4

Fundamentals of Cost Analysis for Decision

Making

Solutions to Review Questions

4-1.

4-2.

4-3.

Strictly speaking, sunk costs can never be differential costs. However, sunk costs can

4-4.

Short-run decisions affect operations within one year (for example, the decision to

4-5.

The full cost of a product is the sum of all fixed and variable costs of manufacturing and

4-6.

4-7.

4-8.

The product life cycle covers the time from initial research and development to the time

4-9.

4-10.

Target cost is the target price minus some desired profit margin. Target price is a price

set by management based on customers’ perceived value for the product and the price

competitors charge. There are four steps to developing target prices and target costs:

1. Develop a product that satisfies the needs of potential customers.

4-11.

Predatory pricing is the practice of a setting a selling price at a low price with the intent

of driving competitors out of the market or of creating a barrier to entry for new

competitors.

4-12.

Dumping is the practice of exporting products to consumers in another country at an

4-13.

Price discrimination is the practice of selling identical goods or services to different

4-14.

Unit gross margins are typically computed with an allocation of fixed costs. Total fixed

costs generally will not change with a change in volume within the relevant range.

4-15.

4-16.

Production constraints mean that managers have to consider the opportunity cost of

4-17.

Common nonfinancial considerations that are important in deciding to drop a product

4-18.

The theory of constraints focuses on these three factors:

Solutions to Critical Analysis and Discussion Questions

4-19.

4-20.

4-21.

Although the variable cost of a passenger is very low, airlines do not usually price

4-22.

4-23.

4-24.

There is a danger that in making pricing decisions, especially in the short term,

4-25.

Variable costs are usually relevant when talking about changes in production volumes.

4-26.

In the short run, sales revenues need only cover the differential costs of production and

4-27.

This is a difficult and complex issue, so the purpose of this question is to stimulate

discussion and have students think about the complexities of using incremental costs as

a basis for decision making.

4-28.

Most likely most and maybe all of the opportunity costs identified are not included in the

accounting records. Although they are important in the decision, they are difficult to

4-29.

The differential costs include:

• Fuel

4-30.

The differential costs include:

• Cost of the car

• Forgone interest income on funds paid for the car

4-31.

This approach will maximize profits only if there are no constraints on production or

4-32.

Fixed costs are relevant anytime they change with the product-mix decision. For

4-33.

4-34.

Profits can be increased by decreasing investments, increasing throughput, and

Solutions to Exercises

4-35. (25 min.) Special Orders: Maria’s Food Service.

a.

Status Quo

3,000 Units

Alternative

3,300 Units

Difference

Sales revenue …….

$ 18,000

$19,050

$1,050

(higher)

Variable costs:

(higher)

Contribution margin

(higher)

Fixed costs …………

Sales revenue ……………………………………………………..

a Variable costs per meal = ($13,500 – $4,500) ÷ 3,000 units

4-36. (25 min.) Special Orders: Alpine Luggage.

Alpine should accept the offer; profit is higher by $80,000.

a.

(All revenues and costs in $000)

Status Quo

80,000 Units

Alternative

85,000 Units

Difference

Sales revenue …………………..

$ 12,800

$13,300

$500

(higher)

Variable costs:

(higher)

Contribution margin ……………

$5,200

(higher)

Sales revenue ……………………………………………………..

4-37. (30 min.) Pricing Decisions: MTA Sandwiches.

a.

Status Quo

6,000 units

Alternative

6,400 units

Difference

Sales revenue ……………

$43,200a

$45,360b

$2,160

(higher)

Less variable costs:

Materials………………..

16,200

17,280

1,080

(higher)

(higher)

Variable overhead …..

(higher)

(higher)

Contribution margin ……

(higher)

Less fixed costs …………

10,800

4-38. (30 min.) Pricing Decisions: Rutkey Collectibles.

a.

Status Quo

20,000 Cars

Alternative

23,000 Cars

Difference

Sales revenue ……………

$800,000a

$884,000b

$84,000

(higher)

Less variable costs:

(higher)

(higher)

(higher)

(higher)

Contribution margin ……

$12,000

(higher)

Less fixed costs …………

c. An important factor to consider would be the effect on the regular business once

4-39. (30 min.) Special Order: Andreasen Corporation.

(All Costs in Thousands of Dollars)

a.

Status Quo

100,000 Units

Alternative

107,500 Units

Difference

Sales revenue ……………

$10,000a

$10,450b

$450

(higher)

Less variable costs:

Materials………………..

3,600

3,885c

285

(higher)

1,505

(higher)

(higher)

(higher)

Contribution margin ……

(higher)

Less fixed costs …………

(higher)

Operating profits would be higher with the additional order by $10,000.

4-40. (30 min.) Special Order: Fairmont Travel Gear.

(All Costs in Thousands of Dollars)

a.

Status Quo

45,000 Units

Alternative

48,000 Units

Difference

Sales revenue ……………

$4,050.0a

$4,239.0b

$189

(higher)

Less variable costs:

Materials………………..

1,215.0

1,314.0c

99.0

(higher)

810.0

(higher)

(higher)

(higher)

Contribution margin ……

(higher)

Less fixed costs …………

405.0

(higher)

c. This question can be answered using the break-even analysis of Chapter 3. The

4-41. (10 min.) Target Costing and Pricing: Sid’s Skins.

Profit

=

(Price – Costs)

=

20% Costs

4-42. (10 min.) Target Costing and Pricing: Domingo Corporation.

Profit

=

(Price – Costs)

=

25% Costs

4-43. (20 min.) Target Costing and Purchasing : Mira Mesa Appliances.

$126.

The target cost for Mira Mesa is calculated as follows:

Profit

=

(Price – Costs)

=

30% Price

4-44. (20 min.) Target Costing: Kearney, Inc.

0.5 hours.

The target cost for Kearney is calculated as follows:

Profit

=

(Price – Costs)

=

20% Costs

4-45. (20 min.) Make-or-Buy Decisions: Mobility Partners.

The $20,000 savings could not be achieved. The cost to make is only $16,000 more

than the cost to purchase from Trailblazers.

Status Quoa

Alternative

Difference

Trailblazers’ offer …………….

$ –0–

$440,000

$440,000

(higher)

Materials ………………………

100,000

100,000

(lower)

Labor …………………………....

212,000

212,000

(lower)

Variable overhead …………..

(lower)

Alternative presentation.

Differential costs to make:

Direct materials ……………….

$ 50

Direct labor …………………….

Variable overhead ……………

Avoidable fixed overhead …

(= $80,000 ÷ 2,000 units)

4-46. (15 min.) Make or Buy Decisions: Mel’s Meals 2 Go.

Mel could save $0.10 per cookie ($0.20 per lunch) by making the cookies rather than

buying them.

Status Quo

(Buy)

Alternative

(Make)

Difference

(Buy–Make)

Cost to buy ……………

$0.60

$ 0

$0.60

(higher)

Direct labor ……………

(lower)

Variable overhead ….

(lower)

4-47. (10 min.) Make or Buy with Opportunity Costs: Mel’s Meals 2 Go.

