CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–17 (FIN MAN); Ex. 4–17 (MAN)

The selling and administrative expenses should not be allocated on the basis of relative

sales dollars. The two product lines have very different attributes. The commercial

product is relatively inexpensive to sell, while the home product has a number of

additional costs associated with it. As a result, allocating selling and administrative

expenses using sales volumes would allocate too much selling and administrative

Ex. 18–18 (FIN MAN); Ex. 4–18 (MAN)

a. Sales order processing activities:

Number of

Sales Orders

×

Activity

Rate

=

Activity

Cost

Generators ………………………………………….

3,000

×

$65

$195,000

Air compressors …………………………..

4,000

×

65

260,000

Total ………………………………………………………………………………………………..

$455,000

Post-sale customer service activities:

Number of

Service Requests

Air compressors …………………………..

×

Activity

Activity

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–18 (FIN MAN); Ex. 4–18 (MAN) (Concluded)

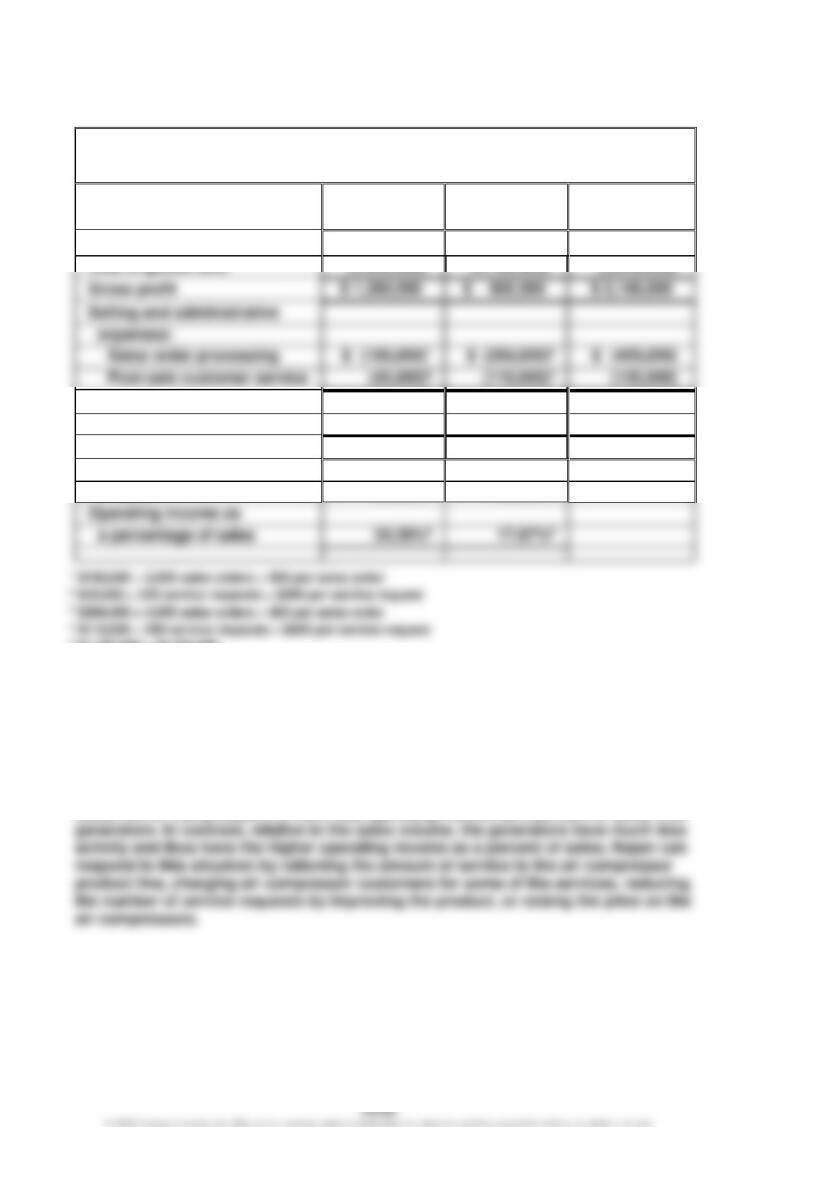

b.

Naper Inc.

