25 Minutes, Strong

a. (1)

(3)

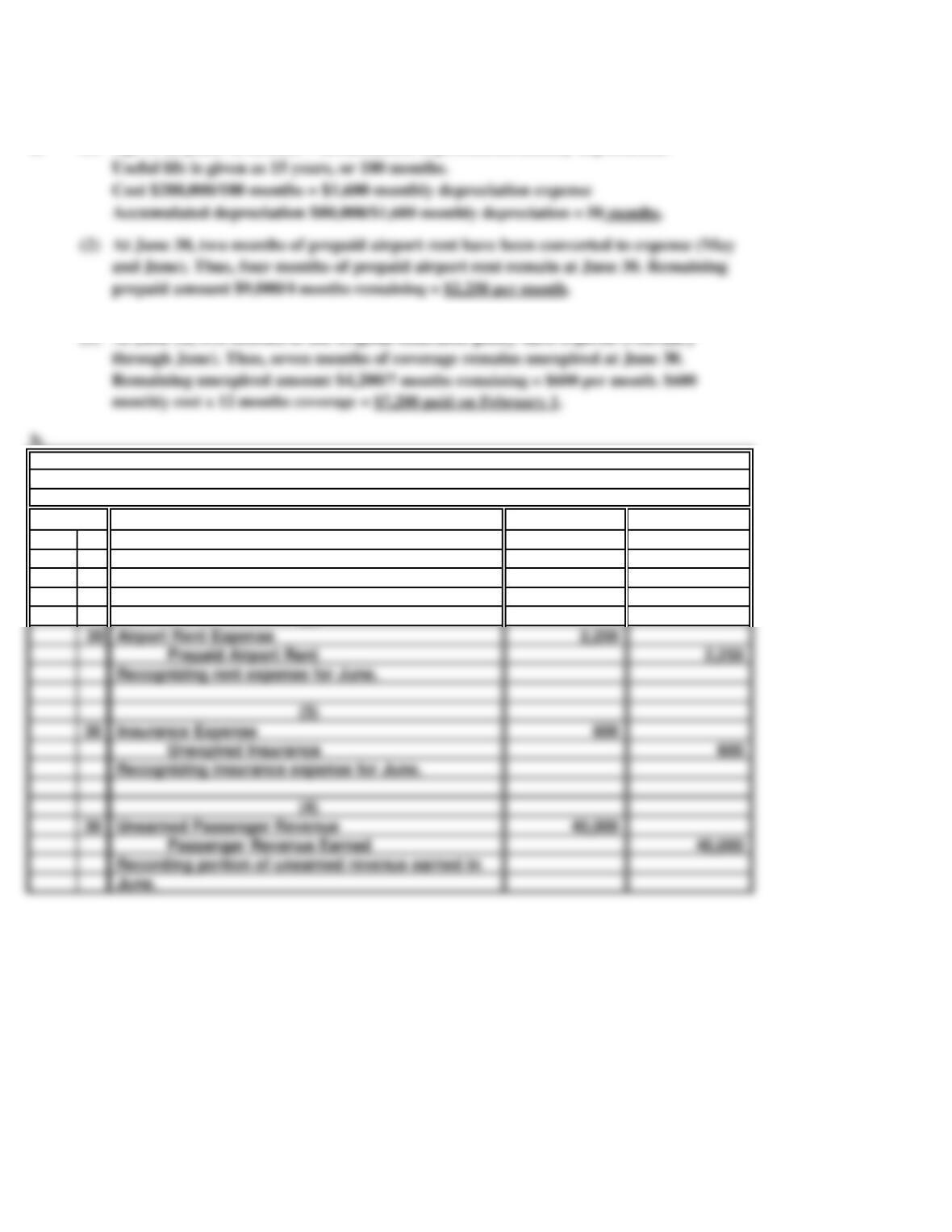

June 30 1,600

Accumulated Depreciation: Airplane 1,600

Prepaid Airport Rent 2,250

Unexpired Insurance 600

Passenger Revenue Earned 40,000

(3)

June.

Recognizing insurance expense for June.

Unearned Passenger Revenue

Recording portion of unearned revenue earned in

(4)

Insurance Expense

Airport Rent Expense

Recognizing rent expense for June.

Depreciation Expense

To record June depreciation expense on airplane.

(2)

(Adjusting Entries)

(1)

General Journal

PROBLEM 4.3A

GUNFLINT ADVENTURES

At June 30, five months of the original insurance policy have expired (February

Age of airplane in months = accumulated depreciation/monthly depreciation.

(2)

Useful life is given as 15 years, or 180 months.

Cost $288,000/180 months = $1,600 monthly depreciation expense

Accumulated depreciation $80,000/$1,600 monthly depreciation = 50 months.

