30 Minutes, Medium

Sept.

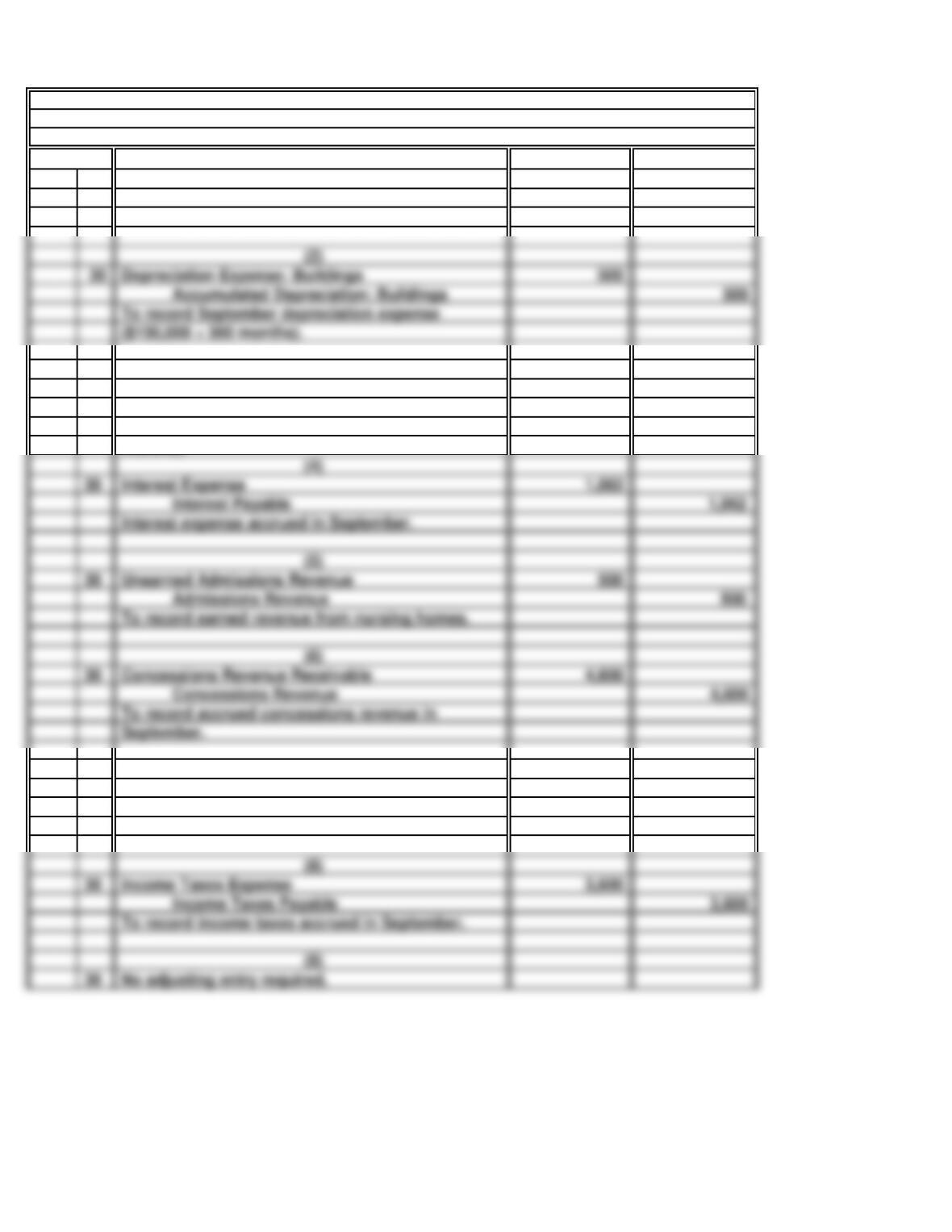

30 600

Prepaid Costume Rental 600

30 300

Accumulated Depreciation: Fixtures and Equip. 300

30 1,062

Interest Payable 1,062

30 500

Admissions Revenue 500

30 4,600

Concessions Revenue 4,600

Interest expense accrued in September.

(5)

(4)

To record earned revenue from nursing homes.

September.

Unearned Admissions Revenue

Interest Expense

(6)

To record accrued concessions revenue in

Concessions Revenue Receivable

30 2,200

Salaries Payable 2,200

30 3,600

30

No adjusting entry required.

To record income taxes accrued in September.

(9)

Income Taxes Expense

(8)

OFF-CAMPUS PLAYHOUSE

PROBLEM 4.4B

Current Yr.

Costume Rental Expense

Costume rental expense incurred in September.

months).

a.

(Adjusting Entries)

(1)

(3)

General Journal

To record accrued salary expense in September.

Salaries Expense

Depreciation Expense: Fixtures and Equipment

To record September depreciation ($18,000 ÷ 60

(7)

30 500

Accumulated Depreciation: Buildings 500

To record September depreciation expense

($150,000 ÷ 300 months).