Product Profitability Report

For the Year Ended December 31

Generators

Air

Compressors

Total

Revenues

$ 4,200,000

$ 3,000,000

$ 7,200,000

Cost of goods sold

Gross profit

$ 1,260,000

$ 2,160,000

Total selling and

administrative expenses

$ (240,000)

$ (370,000)

$ (610,000)

Operating income

$ 1,020,000

$ 530,000

$ 1,550,000

Gross profit as a percentage

of sales

30.00%5

30.00%7

5 $1,260,000 ÷ $4,200,000

6 $1,020,000 ÷ $4,200,000

7 $900,000 ÷ $3,000,000

8 $530,000 ÷ $3,000,000

c. The complete product profitability report provides much greater insight than did the

original report. The air compressors have the lower operating income to sales

percentage because the product is a heavy user of Naper’s sales and service

activities. The air compressors are ordered in small quantities (hence a high number

of sales orders) and have a high amount of post-sale service. All of these factors

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–19 (FIN MAN); Ex. 4–19 (MAN)

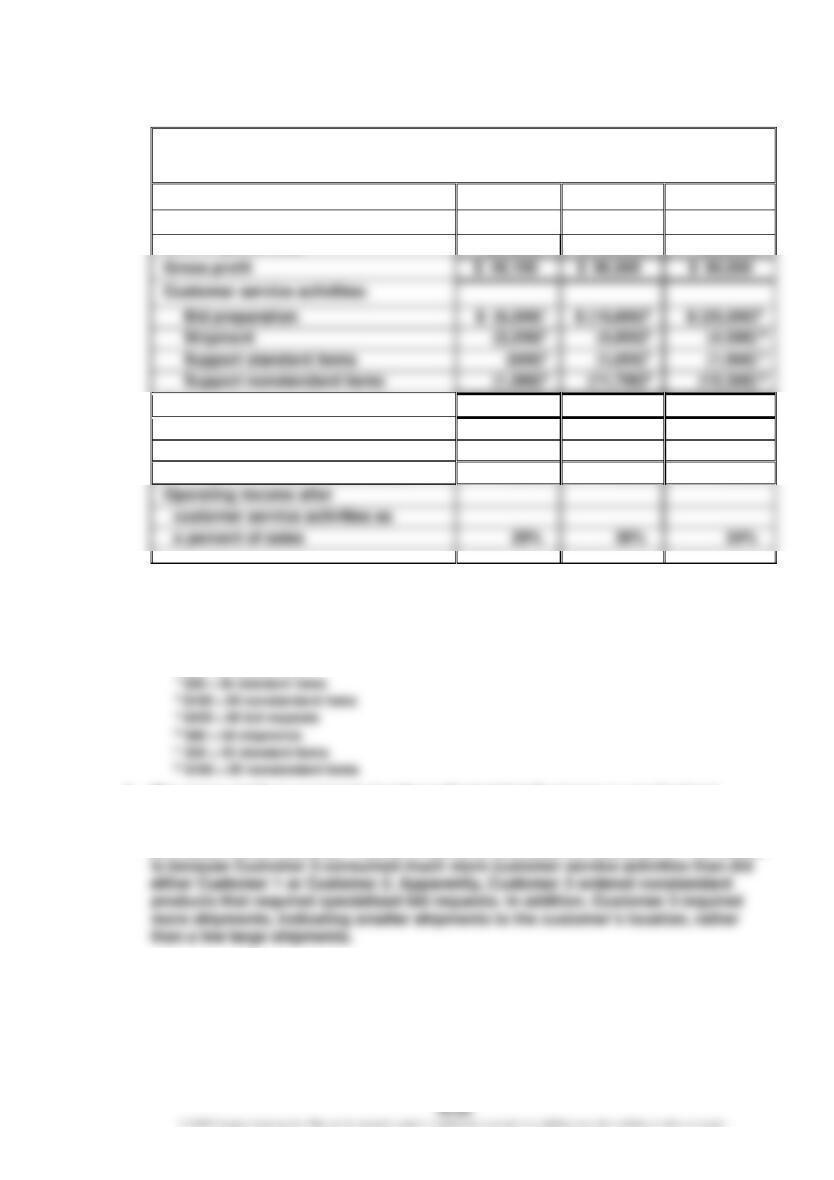

a.

Metroid Electric

Customer Profitability Report

For the Year Ended December 31, 20Y8

Customer 1

Customer 2

Customer 3

Revenue

$130,000

$ 210,000

$180,000

Gross profit

Cost of goods sold

(81,900)

(113,400)

(90,000)

Total customer service activities

$ (10,230)

$ (34,500)

$ (46,560)

Operating income after

customer service activities

$ 37,870

$ 62,100

$ 43,440

Gross profit as a percent of sales

37%

46%

50%

Operating income after

customer service activities as

1 $420 × 15 bid requests

2 $90 × 25 shipments

3 $30 × 20 standard items

4 $180 × 6 nonstandard items

5 $420 × 40 bid requests

6 $90 × 55 shipments

b. The gross profit as a percent of sales indicated that Customer 1 was the least

profitable, while Customer 3 was the most profitable. After deducting the activity

costs associated with customer service activities, Customer 3 became the least

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–20 (FIN MAN); Ex. 4–20 (MAN)