30 Minutes, Medium

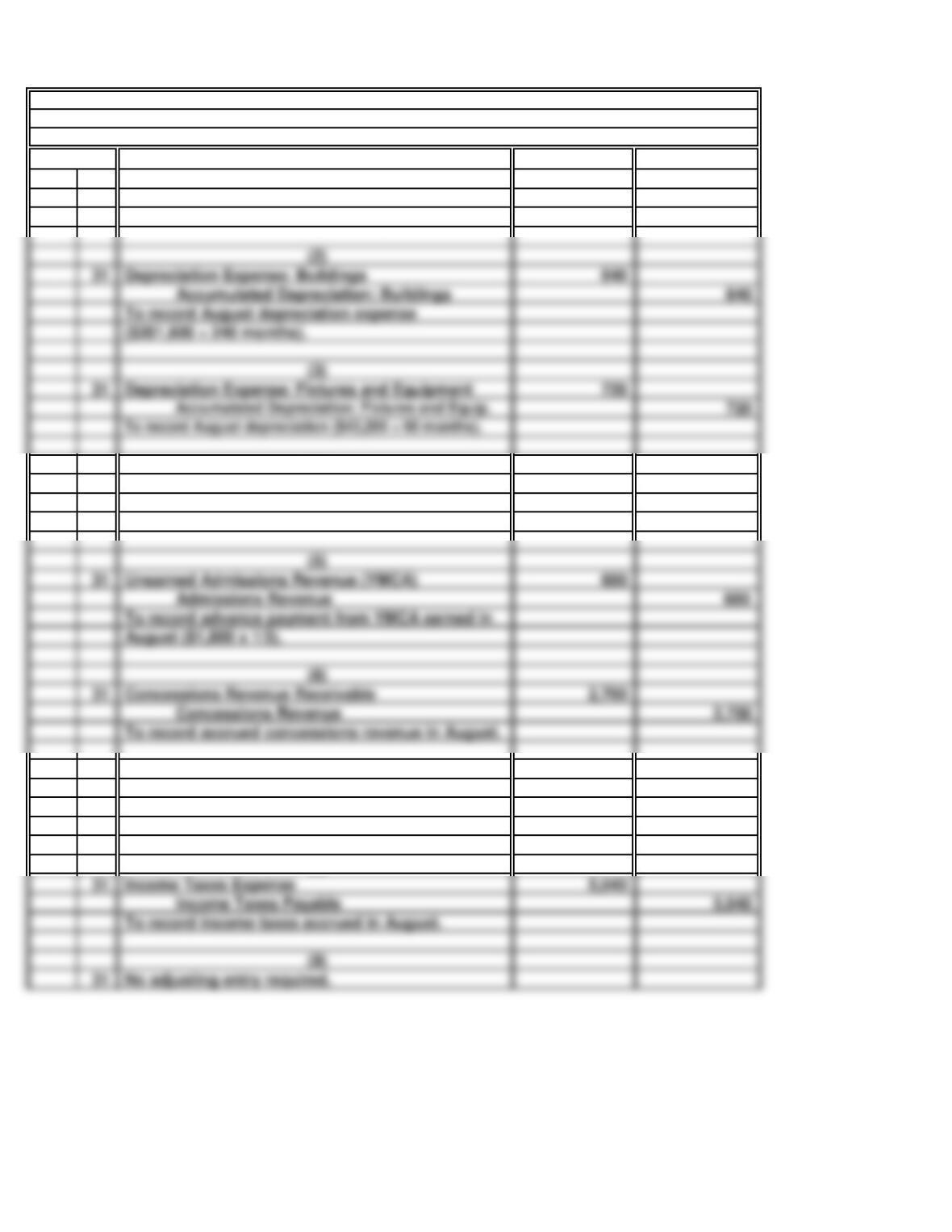

Aug. 31 18,240

Prepaid Film Rental 18,240

31 1,800

Interest Payable 1,800

31 600

31 2,700

Concessions Revenue 2,700

To record advance payment from YMCA earned in

(5)

Unearned Admissions Revenue (YMCA)

Concessions Revenue Receivable

To record accrued concessions revenue in August.

August ($1,800 x 1/3).

(6)

31 2,040

Salaries Payable 2,040

31 5,040

31

No adjusting entry required.

(9)

Income Taxes Expense

To record income taxes accrued in August.

PROBLEM 4.4A

CAMPUS THEATER

Interest Expense

(4)

Current Yr.

a.

(Adjusting Entries)

(1)

General Journal

(7)

(8)

Interest expense accrued in August.

Film Rental Expense

Film rental expense incurred in August.

To record accrued salary expense in August.

Salaries Expense

Accumulated Depreciation: Buildings 840

Depreciation Expense: Fixtures and Equipment

Depreciation Expense: Buildings

To record August depreciation expense

($201,600 ÷ 240 months).

(2)

(3)

b. (1)

c.

Corporations must pay income taxes in several installments throughout the year. The

balance in the Income Taxes Expense account represents the total amount of income taxes

PROBLEM 4.4A

CAMPUS THEATER (concluded)

Eight months (bills received January through August). Utilities bills are recorded as

30 Minutes, Medium

Dec. 31 1,500

Fees Earned 1,500

31 500

Accumulated Depreciation: Equipment 500

31 80

Interest Payable 80

31 2,700

Salaries Payable 2,700

31 3,000

Income Taxes Payable 3,000

To record income taxes accrued in December.

(9)

Salaries Expense

Income Taxes Expense

To record income taxes accrued in December.

(8)

(6)

Depreciation Expense: Equipment

To record interest accrued in December

Interest Expense

($12,000 x 8% x 1/12).

(7)

($60,000 ÷ 120 mo.).

To record December depreciation expense

Year 1

Accounts Receivable

To record accrued but uncollected fees earned.

PROBLEM 4.5A

TERRIFIC TEMPS

a.

(Adjusting Entries)

General Journal

(1)

(2)

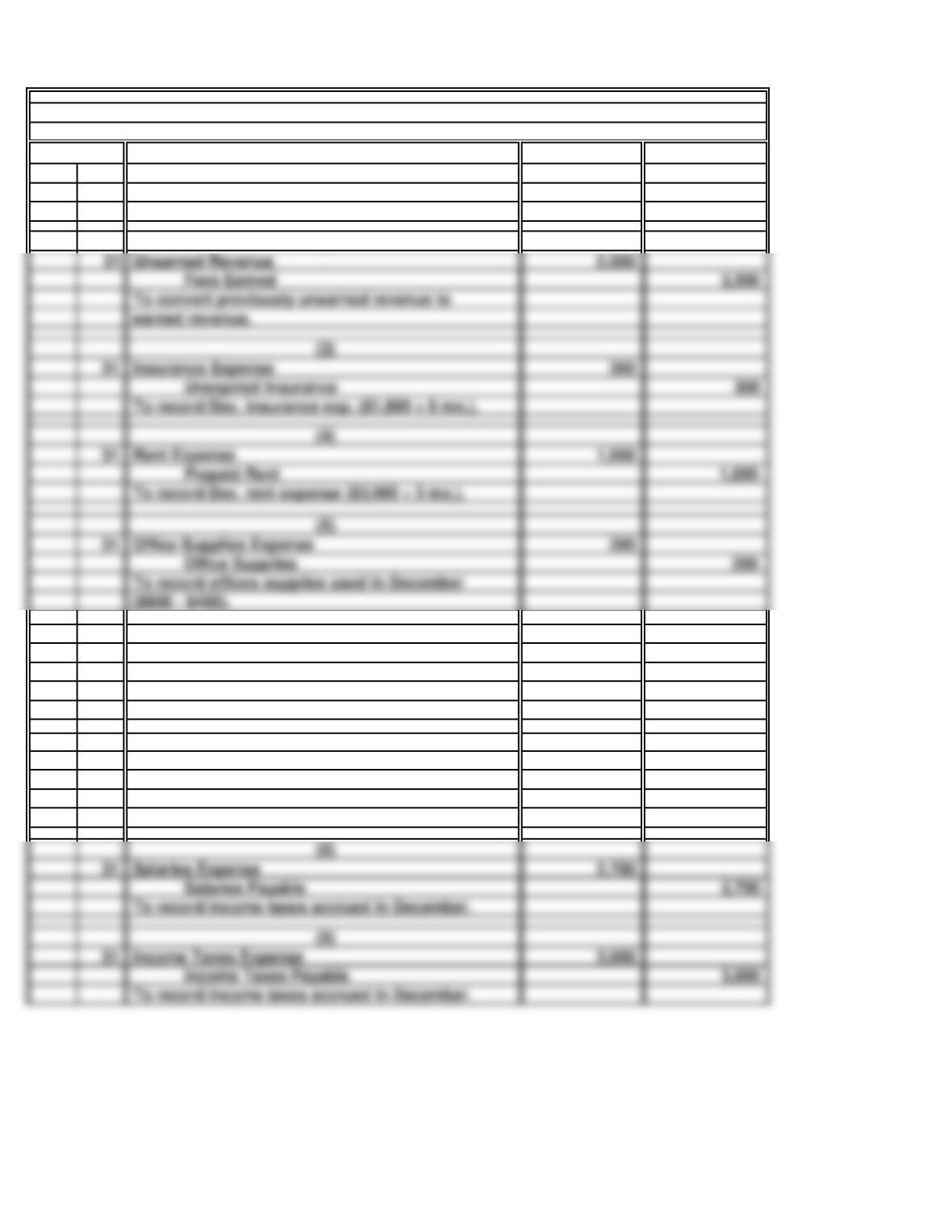

Fees Earned 2,500

31 300

Unexpired Insurance 300

31 1,000

Prepaid Rent 1,000

31 200

Office Supplies 200

Insurance Expense

To record Dec. rent expense ($3,000 ÷ 3 mo.).

(5)

($600 – $400).

Rent Expense

To record offices supplies used in December

Office Supplies Expense

(4)

earned revenue.

Unearned Revenue

To convert previously unearned revenue to

To record Dec. insurance exp. ($1,800 ÷ 6 mo.).