(2)

Depreciation Expense: Buildings

b.

c.

Nine months (bills received January through September). Utility bills are recorded as

PROBLEM 4.4B

OFF-CAMPUS PLAYHOUSE (concluded)

Corporations must pay income taxes in several installments throughout the year. The

(1)

30 Minutes, Medium

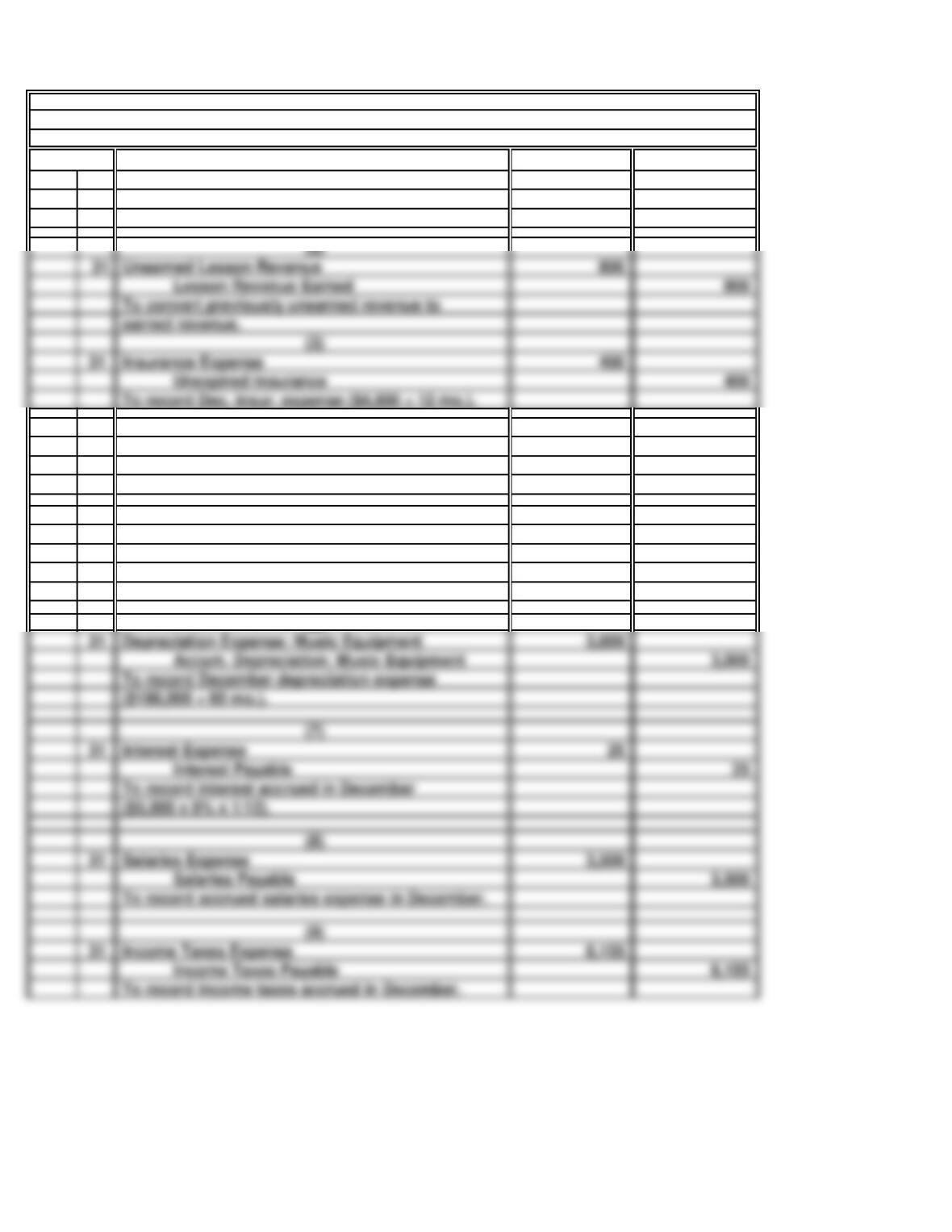

Dec. 31 3,200

Lesson Revenue Earned 3,200

31 1,500

Prepaid Rent 1,500

31 250

Sheet Music Supplies 250

31 3,000

Accum. Depreciation: Music Equipment 3,000

31 25

Interest Payable 25

31 3,500

Salaries Payable 3,500

31 8,155

Income Taxes Payable 8,155

(7)

($5,000 x 6% x 1/12).

Income Taxes Expense

To record accrued salaries expense in December.

To record interest accrued in December

Interest Expense

(8)

($180,000 ÷ 60 mo.).

To record income taxes accrued in December.

Depreciation Expense: Music Equipment

To record December depreciation expense

(9)

Salaries Expense

PROBLEM 4.5B

(4)

(6)

MARVELOUS MUSIC

To record Dec. rent expense ($9,000 ÷ 6 mo.).