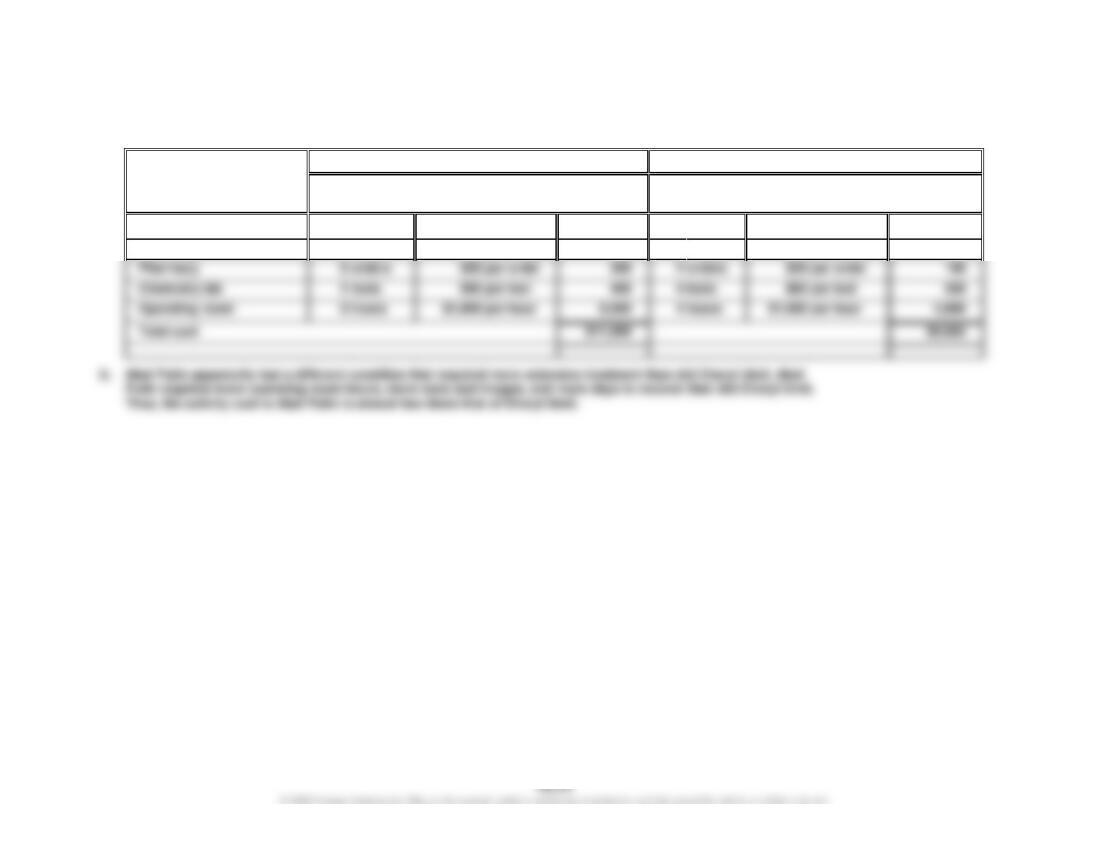

a.

Activity

Abel Putin

Cheryl Umit

Activity

Usage

×

Activity

Rate

=

Activity

Cost

Activity

Usage

×

Activity

Rate

=

Activity

Cost

Room and meals

6

days

$240

per day

$ 1,440

4

days

$240

per day

$ 960

Radiology

4

images

$215

per image

860

3

images

$215

per image

645

Pharmacy

6

orders

per order

300

2

orders

per order

100

Chemistry lab

5

tests

per test

400

4

tests

per test

320

Operating room

8

hours

per hour

4

hours

per hour

Total cost

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Ex. 18–21 (FIN MAN); Ex. 4–21 (MAN)

