Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 4

Learning Objectives

After studying this chapter, students should be able to:

1. Explain coverage under the Federal Income Tax Withholding Law by determining:

(a) the employer-employee relationship, (b) the kinds of payments defined as

wages, and (c) the kinds of pretax salary reductions.

2. Explain: (a) the types of withholding allowances that may be claimed by employees

for income tax withholding and (b) the purpose and use of Form W-4.

3. Compute the amount of federal income tax to be withheld using: (a) the percentage

method; (b) the wage-bracket method; (c) alternative methods such as quarterly

averaging, annualizing of wages, and part-year employment; and (d) withholding of

federal income taxes on supplementary wage payments.

4. Explain: (a) Form W-2, (b) the completion of Form 941, Employer’s Quarterly

Federal Tax Return, (c) major types of information returns, and (d) the impact of

state and local income taxes on the payroll accounting process.

Contents

Chapter 4 outline:

LEARNING OBJECTIVES

COVERAGE UNDER FEDERAL INCOME TAX WITHHOLDING LAWS

Employer-Employee Relationship

Statutory Employees/Nonemployees

Taxable Wages

Fringe Benefits

Withholding on Fringe Benefits

Flexible Reporting

4–2 Payroll Accounting

Pretax Salary Reductions

Cafeteria Plans

Flexible-Spending Accounts

Health Savings Accounts

Archer Medical Savings Accounts

Deferred Arrangements

TAX-DEFERRED RETIREMENT ACCOUNTS

Individual Retirement Accounts

Roth IRA

WITHHOLDING ALLOWANCES

Personal Allowances

Allowances for Dependents

Additional Withholding Allowance

Other Withholding Allowances

Form W-4 (Employee’s Withholding Allowance Certificate)

Completing Form W-4

Withholding Allowances

Changing Form W-4

Exemption from Income Tax Withholding

FEDERAL INCOME TAX WITHHOLDING

Percentage Method

Wage-Bracket Method

OTHER METHODS OF WITHHOLDING

SUPPLEMENTAL WAGE PAYMENTS

Vacation Pay

Supplemental Wages Paid with Regular Wages

Supplemental Wages Paid Separately from Regular Wages

Method A

Method B

Gross-Up Supplemental

Chapter 4 4–3

WAGE AND TAX STATEMENTS

Form W-2

Form W-2c

Form W-3

Penalties

Form W-3c

Privately Printed Forms

RETURNS EMPLOYERS MUST COMPLETE

INFORMATION RETURNS

INDEPENDENT CONTRACTOR PAYMENTS

BACKUP WITHHOLDING

Matching Quiz (p. 4–38)

4–4 Payroll Accounting

Questions for Review (p. 4–38)

Note: All answers and solutions are based on Tax Tables A and B in the textbook and

the tax regulations presented in Chapter 4. Tax Tables A and B are used by employers,

effective January 1, 2017.

3. a. Nonexempt

9. Employees who had no income tax liability in 2017 and do not expect to have any

for 2018 qualify for exemption from withholding of federal income tax from their

10. The special period rule allows employers to use October 31 as the cutoff date for

Chapter 4 4–5

13. The formula is:

14. When the federal income tax has already been withheld from the employee’s regular

wages, the employer may select one of two alternative methods for withholding the

16. Employers who are required to prepare information returns (Form 1099 series)

18. Employees who willfully file false Forms W-4 are subject to fines of up to $1,000 or

4–6 Payroll Accounting

Questions for Discussion (p. 4–39)

1. No, Lagomarsino should not include the cash value of Oberstar’s meals as part of

his taxable wages. The general rule is that the value of meals and lodging furnished

2. Generally, a payroll period is the period of service for which a payment of wages is

3. This question gives students an opportunity to become acquainted with their state’s

income tax withholding law. If your state has no withholding law, you may assign

4. There is no law against withholding more federal income taxes from a worker’s pay

than would be required under the wage-bracket or percentage method. Reynolds

would be proceeding legally by amending her Form W-4 and would be joining many

5. a. The IRS claims that several hundred casino waitresses and waiters fail to report

about $10,000 in tips each year and owe an average of $2,400 in back taxes. Wait-

Chapter 4 4–7

reported.

