74 Chapter 4 Completing the Accounting Cycle

Relevant Example Exercises and Exhibits

• Example Exercise 4-5 Accounting Cycle

• Exhibit 8 – Accounting Cycle

SUGGESTED APPROACH

Rather than simply memorizing the ten steps in their proper order, it is helpful if students understand the

relationships between the steps in the accounting cycle. Students will not make the mistake of listing

“Financial statements prepared” before completing the end-of-period spreadsheet (work sheet) or adjusted

trial balance if they understand that the spreadsheet or adjusted trial balance provides the data necessary

to prepare financial statements. Therefore, you may want to use the activities described below after

covering the end-of-period spreadsheet or adjusted trial balance and closing entries (learning objectives 1

through 3 and/or appendix).

Emphasize that the accounting cycle is the same for all businesses, no matter how complex or how

simple. The accounting cycle is repeated each period in which financial statements are prepared.

GROUP LEARNING ACTIVITY—Accounting Cycle

Show your class TM 4-1, which lists the steps in the accounting cycle in random order. Ask students to

put the steps in the proper order. You can ask them to work individually or in small groups. TM 4-15 lists

the steps in the accounting cycle in the correct order.

WRITING EXERCISE—Accounting Cycle

Write the ten steps of the accounting cycle on the board or display TM 4-15. Ask your students to record

what information is needed as an input to each step in the accounting cycle. For example, source

documents are needed in order to analyze transactions and record them in journals (step 1). Completed

journal entries are needed to post transactions to the ledger (step 2).

After giving the students a few minutes to write, review the inputs needed for each step. Show students

that knowing what information is needed to complete each step in the accounting cycle will make it easy

to put the steps in the proper order.

Possible answers:

1. and 2. Provided above.

3. The unadjusted trial balance requires that steps 1 and 2 are completed and the account names and

balances are obtained from the general ledger.

4. Although adjustment data for the student is provided, the accountant would need to examine the

various accounts to determine which ones require adjustments and the amount to be adjusted. Once the

adjustment accounts have been identified, these tend to repeat in subsequent financial periods.

5. The optional spreadsheet requires data from the unadjusted trial balance and the adjustment data in

order to start and complete the spreadsheet.

6. Step 6 requires the input from step 4 to complete. If the end-of-period spreadsheet is completed, the

adjusting data can be taken from the spreadsheet in order to journalize the adjustments. The posting of

the adjustments is a required step.

7. The adjusted trial balance requires that step 6 be completed. The data is then obtained from the general

ledger once the adjusting data has been posted to update the account balances. If the optional end-of-

period spreadsheet is completed, this step maybe skipped since the spreadsheet contains an adjusted

trial balance as part of the completion process.

8. Financial statements are prepared using the data from the adjusted trial balance or the optional

spreadsheet.

9. Closing data are obtained from the general ledger, trial balance, or spreadsheet. Temporary accounts

are closed in the process described earlier.

10. Post-closing trial balance is completed once the closing process is finalized. The accounts and their

balances can be found in the general ledger once all closing entries are posted. All temporary accounts

should have zero balances. Only permanent (balance sheet) accounts will have a positive balance;

therefore, the post-closing trial balance will include only asset, liability and the owner’s capital

accounts.

Each step in the process depends on the previous step in order to obtain the necessary information to

complete the subsequent step. The optional spreadsheet can consolidate and simplify the process;

however, it does not eliminate the requirements of recording and updating the general ledger using the

journalizing and posting process.

OBJECTIVE 5

Illustrate the accounting cycle for one period.

SYNOPSIS

This objective shows the complete accounting cycle for a new business known as Kelly Consulting. A

total of thirty transactions are listed. Each transaction is analyzed and recorded in the journal. Exhibit 10

shows each journal entry. Each journal entry is posted, and then the unadjusted trial balance is prepared.

Adjustment data are analyzed, journalized, and posted. An adjusted trial balance is prepared. Financial

statements are prepared in order. Next, the closing entries are journalized and posted. The post-closing

trial balance is the last step in the accounting cycle.