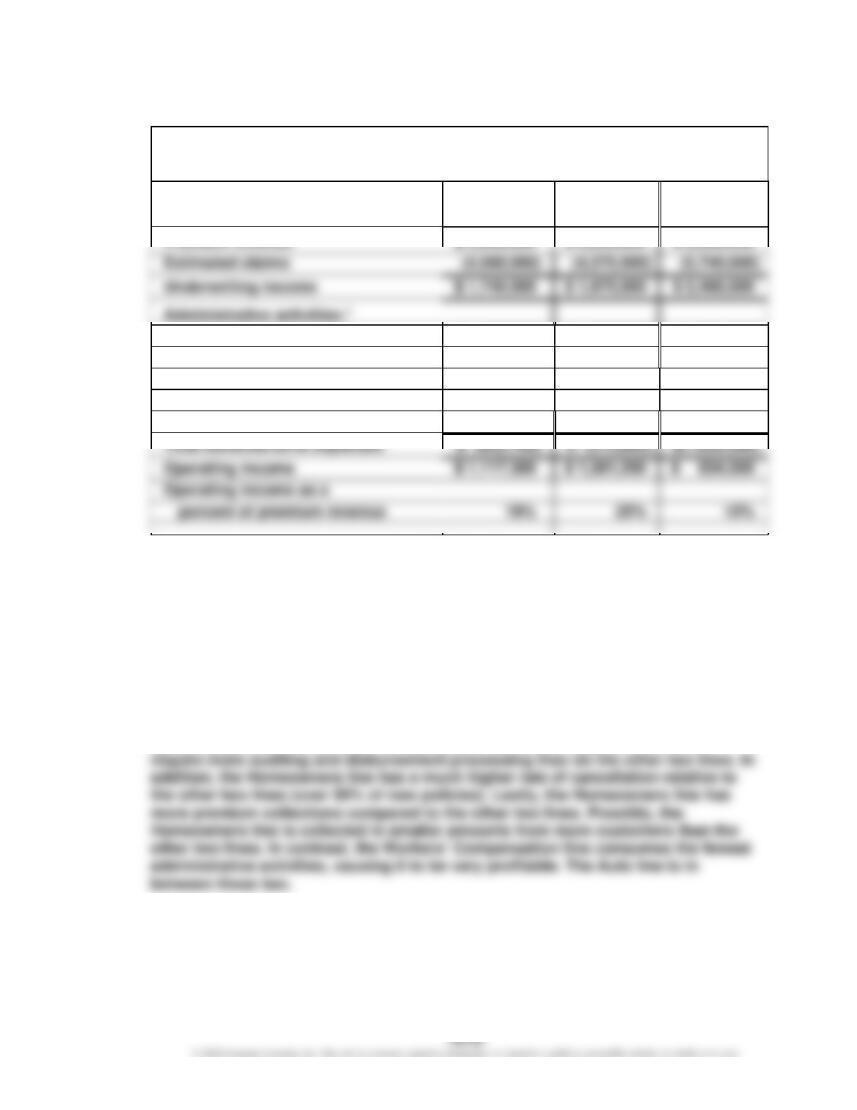

a.

Bounce Back Insurance Company

Product Profitability Report

For the Year Ended December 31

Auto

Workers’

Comp.

Homeowners

New policy processing

$ (146,300)

$ (154,000)

$ (451,000)

Cancellation processing

(88,200)

(54,000)

(396,000)

Claim audits

(128,700)

(36,300)

(313,500)

Claim disbursements processing

(47,000)

(22,000)

(85,000)

Premium collection processing

(212,500)

(47,500)

(380,000)

* The activity costs are determined by multiplying the activity rate by the activity-base usage quantity.

For example, the administrative activity costs for the Auto line are as follows:

$146,300 = 1,330 new policies × $110 per new policy

$88,200 = 490 cancellations × $180 per cancellation

$128,700 = 390 audits × $330 per claim audit

$47,000 = 470 disbursements × $100 per disbursement

$212,500 = 8,500 premiums collected × $25 per premium collected

All three insurance lines have the same percentage of underwriting income to

premium revenue (30%). The differences among the insurance lines are in the way

they consume administrative activities. For example, the Homeowners insurance

line has the least profitability due to its high use of administrative activities.

Specifically, the Homeowners line has smaller and more frequent claims that

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

PROBLEMS

Prob. 18–1A (FIN MAN); Prob. 4–1A (MAN)

1.

a.

Direct labor overhead rate:

$239,200

1,840 direct labor hours

=

$130 per direct labor hour

2.

Automobile

Bumpers

Valve

Covers

Wheels

a.

Direct labor hours:

Stamping Department ……………………..

590 dlh

310 dlh

350 dlh

Plating Department ………………………….

195

200

195

× Direct labor overhead rate …………….

$130 per dlh

b.

Machine hours:

Stamping Department ……………………..

810 mh

570 mh

620 mh

Plating Department ………………………….

