Chapter 04 – Cash and Internal Controls

4-1

Chapter 4

Cash and Internal Controls

INSTRUCTOR’S MANUAL

Authors’ Perspectives

Chapter 4 introduces students to the basics of internal controls. To help students relate to the

PART A: Internal Controls

LO4-2 Identify the components, responsibilities, and limitations of internal control.

Internal controls – Part A begins with a discussion of occupational fraud and accounting

scandals. In some instances, managers have acted unethically in reporting their companies’

PART B: Cash

LO4-3 Define cash and cash equivalents.

LO4-4 Understand controls over cash receipts and cash disbursements.

Cash controls – The discussion of general internal controls in Part A moves to a discussion of

specific cash controls in Part B. One reason for the focus on cash is that cash is the most liquid of

a company’s assets and therefore may be the asset most in need of internal control. In addition,

since most students are familiar with cash, the different forms of cash payments (checks, debit

Chapter 04 – Cash and Internal Controls

4-2

cards, and credit cards), and bank statements, relating internal controls to cash topics makes the

concept of internal controls easier to grasp.

Common Mistake: The term debit card can cause some confusion for someone in the first

accounting course. Throughout this course, we refer to an increase in cash as a debit to cash.

Bank reconciliation – We can present the bank reconciliation as a specific example of an

internal control, rather than a formal financial statement to be issued to the public.

• Illustration 4-10 focuses on cash collections in the company records versus the bank

statement. By pointing out the red circled amounts, we make it easy to see why the two

balances can differ and why a reconciliation is needed.

PART C: Statement of Cash Flows

LO4-7 Identify the major inflows and outflows of cash.

Reporting of cash – Given the focus on internal controls related to cash in Part B, Part C then

provides a discussion of how cash is reported to those outside the company. Part C briefly

mentions that cash is reported as an asset in the balance sheet, but the discussion primarily

and financing cash flows.

Chapter 04 – Cash and Internal Controls

4-3

ANALYSIS

LO4-8 Demonstrate the link between cash reported in the balance sheet and cash

reported in the statement of cash flows.

Cash Analysis – The final section of the chapter involves cash analysis by first showing how the

statement of cash flows reconciles the balance of cash shown in consecutive balance sheets. It’s

Self-Study Materials

■ Let’s Review—Bank reconciliation (p. 195).

■ Let’s Review—Types of cash flow (p. 200).

Chapter 04 – Cash and Internal Controls

4-4

Key Points by Learning Objective

Throughout the chapter, Key Points provide quick synopses of the critical pieces of information

LO4-1 Discuss the impact of accounting scandals and the passage of the Sarbanes-Oxley

Act.

The accounting scandals in the early 2000s prompted passage of the Sarbanes-Oxley Act (SOX).

LO4-2 Identify the components, responsibilities, and limitations of internal control.

Internal control refers to a company’s plan to improve the accuracy and reliability of accounting

LO4-3 Define cash and cash equivalents.

Cash includes coins and currency, checks received, and balances in savings and checking

LO4-4 Understand controls over cash receipts and cash disbursements.

Because cash is the asset of a company most susceptible to employee fraud, controls over cash

LO4-5 Reconcile a bank statement.

In a bank reconciliation, we reconcile the bank’s cash balance for (1) cash transactions already

Chapter 04 – Cash and Internal Controls

4-5

LO4-6 Account for employee purchases.

To make purchases on behalf of the company, some employees are allowed to use debit cards

LO4-7 Identify the major inflows and outflows of cash.

The statement of cash flows reports all cash activities for the period. Operating activities include

Analysis

LO4-8 Demonstrate the link between cash reported in the balance sheet and cash reported

in the statement of cash flows.

Chapter 04 – Cash and Internal Controls

4-6

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

ts

s

Questions

Learning

Objective(s)

Topic

Time

(Min.)