Relevant Example Exercises and Exhibits

• Exhibit 9 – Chart of Accounts for Kelly Consulting

• Exhibit 10 – Journal Entries for April, Kelly Consulting

• Exhibit 11 – Unadjusted Trial Balance, Kelly Consulting

• Exhibit 12 – End-of-Period Spreadsheet, Kelly Consulting

• Exhibit 13 – Adjusting Entries, Kelly Consulting

• Exhibit 14 – Adjusted Trial Balance, Kelly Consulting

• Exhibit 15 – Financial Statements, Kelly Consulting

• Exhibit 16 – Closing Entries, Kelly Consulting

76 Chapter 4 Completing the Accounting Cycle

• Exhibit 17 – Post-Closing Trial Balance, Kelly Consulting

• Exhibit 18 – Ledger, Kelly Consulting

SUGGESTED APPROACH

After defining and working with the accounting cycle in Objective 3, you may wish to select PR 4-5A or

PR 4-5B and work it through using the Excel templates provided in the instructor resources. This will

allow the student to see the entire accounting cycle demonstrated at one time. A word of caution: This

problem is rather lengthy and could take an entire class period to complete. Nevertheless, it is a valuable

review to demonstrate to the students all the foundation materials that have been covered in Chapters 1-4.

OBJECTIVE 6

Explain what is meant by the fiscal year and the natural business year.

SYNOPSIS

The fiscal year for a business usually begins on January 1 and ends on December 31. However, a business

can choose to start its fiscal in another month and its fiscal year-end will then be the 31st of the following

twelfth month. If a business’s fiscal year follows its natural business cycle, it is called the natural business

year. The financial history of a business may be shown by series of income statements and balance sheets.

Keys Terms and Definitions

• Fiscal Year – The annual accounting period adopted by a business.

• Natural Business Year – A fiscal year that ends when business activities have reached the lowest

point in an annual operating cycle.

Relevant Example Exercises and Exhibits

• Exhibit 19 – Financial History of a Business

SUGGESTED APPROACH

Objective 6 asks students to understand the definitions of fiscal year and natural business year, not just to

memorize these definitions. Therefore, the instructor must get the student to internalize these concepts.

LECTURE AID—Fiscal Year

To begin this exercise, explain the definitions of fiscal year and natural business year. Then ask students

who work either full- or part-time to raise their hands. Call on one of these students and ask where he or

she works.

Chapter 4 Completing the Accounting Cycle 77

Next, ask the student at what time of the year the company is at the end of its natural business year (e.g.,

when stocks are lowest; prices are normal; the company is not buying heavily). Ask the student whether

he or she knows when the company closes its fiscal year. If the student doesn’t know, ask when the

company takes a physical inventory count. That may provide a clue.

Repeat the same exercise with several other students.

Use the following examples to help students understand why the fiscal business year may vary from the

calendar year. First, ask students if they would like to be taking inventory and working through the

accounting cycle financial statements closing process the week of Christmas. For retail stores, this is

typically a high volume sales time with after-Christmas sales, returns, and exchanges. Explain that a retail

store will typically choose the slowest time of the year, when inventory levels are low and sales are slow,

to complete this process.

A second example for demonstration purposes is a ski resort. Ski resorts’ busy season is in the winter,

when there is snow. A secondary busy season might be summer for hiking and fishing. Ski resorts’ slow

time is typically in the spring, when snow is melting and the slopes are a muddy mess. This is the time a

ski resort would choose to complete the accounting cycle.

OBJECTIVE 7

Describe and illustrate the use of working capital and the current ratio in evaluating a

company’s financial condition.

SYNOPSIS

Financial statements can also be used to analyze a business in another way. Using numbers obtained from

the financial statements, a business’s liquidity and solvency can be determined. Working capital is

defined as follows: Working Capital = Current Assets – Current Liabilities. Current assets are usually

those that can be converted to cash within one year of operation. A positive working capital is necessary

for a company to pay its current liabilities. The current ratio uses the same two numbers from the balance

sheet. The current ratio is computed as follows: Current Ratio = Current Assets/Current Liabilities. The

current ratio is useful to make comparisons with other companies or industries.

Keys Terms and Definitions

• Current Ratio – A financial ratio that is computed by dividing current assets by current

liabilities.

• Liquidity – The ability to convert assets into cash.

• Solvency – The ability of a firm to pay its debts as they come due.

• Working Capital – The excess of the current assets of a business over its current liabilities.