Accounts Receivable

To record accrued but uncollected revenue.

Year 1

Sheet Music Supplies Expense

($450 – $200).

a.

(Adjusting Entries)

(1)

General Journal

To record offices supplies used in December

Rent Expense

(5)

Lesson Revenue Earned 800

31 400

Unexpired Insurance 400

To convert previously unearned revenue to

Insurance Expense

To record Dec. insur. expense ($4,800 ÷ 12 mo.).

(2)

(3)

Unearned Lesson Revenue

earned revenue.

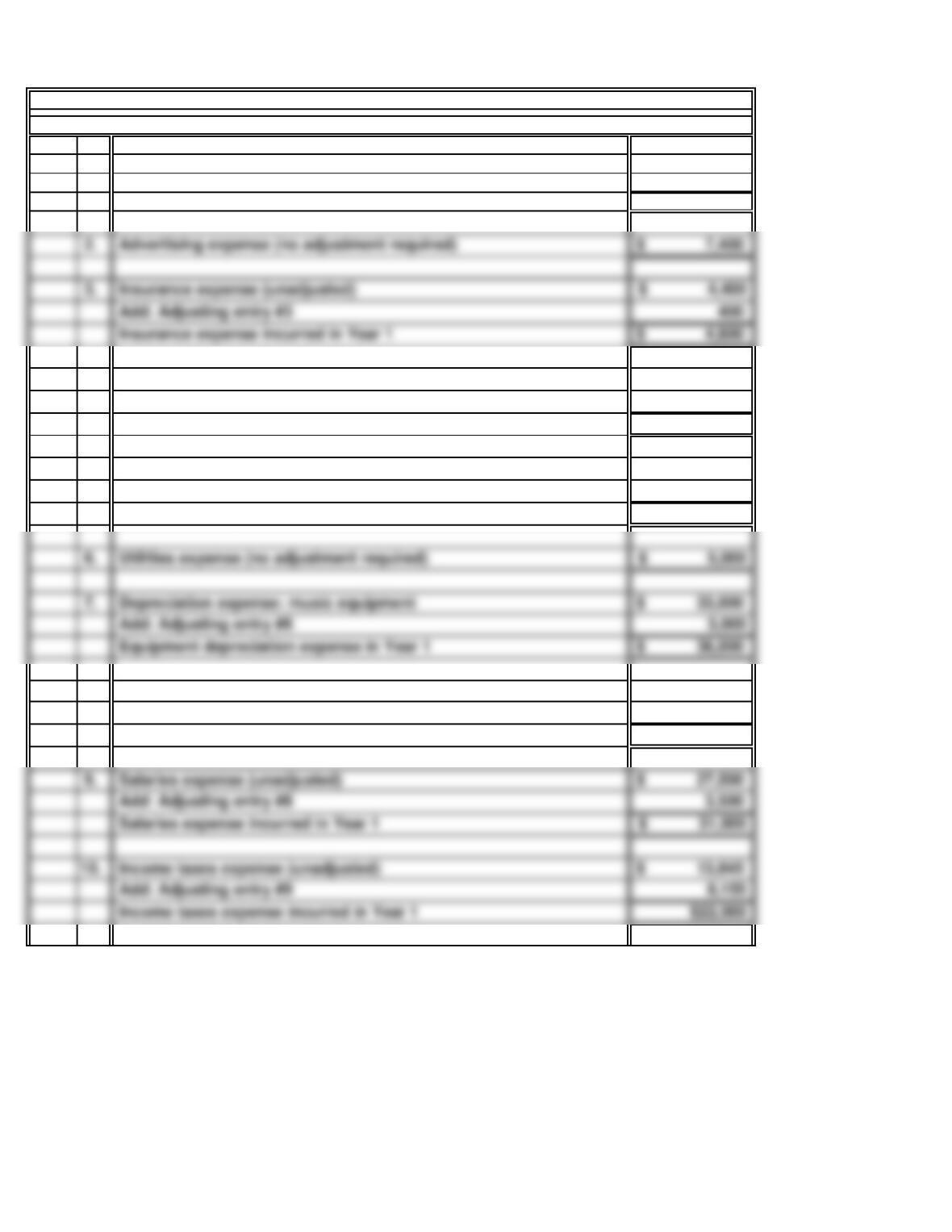

1. $ 154,375

3,200

800

$ 158,375

4. $ 16,500

1,500

18,000$

5. $ 780

250

$ 1,030

6. 5,000$

7. $ 33,000

$ 36,000

Add: Adjusting entry #6

Equipment depreciation expense in Year 1

Utilities expense (no adjustment required)

Depreciation expense: music equipment

8. 25$

25

$ 50

9. $ 27,500

3,500

Salaries expense (unadjusted)

Add: Adjusting entry #8

Salaries expense incurred in Year 1

Income taxes expense (unadjusted)

Add: Adjusting entry #9

Income taxes expense incurred in Year 1

c.