6. Since the fringe benefit is subject to federal income and social security taxes, it

Problem Sets (p. 4–41)

The principles and practices of payroll accounting discussed in Chapter 4 are applied in

the Problem Sets as shown below.

Principle or Practice Problem Set No. (A and B)

1. Using the percentage method to compute 4–2, 4–3

federal income taxes to withhold.

2. Using the wage-bracket method to compute 4–1, 4–3, 4–4, 4–5,

federal income taxes to withhold. 4–8 through 4–9

3. Computing the withholdings for FICA, federal 4–5, 4–8, 4–9

income taxes, state income taxes, and city

income taxes to determine net pay.

4. Computing annual bonus to be paid with 4–6, 4–8

regular salaries.

5. Computing the quarterly totals (weekly and 4–9

monthly paydays) for gross earnings,

deductions, and net pay.

6. Gross-up supplementals. 4–10

7. Compute net pay with tax-free retirement 4–7, 4–11

withholdings.

8. Completing Form 941 and Employer’s Report 4–12

of State Income Tax Withheld.

9. Completing Forms W-2 and Form W-3 for 4–13

calendar year.

4–8 Payroll Accounting

Solutions—Problem Set A

4–1A.

Gross pay ................................................. $300.00

4–2A.

Employee

No.

Employee

Name

Marital

Status

No. of

Withholding

Allowances

Gross Wage

or Salary

Amount

to Be

Withheld

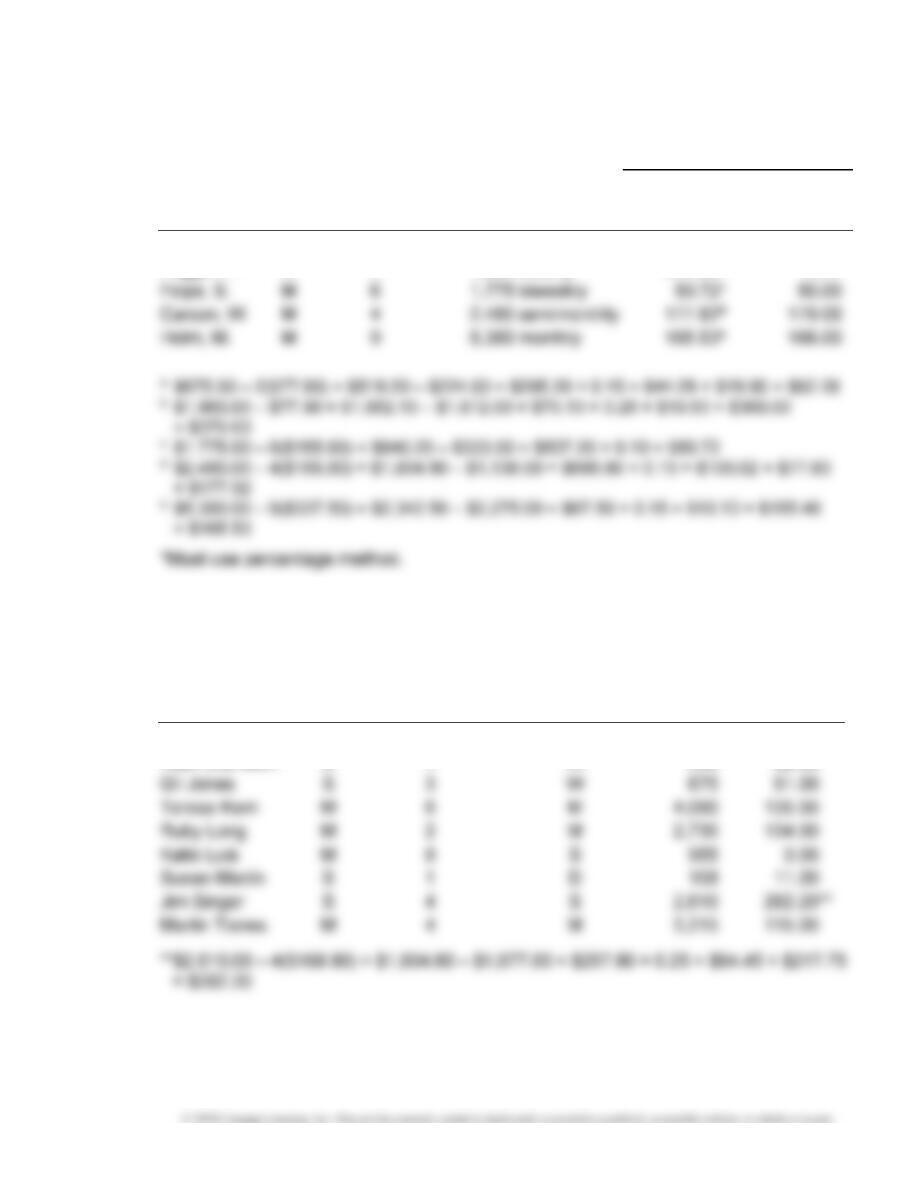

1 Amoroso, A. M 4 $1,610 weekly $151.91a

Chapter 4 4–9

4–3A.

Amount to Be

Withheld

Employee

Marital

Status

No. of

Withholding

Allowances

Gross Wage

or Salary

Percentage

Method

Wage-

Bracket

Method

Corn, A. S 2 $ 675 weekly $ 62.28a $ 62.00

Fogge, P. S 1 1,960 weekly 379.63b N/A*

4–4A.

Employee

Marital

Status

No. of

Withholding

Allowances

Payroll Period

W = Weekly

S = Semimonthly

M = Monthly

D = Daily

Wage

Amount to

Be Withheld

Hal Bower M 1 W $1,350 $149.00

Ruth Cramden S 1 W 590 62.00

4–5A.