78 Chapter 4 Completing the Accounting Cycle

Relevant Example Exercises and Exhibits

• Example Exercise 4-6 Working Capital and Current Ratio

SUGGESTED APPROACH

To help students understand these terms, make it personal.

For example, for liquidity, ask them to imagine being offered the “deal of a lifetime” but the opportunity

is available only for the next hour. What is the first item they possess that comes to mind that would be

easiest to use to pay for “the deal”? For those who have cash in the bank, a quick trip to the ATM would

seal the deal or selling something very popular among their peers could work. Which items would take

more time to sell and thus convert to cash? Probably more expensive items.

Tie solvency to working capital by asking students that if they had to pay their current obligations in a

timely manner, could they do it? They should think about their current sources of cash (job, allowance

from parents, etc.) and their current bills (rent, utilities, school supplies, etc.).

Ask students to consider why current ratio is more indicative of how a company’s ability to meet its

current obligations compares to its industry average than only knowing the value of its current assets and

liabilities.

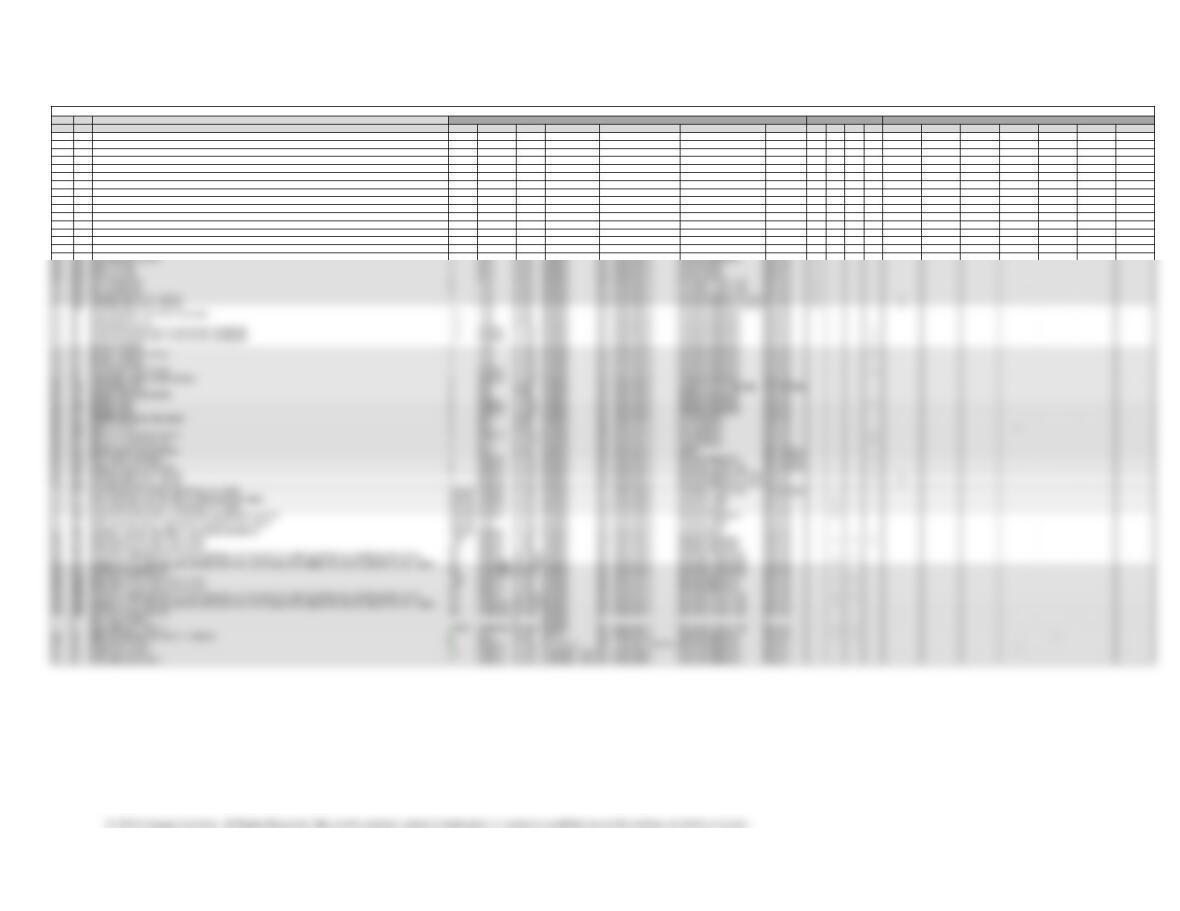

APPENDIX—End-of-Period Spreadsheet

(Work Sheet)

If you elect to include the end-of-period spreadsheet (work sheet) in the curriculum, you may want to

include this discussion early in the chapter material.

