Chapter 4

4.1 The statement of cash flows is a useful document because it is the only

4.2 Cash includes cash and highly liquid short-term marketable securities, called

cash equivalents.

Operating activities include delivering or producing goods for sale and

4.3 The direct method shows cash collections from customers, interest and

dividends collected, other operating cash receipts, cash paid to suppliers and

4.4 The cash flow statement helps investors, creditors and other users determine

the following about a firm:

• Its ability to generate cash flows in the future

4.5 (a) I (g) F

(b) F (h) I

4.6 (a) O (g) O

(b) O (h) F

4.7 (a) L (f) H

(b) H (g) L

4.8 (a) Outflow, F (f) Outflow, F

(b) Inflow, I (g) Outflow, I

4.9 (a)

Beginning retained

earnings

+

Net income

–

Dividends

=

Ending retained

earnings

$3,600

+

$1,050

–

$200

=

$4,450

(b)

Dragoon Enterprises

Statement of Cash Flows

For Year Ending December 31, 2015

Cash flow from operating activities

Accounts payable

300

Accrued wages payable

(100)

Interest payable

(50)

Income taxes payable

150

Net cash provided by operating activities

1,010

Cash flows from investing activities

Purchase of plant and equipment

)

Sale of long-term investments

140

Net cash used for investing activities

)

Cash flows from financing activities

Increase in common stock

Increase in paid-in capital

330

Net cash used by financing activities

)

Increase in cash

Net income

Non-cash operating items:

Depreciation

100

Cash provided (used) by current assets and liabilities:

Inventory

110

4.10 (a) Net income – Change in retained earnings = Dividends

Firm A $75,000 – $70,000 = $ 5,000

Firm B $75,000 – $40,000 = $35,000

(b)

Firm A

Firm B

Cash flow from operating activities

Short-term debt

$

17,000

$

2,000

Long-term debt

20,000

(10,000

)

Dividends paid

(5,000

)

(35,000

)

Net cash flow from financing activities

$

32,000

($

43,000

)

Change in cash

$

0

$

10,000

Inflows

$

Operating activities

Short-term debt

17,000

46

Long-term debt

20,000

54

Outflows

Operating activities

12,000

32

Purchase of PP&E

20,000

54

70,000

61

Reduction of long-term debt

Dividends paid

5,000

14

35,000

30

37,000

100

115,000

100

Change in cash

0

10,000

Net income

$

75,000

$

75,000

Depreciation

10,000

30,000

Deferred taxes

18,000

Accounts receivable

)

)

Inventory

)

10,000

Accounts payable

)

)

Cash provided (used) by operations

12,000

)

$

Cash flow from investing activities

Purchase of plant, property and equipment

20,000

)

($

70,000

)

Cash flow from financing activities

Both firms reported net income of $75,000, but, in reality, they had an entirely

different operating performance, because Firm B had a strong positive operating

4.11

AddieMae, Inc.

Statement of Cash Flows

For Year Ended December 31, 2016

Cash flow from operating activities

Net income

$ 6,200

Depreciation

500

Cash provided by (used for) current assets and liabilities

Accounts receivable

(500

)

Inventory

)

Accounts payable

800

Income taxes payable

300

Cash flows from investing activities

Purchase of plant and equipment

(700

)

Purchase of long-term investments

(300

)

Net cash used by investing activities

(

$ 1,000

)

Cash flows from financing activities

Additions to long-term debt

200

Analysis

Inflows

$

%

Operating activities

500

15

AddieMae, Inc. generated far less cash from operating activities compared to net

income due primarily to growth in inventories, receivables. Accounts payable and

accrued expenses have also grown to support the increase in current assets. The

firm may be expanding as evidenced by the increase in capital assets.

The expansion is being supported by long-term debt and a significant sale of

common stock.

Outflows

$

%

Purchase of property and equipment

700

70

4.12

(a) Cash provided by operations in 2015 is considerably less than net income.