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

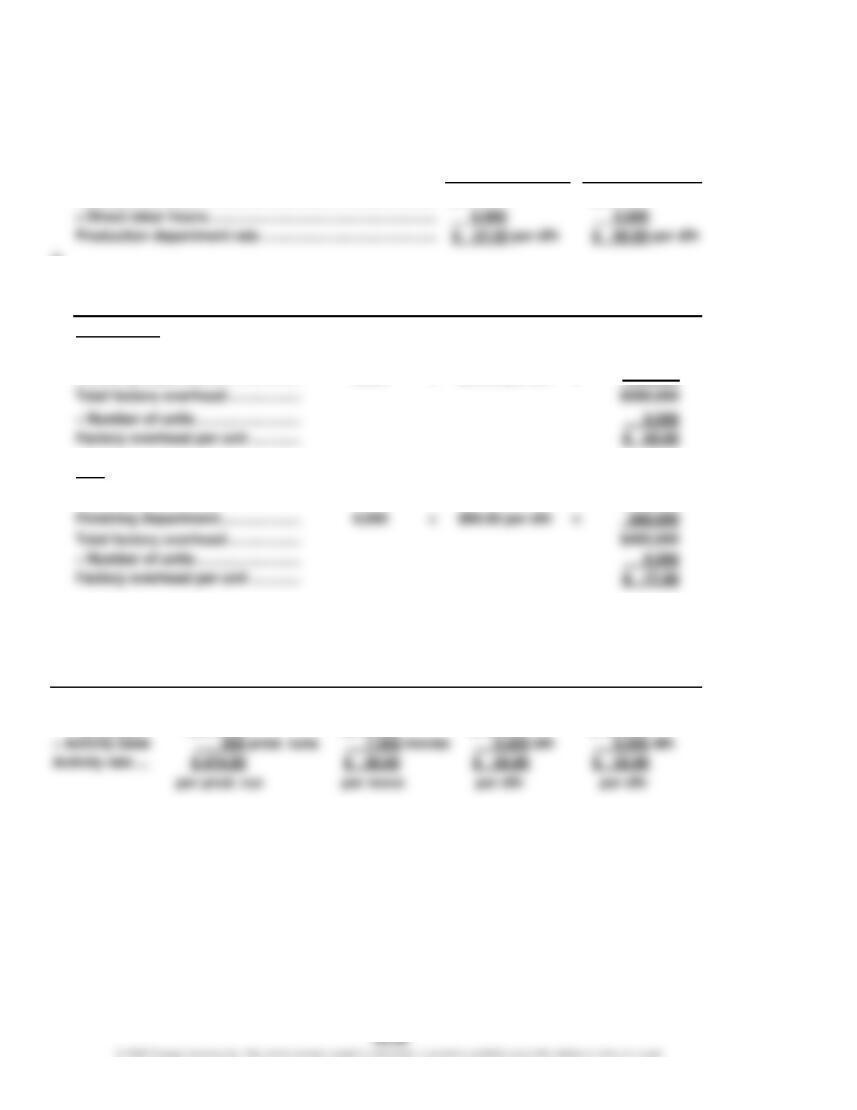

Prob. 18–2A (FIN MAN); Prob. 4–2A (MAN)

1.

Stamping

Dept.

Plating

Dept.

Production department factory

overhead totals …………………………………………………….

$120,000

$104,000

2.

Automobile bumpers

Stamping Department ………………..

590 dir. labor hrs. × $96 per dlh =

$ 56,640

Plating Department ……………………

1,150 dir. mach. hrs. × $40 per dmh =

46,000

Total factory overhead for bumpers ……………………………………………………..