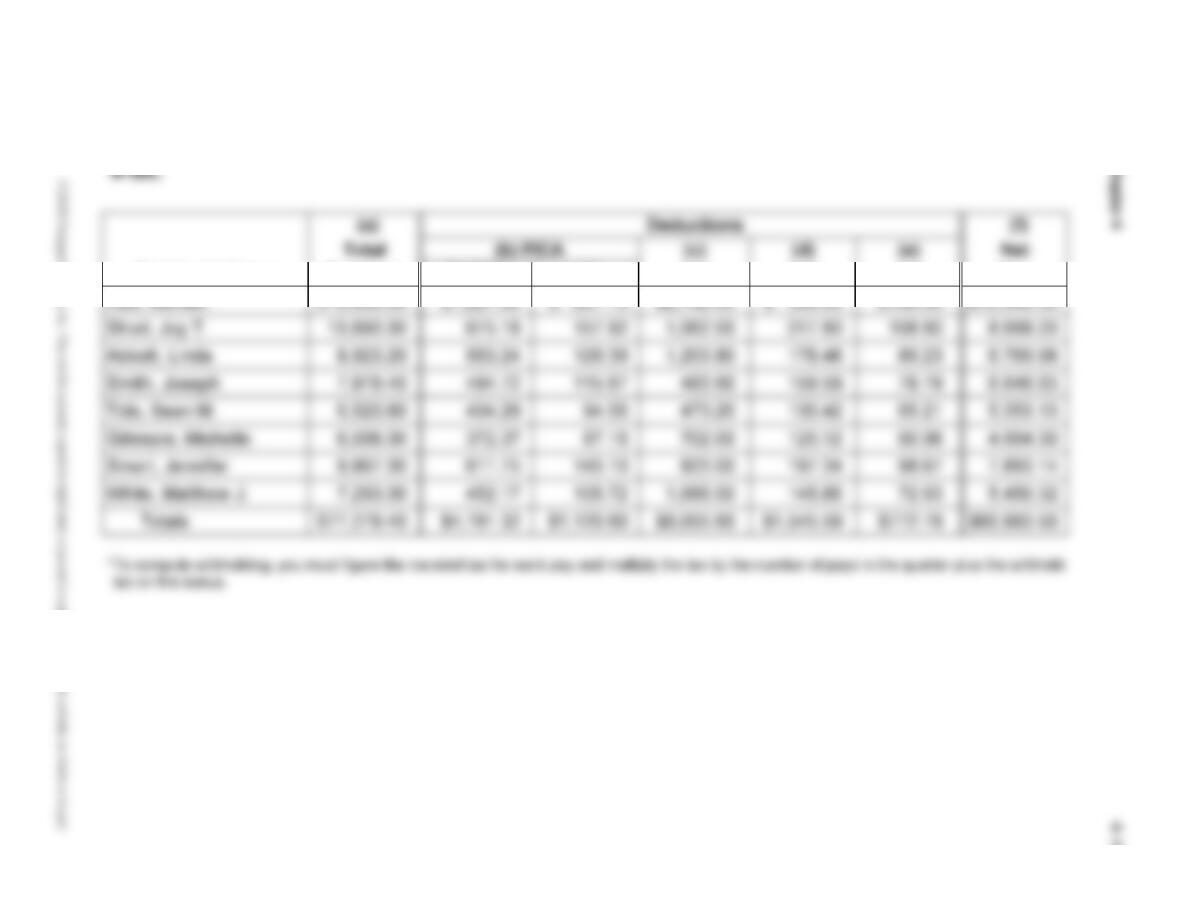

For Period Ending December 21

No. of Deductions (e)

Marital W/H Total (a) FICA (b) (c) (d) Net

Employee Name Status Allowances Earnings OASDI HI FIT SIT CIT Pay

John, Matthew M 3 $2,524.00 $ 62.00* $36.60 $367.13** $ 50.48 $37.86 $1,969.93

Compute the employer’s FICA taxes for the pay period ending December 21.

Chapter 4 4–11

4–6A.

(a) $250

4–7A.

Gross pay .......................................................................................... $ 930.00

4–8A.