The major reason is the $288.2 million increase in accounts receivable. Inventory

also increased substantially ($159.4 million) but the growth in inventory was

(b)

2015

2014

Inflows

$

%

$

%

Operations

24,525

8.2

177,387

78.1

Investment activities

14,408

4.8

0

0

Short-term borrowings

125,248

19.9

Add. to long-term borrowings

135,249

299,430

100.0

227,064

100.0

Outflows

Add. to plant and equipment

94,176

21.2

Investment activities

Purchase of treasury stock

45,854

Dividends

49,290

Repay long-term borrowings

0

250,564

56.9

189,320

100.0

440,261

100.0

Change in cash

110,110

(213,197)

In 2014 Techno generated most of its cash (78%) internally through operations.

About 20% came from short-term borrowings, apparently to finance working

capital. As the result of a strong operating cash flow and a large cash account

balance ($291 million) Techno was able to expand plant and equipment while

4.13 What follows is a sample article. The article should include the following

key points: 1) cash flow from operations is different from net income; 2) a brief

explanation of why the two measurements differ; and 3) cash is what is needed to

stay afloat. A good basis for the article is the example of the “Nocash

Corporation” in Chapter 4.

To get through this patch, the company may have to borrow to cover the cash

shortage, which will require future cash for debt service. If the company doesn’t

turn things around, the problems will compound, leading to potential disaster.

4.14 There is no solution presented here as the students will be choosing a variety

of companies.

4.15 (a) Advantages of large cash balances are that:

• companies can survive economic recessions;

(b) Disadvantages of large cash balances are that:

• cash may be earning little or no return;

to invest in new growth and hire new employees.

(c) Students answers will vary depending on information located at the time they

do research. In 2014, firms with the largest cash and liquid balances were: Apple,

Microsoft, Google and Verizon. Other notable information about Apple at this time