In this case, he should continue to buy the cookies. The cost of making 20,000 cookies

4-48. (30 min.) Dropping Product Lines: Cotrone Beverages.

Status Quo

Alternative:

Drop

Strawberry

Difference

(all lower under

the alternative)

Revenue …………………

$253,200

$167,600

$85,600

Less Variable Costs …

(77,200)

Contribution Margin ….

Less Fixed Costs ……..

(28,480)

4-49. (30 min.) Dropping Product Lines: Freeflight Airlines.

Status Quo

Alternative:

Drop

U.S. to Europe

Difference

(all lower under

the alternative)

Revenue …………………

$ 8.80

$6.00

$2.80

Less Variable Costs …

Contribution Margin ….

$ 4.90

Less Fixed Costs ……..

4-50. (30 min.) Theory of Constraints: CompDesk, Inc.

b. No. Operating profit would decrease by $11,250 (as shown below).

Differential revenues ($300 150 units) …………

$45,000

Differential costs:

Differential revenues ($300 150) …………………

Differential costs:

4-51. (30 min.) Theory of Constraints: Playful Pens, Inc.

Solutions to Problems

4-52. (60 min.) Special Order: Unter Components.

a.

Direct labor hours per unit:

Model

Labor

cost per

unit

÷

Wage rate

per

labor-hour

=

Labor-hours per unit

Star100

$60

÷

$40

=

1.5 hours

Star150

÷

$40

=

2.0 hours

Differential revenues:

=

Differential costs

=

b. Total hours required for the additional business: 3,500 x 1.5 hours + 3,500 x 2.0

hours = 12,250 hours. The total production time required now is 10,000 hours (for

4-52. (continued)

Star100

Star150

Revenue per unit …………………………….

$580

$780

Variable cost per unit ……………………….

220

270

Contribution margin per unit ……………..

$360

Divide by Direct-labor hours per unit ..

Star100.

The total contribution margin with the special order:

Star100

Star150

Total

Special order

Contribution margin per unit

(Price – Variable cost)

$180a

$230a

Number of units

3,500

3,500

Total contribution margin

Regular production:

Contribution margin per unit

Number of units

Star100

Star150

Regular production:

Contribution margin per unit

Number of units

4-52. (continued)

c.

The total contribution margin with the special order:

Star100

Star150

Total

Special order

Contribution margin per unit*

$180

$230

Number of units

Regular production:

Contribution margin per unit*

$360

$510

Additional direct-labor costs [(22,250 hours – 20,000 hours) x $20]

Additional variable overhead (2,250 hours x $10 per hour)

4-53. (30 min.) Special Orders: Sherene Nili

a. Based on profit, Ms. Nili should accept the special order. Accepting the special

order means Ms. Nili will only be able to produce 10 standard dresses. Each

Without

Special

Order

With

Special

Order

Impact

Revenuea ………………………..

$ 80,000

$ 89,000

$ 9,000

increase

Materialsb ………………………..

18,000

20,000

2,000

increase

29,000

34,500

5,500

increase

decrease

Rent ……………………………….

Heat and light …………………..

1,600

1,600

0

Other production costs ………

2,800

2,800

0

Marketing and administration

7,700

7,700

0

Operating profit ………………..

$ 13,000

$ 14,510

$ 1,510

increase*

Additional revenue ………………………

= $24,000 –10 x ($30,000 ÷ 20)

Additional materials ……………………..

Additional labor …………………………..

Reduced machine depreciation ……………………..

4-53. (continued)

c. Ms. Nili should consider whether there will be customers who planned to order a

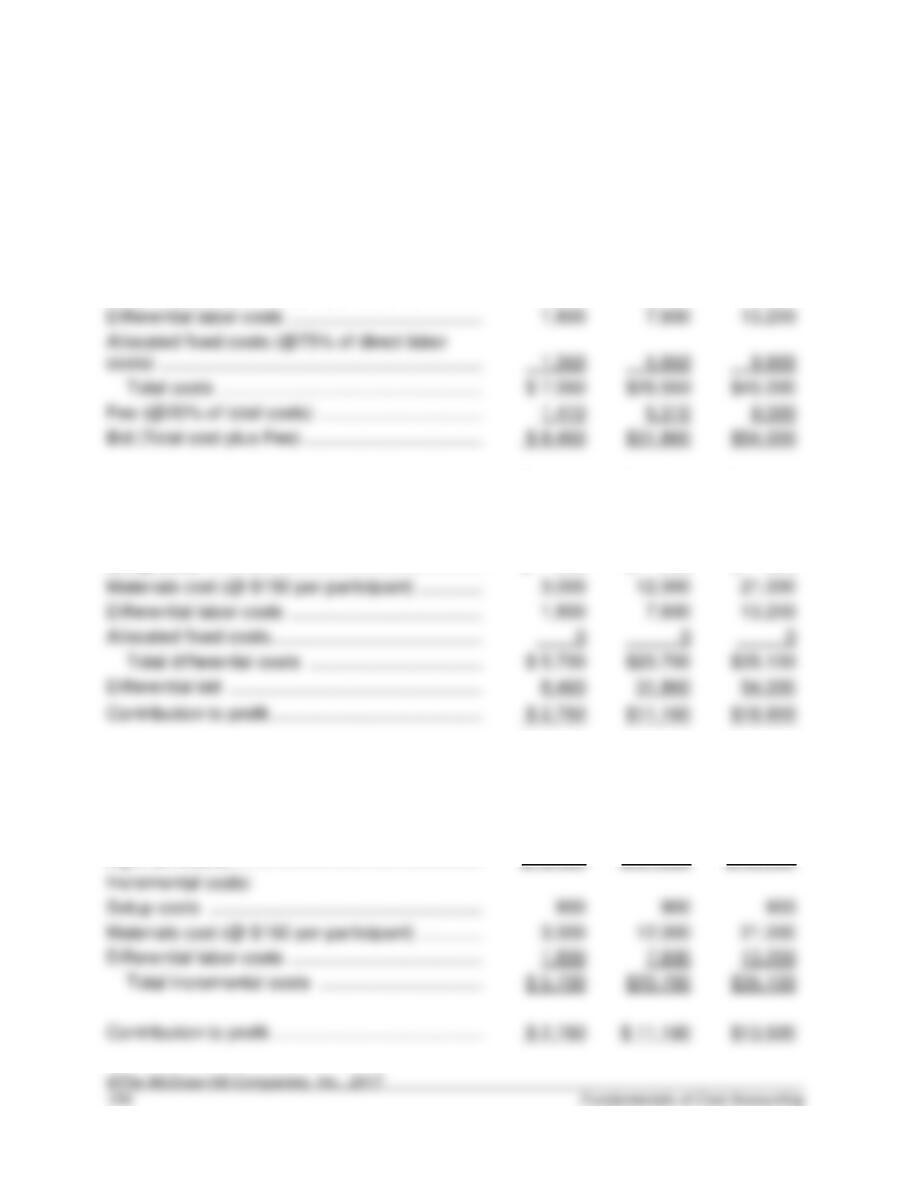

4-54. (30 min.) Pricing Decisions: CSU EE

a.

One

Four

Eight

Seminar

Seminars

Seminars

Number of participants …………………………………………

20

80

140

Setup costs ………………………………………………………..