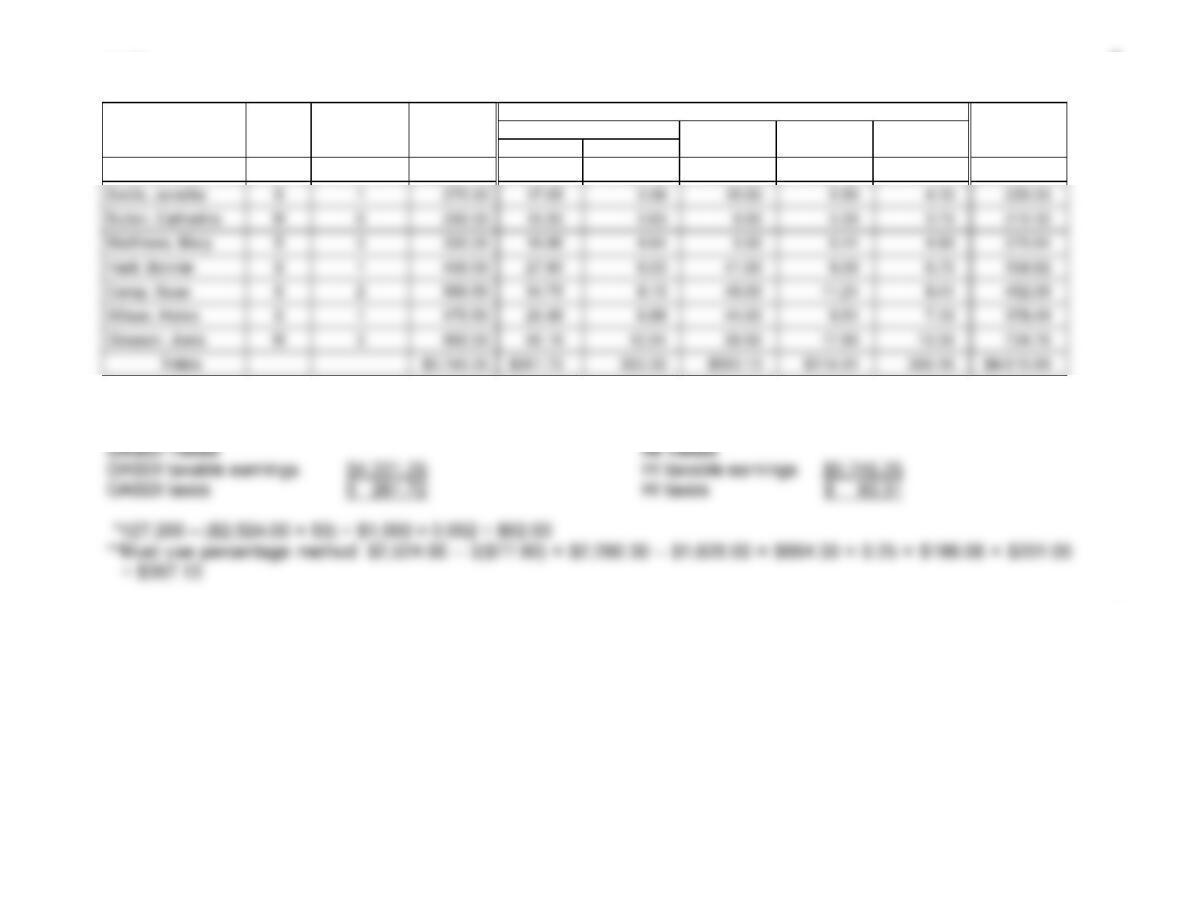

For Period Ending December 28

No. of Earnings Deductions (g)

Marital W/H (a) (b) (c) FICA (d) (e) (f) Net

Employee Name Status Allowances Regular Supp’l. Total OASDI HI FIT SIT CIT Pay

Hall, Michael M 5 $ 5,000.00* $ 4,800.00 $ 9,800.00 $ 607.60 $142.10 $1,514.00 $196.00 $ 98.00 $ 7,242.30

Compute the employer’s FICA taxes for the pay period ending December 28.

4–12 Payroll Accounting

Employee Name Earnings OASDI* HI* FIT SIT CIT Pay

Hall, Michael $19,800.00 $1,227.60 $ 287.10 $2,142.00 $ 396.00 $198.00 $15,549.30