The unadjusted trial balance reports dividends payable of $1,000. Thus, none of the

$1,000 dividend has been paid.

Add: Adjusting entry #4

Rent expense incurred in Year 1

Rent expense (unadjusted)

Interest expense (unadjusted)

Interest expense incurred in Year 1

Add: Adjusting entry #1

Add: Adjusting entry #7

Sheet music supplies expense (unadjusted)

Add: Adjusting entry #5

Sheet music expense incurred in Year 1

Adjusting entry #2

Fees Earned in Year 1

Lesson revenue earned (unadjusted)

PROBLEM 4.5B

b.

MARVELOUS MUSIC (concluded)

2. $ 7,400

3. 4,400$

400

$ 4,800

Advertising expense (no adjustment required)

Insurance expense incurred in Year 1

Insurance expense (unadjusted)

Add: Adjusting entry #3

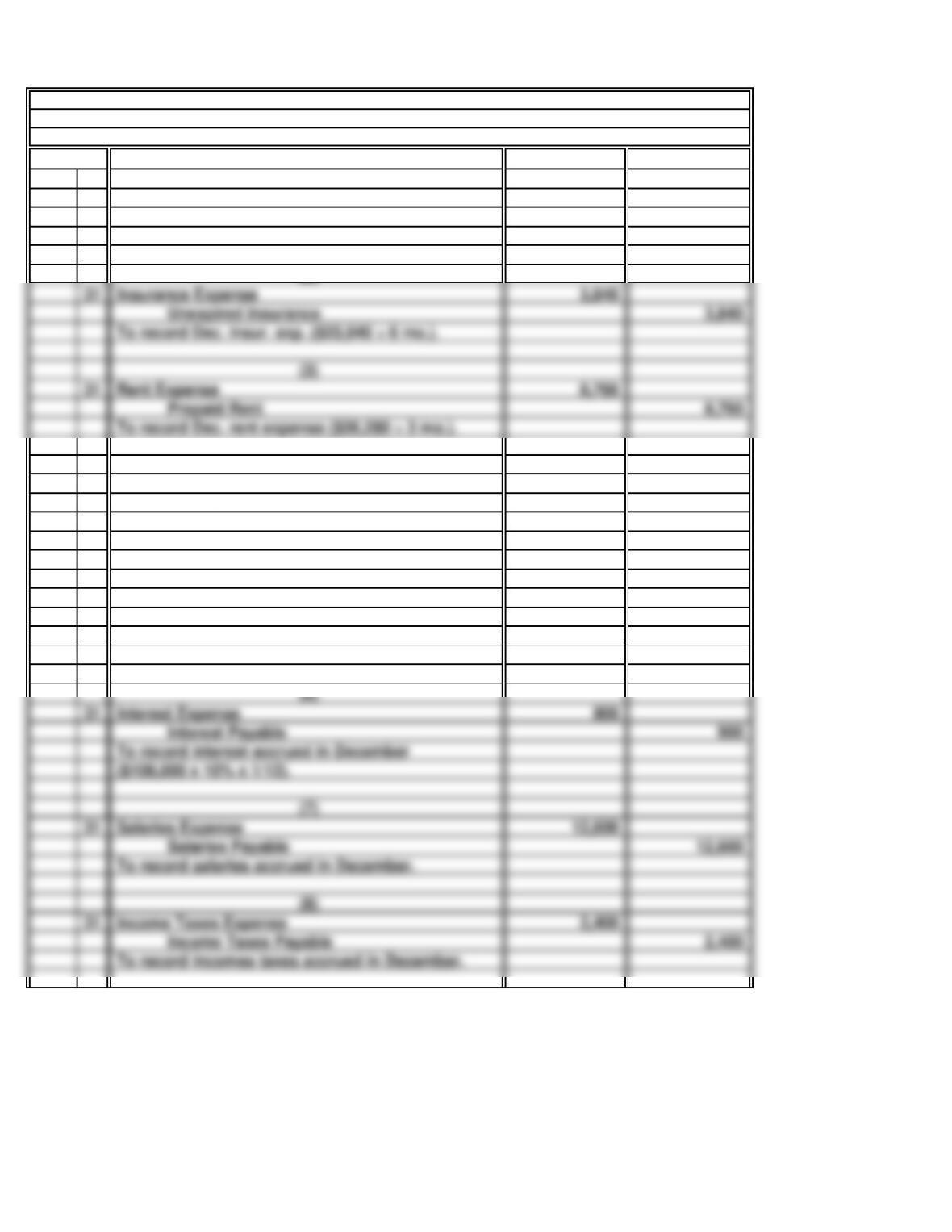

30 Minutes, Medium

Dec. 31 25,200

Client Fees Earned 25,200

31 2,064

Office Supplies 2,064

31 3,600

Accumulated Dep.: Computer Equip. 3,600

31 900

Interest Payable 900

31 12,600

Salaries Payable 12,600

31 2,400

Income Taxes Payable 2,400

To record incomes taxes accrued in December.