$ 102,640

Valve covers

Plating Department ……………………

30,000

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

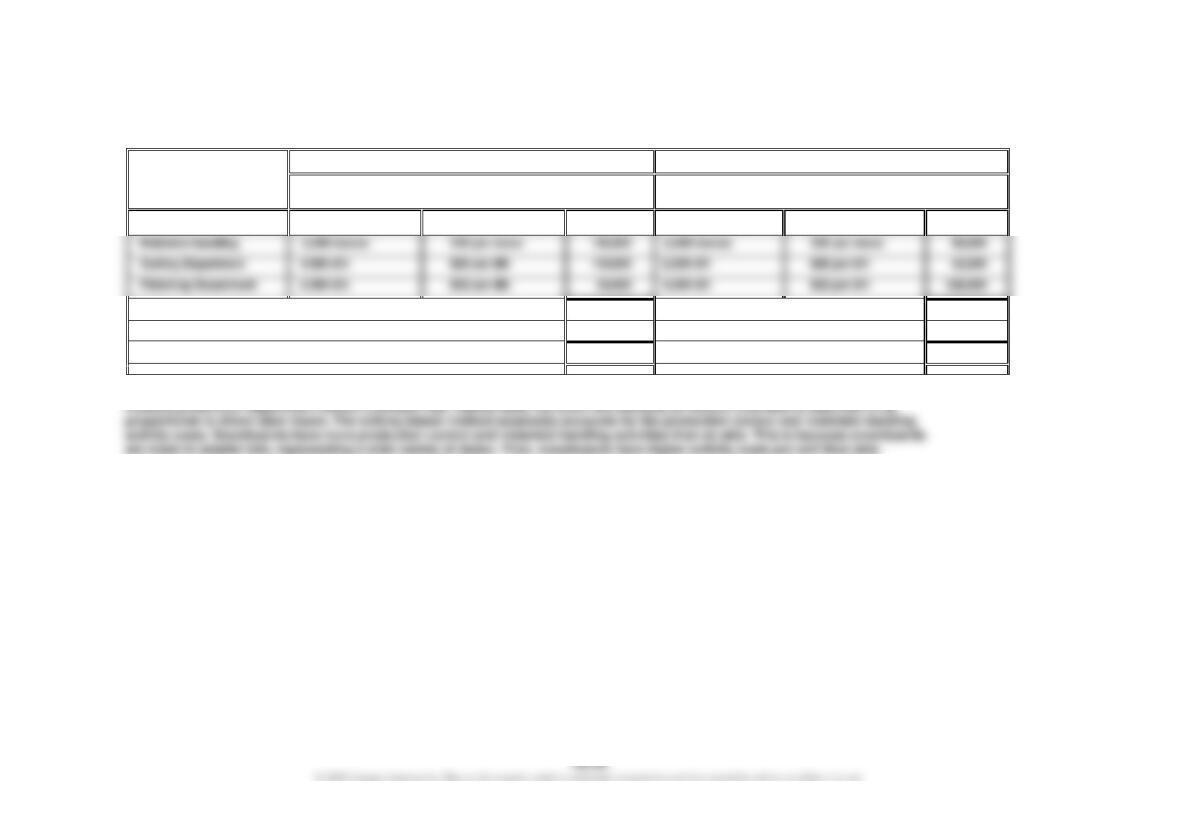

Prob. 18–3A (FIN MAN); Prob. 4–3A (MAN)

1.

Production department rates:

Cutting

Department

Finishing

Department

÷ Direct labor hours …………………………………………………..

Production department rate ………………………………………

Factory overhead ………………………………………………………

$315,000

$540,000

2.

Direct

Labor Hours

×

Production

Department

Rate

=

Factory

Overhead

Snowboards:

Cutting Department ……………………

4,000

×

$52.50 per dlh

=

$210,000

Factory overhead per unit ………….

Finishing Department …………………

2,000

×

$90.00 per dlh

=

180,000

Skis:

Cutting Department ……………………

2,000

×

$52.50 per dlh

=

$105,000

Total factory overhead ……………….

$465,000

÷ Number of units ………………………

3.

Activity-based rates:

Production

Control

Materials

Handling

Cutting

Department

Finishing

Department

Factory

overhead ..

