4-21

PROBLEM 4-29 (40 MINUTES)

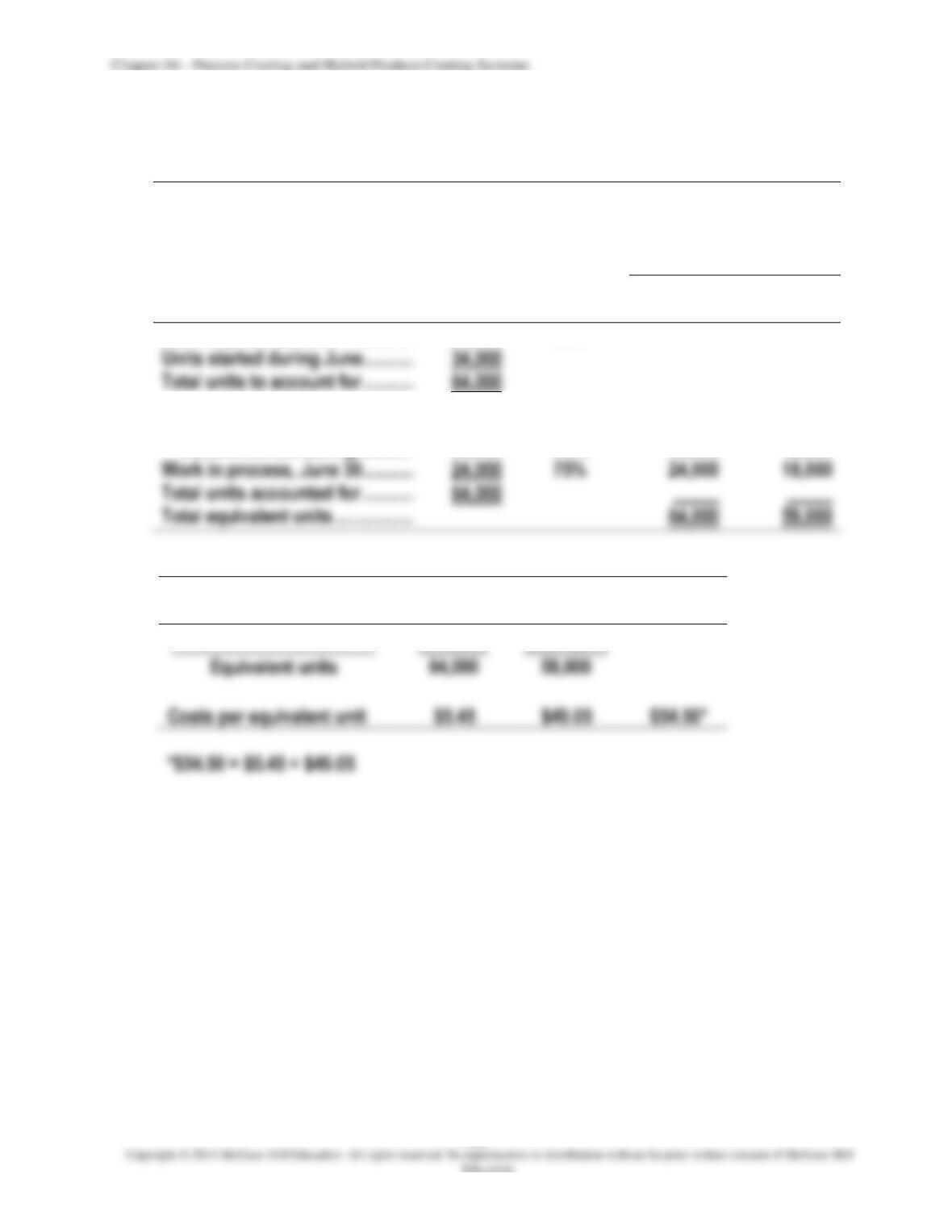

1.

a. Equivalents units:

Physical

Units

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, June 1 ………………

30,000

35%

Units started during June …………….

34,000

Total units to account for …………….

64,000

Units completed and

transferred out during June ……..

40,000

100%

40,000

40,000

Work in process, June 30 …………….

24,000

75%

24,000

Total units accounted for …………….

64,000

_____

b. Unit costs:

Direct

Material

Conversion

Total

Costs per equivalent unit

Total costs to account for

$348,800

$2,844,900

4-22

PROBLEM 4-29 (CONTINUED)

c.

Cost of goods completed and transferred out during June:

Cost remaining in June 30 work-in-process inventory:

Direct material:

percost

of number

Conversion:

Total cost of June 30 work in process ………………………………………….. $1,013,700

Check: Cost of goods completed and transferred out ……………………….

Total costs accounted for …………………………………………………….

percost

of number

2.