Interest Expense

(7)

($108,000 x 10% x 1/12).

To record interest accrued in December

Income Taxes Expense

To record salaries accrued in December.

Salaries Expense

(6)

PROBLEM 4.6B

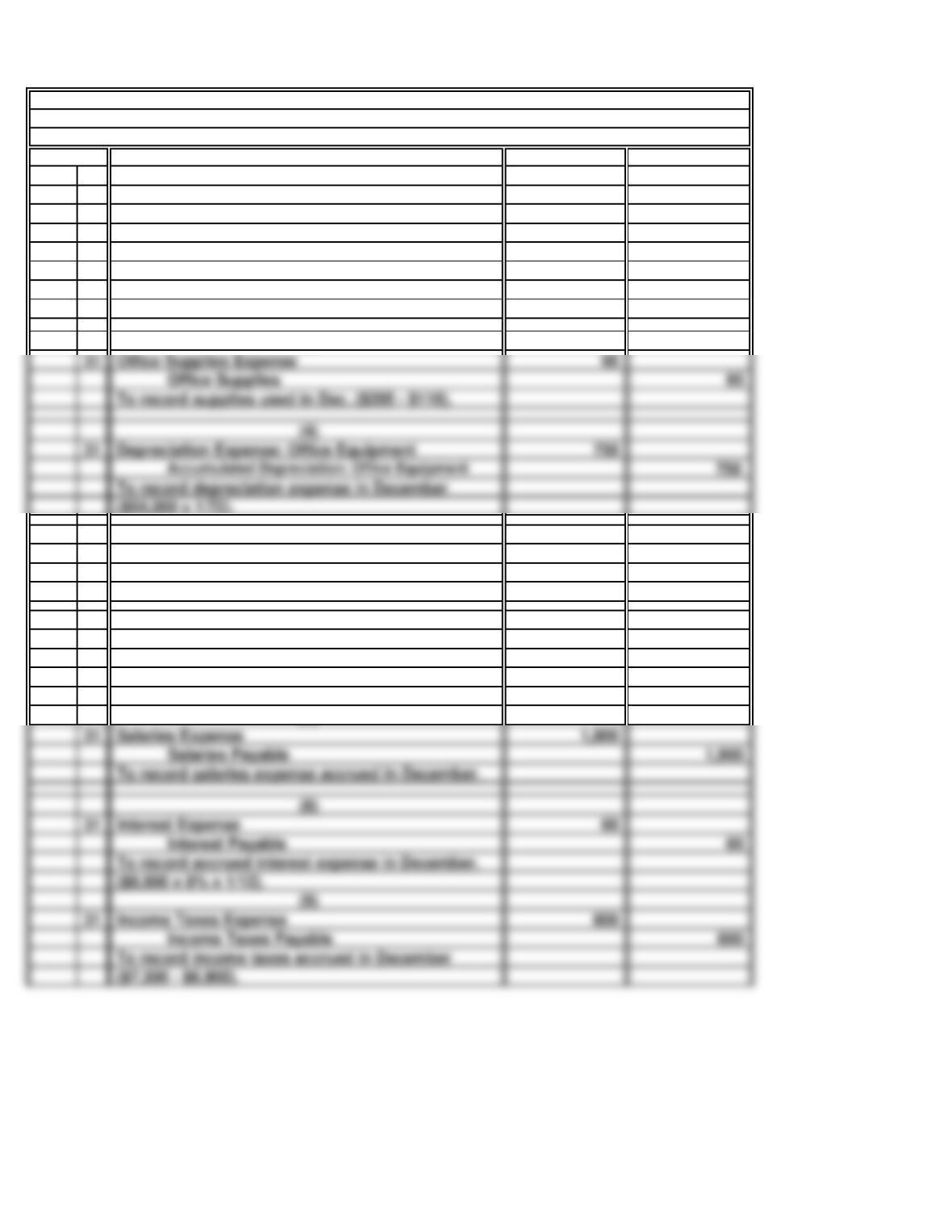

Office Supplies Expense

MATE EASE

(4)

a.

Year 1

General Journal

Unearned Member Dues

To record office supplies used in December

To record December depreciation expense

(5)

Depreciation Expense: Computer Equip.

($2,592 – $528).

($129,600 ÷ 36 mo.).

(Adjusting Entries)

(1)

(2)

earned revenue.

To convert previously unearned revenue to

Unexpired Insurance 3,840

Prepaid Rent 8,760

Rent Expense

To record Dec. insur. exp. ($23,040 ÷ 6 mo.).

(3)

To record Dec. rent expense ($26,280 ÷ 3 mo.).