$ 900

$ 900

$ 900

Materials cost (@ $150 per participant) …………………..

3,000

12,000

21,000

Differential labor costs ………………………………………….

7,800

Allocated fixed costs (@75% of direct labor

costs) …………………………………………………………………

b.

One

Four

Eight

Seminar

Seminars

Seminars

Differential costs:

Setup costs ………………………………………………………..

$ 900

$ 900

$ 900

Materials cost (@ $150 per participant) …………………..

3,000

12,000

21,000

Differential labor costs ………………………………………….

7,800

Allocated fixed costs……………………………………………..

0

Differential bid …………………………..………………………..

8,460

Contribution to profit ……………………………………………..

c. Disagree. The contribution to profit is greatest for eight seminars.

One

Four

Eight

Seminar

Seminars

Seminars

Bid (from requirement a, above, @90% for

eight seminars) …………………………………………………….

$ 8,460

$ 31,860

$ 48,600

Incremental costs:

Setup costs ………………………………………………………..

900

900

900

Materials cost (@ $150 per participant) …………………..

3,000

12,000

21,000

Differential labor costs ………………………………………….

7,800

Contribution to profit ……………………………………………..

$ 11,160

4-55. Pricing Decisions: M. Anthony, LLP.

Variable cost per song = $20,000 (= $17,000 + $3,000)

Profit

=

(P – V)X – F

=

b. Profit will be $40,000 higher if the price is $90,000 per song:

Price per song

$80,000

$90,000

Number of songs ……….

Revenue …………………..

$4,800,000

$4,680,000

Variable cost …………….

Contribution margin ……

$3,600,000

$3,640,000

Fixed cost …………………

Profit ………………………..

c. Profit will be $150,000 more if M. Anthony accepts the order. The contribution

margin per song for the school’s songs will be $25,000 (= $40,000 – $15,000):

4-55 (continued)

d. The lowest price on the school’s songs that M. Anthony can accept without reducing

4-56. (120 min.) Comprehensive Differential Costing Problem: Davis Kitchen

Supply.

This problem gives students a good understanding of the fixed/variable cost

dichotomy. It is worthwhile to emphasize to students that fixed costs may be

“unitized” (i.e., allocated to individual units of product) for certain purposes, and that

a. Recommendation: Lowering prices reduces operating profit. Other factors, such as

the reduction of available capacity and the impact on market share, could also affect

the decision.

Before Price

Reduction

After

Price

Reduction

Impact

Sales price ………………………

$ 370

$ 325

Quantity …………………………..

6,000

7,000

Revenue ………………………….

increase

increase

Variable marketing costs ……

increase

decrease*

Fixed manufacturing costs …

Fixed marketing costs ……….

4-56. (continued)

b. Recommendation: Don’t accept contract.

Without

Government

Contract

With Government Contract

Impact

Regular

Government

Total

Revenue …………………………………………

$2,960,000

$2,590,000

$245,000a

$2,835,000

$125,000

decrease

Variable manufacturing costs …………….

1,200,000

1,050,000

150,000

1,200,000

–0–

Variable marketing costs …………………..

decrease

Fixed manufacturing costs ………………..

–0–

Fixed marketing costs ………………………

4-56. (continued)

c. Minimum price = variable mfg. costs + shipping costs + order costs =

Some students solve for this price using the break-even formula:

X = 2,000 units = F/(P – V)

2000 units = $4,000/(P – $190)

d. The manufacturing costs are sunk; therefore, any price in excess of the differential

4-56. (continued)

e. No, the $215 proposed purchase price is not acceptable.

All Production In-house

2,000 Units Contracted

Total revenue ……………………………………………..

$2,220,000

$2,220,000

Total variable manufacturing costs ………………… ……………

900,000

1,030,000

a

Total variable marketing costs ………………………. ……………………

Total contribution margin ……………………………… …………………………

$1,170,000

$1,050,000

Total fixed manufacturing costs …………………….. …………………

360,000

c

Total fixed marketing costs …………………………... ………………………

The $215 proposed purchase price is not acceptable; it would decrease income by

$12,000.

A shorter approach follows:

Variable manufacturing cost saved ……………………….

$150

per unit

Variable marketing saved ($25 – $20) …………………..

per unit

Fixed manufacturing cost saved …………………………...

per unit

4-56. (continued)

f.

6,000 Regular

Stoves Produced

Contract 2,000 Regular Stoves;

Produce 1,600 Modified Stoves and 4,000 Regular Stoves

In-house

Regular (In)

Regular (Out)

Modified

Total

Revenue ……………………………….

$2,220,000

$1,480,000

$740,000

$720,000

$2,940,000a

Variable manufacturing costs …..

900,000

600,000

430,000

440,000

1,470,000b

Variable marketing costs …………

$270,000

$200,000

Fixed manufacturing costs ……….

360,000

Fixed marketing costs ……………..

Now the proposal should be accepted at a price of $215. The use of freed-up facilities makes the deal with the subcontractor

more valuable. Compared to part e, Davis no longer saves any fixed manufacturing cost by subcontracting because the