1

LO4-1

Define occupational fraud

5

2

LO4-1

Explain internal control

5

3

LO4-1

Discuss what managerial stewardship means

5

4

LO4-1

5

5

LO4-1

Explain the fraud triangle

5

LO4-1

Outline the major provisions of the Sarbanes-Oxley

Act

5

7

LO4-2

Describe the components of internal control

5

LO4-2

Describe the difference between preventive controls

5

and detective controls

9

LO4-2

Explain separation of duties

5

10

LO4-2

Identify responsibility for internal control

5

11

LO4-2

Recognize limitations of internal control

5

12

LO4-2

Define collusion

5

13

LO4-2

Describe likelihood of fraud by top-level employees

5

14

LO4-3

Define cash and cash equivalents

5

15

LO4-3

Describe how to record a purchase with a check

5

16

LO4-4

Discuss controls for cash receipts

5

17

LO4-4

Describe how credit card sales are reported

5

19

LO4-4

Discuss controls for cash disbursements

5

20

LO4-4

Understand a credit card

5

21

LO4-5

Identify the purpose of a bank reconciliation

5

LO4-5

5

23

LO4-5

Describe timing differences in the cash balance

5

24

LO4-5

Make adjustments related to the bank reconciliation

5

25

LO4-6

Explain purchase cards and a petty cash fund

5

26

LO4-6

Describe managerial control over employee

purchases with credit cards and the petty cash fund

5

27

LO4-7

Explain the relationship between the balance sheet

and statement of cash flows

5

28

LO4-7

Describe operating, investing, and financing cash

flows

5

29

LO4-8

Understand why analysis of the cash balance is

important

5

30

LO4-8

Compute the ratio of cash to noncash assets

5

Chapter 04 – Cash and Internal Controls

4-7

Brief

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

BE4-1

LO4-1

Identify terms associated with the Sarbanes-Oxley

Act

5

BE4-2

LO4-2

Identify terms associated with components of

internal control

5

BE4-3

LO4-2

Define control activities associated with internal

control

5

LO4-3

Identify cash and cash equivalents

5

LO4-4

Determine cash sales

5

LO4-4

Record cash expenditures

5

LO4-5

Identify terms associated with a bank reconciliation

5

LO4-5

Prepare a bank reconciliation

LO4-5

Reconcile timing differences in the bank’s balance

5

LO4-5

Reconcile timing differences in the company’s

balance

5

BE4-11

LO4-5

Record adjustments to the company’s cash balance

5

BE4-12

LO4-5

Prepare a bank reconciliation

5

BE4-13

LO4-6

Record employee purchases

5

BE4-14

LO4-7

Match types of cash flows with their definitions

5

BE4-15

LO4-7

5

BE4-16

LO4-7

Determine investing cash flows

5

BE4-17

LO4-7

Determine financing cash flows

5

BE4-18

LO4-8

Calculate the ratio of cash to noncash assets

5

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

E4-1

LO4-1

Answer true-or-false questions about occupational

fraud

15

E4-2

LO4-1

Answer true-or-false questions about the Sarbanes-

Oxley Act

15

E4-3

LO4-2

Answer true-or-false questions about internal

controls

15

LO4-2

Determine control activity violations

LO4-3

Calculate the amount of cash to report

E4-6

LO4-4

Discuss internal control procedures related to cash

receipts

10

E4-7

LO4-4

Discuss internal control procedures related to cash

disbursements

10

E4-8

LO4-4

Discuss internal control procedures related to cash

receipts

10

reconciliation

Chapter 04 – Cash and Internal Controls

4-8

E4-10

LO4-5

Calculate the balance of cash using a bank

reconciliation

10

E4-11

LO4-5

Calculate the balance of cash using a bank

reconciliation

10

LO4-6

Record transactions for employee purchases

10

LO4-6

Record transactions for employee purchases

10

LO4-7

Classify cash flows

10

LO4-7

Calculate net cash flows

10

LO4-7

Calculate operating cash flows

10

LO4-7

Calculate investing cash flows

10

LO4-7

Calculate financing cash flows

10

LO4-7

Compare operating cash flows to net income

15

Problems

Learning

Objective(s)

Topic

Time

(Min.)

P4-1A

LO4-4

Discuss control procedures for cash receipts

15

P4-2A

LO4-5

Prepare the bank reconciliation and record cash

adjustments

25

P4-3A

LO4-5

Prepare the bank reconciliation and record cash

adjustments

30

P4-4A

LO4-7

Prepare the statement of cash flows

15

P4-5A

LO4-7

Record transactions, post to the Cash T-account, and

prepare the statement of cash flows

40

Prepare a bank reconciliation and discuss cash

procedures

20

P4-2B

LO4-5

Prepare the bank reconciliation and record cash

adjustments

25

P4-3B

LO4-5

Prepare the bank reconciliation and record cash

adjustments

30

P4-4B

LO4-7

Prepare the statement of cash flows

15

P4-5B

LO4-7

Record transactions, post to the Cash T-account, and

prepare the statement of cash flows

40

Additional

Perspectives

Topic

Time

(Min.)