Insurance Expense

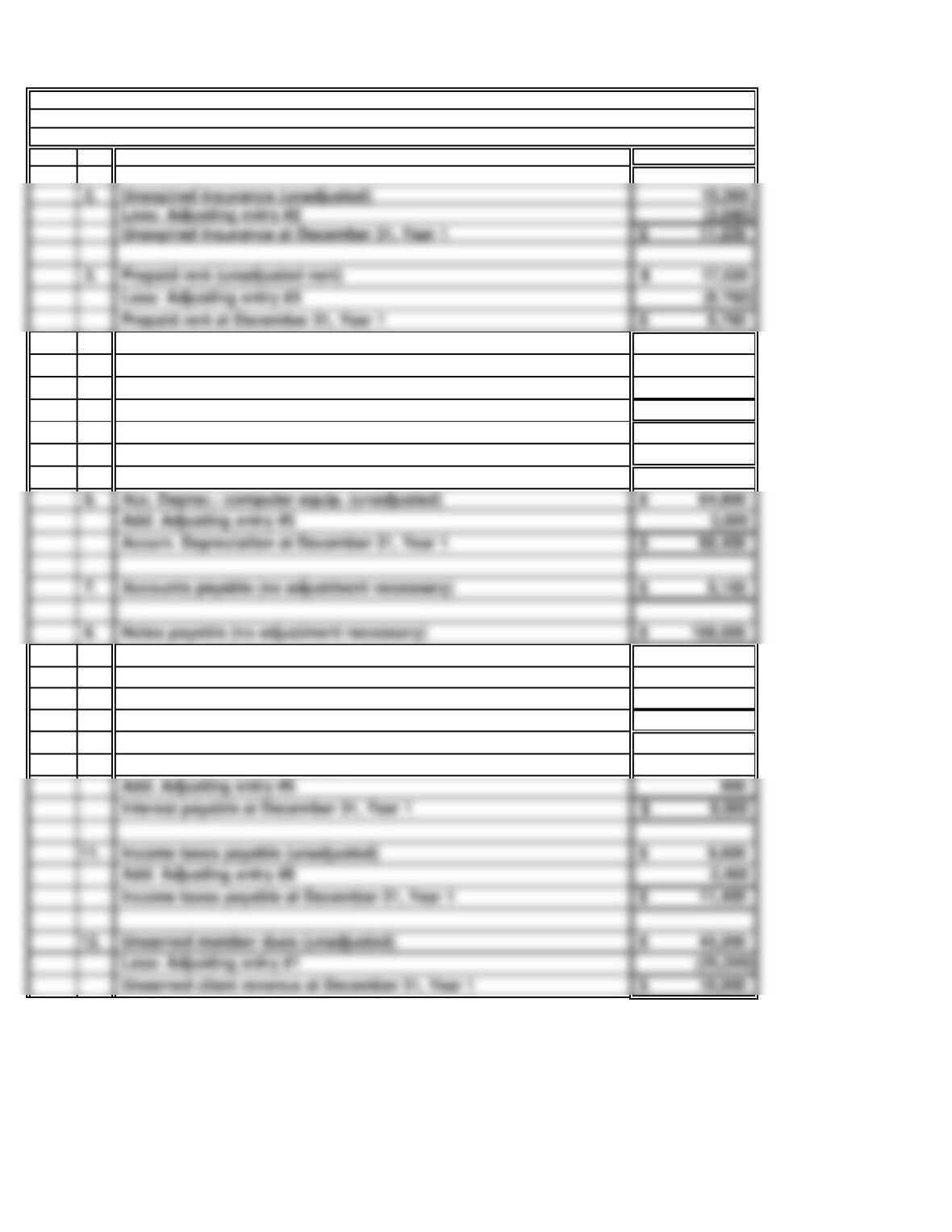

1. $ 203,400

4. $ 2,592

(2,064)

528$

5. 129,600$

6. $ 64,800

$ 68,400

7. $ 5,160

8. $ 108,000

Acc. Deprec.: computer equip. (unadjusted)

Add: Adjusting entry #5

Accum. Depreciation at December 31, Year 1

Accounts payable (no adjustment necessary)

Notes payable (no adjustment necessary)

9. –$

12,600

$ 12,600

10. $ 8,100

900

11. $ 9,000

$ 11,400

12. $ 43,200

$ 18,000

Add: Adjusting entry #6

Interest payable at December 31, Year 1

Unearned client revenue at December 31, Year 1

Less: Adjusting entry #1

Unearned member dues (unadjusted)

Income taxes payable (unadjusted)

Add: Adjusting entry #8

Income taxes payable at December 31, Year 1

Cash (no adjustment required)

PROBLEM 4.6B

b.

MATE EASE (continued)

Interest payable (unadjusted)

Computer equip. (no adjustment necessary)

Less: Adjusting entry #4

Office supplies at December 31, Year 1

Office supplies (unadjusted)

Salaries payable at December 31, Year 1

Add: Adjusting entry #7

Salaries payable (unadjusted)

2. 15,360

3. 17,520$

(8,760)

$ 8,760

Prepaid rent (unadjusted rent)

Less: Adjusting entry #2

Unexpired insurance at December 31, Year 1

Unexpired insurance (unadjusted)

Less: Adjusting entry #3

Prepaid rent at December 31, Year 1

c.