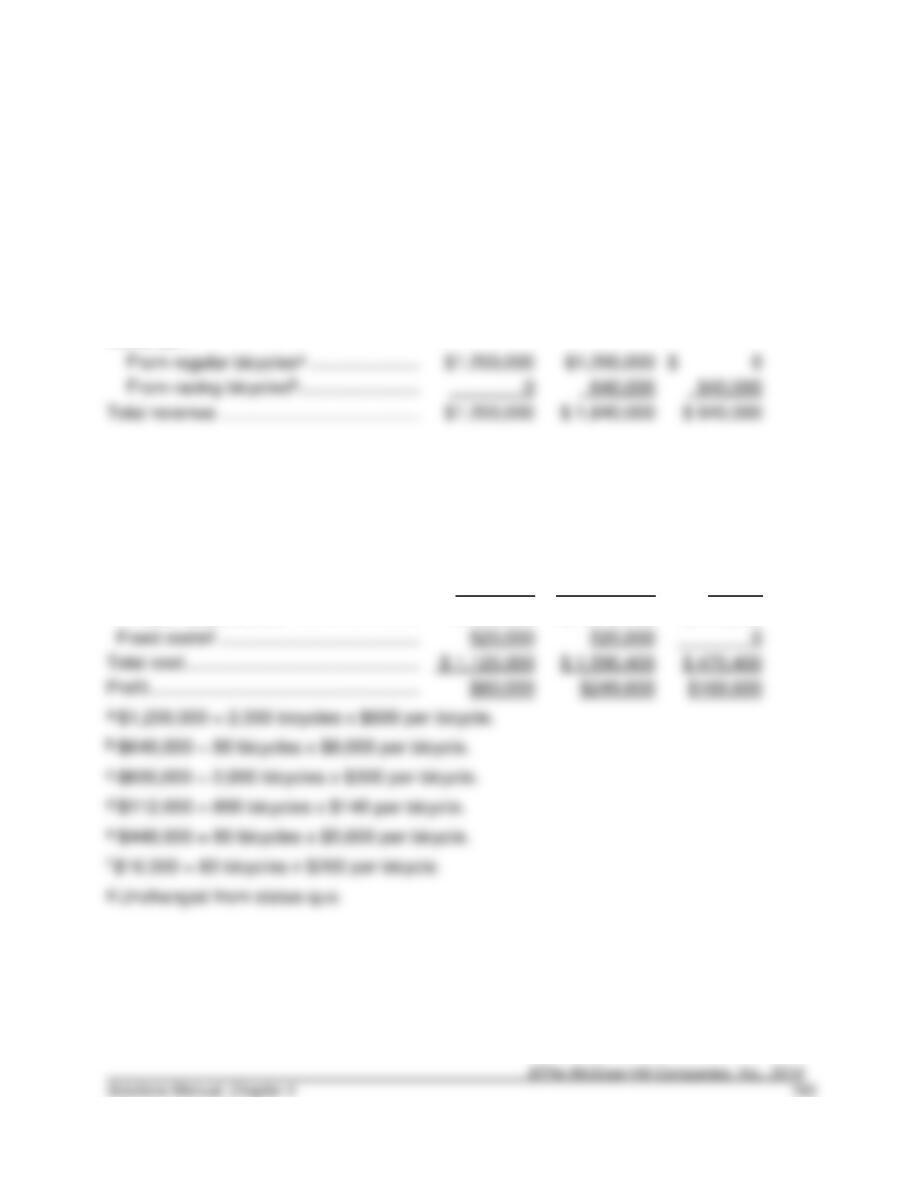

4-57. (60 min.) Make or Buy: King City Specialty Bikes (KCSB).

a. The in-house unit cost that should be used to evaluate the quotation received from the

outside contractor is $192. Therefore the proposal for $140 from the outside contractor

should be accepted.

Without contract:

Per unit

Number of

Bicycles

Total costs

Variable costs

Fixed costs

Total fixed costs …………………………

The unit variable costs incurred by KCSB for the bikes assembled by the supplier are

$144 (= $240 x [1 – 40%]) manufacturing costs and $24 (= $60 x [1 – 60%])

nonmanufacturing costs, for a total of $168 (= $144 + $24) per bicycle.

With contract (before payment to supplier)

Total costs

For the bikes assembled by KCSB:

Variable costs:

Per unit

For the bikes assembled by KCSB ……….

For the bikes not assembled by KCSB ….

Total variable costs …………………………...

Fixed costs

Total fixed costs …………………………………

4-57. (continued)

b. The additional revenue from the racing bicycles is greater than the additional costs

from using the supplier and assembling the racing bicycles. Therefore the supplier’s

offer should be accepted.

Status Quo

Accept

Supplier’s

Offer and

Assemble 80

Racing

Bicycles

Difference

Revenue:

From regular bicyclesa ………………….

From racing bicyclesb ……………………

Total revenue ………………………………….

$ 1,840,000

$ 640,000

Costs:

Variable costs

From regular bicyclesc ………………….

$ 600,000

$ 494,400

$ (105,600)

Payment to supplierd …………………….

0

112,000

112,000

For racing bicycles (manufacturing)e .

0

448,000

448,000

For racing bicycles (marketing)f ……..

0

16,000

16,000

Total variable cost ………………………

$ 600,000

$ 1,070,400

$ 470,400

Fixed costsg ………………………………….

520,000

Total cost ………………………………………..

$ 1,590,400

$ 470,400

Profit ………………………………………………

4-58. Decision Whether to Add or Drop: Agnew Manufacturing.

a. The regional market should not be dropped as this market not only covers all the

variable costs and separable fixed costs but also gives net market contribution of

$390,000 toward the common fixed costs.

Variable manufacturing costs:

b. Quarterly income statement (in thousands):

Model

Standard

Model

Superior

Model

DeLuxe

Total

Sales revenue …………………………...

$3,000

$2,400

$2,400

$7,800

Less variable costs …………………….

Manufacturing ………………………..

1,800

1,680

1,440

4,920

Marketing …………………………..….

90

48

48

186

Contribution margin

1,110

2,694

Less fixed costs:

Marketing ($630 – $186) ………….

444

Administrative…………………………

312

4-59. Decision Whether to Add or Drop: O’Neil Enterprises.

a.

Status Quo

Alternative:

Drop

Beef Barley

Difference

(all lower under

the alternative)

Revenue …………………

$126,600

$83,800

$42,800

Less Variable Costs …

(100,700)

(62,100)

(38,600)

Contribution Margin ….

Less Fixed Costs ……..

.

b.

Status Quo

Alternative:

Drop

Beef Barley

Difference

(all lower under

the alternative)

Revenue …………………

$126,600

$79,610

a

$46,990

Less Variable Costs …

(100,700)

(58,995)

b

(41,705)

Contribution Margin ….

Less Fixed Costs ……..

4-60. (30 min.) Decision Whether to Close a Store: Power Music.

We recommend that Power Music close the store. The cost savings are greater than

the lost margin on the sales. The difference, however, is not large and if there are

other considerations, they might outweigh the estimated increase in profits.

The analysis shows that closing the Fifth Avenue Store results in lost gross margin of

$270,000 (= $1,950,000 in sales less $1,680,000 in cost of goods sold). The cost

savings are $283,500:

Payroll, Direct Labor, and Supervisiona

$153,000

Renta

48,300

55,200

4-61. (45 min.) Closing a Plant: Ironwood Corporation.

a.

Ironwood Corporation

Computation of Estimated Profit from Operations

after Expansion of Minnesota Factory

Minnesota factory:

Sales ($280,000 x 150%) ……………………………………….

$420,000

Fixed costs

Factory ($56,000 x 120%) ……………………………………

Administration ($22,000 x 110%) ………………………….

Variable costs [$2 ($420,000 ÷ $5 sales price)] ……….

Allocated home office costs ……………………………………..

Total ………………………………………………………………….

Estimated operating profit ………………………………………..

Wisconsin factory—estimated operating profit ……………….

b.

Ironwood Corporation

Computation of Estimated Profit from Operations

after Negotiation of Royalty Contract

Estimated operating profit:

Wisconsin factory ……………………………………………………………

$108,000

Minnesota factory …………………………..……………………………….

82,000

Estimated royalties to be received (30,000 $1) ………………….

4-61. (continued)

c.