AP4-1

Continuing Problem: Great Adventures

45

AP4-2

Financial Analysis: American Eagle Outfitters, Inc.

40

Comparative Analysis: American Eagle Outfitters, Inc. vs. The

Buckle, Inc.

AP4-5

Ethics

20

Internet Research

30

AP4-7

Written Communication

25

Chapter 04 – Cash and Internal Controls

4-9

Alternate Let’s Review

Problem #1

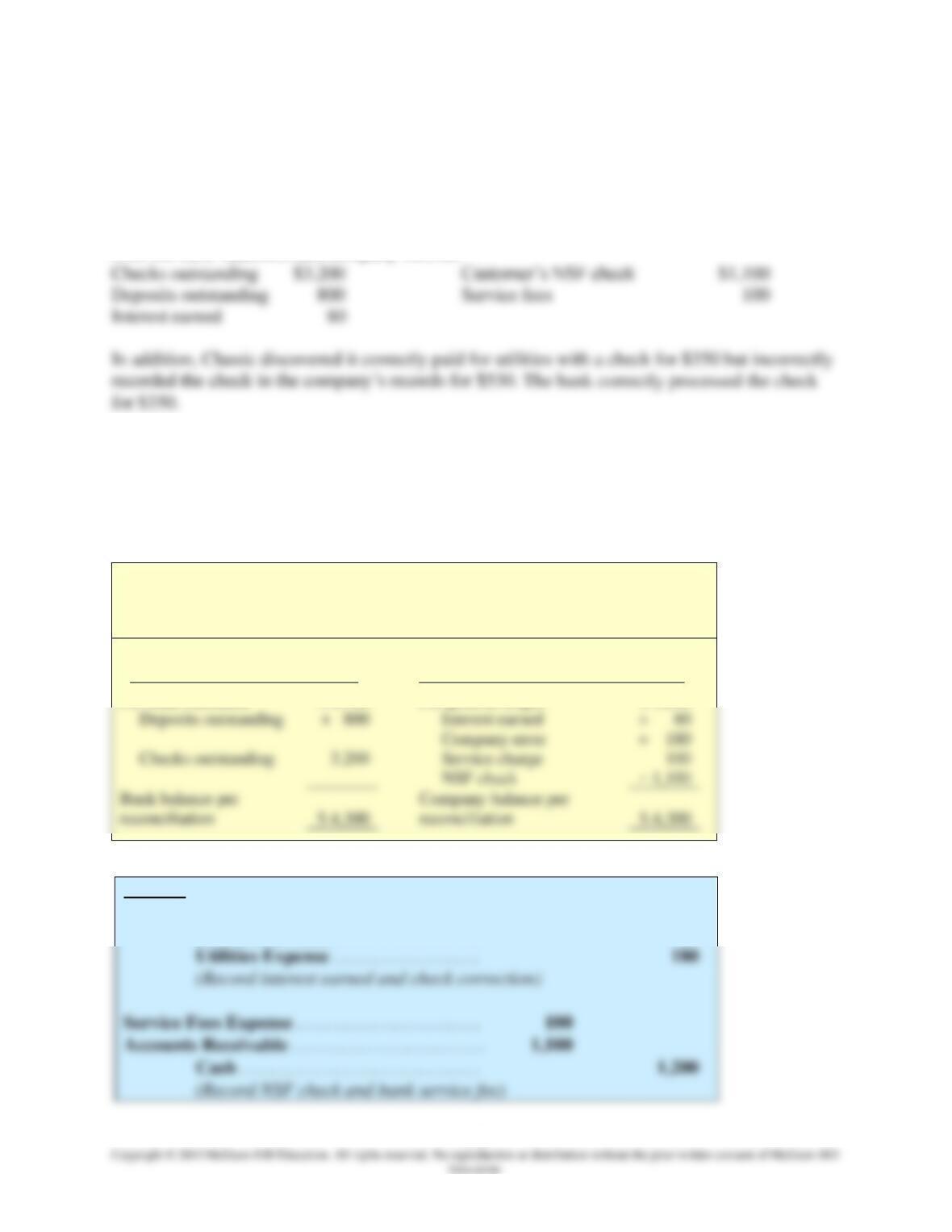

At the end of April, Classic Cinema’s accounting records show a cash balance of $5,240. The

April bank statement reports a cash balance of $6,700. The following information is gathered

from the bank statement and company records:

Required:

1. Prepare a bank reconciliation for the month of April.

2. Adjust the balance of cash in the company’s records.

Solution:

1.

