1. The end-of-period spreadsheet illustrates the flow of accounting information from the unadjusted

trial balance into the adjusted trial balance and into the financial statements. In doing so, the

spreadsheet illustrates the impact of the adjustments on the financial statements.

2. a. Current assets are composed of cash and other assets that may reasonably be expected

to be realized in cash or sold or used up, usually within one year or less, through the normal

3. Current liabilities are liabilities that will be due within a short time (usually one year or less) and

that are to be paid out of current assets. Liabilities that will not be due for a comparatively long

time (usually more than one year) are called long-term liabilities.

5. Closing entries are necessary at the end of an accounting period (1) to transfer the balances in

6. Adjusting entries bring the accounts up to date, while closing entries reduce the revenue, expense,

and dividends accounts to zero balances for use in recording transactions for the next accounting

p

eriod.

7. The purpose of the post-closing trial balance is to make sure that the ledger is in balance at the

b

eginning of the next period.

8. a. The financial statements are the most important output of the accounting cycle.

b. Yes, all companies have an accounting cycle that begins with analyzing and journalizing

transactions and ends with a post-closing trial balance. However, companies may differ in

how they implement the steps in the accounting cycle. For example, while most companies

9. The natural business year is the fiscal year that ends when business activities have reached the

lowest point in the annual operating cycle.

10. All the companies listed are general merchandisers whose busiest time of the year is during the

b

CHAPTER 4

COMPLETING THE ACCOUNTING CYCLE

DISCUSSION QUESTIONS

CHAPTER 4 Completing the Accounting Cycle

PE 4–1A

2. Income statement 6. Income statement

4. Balance sheet 8. Balance sheet

1. Balance sheet 5. Balance sheet

3. Income statement 7. Retained earnings statement

PE 4–2A

PE 4–2B

Grab Bag Delivery Services

Retained Earnings Statement

PRACTICE EXERCISES

Gemini Advertising Services

Retained Earnings Statement

CHAPTER 4 Completing the Accounting Cycle

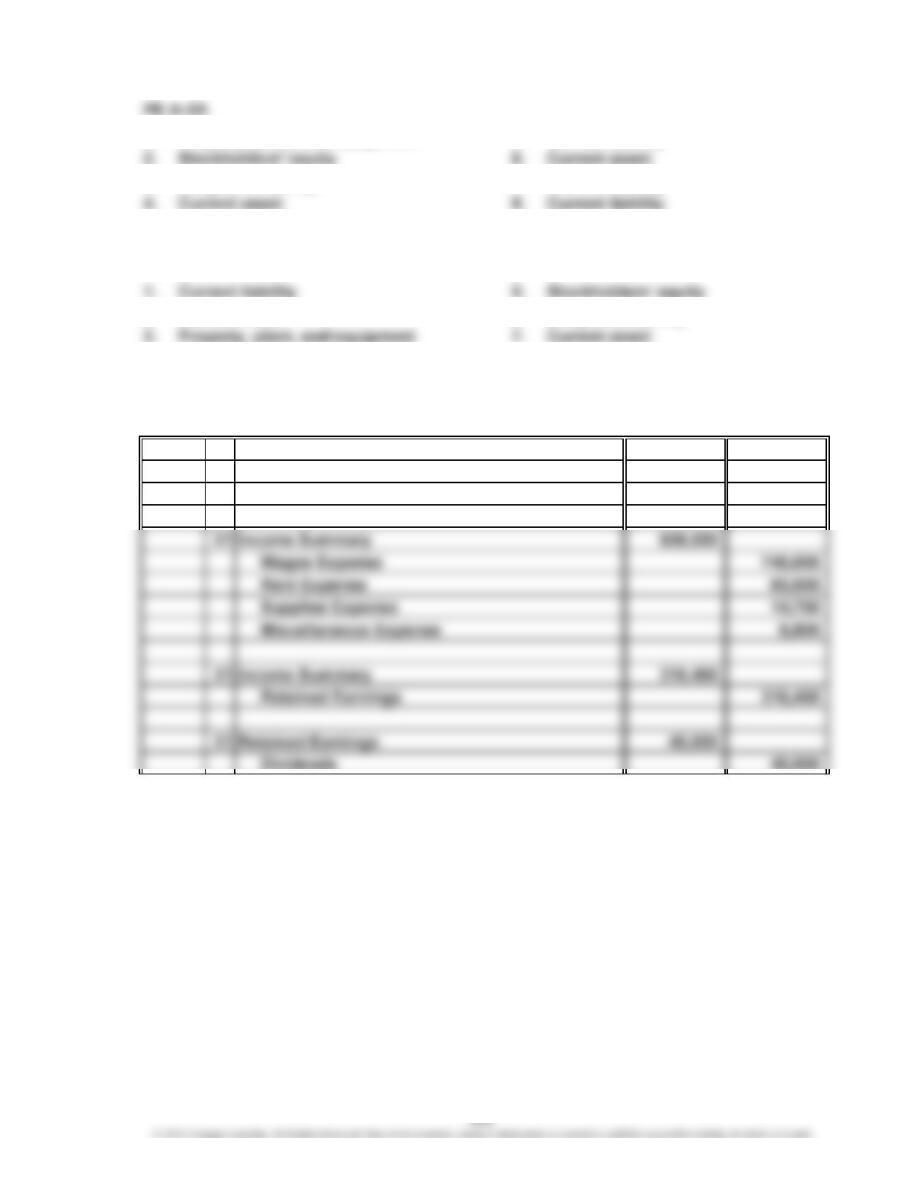

1. Property, plant, and equipment 5. Current liability

3. Long-term liability 7. Current liability

PE 4–3B

2. Current asset 6. Long-term liability

4. Current asset 8. Current liability

PE 4–4A

Oct. 31 Fees Earned 1,145,000

Income Summary 1,145,000

Closing Entries

CHAPTER 4 Completing the Accounting Cycle

PE 4–4B

Apr. 30 Fees Earned 356,500

Income Summary 356,500

30 Income Summary 363,600

Wages Expense 283,100

PE 4–5A

The following two steps are missing: (1) posting the transactions to the ledger

PE 4–5B

The following two steps are missing: (1) assembling and analyzing adjustment

PE 4–6A

a.