Ironwood Corporation

Computation of Estimated Profit from Operations

after Shutdown of North Dakota Factory

Estimated operating profit:

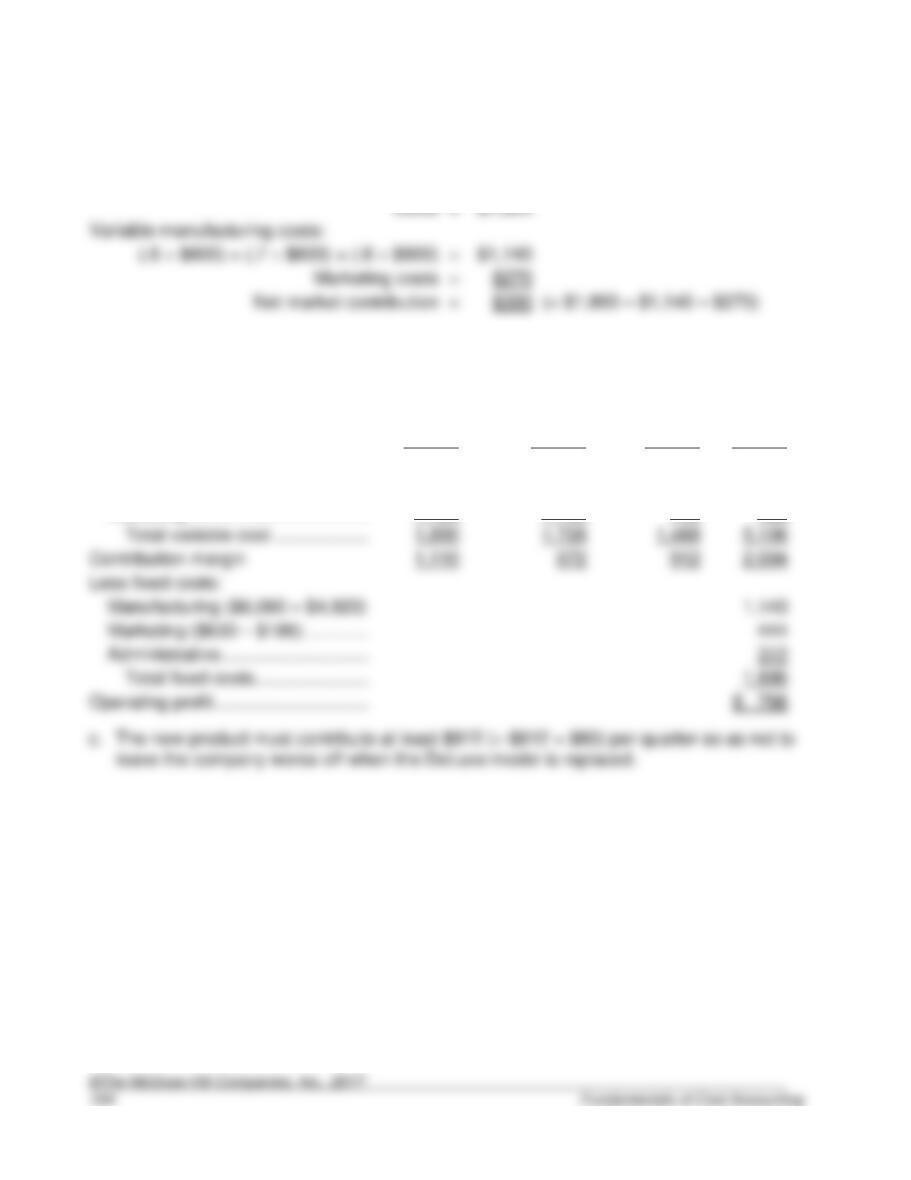

4-62. (60 min.) Optimum Product Mix: Austin Enterprises.

a.

Basic

Classic

Formal

Total revenuea ……………………………………..

$600,000

$640,000

$5,700,000

Less variable manufacturing costs:

a Revenue:

Basic

=

$30 x 20,000 units

Classic

=

$64 x 10,000 units

Formal

=

$190 x 30,000 units

b Direct materials:

Basic

$200,000

=

$20 x .5 yards x 20,000 units

Classic

$ 60,000

=

$20 x .3 yards x 10,000 units

Formal

$360,000

=

$20 x .6 yards x 30,000 units

Basic

=

$ 16 x .7 hours x 20,000 units

Classic

=

$ 16 x 2 hours x 10,000 units

Formal

=

$ 16 x 7 hours x 30,000 units

Basic

$ 56,000

=

$ 4 x .7 hours x 20,000 units

Classic

$ 80,000

=

$ 4 x 2 hours x 10,000 units

Formal

=

$ 4 x 7 hours x 30,000 units

e Variable marketing:

Basic

=

10% x $600,000 revenue

Classic

=

10% x $640,000 revenue

Formal

=

10% x $5,700,000 revenue

4-62. (continued)

b. Contribution margin per constrained resource, labor:

Basic

$4.286

=

($60,000 ÷ 20,000 units) ÷ .7 hours

c. The most profitable combination is to produce up to the demand of Classic with a

4-62. (continued)

d.

Basic

Classic

Total revenuea ………………………………………….

$428,550

$640,000

Less variable manufacturing costs:

Direct materialsb …………………………………….

142,850

60,000

Variable overheadd ………………………………..

80,000

Variable marketinge ………………………………..

64,000

a Revenue:

Basic

$428,550

14,285 units

Classic

$640,000

10,000 units

b Direct materials:

Basic

$142,850

.5 yards

14,285 units

c Direct labor:

Basic

$ 16

.7 hours

14,285 units

Classic

$320,000

$ 16

2 hours

10,000 units

d Variable overhead:

Basic

$ 4

.7 hours

14,285 units

Classic

$ 4

2 hours

10,000 units

e Variable marketing:

Basic

$42,855

$428,550 revenue

4-62. (continued)

e. At an increase in the cost of labor from $16 to $19, the contribution margins per

constrained resource of labor (10,000 additional hours) would be as follows:

Contribution margins before labor cost increase:

Basic $3.00 = $60,000 ÷ 20,000 units

The contribution per unit of constrained resource would be as follows:

Basic $1.286 = $.90 ÷ .7 hours

1/2-litre

1 -litre

Selling price ………………………….

$ 15.00

$27.00

Variable costs

Total variable cost …………………

Contribution margin ……………….

$ 19.00

÷ Hours to produce 1 unit ……….

Contribution margin per hour …..

4-63. (20 min.) Optimum Product Mix: Bubble Company.

Bubble should produce only 1/2-litre bottles.

Although the capacity of the machine is missing, it is not necessary to answer the

question. Because the demand for both products is essentially unlimited, the machine

An equivalent approach is to consider the machine depreciation when computing the

contribution margin (it is listed as variable with respect to hours). In the solution above,

we recognize that because we will operate the machine at capacity, the cost is really

fixed. If we treat it as variable, the solution is as follows:

1/2-litre

1 -litre

Selling price ………………………….

$ 15.00

$27.00

Variable costs

Total variable cost …………………

Contribution margin ……………….

$11.00

÷ Hours to produce 1 unit ……….

Contribution margin per hour …..