$237,000

$270,000

$156,000

$192,000

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

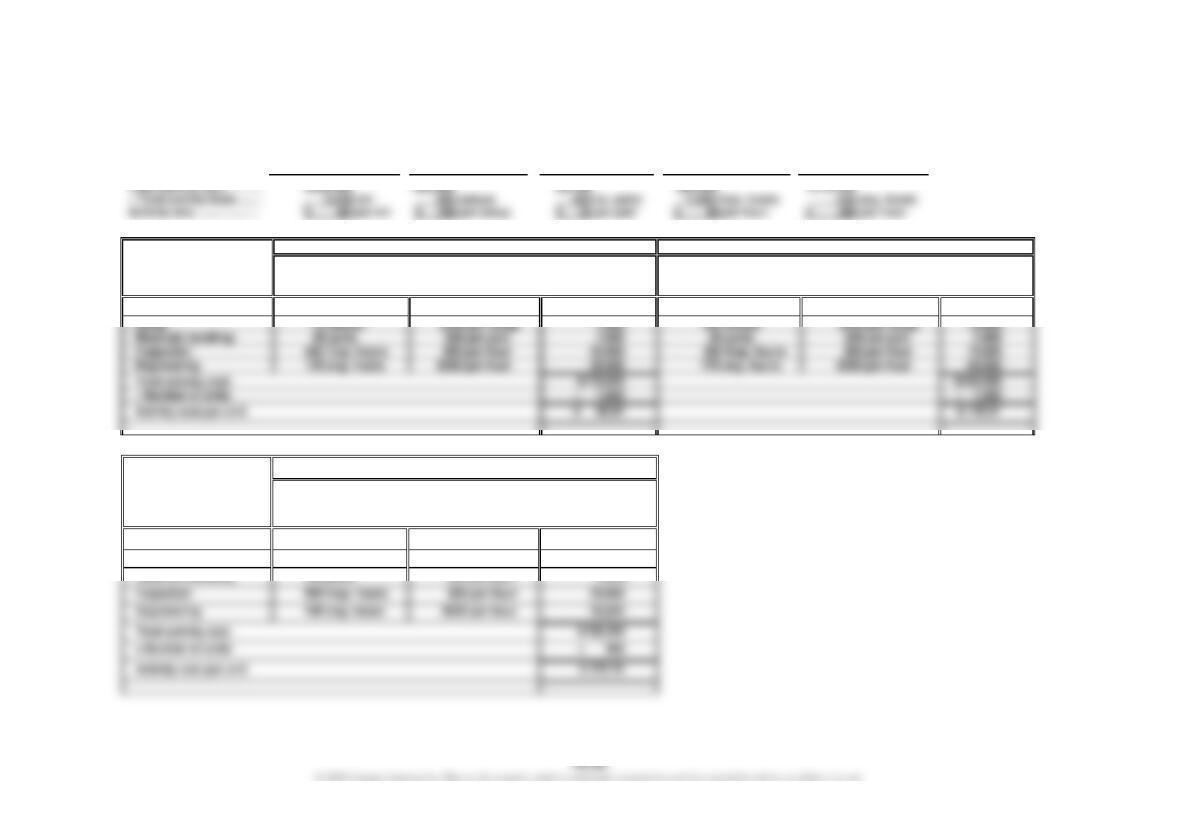

Prob. 18-3A (FIN MAN); Prob. 4-3A (MAN) (Concluded)

4.

Activity

Snowboards

Skis

Activity

Usage

×

Activity

Rate

=

Activity

Cost

Activity

Usage

×

Activity

Rate

=

Activity

Cost

Production control

430 prod, runs

$474 per prod, run

$203,820

70 prod, runs

$474 per prod, run

$ 33,180

Total

$551,820

$303,180

÷ Number of units

÷ 6,000

÷ 6,000

Activity cost per unit

$ 91.97

$ 50.53

5. The activity-based overhead allocation reveals that snowboards consume more factory overhead on a per-unit basis than do skis. The

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Prob. 18-4A (FIN MAN); Prob. 4-4A (MAN)

1.

Production

Setup

Materials

Handling

Inspection

Engineering

$55,000

2.

Activity

Alpha

Beta

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Production

1,440 mh

$80 per mh

$115,200

1,080 mh

$80 per mh

$ 86,400

Setup

165 setups

$30 per part

Inspection

20,000

300 insp. hours

Engineering

35,000

$280 per hour

$179,650

$169,300

Activity

Omega

Activity-

Base

Usage

×

Activity

Rate

=

Activity

Cost

Production

720

mh

$80

per mh

$ 57,600

Setup

310

setups

$100

per setup

31,000

Inspection

500

insp. hours

per hour

25,000

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Prob. 18–4A (FIN MAN); Prob. 4–4A (MAN) (Concluded)

3. The unit costs are different even though each product requires 0.8 machine hour

Prob. 18–5A (FIN MAN); Prob. 4–5A (MAN)

1.

Customer

Service

Project

Bidding

Engineering

Support

Activity cost …………………………

$31,500

$74,000

$120,750

2.

Gough Industries

Customer service …………………

36

sr

×

$175

per sr

=

$ 6,300

Project bidding …………………….

50

bids

×

$400

per bid

=

20,000

Engineering support …………….

18

dc

×

$750

per dc

=

13,500

Total nonmanufacturing activity costs …………………………..…………………….

$ 39,800

Breen Inc.

Customer service …………………

28

sr

×

$175

per sr

=

$ 4,900

Project bidding …………………….

40

bids

×

$400

per bid

=

16,000

Engineering support …………….

35

dc

×

$750

per dc

=

26,250

Total nonmanufacturing activity costs …………………………..…………………….

$ 47,150

The Martin Group

Engineering support …………….