(3)

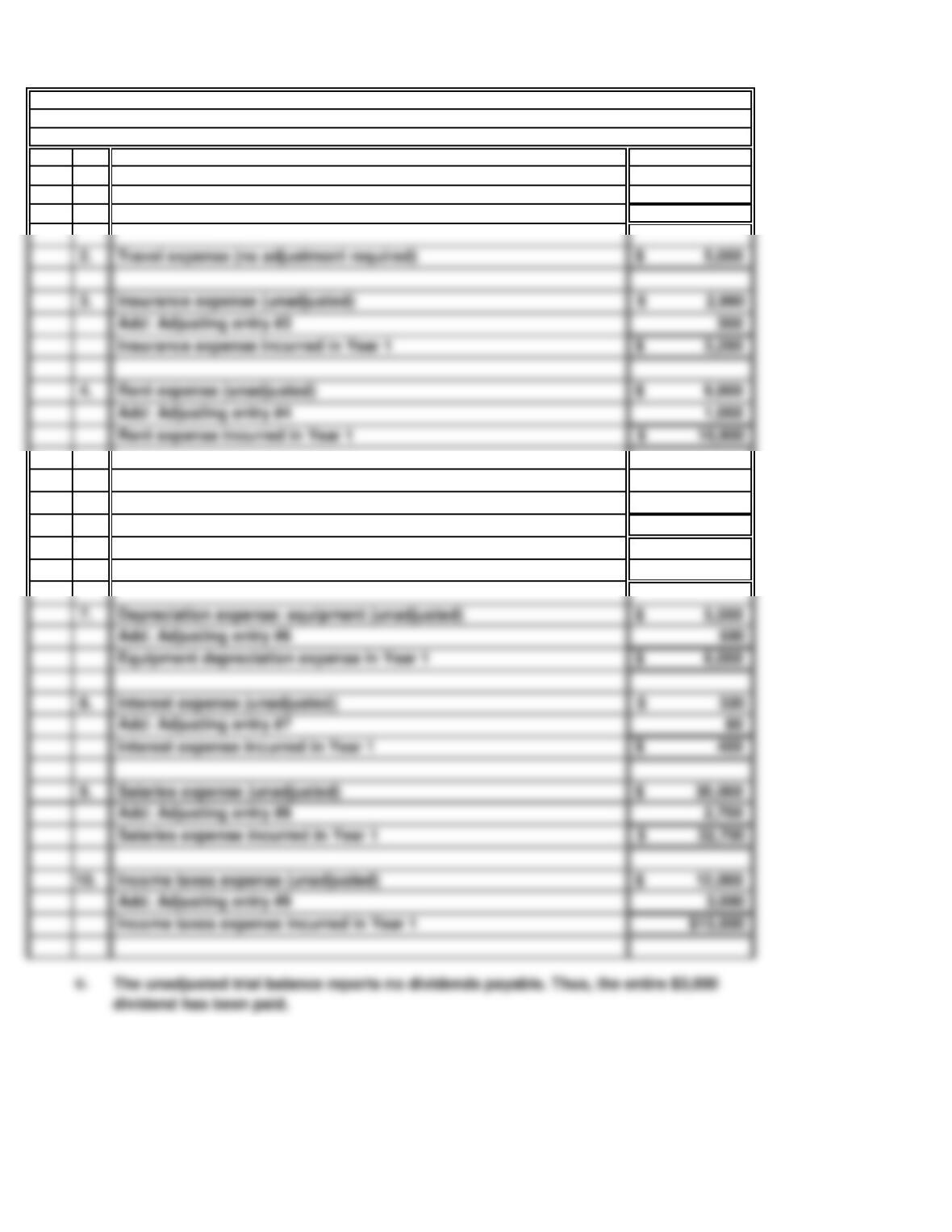

1. $ 75,000

1,500

2,500

$ 79,000

5. $ 780

200

$ 980

6. 4,800$

$ 6,000

80

$ 400

2,700

Add: Adjusting entry #8

Add: Adjusting entry #6

Equipment depreciation expense in Year 1

Add: Adjusting entry #7

Interest expense incurred in Year 1

Salaries expense incurred in Year 1

Income taxes expense incurred in Year 1

PROBLEM 4.5A

b.

TERRIFIC TEMPS (concluded)

Fees earned (unadjusted)

Add: Adjusting entry #1

Adjusting entry #2

Fees Earned in Year 1

Add: Adjusting entry #5

Office supplies expense incurred in Year 1

Office supplies expense (unadjusted)

Utilities expense (no adjustment required)

2. $ 5,000

3. 2,980$

300

$ 3,280

4. $ 9,900

1,000

Rent expense (unadjusted)

Add: Adjusting entry #4

Insurance expense incurred in Year 1

Add: Adjusting entry #3

Travel expense (no adjustment required)

Insurance expense (unadjusted)