Closing Entries

2016

2015

CHAPTER 4 Completing the Accounting Cycle

PE 4–6B

a.

Current assets………………

2016

$1,586,250

2015

$1,210,000

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–1

2. Retained earnings statement: 4

3. Balance sheet: 1, 2, 3, 6, 7, 10

Ex. 4–2

EXERCISES

CHAPTER 4 Completing the Accounting Cycle

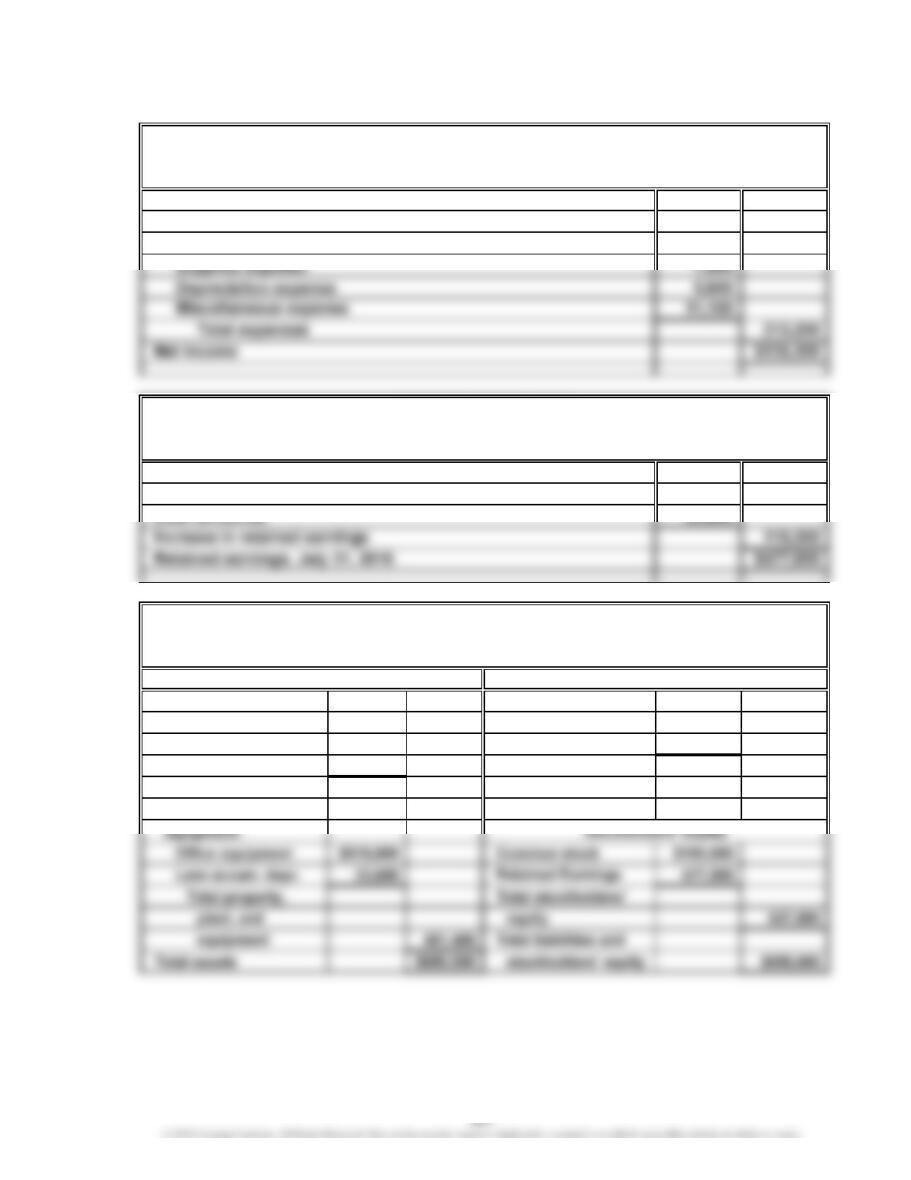

Ex. 4–3

Fees earned $348,500

Expenses:

Salary expense $189,000

Retained earnings, August 1, 2015 $366,700

Net income $135,300

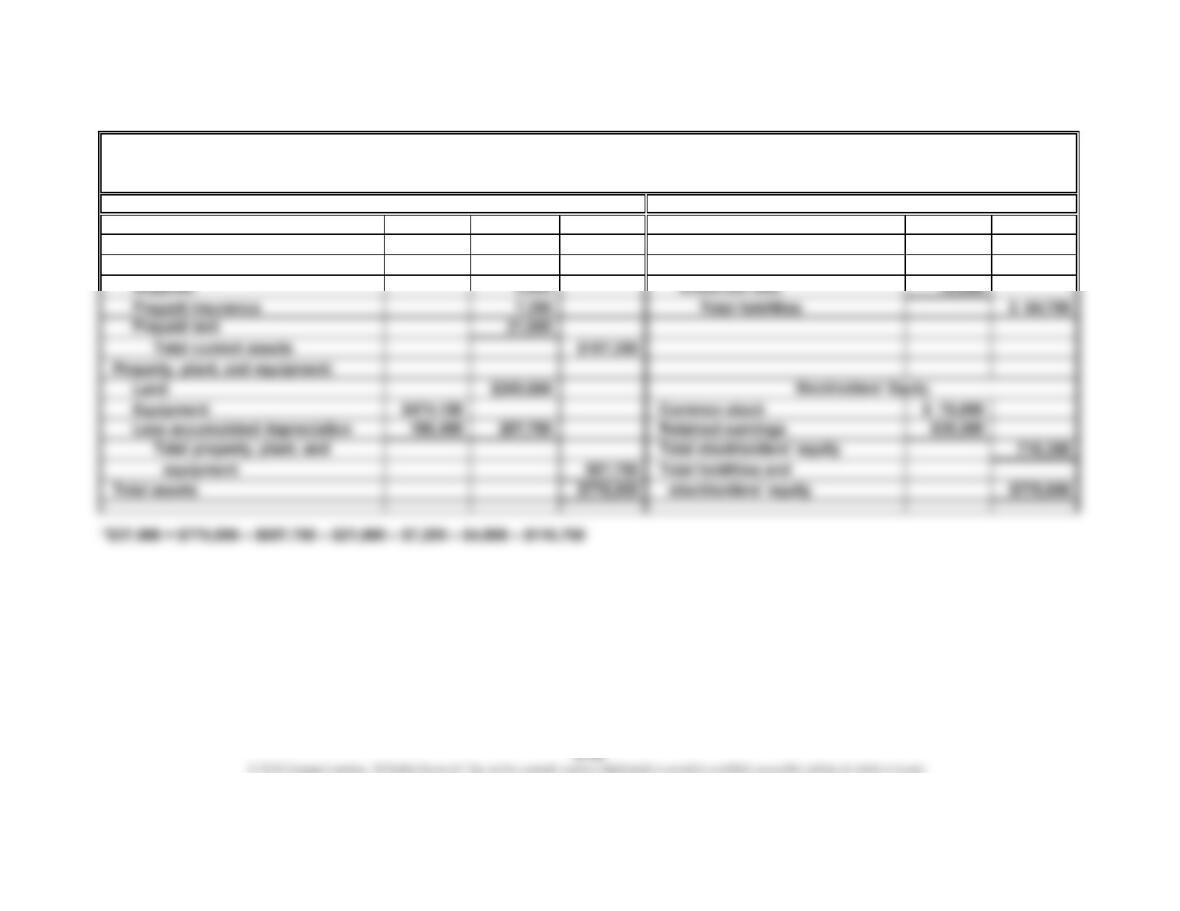

Current assets: Current liabilities:

Cash $ 58,000 Accounts payable $20,500

Accounts receivable 106,200 Salaries payable 2,500

Supplies 4,400 Total liabilities $ 23,000

Total current assets $168,600

Property, plant, and

BAMBOO CONSULTING

Income Statement

For the Year Ended July 31, 2016

BAMBOO CONSULTING

Retained Earnings Statement

For the Year Ended July 31, 2016

BAMBOO CONSULTING

Balance Sheet

July 31, 2016

Assets Liabilities

CHAPTER 4 Completing the Accounting Cycle

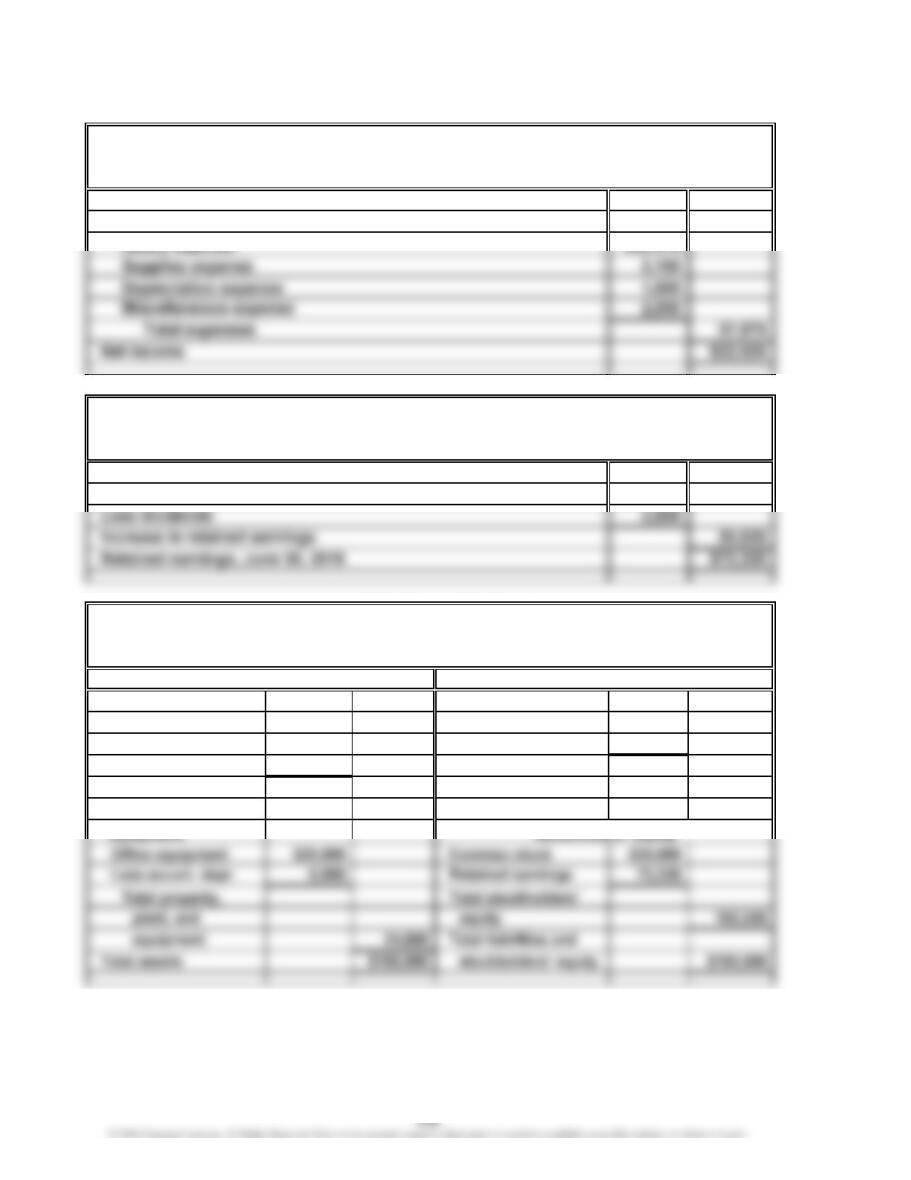

Ex. 4–4

Fees earned $60,000

Expenses:

Retained earnings, July 1, 2015 $ 52,200

Net income $22,025

Current assets: Current liabilities:

Cash $27,000 Accounts payable $3,300

Accounts receivable 53,500 Salaries payable 375

Supplies 900 Total liabilities $ 3,675

Total current assets $ 81,400

Property, plant, and

equipment:

ELLIPTICAL CONSULTING

Income Statement

For the Year Ended June 30, 2016

Stockholders’ Equity

ELLIPTICAL CONSULTING

Retained Earnings Statement

For the Year Ended June 30, 2016

ELLIPTICAL CONSULTING

Balance Sheet

June 30, 2016

Assets Liabilities

CHAPTER 4 Completing the Accounting Cycle

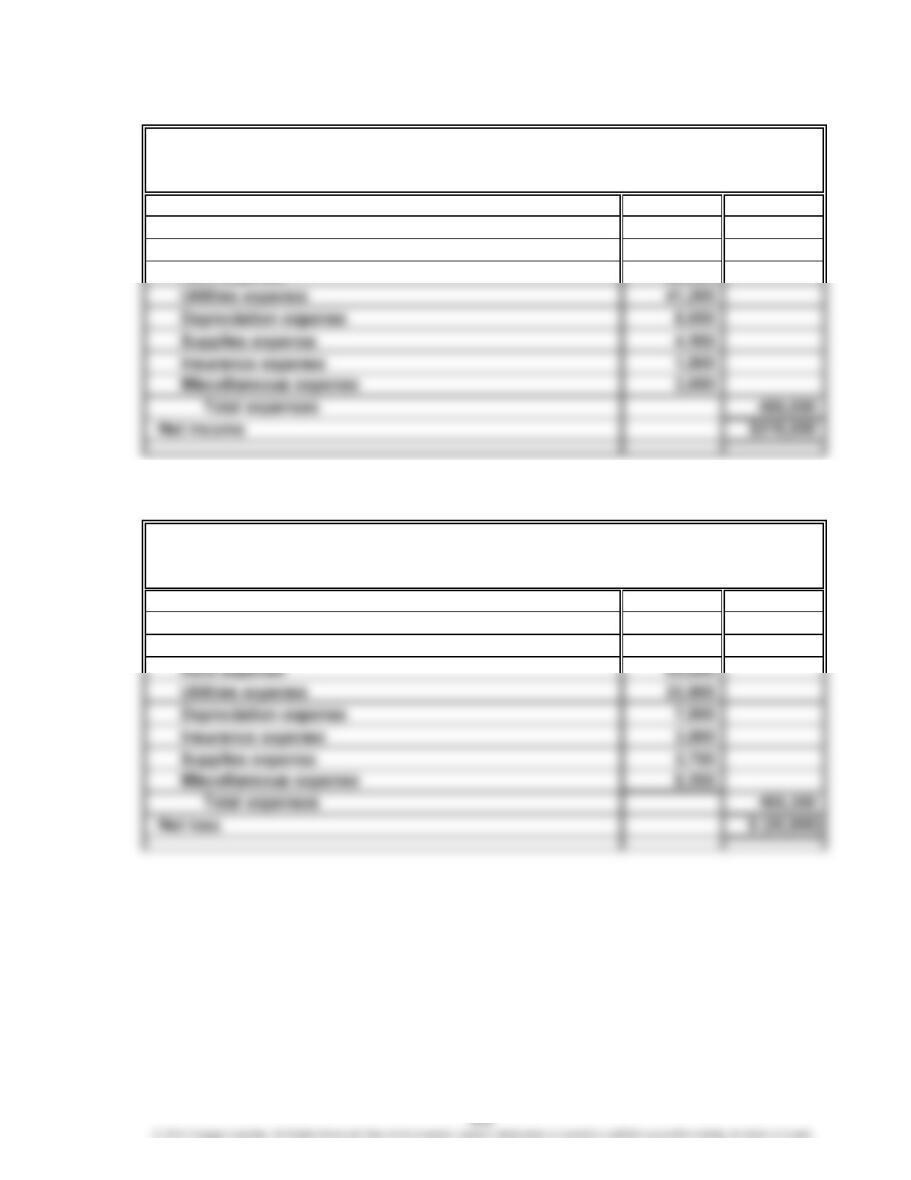

Ex. 4–5

Fees earned $674,000

Expenses:

Salaries expense $336,900

Rent expense 60,000

Ex. 4–6

Service revenue $448,400

Expenses:

Wages expense $360,000

Income Statement

For the Year Ended February 29, 2016

LASER MESSENGER SERVICE

Income Statement

For the Year Ended April 30, 2016

WHOLISTIC HEALTH SERVICES CO.