Chapter 4 4–13

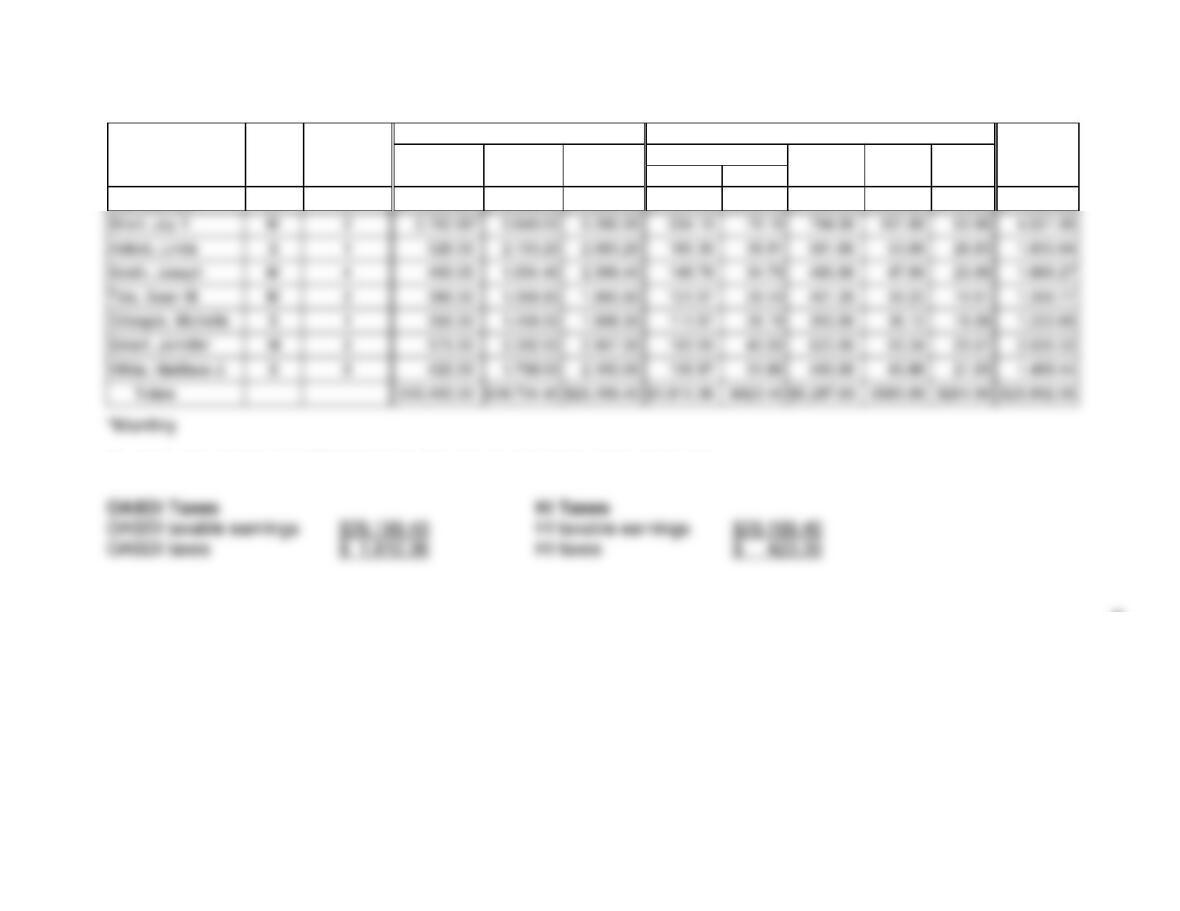

4–10A.

(a)

$100

4–11A.

(c) Clausen’s take-home pay with the

retirement contribution deducted:

Weekly pay .......................................................................... $ 820.00

(d) Clausen’s take-home pay without the

retirement contribution deducted:

Weekly pay .......................................................................... $820.00

Chapter 4 4–15

4–12A.

(a)

FEDERAL DEPOSIT INFORMATION WORKSHEET

Employer

Identification Number

00-0004701

Name

Quality Repairs

FEDERAL DEPOSIT INFORMATION WORKSHEET

Employer

Identification Number

00-0004701

Name

Quality Repairs

4–16 Payroll Accounting

4–12A. (Continued)