Rent expense incurred in Year 1

30 Minutes, Medium

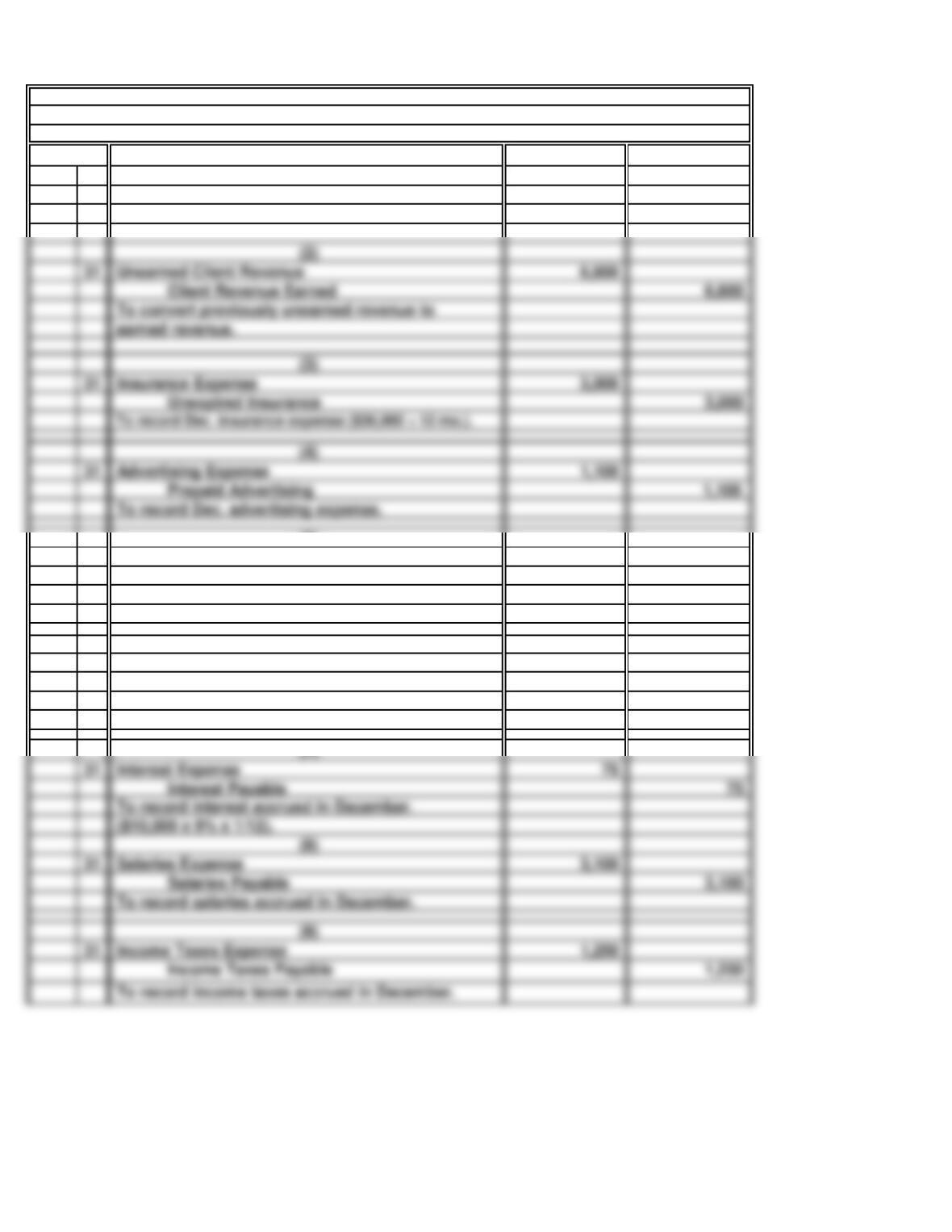

Dec. 31 6,400

Client Revenue Earned 6,400

31 2,900

Climbing Supplies 2,900

31 1,200

Accumulated Dep.: Climbing Equipment 1,200

31 75

31 3,100

Salaries Payable 3,100

31 1,250

Income Taxes Expense

(9)

To record salaries accrued in December.

($10,000 x 9% x 1/12).

(8)

To record interest accrued in December.

Salaries Expense

Interest Expense

(7)

(5)

To recorded December depreciation expense

($4,900 – $2,000).

To record accrued but uncollected revenue.

Climbing Supplies Expense

a.

(Adjusting Entries)

General Journal

PROBLEM 4.6A

(6)

($57,600 ÷ 48 mo.).

Depreciation Expense: Climbing Equip.

To record climbing supplies used in December

ALPINE EXPEDITIONS

Year 1

Accounts Receivable

(1)

Client Revenue Earned 6,600

Unexpired Insurance 3,000

31 1,100

Prepaid Advertising 1,100

(3)

Unearned Client Revenue

To convert previously unearned revenue to

To record Dec. advertising expense.

Advertising Expense

earned revenue.

(4)

(2)

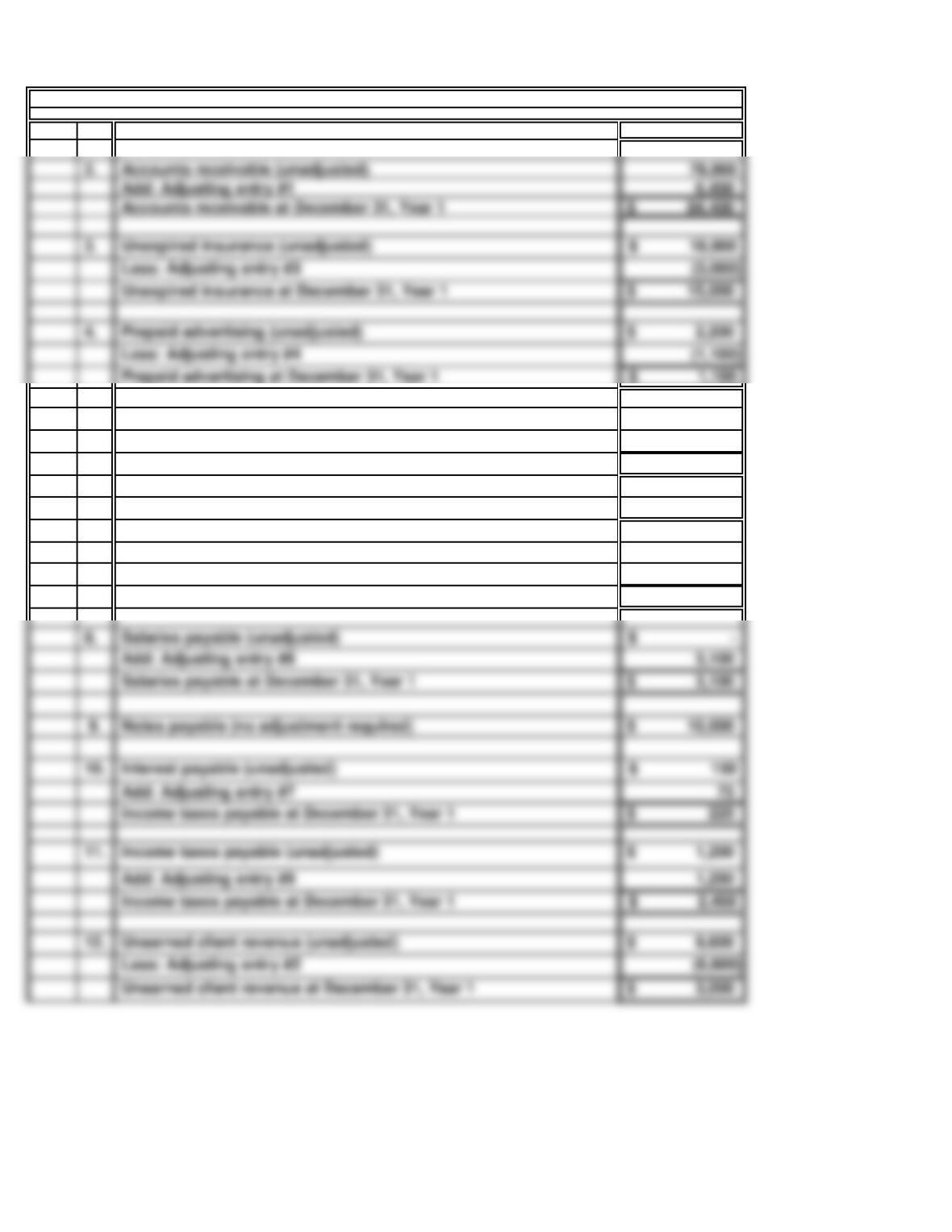

1. $ 13,900

5. $ 4,900

(2,900)

$ 2,000

6. 57,600$

7. $ 38,400

1,200

$ 39,600

8. –$

3,100

$ 3,100

9. $ 10,000

$ 225

1,250

12. $ 9,600

Notes payable (no adjustment required)

Add: Adjusting entry #9

Unearned client revenue (unadjusted)

Income taxes payable at December 31, Year 1

Salaries payable (unadjusted)

Salaries payable at December 31, Year 1

Add: Adjusting entry #8

Add: Adjusting entry #7

Acc. Depreciation: climbing equip. at December 31, Year 1

PROBLEM 4.6A

b.

ALPINE EXPEDITIONS (continued)

Cash (no adjustment required)

Acc. Depreciation: climbing equip. (unadjusted)

Less: Adjusting entry #5

Climbing supplies (unadjusted)

Add: Adjusting entry #6

Climbing supplies at December 31, Year 1

Climbing equipment (no adjustment necessary)

2. 78,000

3. 18,000$

(3,000)

$ 15,000

4. $ 2,200

(1,100)

Unexpired insurance (unadjusted)

Less: Adjusting entry #3

Unexpired insurance at December 31, Year 1

Prepaid advertising (unadjusted)

Less: Adjusting entry #4

Add: Adjusting entry #1

Accounts receivable at December 31, Year 1

Accounts receivable (unadjusted)

Prepaid advertising at December 31, Year 1

c.