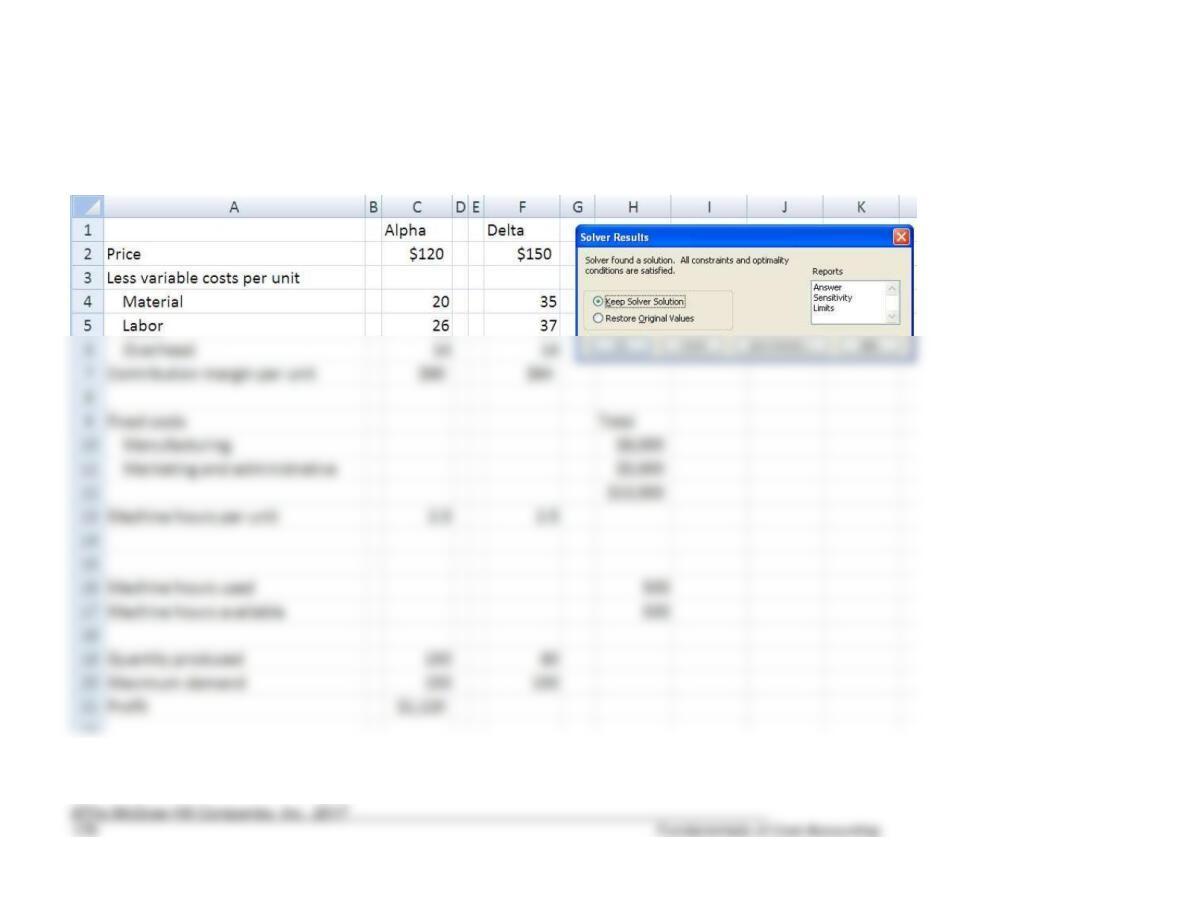

4-64. (20 min.) Optimum Product Mix – Excel Solver: Slavin Corporation.

a. Slavin should produce 150 units of Alpha and 80 units of Delta. The next two pages

show the setup using Excel Solver and the solution. The problem can be solved

without Excel as follows. First, compute the contribution margins per hour on the

machine for the two products:

Alpha:

($60 ÷ 2.0) = $30.00 per hour

b. As shown in the Excel spreadsheet, production of 150 units of Alpha and 80

4-64. (continued)

(i)Setup of Excel Solver:

4-64. (continued)

(ii) Solution to problem:

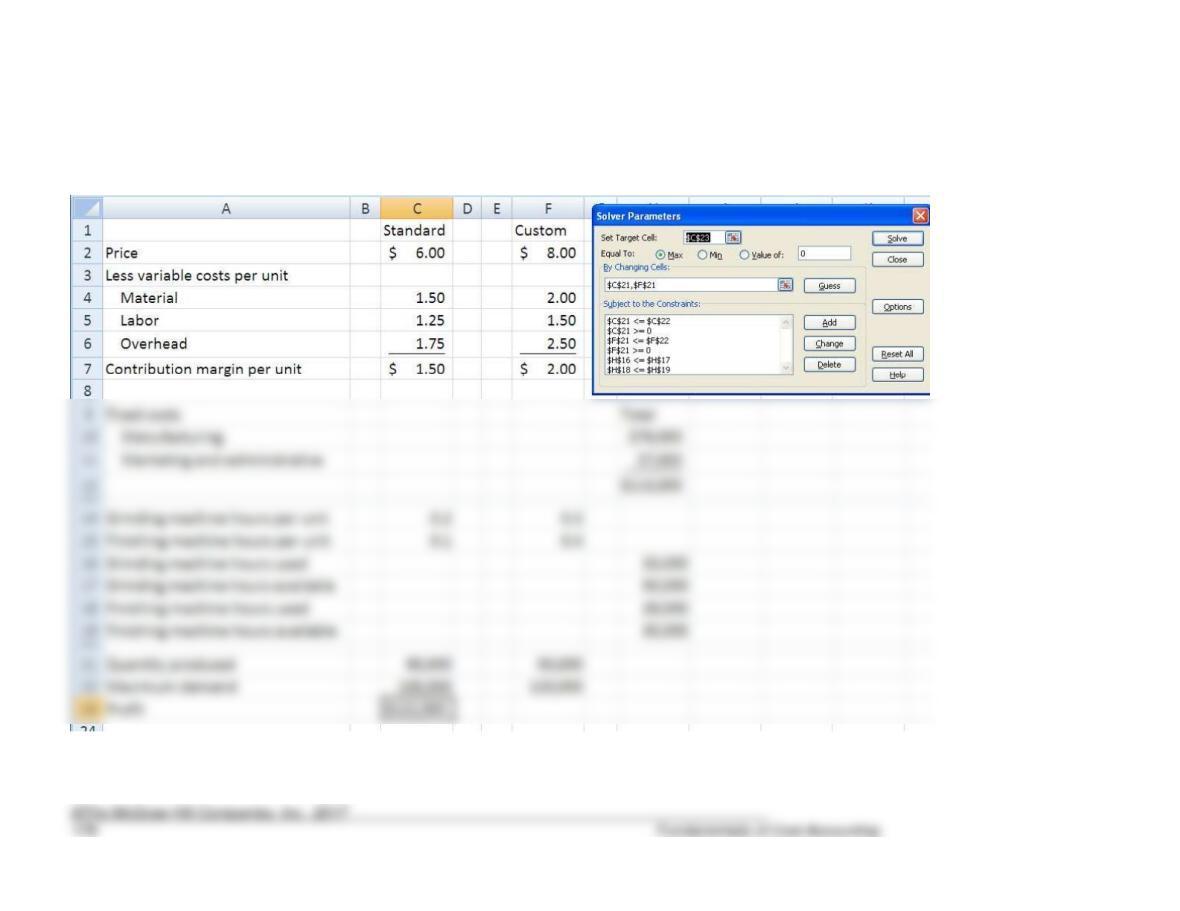

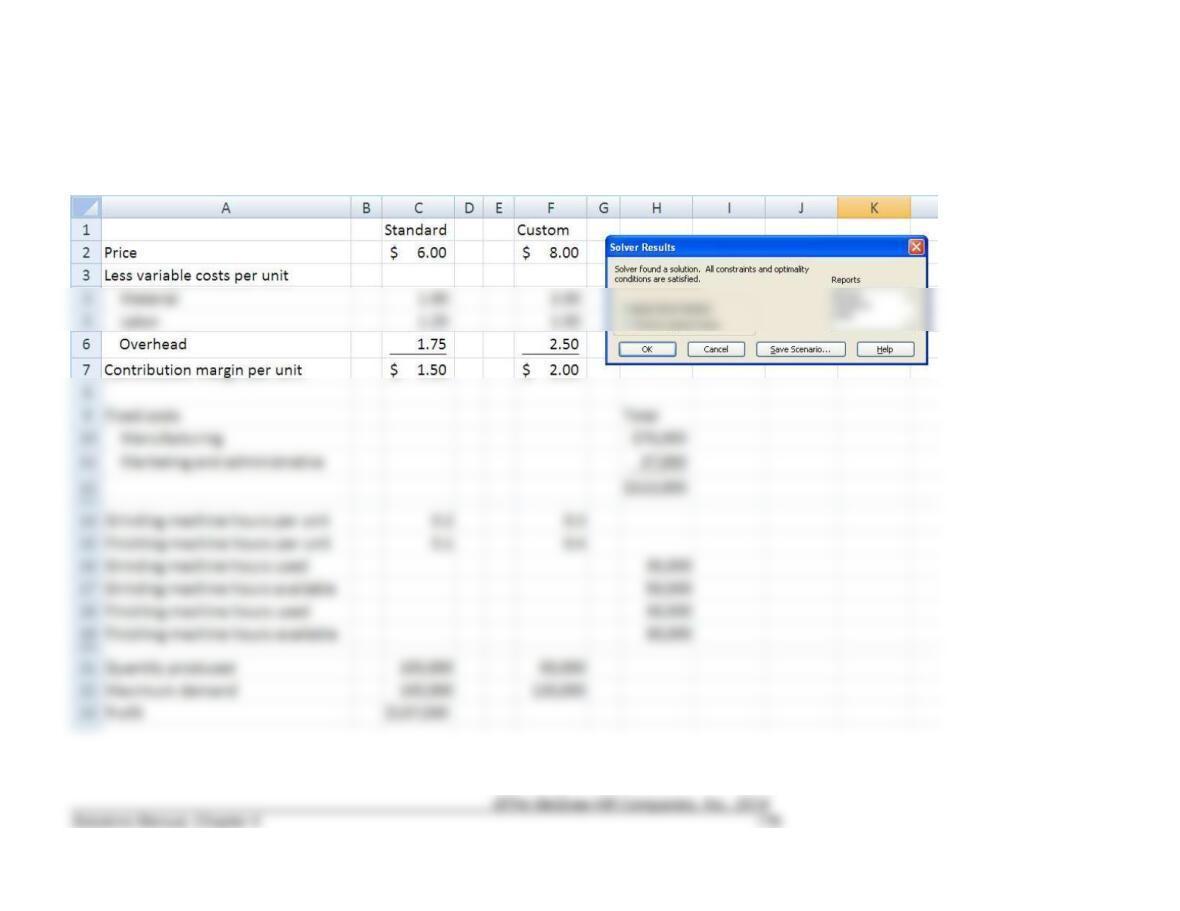

4-65. (20 min.) Optimum Product Mix – Excel Solver: Layton Machining

Company.

a. Layton should produce 100,000 Standard units 50,000 Custom units. The next two

pages show the setup using Excel Solver and the solution. The problem can be

solved without Excel as follows. First, compute the contribution margins per hour

on the machine for the two products:

Standard (Grinding machine):

($1.50 ÷ 0.2) = $7.50 per hour

Standard (Finishing machine):

($1.50 ÷ 0.1) = $15.00 per hour

Custom (Finishing machine):

($2.00 ÷ 0.4) = $5.00 per hour

Because Standard has a higher contribution margin per unit of both constraining

resources, Layton should produce up to demand (100,000 units) assuming

machine capacity is available. It requires 20,000 grinding hours to produce 100,000

4-65. (continued)

(i)Setup of Excel Solver:

4-65. (continued)

(ii) Solution to problem:

Solutions to Integrative Cases

4-66. (30 min.) The Effect of Cost Structure on Predatory Pricing: American

Airlines.

a The relation between variable cost and price is important in a predatory pricing case

because there is no rational economic reason for setting price below variable cost (and

4-67. (120 min.) Make versus Buy: Liquid Chemical Company.

NOTE: Working this case requires knowledge of how to calculate discounted cash

flows.

a The four alternatives are:

• Alternative A: It is the “status quo,” i.e., Liquid Chemical Co. will continue making the

containers and performing maintenance.

b. The incremental cash flow analyses were conducted assuming a five-year time

horizon. The detailed cash flow analyses for Alternatives A, B, C, and D as well as

more detailed information on the calculations are shown on pages 183-190 below.

General considerations for the incremental cash flows are provided below.

• All cash flows occur at the end of the year.

• The last day of Year 0 is when the decision on the alternatives is made. It can also be

4-67. (continued)

Alternative A

Alternative B

Alternative C

Alternative D

Make

Containers;

Make

Containers; Buy

Buy Containers;

Perform

Buy Containers;

Buy

c. Although Alternative C seems to be the more attractive, its net present value is not

significantly different from the net present values of Alternatives A and D. This