CHAPTER 4 Completing the Accounting Cycle

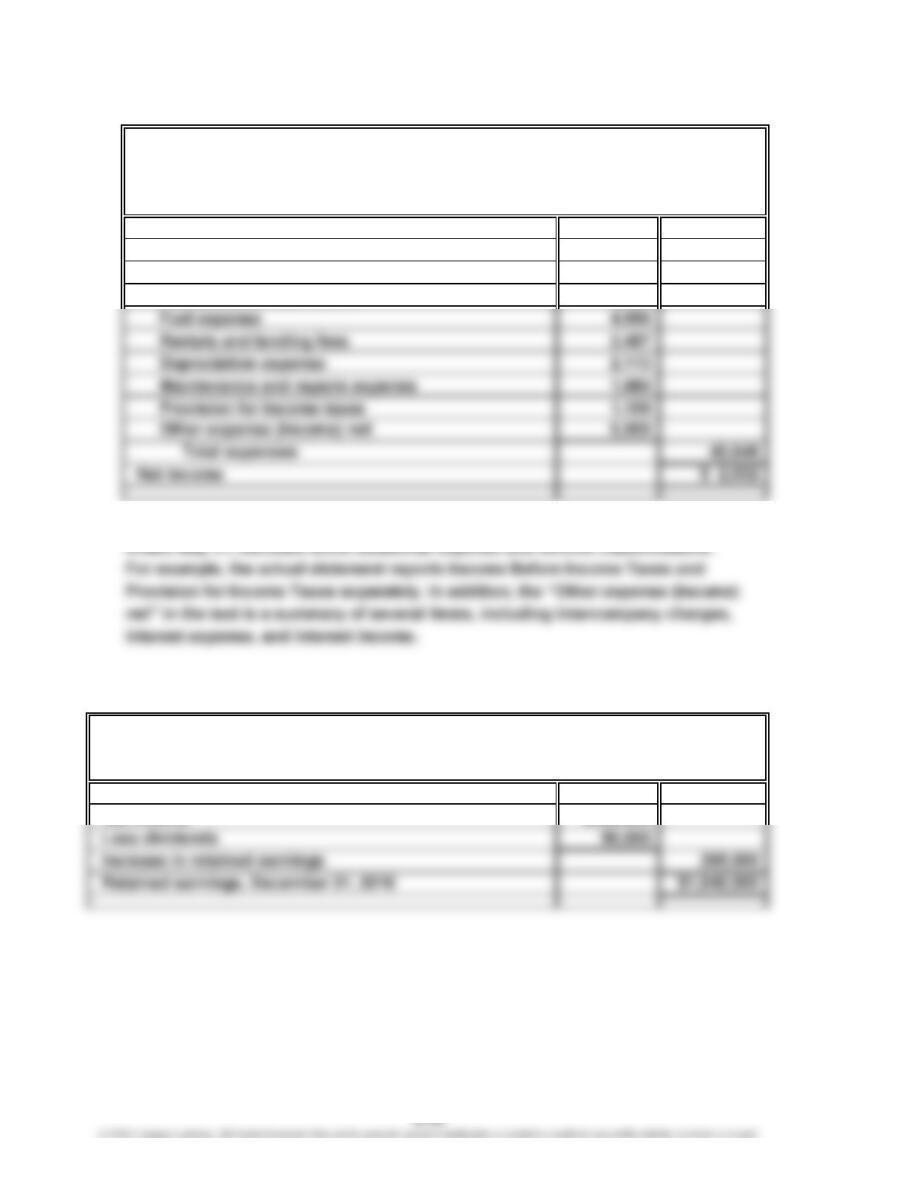

Ex. 4–7

a.

Revenues $42,680

Expenses:

Salaries and employee benefits $16,099

Purchased transportation 6,335

b. The income statements are very similar. The actual statement, which is for the year

Ex. 4–8

Retained earnings, January 1, 2016 $1,375,000

Net income $355,000

APEX SYSTEMS CO.

Retained Earnings Statement

For the Year Ended December 31, 2016

FEDEX CORPORATION

Income Statement

(in millions)

For the Year Ended May 31

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–9

Retained earnings, May 1, 2015 $475,500

Net loss $31,200

Ex. 4–10

a. Current asset: 1, 3, 5, 6

Ex. 4–11

Because current liabilities are usually due within one year, $15,000 ($1,250 × 12

RESTORATION ARTS

Retained Earnings Statement

For the Year Ended April 30, 2016

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–12

Current assets: Current liabilities:

Cash* $ 37,500 Accounts payable $37,700

Accounts receivable 116,750 Salaries payable 9,000

OPTIMUM WEIGHT LOSS CO.

Balance Sheet

November 30, 2016

Assets Liabilities

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–13

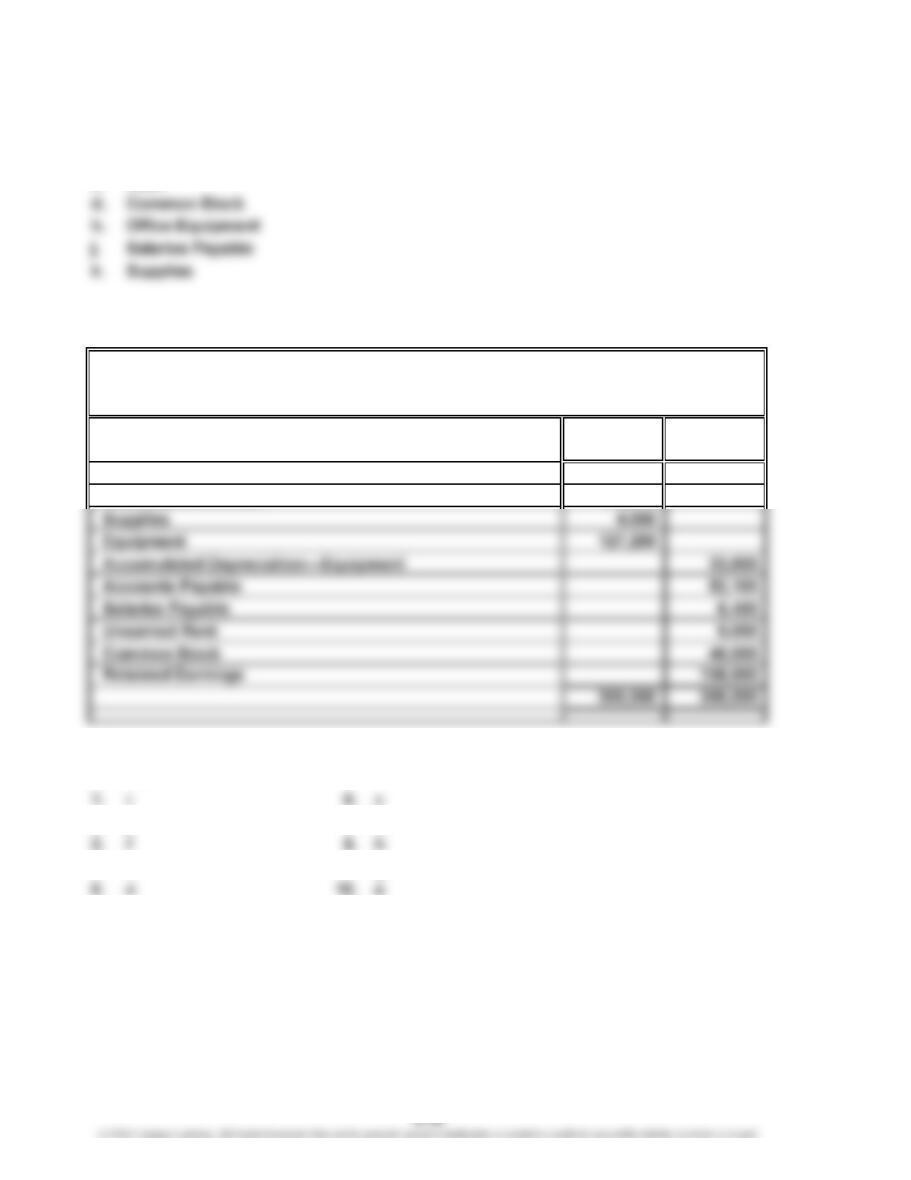

2. Accounts payable should be a current liability.

4. “Accumulated depreciation” should be deducted from the related fixed asset.