The company is following the realization principle requiring that revenue not

PROBLEM 4.6A

MATE EASE (concluded)

60 Minutes, Strong

Dec. 31 1,500

Client Fees Earned 1,500

31 2,500

Client Fees Earned 2,500

31 300

Prepaid Rent 300

31 90

Unexpired Insurance 90

31 1,900

Salaries Payable 1,900

31 60

Interest Payable 60

31 600

Income Taxes Payable 600

Interest Expense

To record salaries expense accrued in December.

Salaries Expense

($7,500 – $6,900).

Income Taxes Expense

To record income taxes accrued in December

(8)

To record accrued interest expense in December.

($9,000 x 8% x 1/12).

(9)

(5)

($1,080 x 1/12).

Rent Expense

To record office rent in December ($1,800 x 1/6).

(6)

(7)

To record December insurance expense

Insurance Expense

PROBLEM 4.7B

Unearned Retainer Fees

To record advance collections earned in December.

STILLMORE INVESTIGATIONS

Accounts Receivable

a.

(Adjusting Entries)

(1)

(2)

(3)

Year 1

General Journal

To record accrued revenue in December.

Office Supplies 95

31 750

To record depreciation expense in December

Depreciation Expense: Office Equipment

($54,000 x 1/72).

(4)

Office Supplies Expense

To record supplies used in Dec. ($205 – $110).

b.