Classic Cinema

Bank Reconciliation

April 30

Bank’s Cash Balance

Company’s Cash Balance

Per bank statement

$ 6,700

Per general ledger

$ 5,240

+ 180

reconciliation

$ 4,300

reconciliation

$ 4,300

2.

April 30

Debit

Credit

Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

260

Interest Revenue . . . . . . . . . . . . . . . .

80

Chapter 04 – Cash and Internal Controls

4-10

Problem #2

A company reports in its current year each of the transactions listed below.

Required:

Indicate whether each transaction should be reported as an operating, investing, or financing cash

flow in the company’s statement of cash flows, and whether each is a cash inflow or outflow.

Transaction

Type of Cash Flow

Inflow or Outflow

1. Issue common stock for cash.

2. Receive cash from customers.

3. Sell equipment for cash.

4. Pay cash for advertising.

Solution:

Chapter 04 – Cash and Internal Controls

4-11

Common Mistakes

Common Mistakes made by students are highlighted in each of the chapters. With greater

awareness of the potential pitfalls, student can avoid making the same mistakes and gain a deeper

understanding of the chapter material.

Common Mistake

debit card will result in a decrease in your cash account. The term debit card refers to the bank’s

The term debit card can cause some confusion for someone in the first accounting course.

this confuse you.

Common Mistake

reason for the difference in terminology is a difference in perspective. When a company makes a

deposit, it views this as an increase to cash, so it records a debit to the Cash account. However,

liability, which is recorded as a credit. Similarly, a withdrawal of cash from the bank is viewed

views this withdrawal as a decrease to the amount owed to the company, so it debits its liability.

Notice that bank statements refer to an increase (or deposit) in the cash balance as a credit and a

decrease (or withdrawal) as a debit. This terminology is the opposite of that used in financial

Common Mistake

its balance of cash downward to reverse the increase in cash it recorded at the time of deposit.

the customer honors the funds it owes.

Students sometimes mistake an NSF check as a bad check written by the company instead of one

written to the company. When an NSF check occurs, the company has deposited a customer’s

Common Mistake

balance because they are already properly recorded in the company’s accounting records.

Some students try to update the Cash account for deposits outstanding, checks outstanding, or a

Chapter 04 – Cash and Internal Controls

4-12

Decision Points and Decision Maker’s Perspective

Decision Points and Decision Maker’s Perspectives are provide throughout each chapter to give

insight into how measurement and communication of financial accounting information help

decision makers.

Decision Points

Question

Accounting Information

Analysis

Does the company

maintain adequate

internal controls?

Management’s discussion,

auditor’s opinion

If management or the auditor notes

any deficiencies in internal controls,

financial accounting information may

be unreliable.

Question

Accounting Information

Analysis

fraud), the company benefits.

Question

Accounting Information

Analysis & Decision

term.

Is the company able to

Statement of cash flows

Cash flows generated from internal

Decision Maker’s Perspective

How Much Cash Is Enough?

Investors and creditors closely monitor the amount of cash a company holds. The company needs

enough cash, or enough other assets that can quickly be converted to cash, to pay obligations as

Chapter 04 – Cash and Internal Controls

4-13

Ethical Dilemma

Suppose that you were sent to prison for a crime you did not commit. While in prison, the

warden learns that you have taken financial accounting and are really good at “keeping the

books.” In fact, you are so good at accounting that you offer to teach other inmates basic

financial skills that they’ll use someday after being released.

However, the warden plans to use his position of authority at the prison to steal money.

He uses prisoners as low-cost labor to do projects around town. Because other legitimate

companies cannot compete with these low costs, they bribe the warden not to bid on jobs. The

Key Issues

• Benefitting personally vs. seeing others abused

Option 1: Continue to falsify the accounting records

• You need to take care of yourself in prison. Prison life has a different set of rules.

Option 2: Discontinue falsifying the accounting records

• By falsifying documents, you are just as guilty as the person (warden) stealing the

money.