Deferred expenses are assets that eventually convert into expenses. For Alpine

PROBLEM 4.6A

ALPINE EXPEDITIONS (concluded)

60 Minutes, Strong

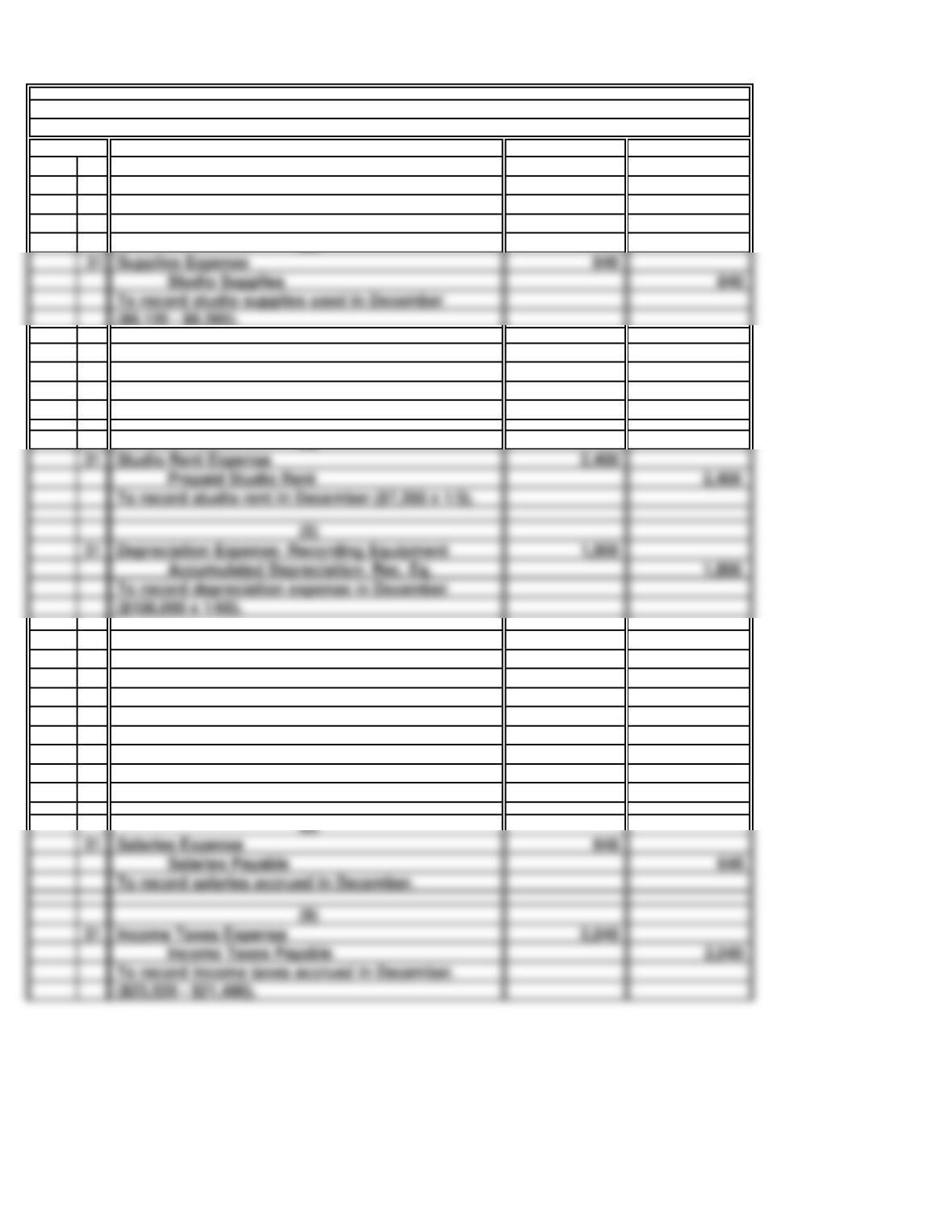

Dec. 31 5,280

Studio Revenue Earned 5,280

31 300

Unexpired Insurance 300

31 2,400

Prepaid Studio Rent 2,400

31 1,800

Accumulated Depreciation: Rec. Eq. 1,800

(5)

($108,000 x 1/60).

Depreciation Expense: Recording Equipment

To record studio rent in December ($7,200 x 1/3).

To record depreciation expense in December

Studio Rent Expense

31 144

Interest Payable 144

31 4,320

Studio Revenue Earned 4,320

31 648

Salaries Payable 648

31 2,040

Income Taxes Payable 2,040

($23,520 – $21,480).

Income Taxes Expense

To record income taxes accrued in December.

(8)

To record salaries accrued in December.

(9)

Salaries Expense

PROBLEM 4.7A

To record accrued studio revenue earned in

(4)

KEN HENSLEY ENTERPRISES, INC.

a.

(Adjusting Entries)

(1)

(2)

(3)

General Journal

To record advance collections earned in Dec.

Year 1

Insurance Expense

To record December insurance expense ($1800 x1/6).

Accounts Receivable

December.

Unearned Studio Revenue

December ($19,200 x 9% x 1/12).

(6)

(7)

To record accrued interest expense in

Interest Expense

Studio Supplies 840

($9,120 – $8,280).

To record studio supplies used in December

Supplies Expense

b.