FEDERAL DEPOSIT INFORMATION WORKSHEET

Employer

Identification Number

00-0004701

Name

Quality Repairs

Chapter 4 4–17

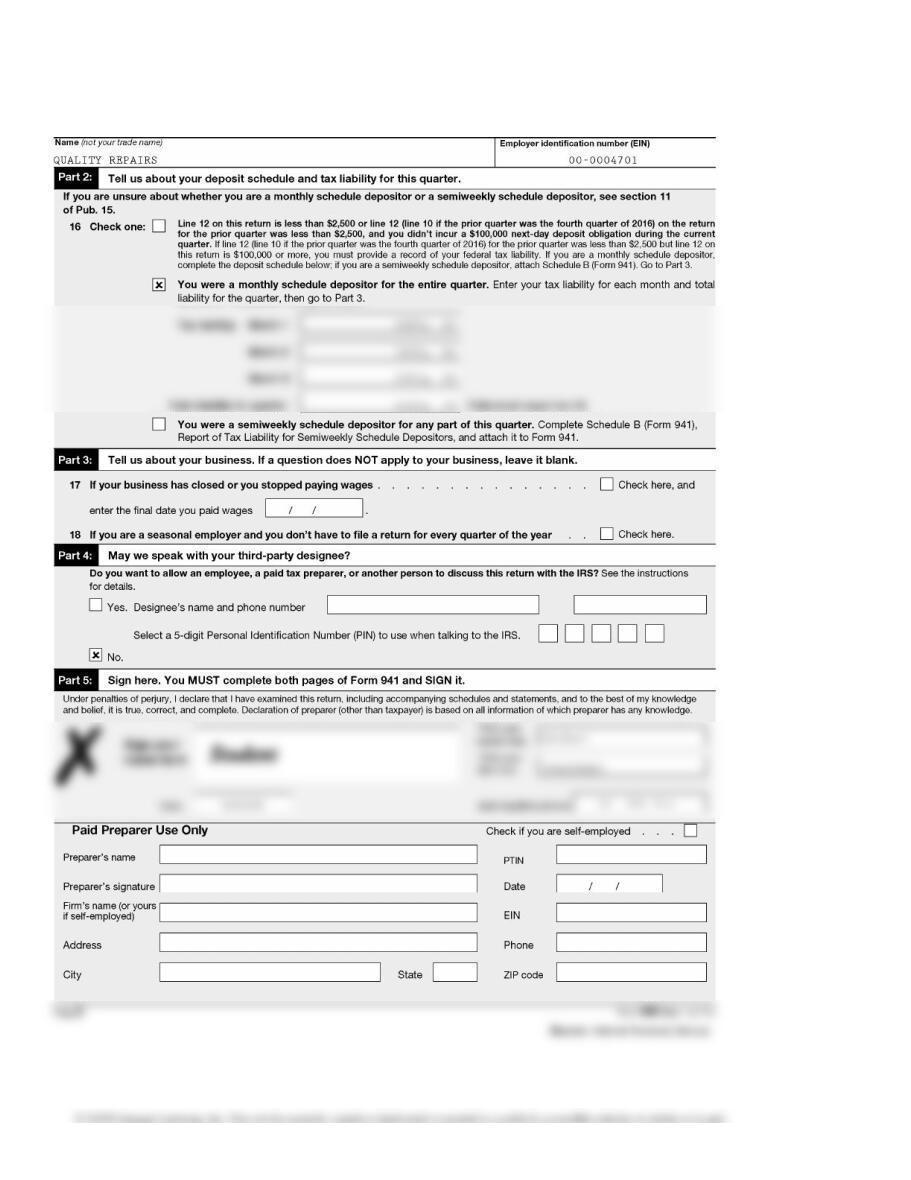

4–12A. (Continued) Form 941