Case

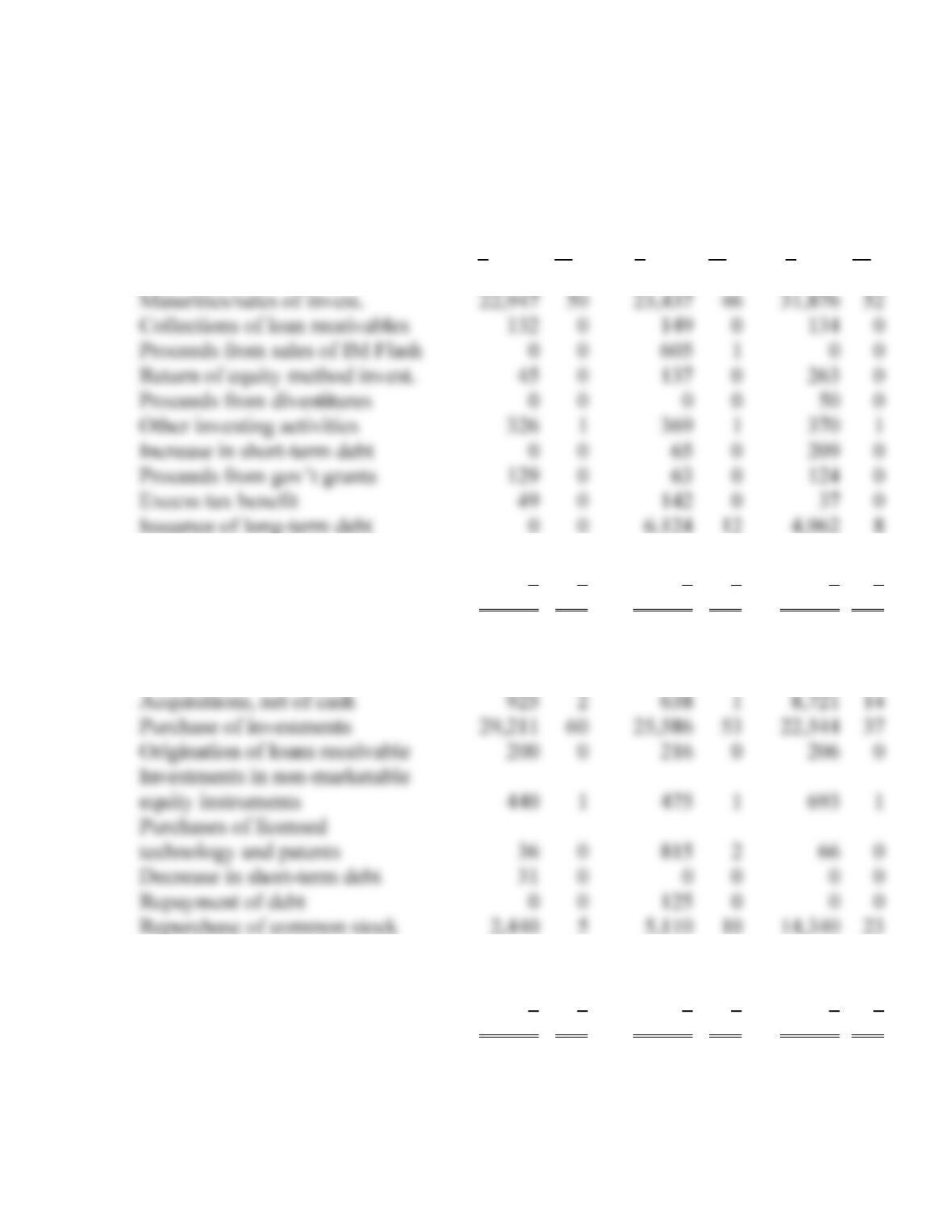

4.1 (a)

Intel

Statement of Cash Flows Summary Analysis

(dollars in millions)

2013

2012

2011

Inflows:

$

%

$

%

$

%

Operations

20,776

45

18,884

36

20,963

35

Proceeds from sales of shares

1,588

4

2,111

4

2,045

4

Effect of exchange rate

0

0

0

0

5

0

Total Inflows

45,992

100

52,086

100

61,038

100

Outflows:

Additions to PPE

10,711

22

11,027

23

10,764

18

Acquisitions, net of cash

925

2

638

1

8,721

Purchase of investments

29,211

25,586

22,544

Origination of loans receivable

200

0

216

0

0

440

1

475

1

1

technology and patents

0

815

2

66

0

Decrease in short-term debt

0

0

0

0

0

Repurchase of common stock

2,440

5

5,110

14,340

23

Payments of dividends

4,479

9

4,350

9

4,127

7

Other financing

314

1

328

1

10

0

Effect of exchange rate

9

0

3

0

0

0

Total Outflows

48,796

100

48,673

100

61,471

100

Change in cash

(2,804)

3,413

(433)

Maturities/sales of invest.

22,947

46

31,876

Collections of loan receivables

132

0

149

0

0

Proceeds from sales of IM Flash

0

0

1

0

0

Return of equity method invest.

0

137

0

0

Proceeds from divestitures

0

0

0

0

50

0

Other investing activities

326

1

1

1

Increase in short-term debt

0

0

0

0

Proceeds from gov’t grants

0

0

0

Excess tax benefit

0

142

0

0

Issuance of long-term debt

0

0

12

8

The relatively low percentage of cash flow from operations is explained by the

purchases and ultimate maturities of investments. In all three years between 82%

and 95% of cash has been generated from operations or maturities of investments.

Investments have most likely been purchased from cash that was originally

generated from operations.

The majority of cash is used to purchase available-for-sale investments and trading

assets. Given Intel’s significant generation of CFO each year, it is appropriate to

invest excess cash so a return is received until the firm has need for the excess

funds. It is noteworthy that the dollar amounts have increased over the past three

years. Intel continues to invest yearly in new property, plant and equipment which

is an expected expenditure for this type of firm since Intel should be updating and

replacing plant and equipment as new products are developed. It is also good that

Intel is pursuing acquisitions to diversify into areas other than semiconductors with

the changing computing environment. In 2011 McAfee was acquired.