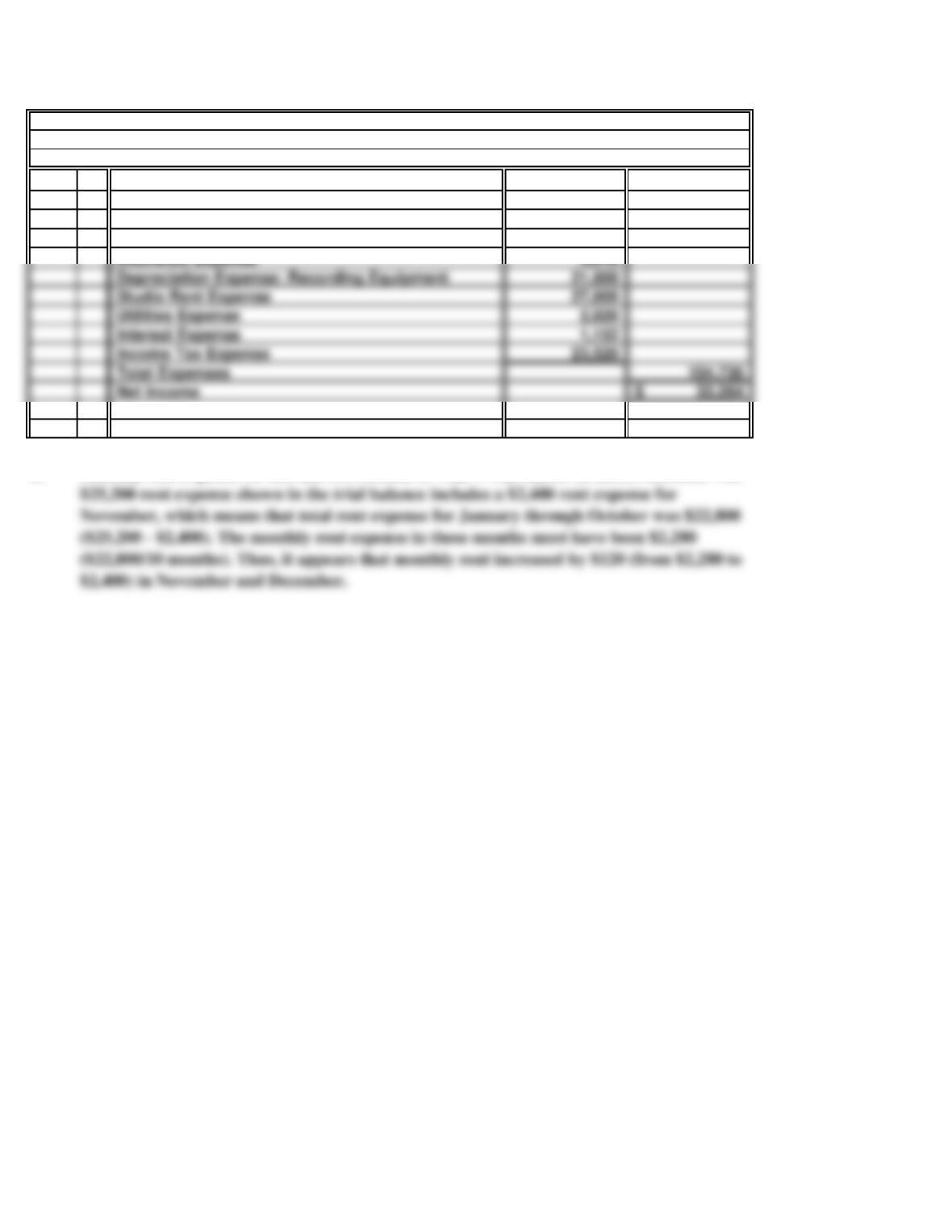

138,000$

22,248$

2,280

c.

Monthly rent expense for the last two months of Year 1 was $2,400 ($7,200/3 months). The

Supplies Expense

Salaries Expense

PROBLEM 4.7A

KEN HENSLEY ENTERPRISES, INC. (continued)

Ken Hensley Enterprises, Inc.

For the Year Ended December 31, Year 1

Studio Revenue Earned

Income Statement

3,516

2,820

1,152

Income Tax Expense

Studio Rent Expense

Interest Expense

Insurance Expense

Utilities Expense

Depreciation Expense: Recording Equipment

Net Income

Total Expenses

d.

3,516$

e.

f.

Net Owners’

Revenue – Expenses = Income Assets = Liabilities + Equity

INE I I NE I

3.

2.

PROBLEM 4.7A

KEN HENSLEY ENTERPRISES, INC. (concluded)

December 31, Year 1

Adjustment

Insurance expense of $300 per month in the last 5 months of the year was $12 per month

more than the average monthly cost in the first 7 months of the year ($300 – $288).

Insurance expense for 12 months ended

Income Statement

Balance Sheet

1.

Average monthly insurance expense for Jan.-July

@ $300/month

Less: Insurance expense for August through December

Insurance expense for January through July

months

20 Minutes, Strong

a. NE O U NE NE NE

b. NE U O O NE O

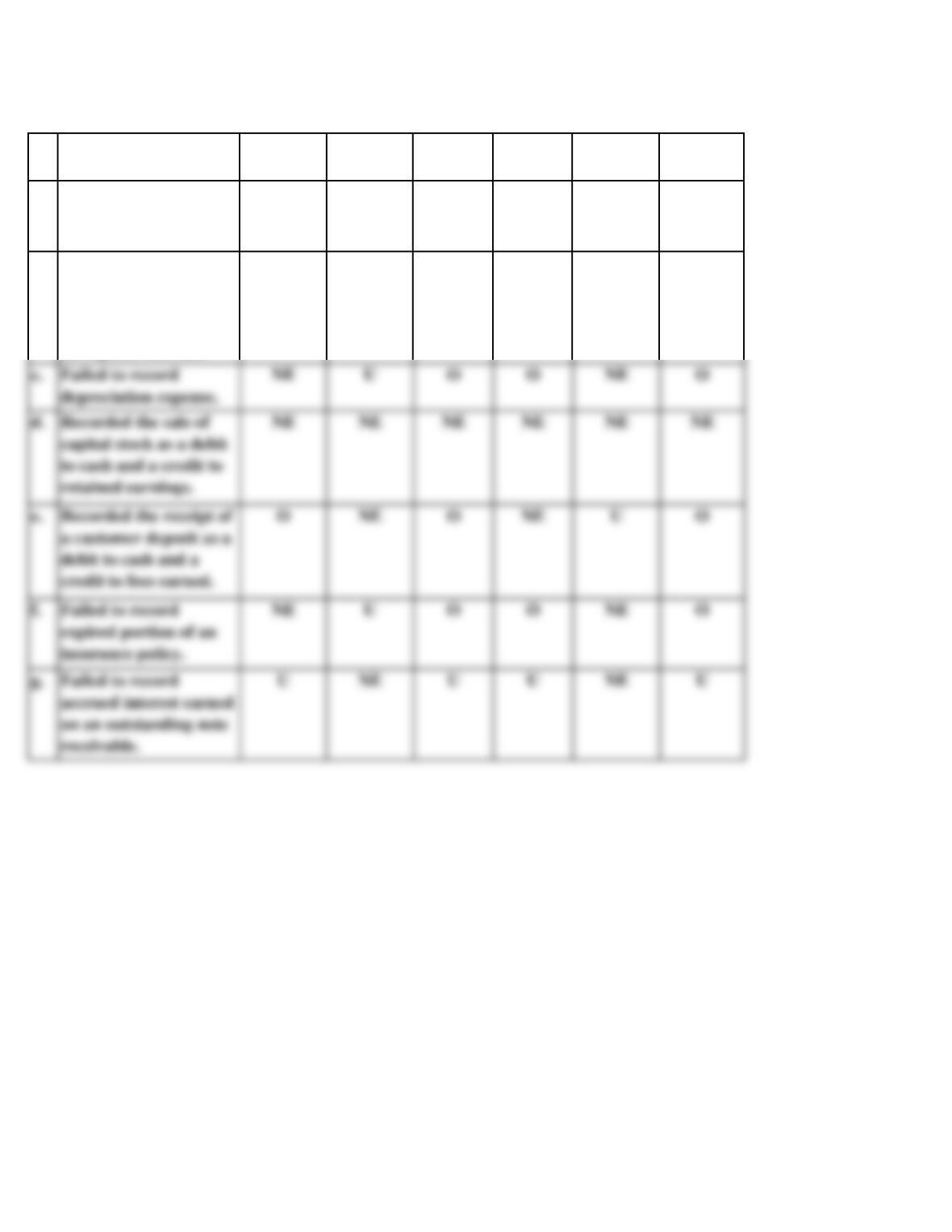

PROBLEM 4.8A

COYNE CORPORATION

Error

Total

Revenue

Total

Expenses

Net

Income

Total

Assets

Total

Liabilities

Owners’

Equity

Recorded a dividend as

an expense reported in

the income statement.

Recorded the payment

of an account payable

as a debit to accounts

payable and a credit to

an expense account.

20 Minutes, Easy

Dec. 31 13,600

Salaries Payable 13,600

31 1,250

Accumulated Depreciation: Furn. & fixtures 1,250

31 400

Interest Payable 400

31 900

31

31 12,600

Income Taxes Payable 12,600

To record income taxes accrued in December.