4–18 Payroll Accounting

4–12A. (Continued)

Chapter 4 4–19

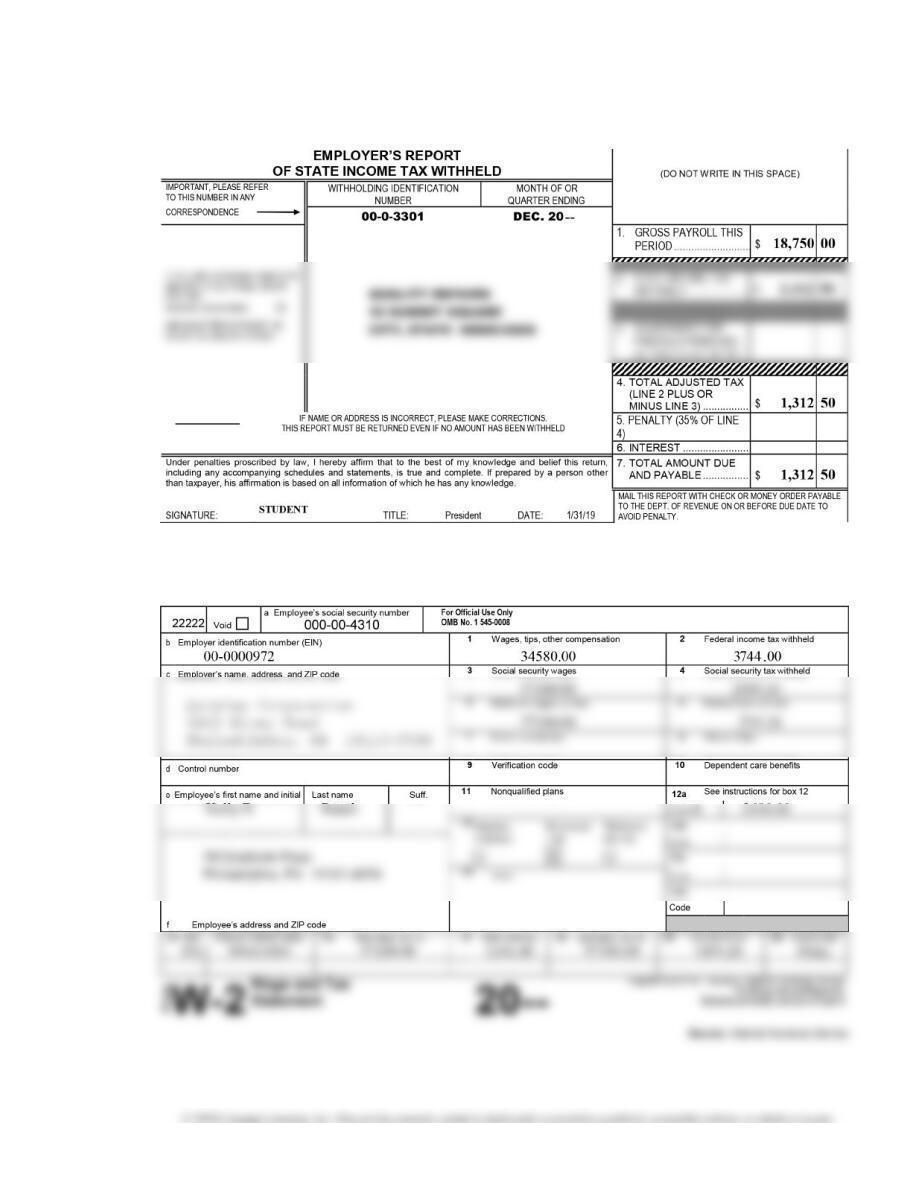

4–12A. (Concluded) Employer’s Report of State Income Tax Withheld

(c)