situation requires a careful examination of facts and assumptions made. A brief

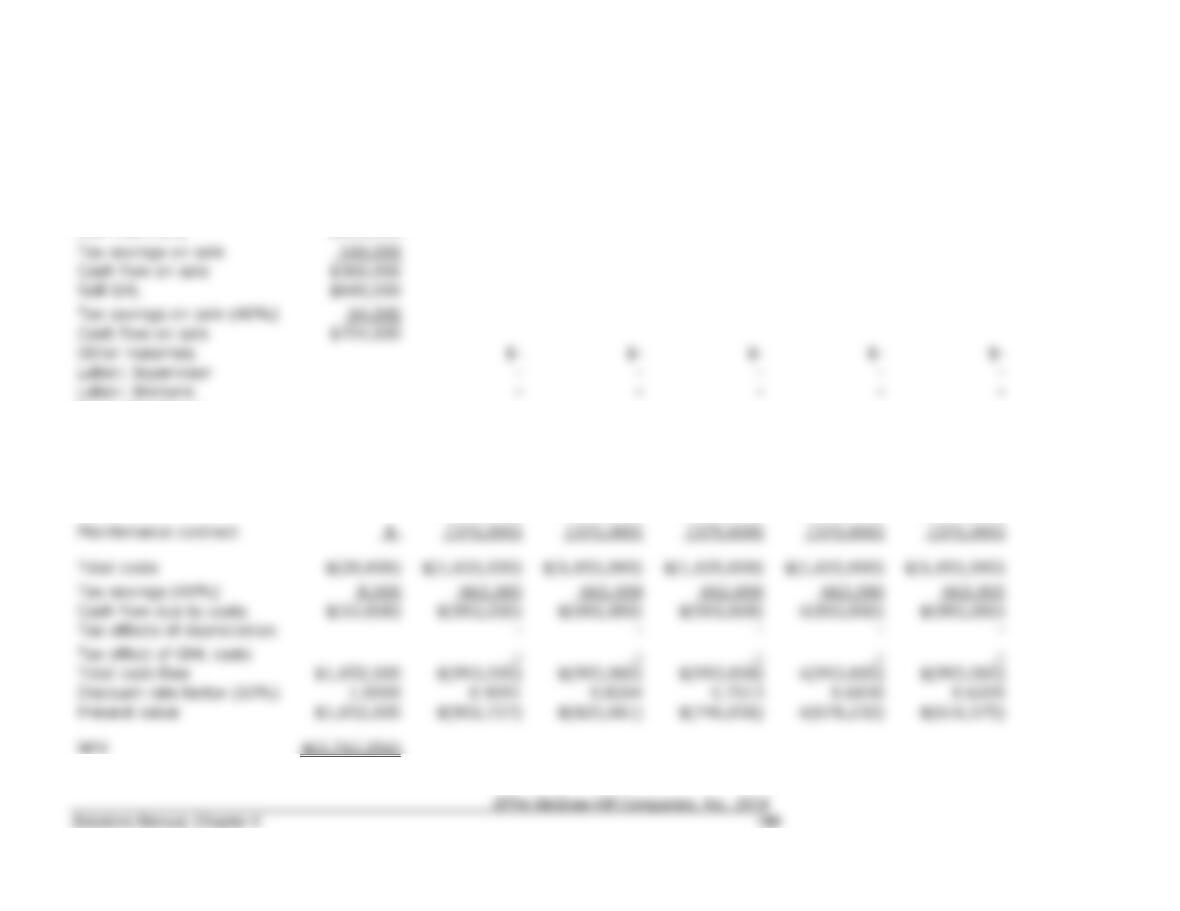

4-67. (continued)

Incremental Cash Flow – Alternative A

Make Containers and Perform Maintenance

Year of Operation

0

1

2

3

4

5

Buy GHL

$(240,000)

Tax savings on purchase (40%)

$96,000

Cash flow on purchase

$(144,000)

Other materials

$(500,000)

$(500,000)

$(500,000)

$(500,000)

$(500,000)

Labor: Supervisor

Labor: Workers

Rent: Warehouse

Maintenance

Other expenses

Manager’s salary

Total costs

Tax savings (40%)

Cash flow due to costs

$(815,100)

$(815,100)

$(815,100)

$(815,100)

$(815,100)

Tax effects of depreciation

60,000

60,000

60,000

60,000

Tax effect of GHL costs

Total cash flow

$(675,100)

$(675,100)

$(675,100)

$(675,100)

$(959,100)

Discount rate factor (10%)

1.0000

Present value

$(613,727)

$(557,934)

$(507,213)

$(461,102)

$(595,526)

$(2,735,502)

4-67. (continued)

Considerations (Alternative A):

• Under this alternative, GHL consumption is 40 tons per year. At the end of Year 4 the GHL stock is zero, and a

4-67. (continued)

Incremental Cash Flow – Alternative B

Make Containers and Buy Maintenance

Year of Operation

0

1

2

3

4

5

Buy GHL

$(120,000)

Tax savings on purchase (40%)

$48,000

Cash flow on purchase

$(72,000)

Other materials

$(450,000)

$(450,000)

$(450,000)

$(450,000)

$(450,000)

Labor: Supervisor

(50,000)

(50,000)

(50,000)

(50,000)

(50,000)

Labor: Workers

(360,000)

(360,000)

(360,000)

(360,000)

(360,000)

Rent: Warehouse

(85,000)

(85,000)

(85,000)

(85,000)

(85,000)

Maintenance

(36,000)

(36,000)

(36,000)

(36,000)

(36,000)

Other expenses

Manager’s salary

(80,000)

(80,000)

(80,000)

(80,000)

(80,000)

Maintenance contract

Total costs

$(1,528,500)

$(1,528,500)

$(1,528,500)

$(1,528,500)

$(1,528,500)

Tax savings (40%)

611,400

611,400

611,400

611,400

611,400

Cash flow due to costs

$(917,100)

$(917,100)

$(917,100)

$(917,100)

$(917,100)

Tax effects of depreciation

60,000

60,000

60,000

60,000

Tax effect of GHL costs

Total cash flow

$(785,100)

$(785,100)

$(785,100)

$(785,100)

$(957,100)

Discount rate factor (10%)

Present value

$(713,727)

$(648,843)

$(589,857)

$(536,234)

$(594,284)

$(3,082,945)

4-67. (continued)

Considerations (Alternative B):

• Under this alternative, GHL consumption is 36 tons per year (= 40 X 90%). At the end of Year 4 the GHL stock is

16 tons, and a purchase of 20 tons is necessary. At that time, the price will be $6,000 per ton.

4-67 (continued)

Incremental Cash Flow – Alternative C

Buy Containers and Perform Maintenance

Year of Operation

0

1

2

3

4

5

Sell machinery

$200,000

Tax savings on sale (40%)

160,000

Cash flow on sale

$360,000

Sell GHL

$560,000

Tax savings on sale (40%)

Cash flow on sale

$616,000

Other materials

Labor: Supervisor

Labor: Workers

Rent: Warehouse

Severance pay

Other expenses

Manager’s salary

Container contract

Total costs

Tax savings (40%)

Cash flow due to costs

Tax effects of depreciation

Tax effect of GHL costs

Total cash flow

$966,400

Discount rate factor (10%)

1.0000

0.9091

0.8264

0.7513

0.6830

0.6209

Present value

$966,400

4-67 (continued)

Considerations (Alternative C):

• Under this alternative, GHL consumption is 4 tons per year (40 X 10%), or 20 tons over five years. Therefore,

Liquid Chemical can sell 140 tons (= 160 – 20) at the end of Year 0 at $4,000 per ton.

4-67 (continued)

Incremental Cash Flow – Alternative D

Buy Containers and Buy Maintenance

Year of Operation

0

1

2

3

4

5

Sell machinery

$200,000

Tax savings on sale

Cash flow on sale

Sell GHL

$640,000

Tax savings on sale (40%)

Cash flow on sale

Other materials

Labor: Supervisor

–

–

–

–

–

Labor: Workers

Rent: Warehouse

–

–

–

–

–

Severance pay

$(20,000)

–

–

–

–

–

Pension

(30,000)

(30,000)

(30,000)

(30,000)

(30,000)

Other expenses

–

–

–

–

–

Manager’s salary

–

–

–

–

–

Container contract

(1,250,000)

(1,250,000)

(1,250,000)

(1,250,000)

(1,250,000)

Maintenance contract

(375,000)

(375,000)

(375,000)

(375,000)

(375,000)

Total costs

Tax savings (40%)

Cash flow due to costs

$(12,000)

Tax effects of depreciation

Tax effect of GHL costs

–

–

–

–

–

Total cash flow

Discount rate factor (10%)

Present value

4-67 (continued)

Considerations (Alternative D):

• Under this alternative, there is no GHL consumption. Therefore, Liquid Chemical can sell 160 tons at the end of

Year 0 at $4,000 per ton.