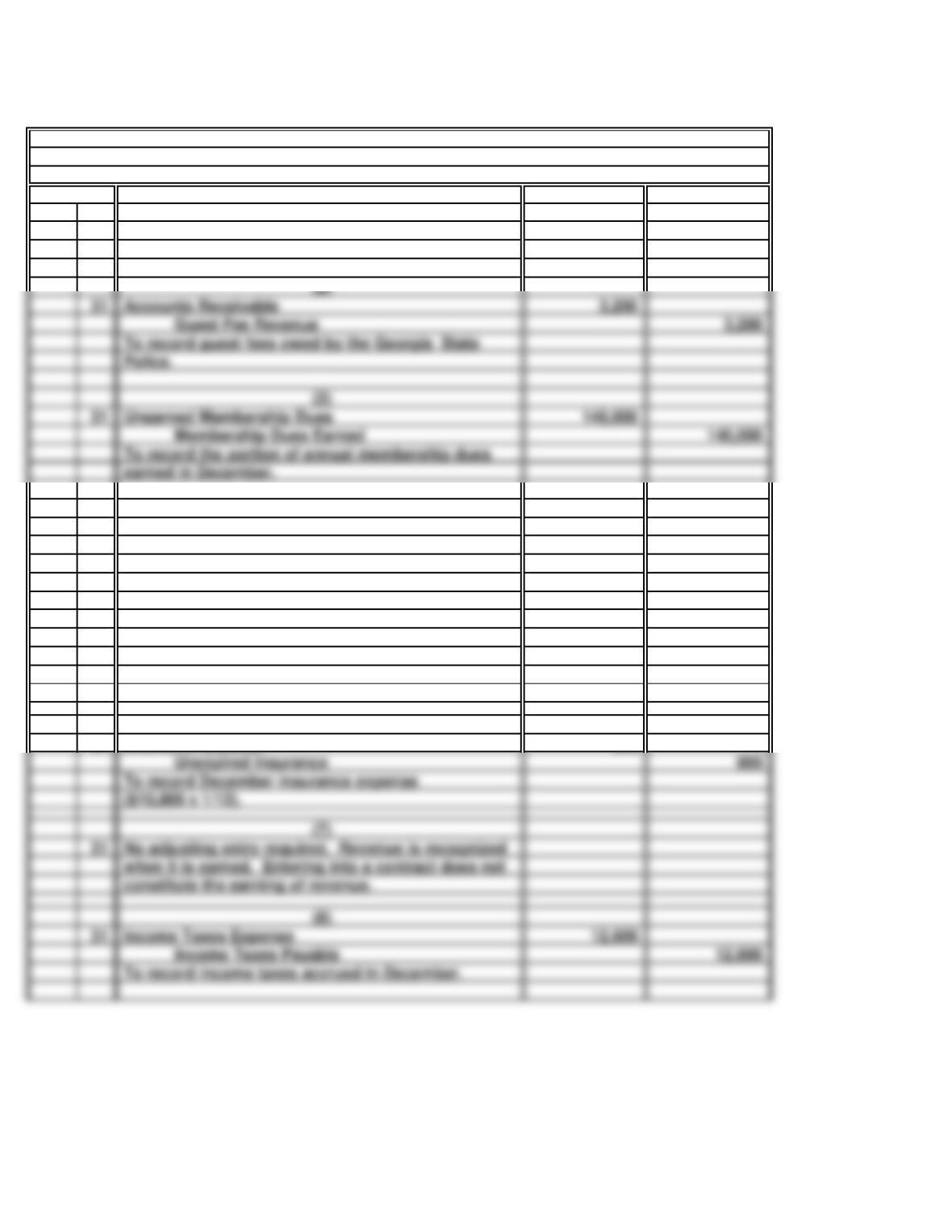

when it is earned. Entering into a contract does not

(8)

To record December insurance expense

(7)

constitute the earning of revenue.

No adjusting entry required. Revenue is recognized

($10,800 x 1/12).

Income Taxes Expense

Insurance Expense

(6)

($60,000 x 8% x 1/12).

To record accrued interest expense in December

SOLUTIONS TO PROBLEMS SET B

a.

(Adjusting Entries)

(1)

To record accrued salaries at December 31.

PROBLEM 4.1B

GEORGIA GUN CLUB

Current Yr.

Salaries Expense

($120,000 ÷ 8 years x 1/12).

Interest Expense

(4)

(5)

Depreciation Expense: Furniture and Fixtures

To record December depreciation expense

31 3,200

Guest Fee Revenue 3,200

Membership Dues Earned 140,000

Accounts Receivable

To record guest fees owed by the Georgia State

earned in December.

(2)

Police.

(3)

Unearned Membership Dues

To record the portion of annual membership dues

b.

1.

c.

Accruing unpaid expenses.

PROBLEM 4.1B

GEORGIA GUN CLUB (concluded)

The clubhouse was built in 1956 and has been fully depreciated for financial accounting

2.

3.

4.

5.

6.

7.

8.

Accruing uncollected revenue.

Converting liabilities to revenue.

Converting assets to expenses.

Accruing unpaid expenses.

Converting assets to expenses.

No adjusting entry required.

Accruing unpaid expenses.

40 Minutes, Medium

a.

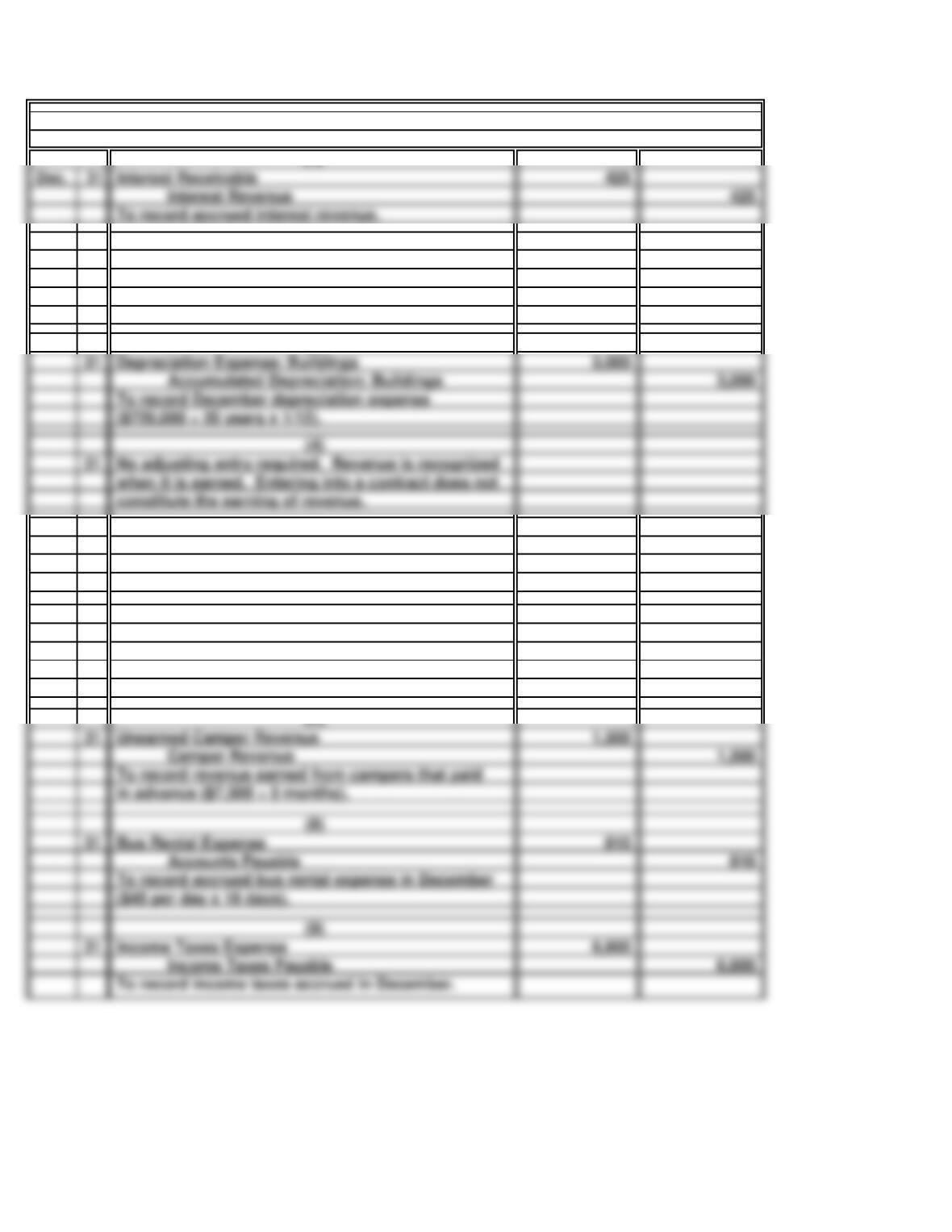

31 80

Interest Payable 80

31 3,000

Accumulated Depreciation: Buildings 3,000

31

Depreciation Expense: Buildings

To record December depreciation expense

(4)

($720,000 ÷ 20 years x 1/12).

