statement and statement of

Contributed capital

Balance sheet and statement of stock-

Operating income

Income statement

Common stock issued

Reporting Earnings and Financial Position 105

8.

Dividends

Stockholders’ equity

Cash paid and/or promised to

owners as a result of profitable

operations

11.

Accrued liabilities

Balance sheet

Cash to be paid in the future for

resources already consumed

12.

Wages payable

Balance sheet

Cash to be paid in the future for

labor services used in past op-

erations

operations

Notes payable

Balance sheet

Cash borrowed in the past, to be

repaid in the future

Service revenue

Income statement

The reward that has been earned

customers

16.

Inventory

Balance sheet

Cost of merchandise acquired in

the past to be sold in the future

Advertising

expense

Income statement

Cost of advertising services

consumed in operations during

the operating period just ended

ceived in the past in exchange

for shares of ownership in the

firm

E4–18 a. Articulation refers to the interrelationships among financial state-

ments. It is the process by which financial statements work together

9.

Depreciation

expense

Income statement

The portion of long-term fixed

assets that was consumed dur-

ing the period just ended

10.

Copyrights

Balance sheet

Cost of legal protection re-

sources acquired in the past to

be used in future operations

106 Chapter 4

E4–19 Crane Pool Corporation

Statement of Stockholders’ Equity

For the Year Ended June 30, 2007

Contributed

Capital

Retained

Earnings

Total

Balance at June 30, 2006

$657

$1,536

$ 2,193

E4–20 a. Marvelous Enterprises

Income Statement

For the Month Ended April 30

Sales revenue $26,000

Cost of goods sold 15,050

Gross profit $10,950

Reporting Earnings and Financial Position 107

b. Marvelous Enterprises

Statement of Stockholders’ Equity

For the Month Ended April 30

Contributed

Capital

Retained

Earnings

Total

PROBLEMS

P4-1 An example report follows:

THE PURPOSE OF FINANCIAL STATEMENTS

Report for A. Suliman

Corporations in the United States provide four primary financial state-

ments: a balance sheet, an income statement, a statement of cash flows,

and a statement of stockholders’ equity. The balance sheet identifies ma-

jor categories of assets, liabilities, and owners’ equity. Assets are classi-

fied as current assets, long-term investments, plant assets, and other as-

108 Chapter 4

A statement of cash flows identifies the change in cash during a fiscal pe-

riod. The change is explained by cash receipts and payments associated

A statement of stockholders’ equity describes changes in stockholders’

equity during a fiscal period. These changes include issuing or repur-

chasing stock, which affects the amount of contributed capital. They also

P4-2 A. Dating the sales in April rather than May will increase Green–Grow’s

sales revenue and net income for the fiscal year ending in April. Al-

B. Assuming the additional sales are sufficient, the company will meet

the banks’ net income and working capital ratio requirements.

C. The company’s president should consider alternatives that resolve

D. Flower is in a tough position, but not one in which she should com-

Reporting Earnings and Financial Position 109

P4-3 A. 1. Company is not identified (no company name in title)

2. Date expressed incorrectly (should be stated: For the year ending

December 31, 2007)

with net income.

B. Parrot Company

Income Statement

For Year Ending December 31, 2007

Sales revenue $ 260,722

Cost of goods sold 102,690

110 Chapter 4

P4-4

2002

2003

2004

Revenue

$28,365

$32,187

$36,835

Cost of revenue

5,699

6,059

6,716

E. Microsoft’s performance improved over the three-year period from

2002 to 2004. Cost of revenue as a percentage of revenue declined

P4-5 A. 1. Income statement

2. Income statement

9. Income statement

10. Comprehensive income

Operating expenses

27,801

Net income

5,355

7,531

8,168

Revenue