×

$750

per dc

=

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

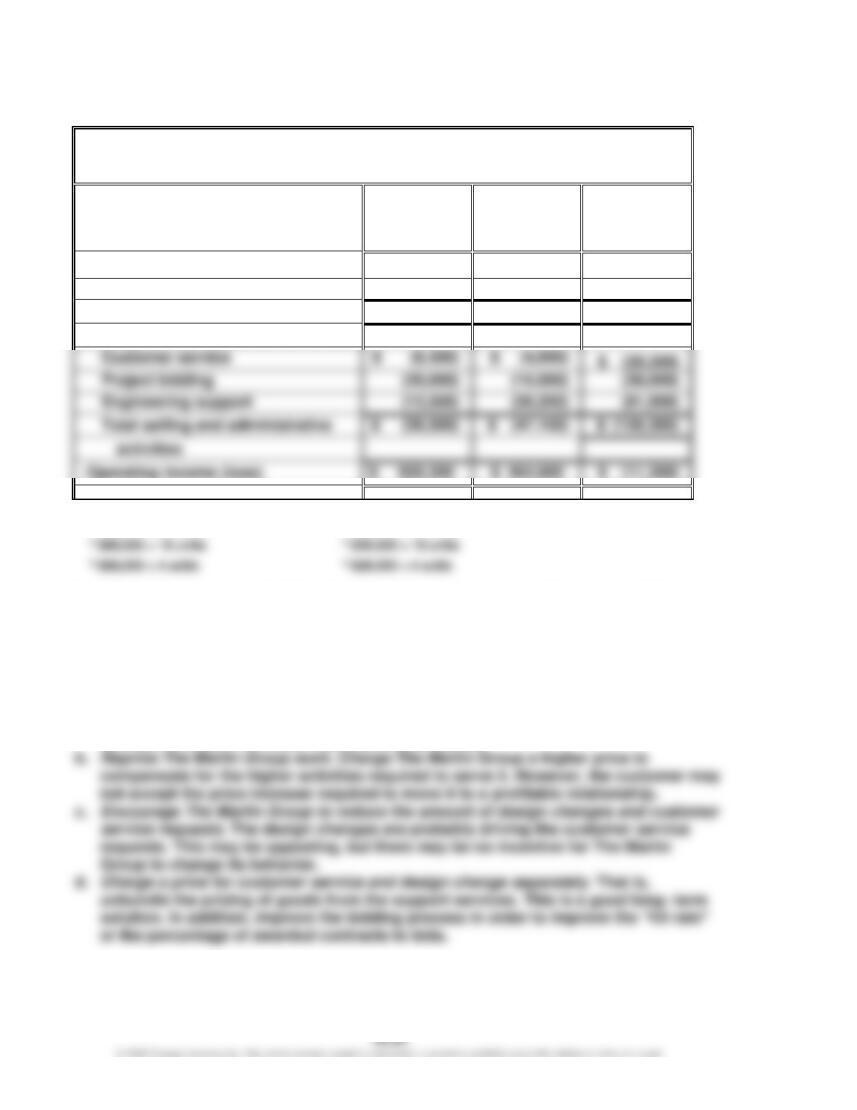

Prob. 18–5A (FIN MAN); Prob. 4–5A (MAN) (Concluded)

3.

Arctic Air Inc.

Customer Profitability Report

For the Year Ended December 31

Gough

Industries

Breen Inc.

The

Martin Group

Revenues

$1,800,0001

$ 960,0002

$ 240,0003

Cost of goods sold

(840,000)4

(448,000)5

(112,000)6

Gross profit

$ 960,000

$ 512,000

$ 128,000

Selling and administrative activities:

1 $60,000 × 30 units

4 $28,000 × 30 units

4. The Martin Group is unprofitable, while the other two customers have acceptable

margins. This is because The Martin Group requires many customer service, project

bidding, and design change activities. For example, The Martin Group awards

contracts on only 4.2% of the bid efforts (4 contracts ÷ 95 bids); it requests a large

amount of service; and it requires extensive design change effort. The company’s

options include:

a. Stop bidding The Martin Group projects. This does not necessarily mean that all

the costs can be avoided. The costs only will be eliminated if the reduced

activity translates into lower headcount (dismissals).

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Prob. 18–6A (FIN MAN); Prob. 4–6A (MAN)

1.

Activity

Activity Cost

÷

Activity Base

=

Activity Rate

Scheduling and admitting ………

$ 432,000

÷

6,000

patients

=

$72

per patient

Housekeeping ………………………..

4,212,000

÷

27,000

pds*

=

$156

per pd

Nursing ………………………………….

÷

wcus*

=

$28

per wcu

* “pd” stands for patient day; “wcu” stands for weighted care unit

2.

Activity

Activity

Usage

×

Activity

Rate

=

Total Activity

Cost by

Procedure

Procedure A

Scheduling and admitting

280

patients

$72

per patient

$ 20,160

Housekeeping

1,680

pds

$156

per pd

262,080

Nursing

19,200

wcus

$28

per wcu

537,600

$819,840

Housekeeping

3,250

pds

$156

per pd

507,000

Housekeeping

4,800

pds

$156

per pd

748,800

CHAPTER 18 (FIN MAN); CHAPTER 4 (MAN) Activity-Based Costing

Prob. 18–6A (FIN MAN); Prob. 4–6A (MAN) (Concluded)

3.

Procedure A

Procedure B

Procedure C

Reimbursement (patient days ×

reimbursement rate)*

$ 682,080

$1,319,500

$ 1,948,800

* 1,680 patient days × $406 per patient day = $682,080

3,250 patient days × $406 per patient day = $1,319,500

4,800 patient days × $406 per patient day = $1,948,800

4. Procedure A requires more activity cost than is being reimbursed by the insurance

company. As a result, the hospital may wish to determine if the costs of providing