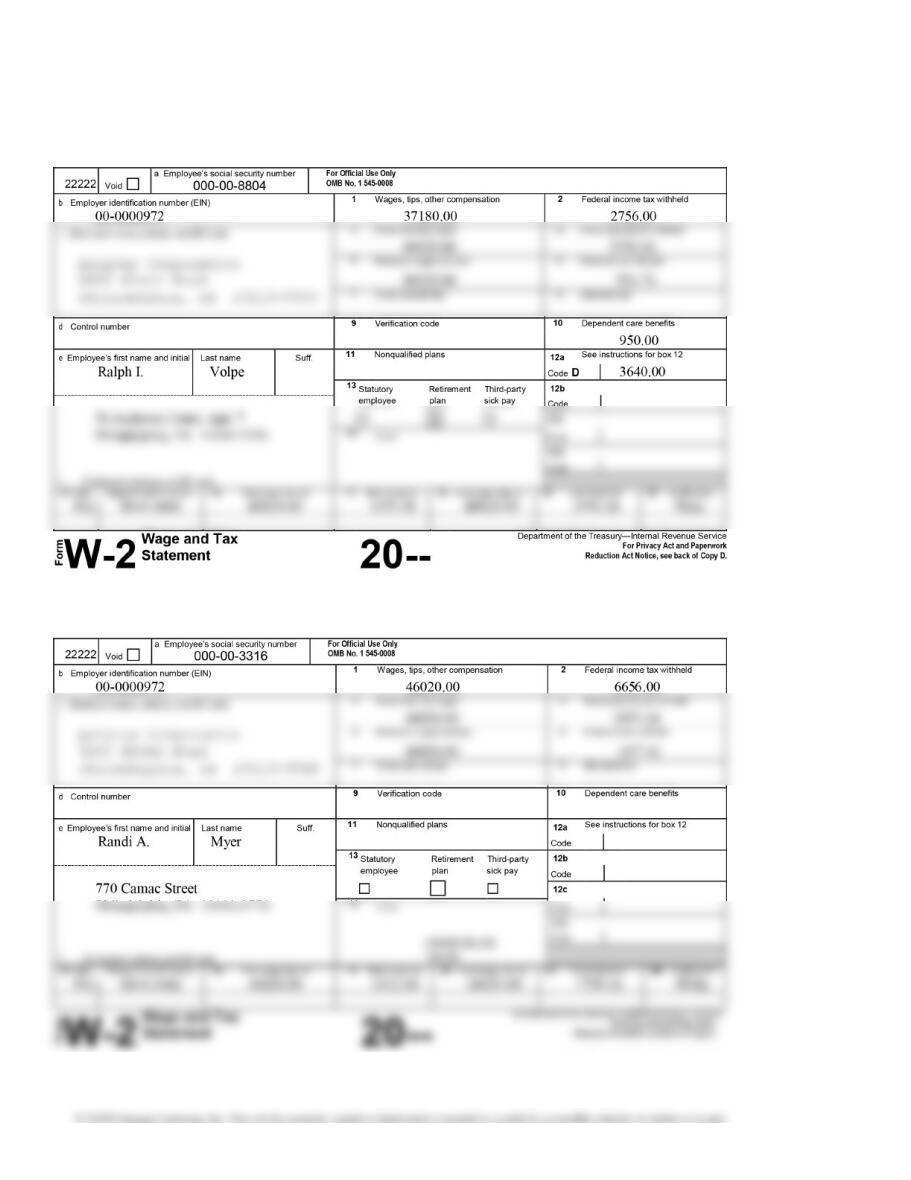

4–13A. Wage and Tax Statement

(a)

4–20 Payroll Accounting

4–13A. (Continued)

(b)

(c)

Source: Internal Revenue Service.