6. Accounts receivable should be a current asset.

8. Wages payable should be a current liability.

A corrected balance sheet would be as follows:

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–13 (Concluded)

Current assets: Current liabilities:

Cash $ 18,500 Accounts payable $31,300

Accounts receivable 41,400 Wages payable 6,500

LABYRINTH SERVICES CO.

Balance Sheet

August 31, 2016

Assets Liabilities

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–14

c. Depreciation Expense—Equipment

g. Fees Earned

j. Supplies Expense

Ex. 4–15

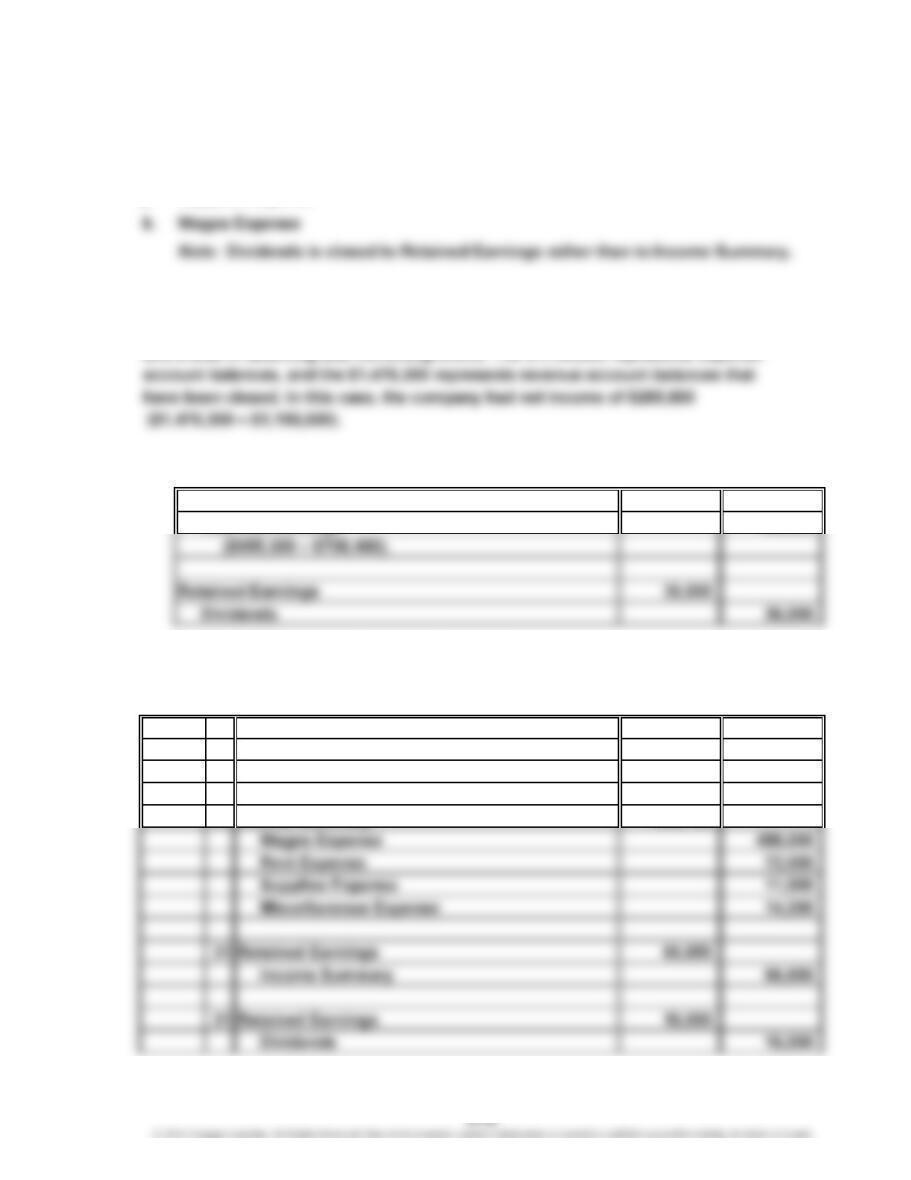

The income summary account is used to close the revenue and expense accounts,

and it aids in detecting and correcting errors. The $1,190,500 represents expense

Ex. 4–16

a. Income Summary 156,900

Retained Earnings 156,900

b. $1,559,900 ($1,439,000 + $156,900 – $36,000)

Ex. 4–17

Oct. 31 Fees Earned 519,300

Income Summary 519,300

31 Income Summary 586,150

Closing Entries

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–18

a. Accounts Payable

b. Accumulated Depreciation

c. Cash

Ex. 4–19

Debit Credit

Balances Balances

Cash 46,540

Accounts Receivable 122,260

Ex. 4–20

2. j 7. d

4. b 9. g

LA CASA SERVICES CO.

Post-Closing Trial Balance

March 31, 2016

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–21

a.