40,585$

3,500

110

900

1,000

1,900

30,000

8,000

1,000

64,000

700

9,000

6,075

1,100

7,500

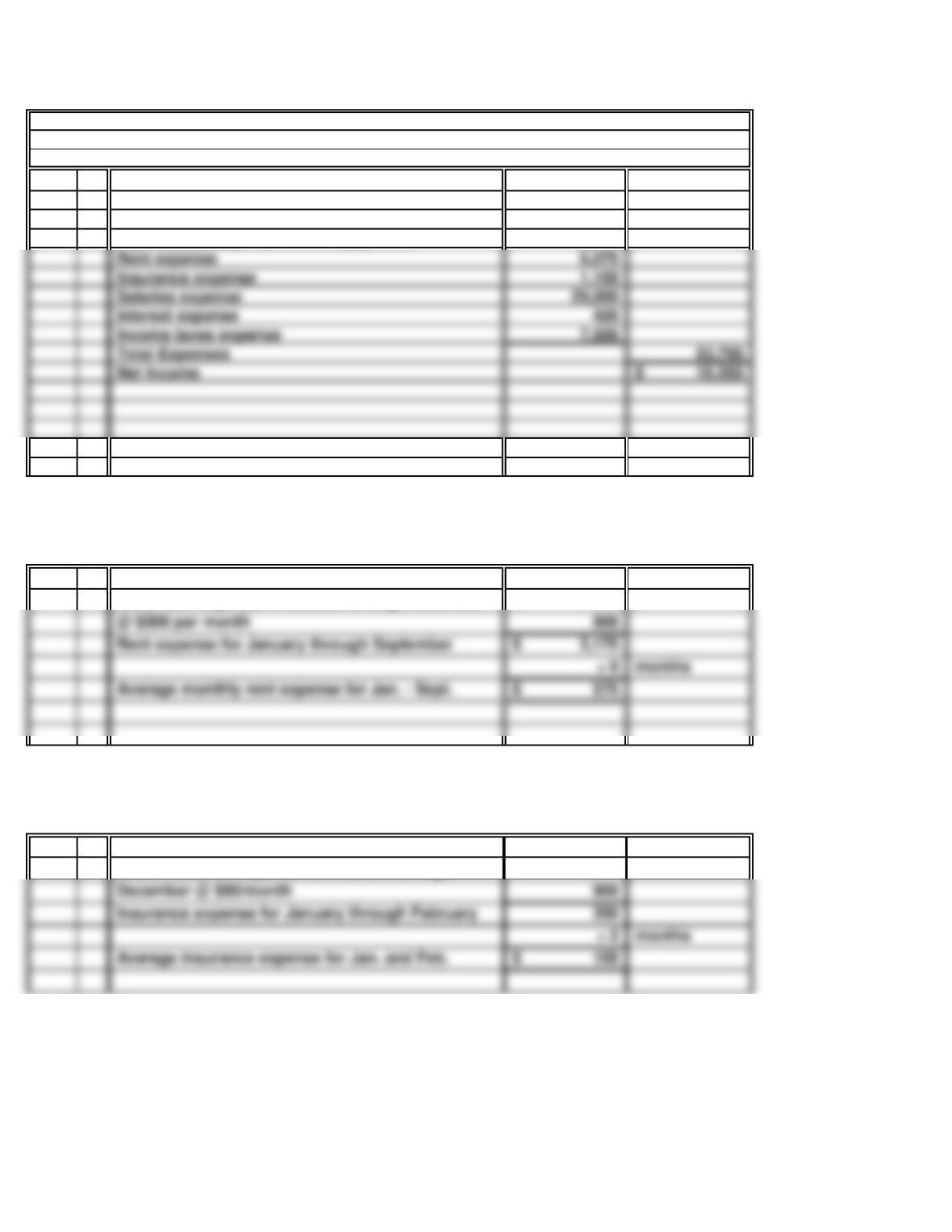

Salaries expense

Depreciation expense: Office equipment

Rent expense

Insurance expense

Income tax expense

Interest expense

Salaries payable

Unearned retainer fees

Retained earnings

Dividends

Client fees earned

Office supplies expense

PROBLEM 4.7B

STILLMORE INVESTIGATIONS (continued)

STILLMORE INVESTIGATIONS

December 31, Year 1

Cash

Capital stock

Adjusted Trial Balance

Accounts receivable

Office supplies

Prepaid rent

180

2,350

9,000

Income taxes payable

Note payable

Accumulated depreciation: Office equipment

Interest payable

Accounts payable

Unexpired insurance

Office Equipment

c.

64,000$

700$

9,000

d.

6,075$

Average monthly rent expense for Jan. – Sept.

@ $300 per month

e.

1,100$

December @ $90/month

Insurance expense for January through February

Average insurance expense for Jan. and Feb.

Insurance expense for 12 months ended Dec. 31, Year 1

Rent expense of $300/month in the last 3 months of the year was $275/month less

than the average monthly cost in the first 9 months of the year ($575 – $300).

Rent expense for 12 months ended December 31, Year 1

Less: Rent expense in October through December

PROBLEM 4.7B

STILLMORE INVESTIGATIONS (continued)

STILLMORE INVESTIGATIONS

For the Year Ended December 31, Year 1

Income Statement

Office supplies expense

Client fees earned

Depreciation expense: office equipment

Less: Insurance expense from March through

Insurance expense of $90/month in the last 10 months of the year was $10/month

less than the average monthly cost in the first 2 months of the year ($100 – $90).

6,075

1,100

7,500

Salaries expense

Rent expense

Insurance expense

Interest expense

Income taxes expense

Net Income

Total Expenses

g.

Net Owners’

Revenue – Expenses = Income Assets = Liabilities + Equity

INE I I NE I

INE INE D I

2.

3.

1.

Adjustment

PROBLEM 4.7B

STILLMORE INVESTIGATIONS (concluded)

Income Statement

Balance Sheet

20 Minutes, Strong

a. NE NE NE U U NE

Total

Assets

Total

Liabilities

Owners’

Equity

PROBLEM 4.8B

STEPHEN CORPORATION

Error

Total

Revenue

Total

Expenses

Net

Income

Recorded a declared

but unpaid dividend by

debiting dividends and

crediting Cash.

g. NE U O NE U O

Purchased equipment

and debited supplies

expense and credited

Recorded the sale of

capital stock as a debit

to cash and a credit to

30 Minutes, Medium

a.

b.

c.

f.

SOLUTIONS TO CRITICAL THINKING CASES

YEAR-END ADJUSTMENTS

Management services rendered in December, but which are not billed to customers until

CASE 4.1

Not recording salaries and wages expense until payroll dates is a common practice. However,

No adjusting entry is needed, because although the revenue was collected in advance on

Three months’ revenue was collected in advance on December 1 and was credited to an

the period. Of course, recognizing revenue also increases owners’ equity.

e.

An adjusting entry should be made to record depreciation expense on all equipment owned.

25 Minutes, Medium

a. (1)

(2)

(3)

b.

CASE 4.2

AVIS RENT-A-CAR

THE CONCEPT OF MATERIALITY:

The concept of materiality does mean that financial statements are not precise “down to

The concept of materiality would not permit Avis to charge the purchase of new

automobiles for its rental fleet directly to expense. Although the cost of each individual

An event or transaction is “material” when knowledge of the item reasonably may be

expected to influence the decisions of users of financial statements. One

In evaluating the “materiality” of an event or transaction, accountants should consider:

However, charging the purchases of new cars directly to expense would definitely cause a

10 Minutes, Easy

a.

b.

Note to instructor: It is likely that the bank would insist upon receiving a set of audited financial

The decision by management to wait three years before converting the $40,000 capitalized

advertising expenditure to advertising expense clearly violates generally accepted

ETHICS, FRAUD & CORPORATE GOVERNANCE

CASE 4.3

The decision to capitalize the $40,000 advertising expenditure for three years certainly

has ethical implications if management’s intent was to purposely inflate profitability, and

EXPENSE MANIPULATION

10 Minutes, Easy

1.

CASE 4.4

IDENTIFYING ACCOUNTS

Accounts from Hershey’s balance sheet likely to have required an adjusting entry are:

Accounts Receivable–Trade

INTERNET

2.

3.

4.

7.