No adjusting entry required. Revenue is recognized

when it is earned. Entering into a contract does not

constitute the earning of revenue.

31 1,515

Salaries Payable 1,515

31 2,700

Camper Revenue 2,700

31 1,500

Camper Revenue 1,500

31 810

Accounts Payable 810

31 6,600

Income Taxes Payable 6,600

Bus Rental Expense

To record revenue earned from campers that paid

(9)

Income Taxes Expense

Unearned Camper Revenue

($45 per day x 18 days).

To record accrued bus rental expense in December

(8)

in advance ($7,500 ÷ 5 months).

Interest Expense

PROBLEM 4.2B

(Adjusting Entries)

(1)

General Journal

BIG OAKS

(2)

(3)

Salaries Expense

To record accrued interest expense in December

($12,000 x 8% x 1/12).

To record accrued camper revenue earned in

Camper Revenue Receivable

December.

(5)

To record accrued salary expense in December.

(6)

Interest Revenue 425

Interest Receivable

To record accrued interest revenue.

b.

1.

c.

Owners’

Revenue –Expenses = Assets = Liabilities + Equity

e.

557,000$

December depreciation expense from part a …………………………..

Accumulated depreciation, buildings, December 31 ………………………………

Net book value at December 31 …………………………………………..

Original cost of buildings ………………………………………………

720,000$

Balance Sheet

Adjustment

Net

Income

Income Statement

BIG OAKS (concluded)

PROBLEM 4.2B

Accruing uncollected revenue.

2.

3.

4.

5.

6.

7.

8.

9.

Accruing unpaid expenses.

Converting liabilities to revenue.

Accruing unpaid expenses.

Accruing uncollected revenue.

Accruing unpaid expenses.

Accruing unpaid expenses.

Converting assets to expenses.

No adjusting entry required.

25 Minutes, Strong

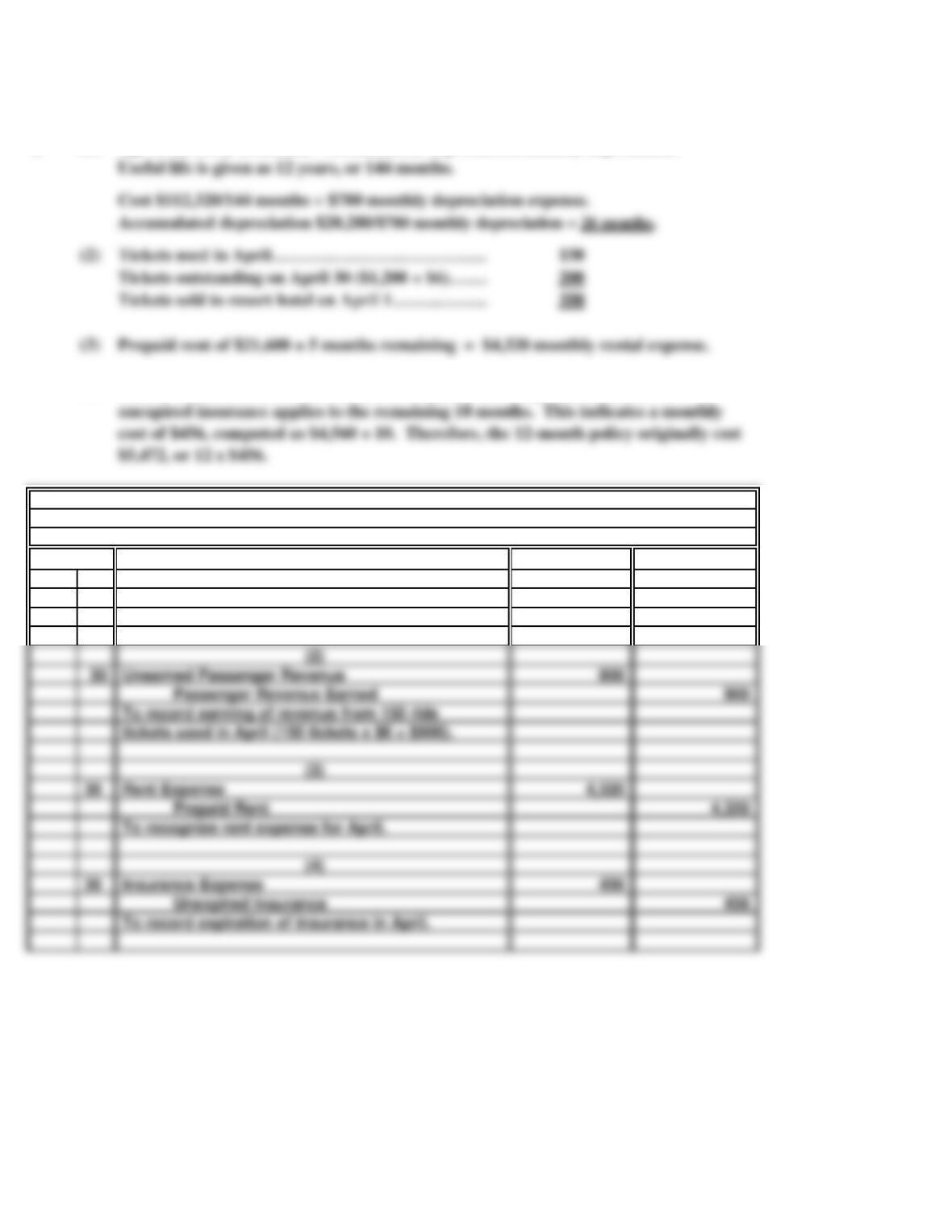

a. (1)

(4)

Apr. 30 780

Accumulated Depreciation: Ferry 780

Passenger Revenue Earned 900

Prepaid Rent 4,320

To record expiration of insurance in April.

Unearned Passenger Revenue

To record earning of revenue from 150 ride

Insurance Expense

Rent Expense

To recognize rent expense for April.

tickets used in April (150 tickets x $6 = $900).

b.

(Adjusting Entries)

(1)

Current Yr.

PROBLEM 4.3B

RIVER RAT

Age of the ferry in months = accumulated depreciation/monthly depreciation.

General Journal

Since 2 months of the 12-month life of the policy have expired, the $4,560 of

Depreciation Expense: Ferry

To record April depreciation expense on ferry.

(3)

Useful life is given as 12 years, or 144 months.

Cost $112,320/144 months = $780 monthly depreciation expense.

Accumulated depreciation $20,280/$780 monthly depreciation = 26 months.