Current assets…………

…

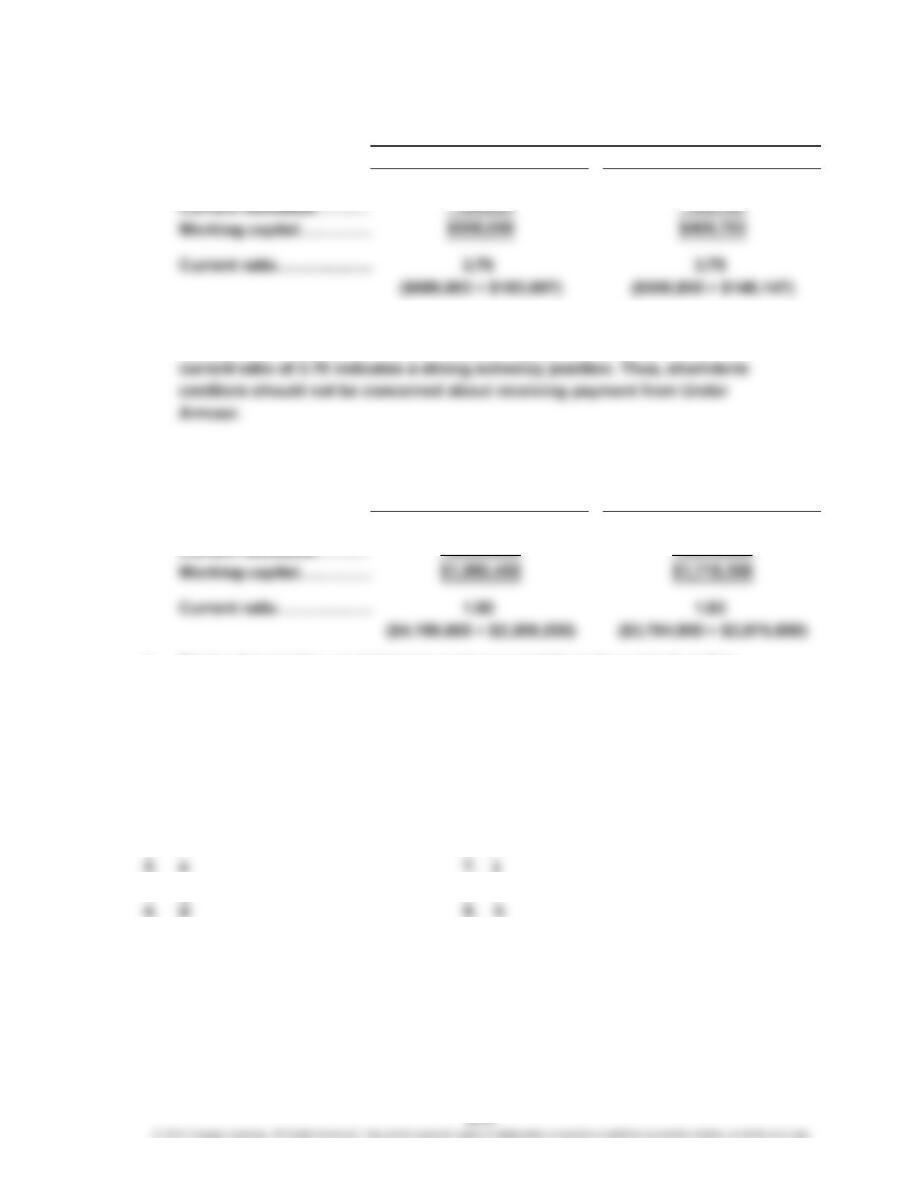

b. Under Armour’s working capital increased by $96,353 ($506,056 – $409,703)

during Year 2. The current ratio increased slightly to 3.76 in Year 2. A

Ex. 4–22

a.

Current assets…………

…

…

b. Starbucks’ working capital improved (increased) from Year 1 to Year 2 by

$271,300 ($1,990,400 – $1,719,100). Starbucks’ current ratio also improved

(increased) from 1.83 in Year 1 to 1.90 in Year 2. The improved working capital

and current ratio indicate that short-term creditors should not be concerned

about receiving payment from Starbucks.