GROUP LEARNING ACTIVITY—Preparing an End-of-Period Spreadsheet

(Work Sheet)

TM 4-2 presents information that can be used in explaining the purpose of the end-of-period spreadsheet

(work sheet). After reviewing this material, use TM 4-3 to explain how to complete the columns of the

It is helpful to allow your students to practice completing an end-of-period spreadsheet. The following

group learning activity will assist in accomplishing this goal.

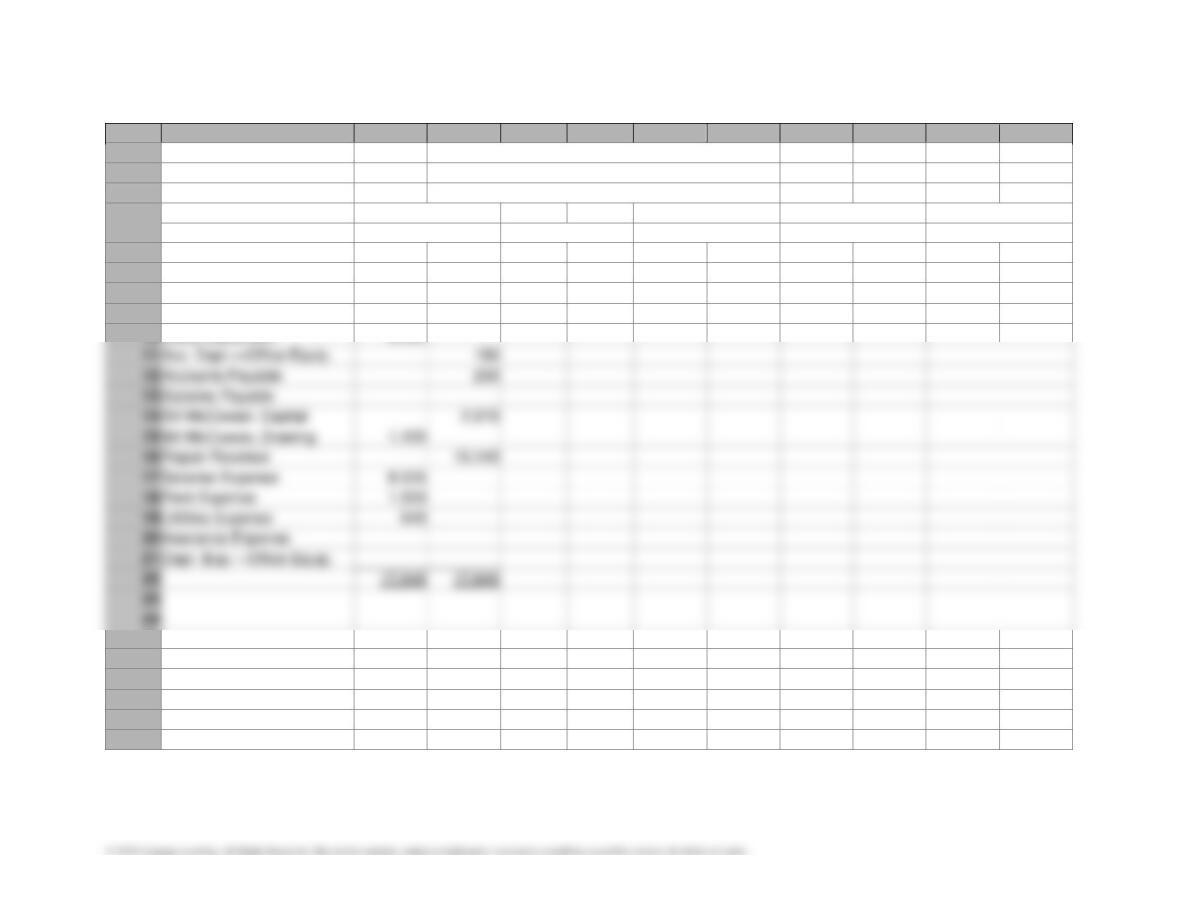

Handout 4-1 is an end-of-period spreadsheet (work sheet) for Dixie Machinery. The Trial Balance

columns have been completed using account balances from the company’s ledger. Make copies of this

Chapter 4 Completing the Accounting Cycle 79

handout for each of your students. Divide the class into small groups and instruct them to enter the

adjusting entries from TM 4-4 on the spreadsheet. Also ask them to complete the Adjusted Trial Balance

columns.