Ex. 4–23

1. i 6. f

3. g 8. e

5. c 10. b

$558,850

149,147

December 31

Year 2 Year 1

Year 1Year 2

$689,663

183,607

2,209,200 2,075,800

$4,199,600 $3,794,900

…

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–24

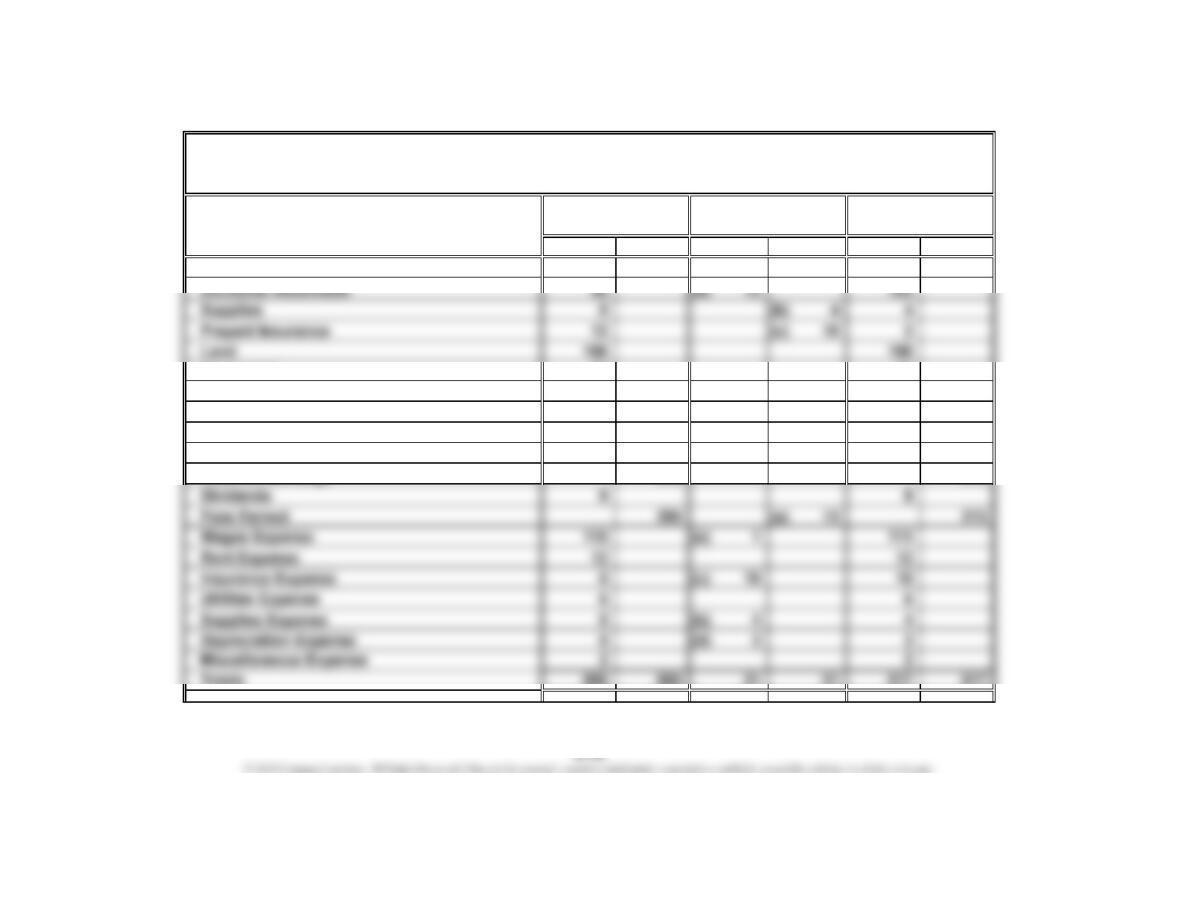

Account Title Debit Credit Debit Credit

Cash 12 12

Equipment 50 50

Accum. Depr.—Equipment 4 (d) 3 7

Accounts Payable 36 36

Wages Payable 0 (e) 1 1

Common Stock 50 50

Retained Earnings 210 210

ALERT SECURITY SERVICES CO.

End-of-Period Spreadsheet (Work Sheet)

For the Year Ended October 31, 2016

Unadjusted Adjusted

Debit Credit

Trial Balance Adjustments Trial Balance

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–25

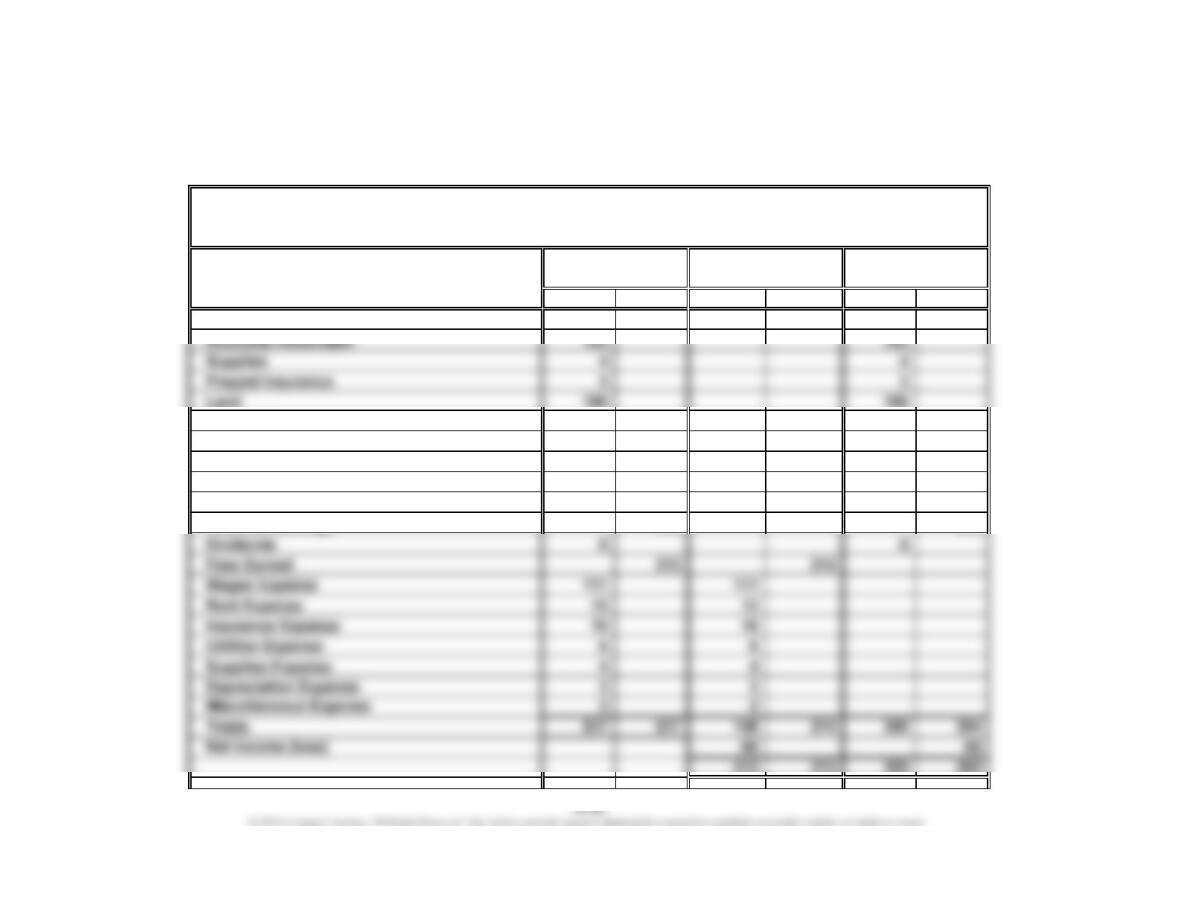

Account Title Debit Credit Debit Credit

Cash 12 12

Equipment 50 50

Accum. Depr.—Equipment 7 7

Accounts Payable 36 36

Wages Payable 1 1

Common Stock 50 50

Retained Earnings 210 210

Debit Credit

Trial Balance Statement Sheet

ALERT SECURITY SERVICES CO.

End-of-Period Spreadsheet (Work Sheet)

For the Year Ended October 31, 2016

Adjusted BalanceIncome

CHAPTER 4 Completing the Accounting Cycle

Ex. 4–26

Fees earned $213

Expenses:

Wages expense $111

Rent expense 12

ALERT SECURITY SERVICES CO.

Income Statement

For the Year Ended October 31, 2016