Check your students’ understanding of using the end-of-period spreadsheet to compute net income by

asking the following questions:

1. If the totals of the Income Statement columns of a spreadsheet are Debit, $2,800 and Credit, $2,500,

2. If the totals of the Balance Sheet columns of a spreadsheet are Debit, $1,250 and Credit, $1,110, what

Handout 4-1

A

B

C

D

E

F

G

H

I

J

K

1

Dixie Machinery

2

End-of-Period Spreadsheet (Work Sheet)

3

For the Year Ended December 31, 20—

4

Unadjusted

Adjusted

Income

Balance

5

Trial Balance

Adjustments

Trial Balance

Statement

Sheet

6

Account Title

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

7

Cash

825

8

Accounts Receivable

300

9

Prepaid Insurance

500

10

Office Equipment

5,050

11

Acc. Depr.—Office Equip.

180

12

Accounts Payable

250

13

Salaries Payable

14

Bill McCowan, Capital

2,370

15

Bill McCowan, Drawing

16

Repair Revenue

17

Salaries Expense

18

Rent Expense

19

Utilities Expense

640

20

Insurance Expense

21

Depr. Exp.—Office Equip.

22

23

24

25

26

27

28

29

30

Handout 4-2

CLOSING ENTRIES

Part A—Make entries that will bring the revenue, expense, and drawing accounts to a

zero balance. Do this by moving the balance of each account to the capital account.

After you have completed your entries, compute the balance of the capital account.

Service Revenue

3,500

1,200

10,000

Salaries Expense

1,400

Rent Expense

600

Part B—Prepare closing entries in the format used by accountants. To do this, close the

revenue, expense, and drawing accounts in the following order:

(a) Close the revenue account to Income Summary.

(b) Close the expense accounts to Income Summary.

After you have completed all the entries, compute the balance in the capital account.

Service Revenue

3,500

1,200

10,000

Salaries Expense

1,400

Rent Expense

600

Type Item Description LO(s) Difficulty Time Est BUSPROG AICPA ACBSP – APC Bloom’s EE Excel GL SMH FAI Service Real World Writing Ethics Internet Group

DQ 1 1 Easy 5 min. Analytic FN – Measurement Recording Transactions Remembering

DQ 2 2 Easy 5 min. Analytic FN – Measurement Current Assets Remembering

DQ 3 2 Easy 5 min. Analytic FN – Measurement Current Liabilities Remembering

DQ 4 3 Easy 5 min. Analytic FN – Measurement Recording Transactions Remembering

DQ 5 3 Easy 5 min. Analytic FN – Measurement Closing Entries Remembering

DQ 6 3 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering

DQ 7 4 Easy 5 min. Analytic FN – Measurement Recording Transactions Remembering

DQ 8 4 Easy 5 min. Analytic FN – Measurement Recording Transactions Remembering

DQ 9 6 Easy 5 min. Analytic FN – Measurement GAAP Remembering

DQ 10 6 Easy 5 min. Analytic FN – Measurement GAAP Remembering

PE 1A Flow of accounts into financial statements 1 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering x

PE 1B Flow of accounts into financial statements 1 Easy 5 min. Analytic FN – Measurement Adjusting Entries Remembering x

PE 2A Statement of owner’s equity 2 Easy 5 min. Analytic FN – Measurement Financial Statements Applying x

PE 2B Statement of owner’s equity 2 Easy 5 min. Analytic FN – Measurement Financial Statements Applying x

PE 3A Classified balance sheet 2 Easy 5 min. Analytic FN – Measurement Financial Statements Applying x

HOMEWORK CHART WITH LEARNING OUTCOMES TAGGING

TAGGING

RESOURCES

FOCUS