Journal entry:

Finished-Goods Inventory ……………………………………….

Work-in-Process Inventory ……………………………………………………….

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-23

PROBLEM 4-30 (35 MINUTES)

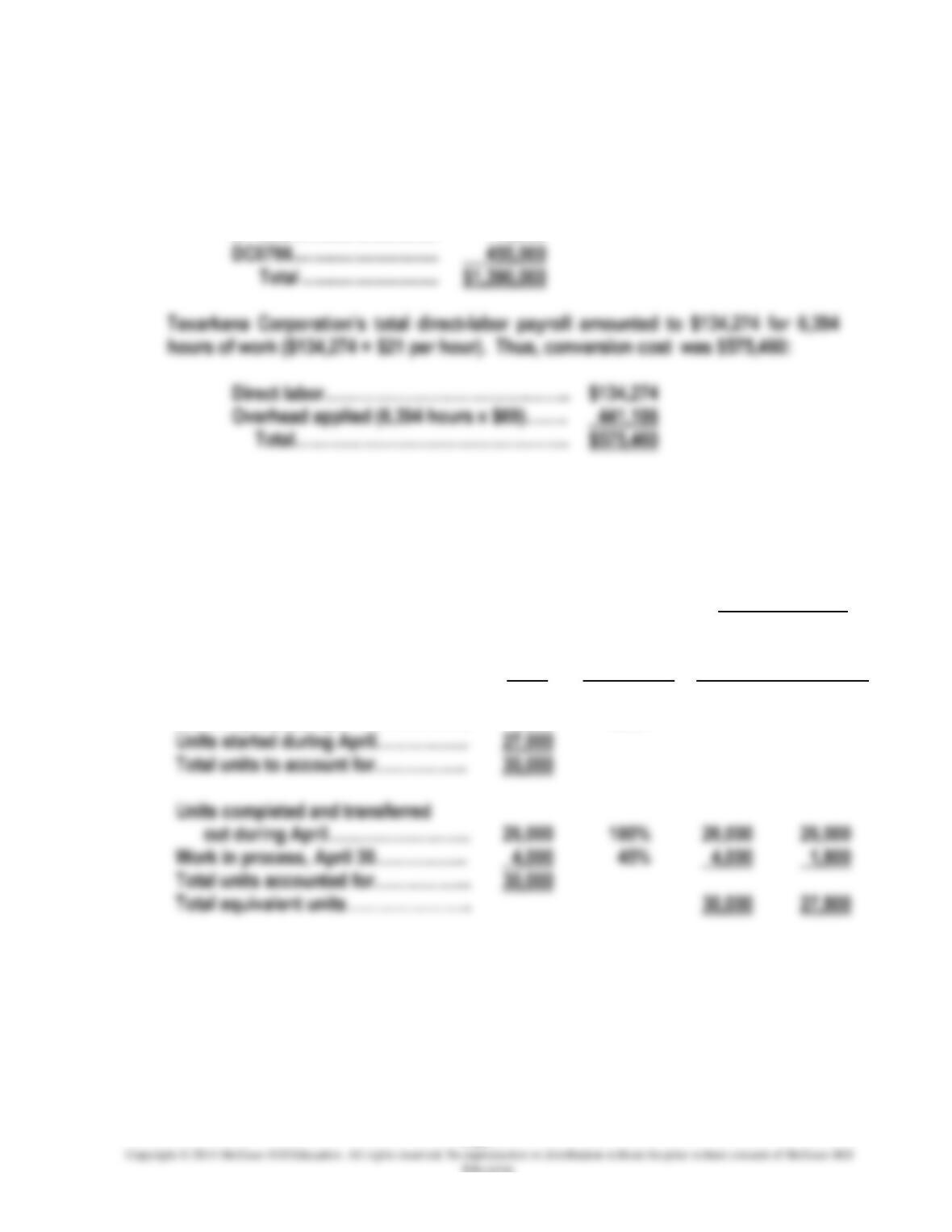

1. Direct material cost was $1,390,000:

JR1163 ………………………….

$ 225,000

JY1065 ………………………….

710,000

DC0766 ………………………….

455,000

Total ………………………..

$1,390,000

Direct labor……………………………….……..

$134,274

Overhead applied (6,394 hours x $69)……..

Total…………………………………………..

$575,460

2. Goods completed during April cost $2,002,000 (26,000 units x $77) as the following

calculations show:

Physical

Units

Percentage

Of

Completion

With

Respect to

Conversion

Equivalent Units

Direct

Material Conversion

Work in process, April 1……………….

3,000

80%

Units started during April……………..

Total units to account for……………..

Work in process, April 30……………..

4,000

Total units accounted for………………

Total equivalent units…………………..

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-24

PROBLEM 4-30 (CONTINUED)

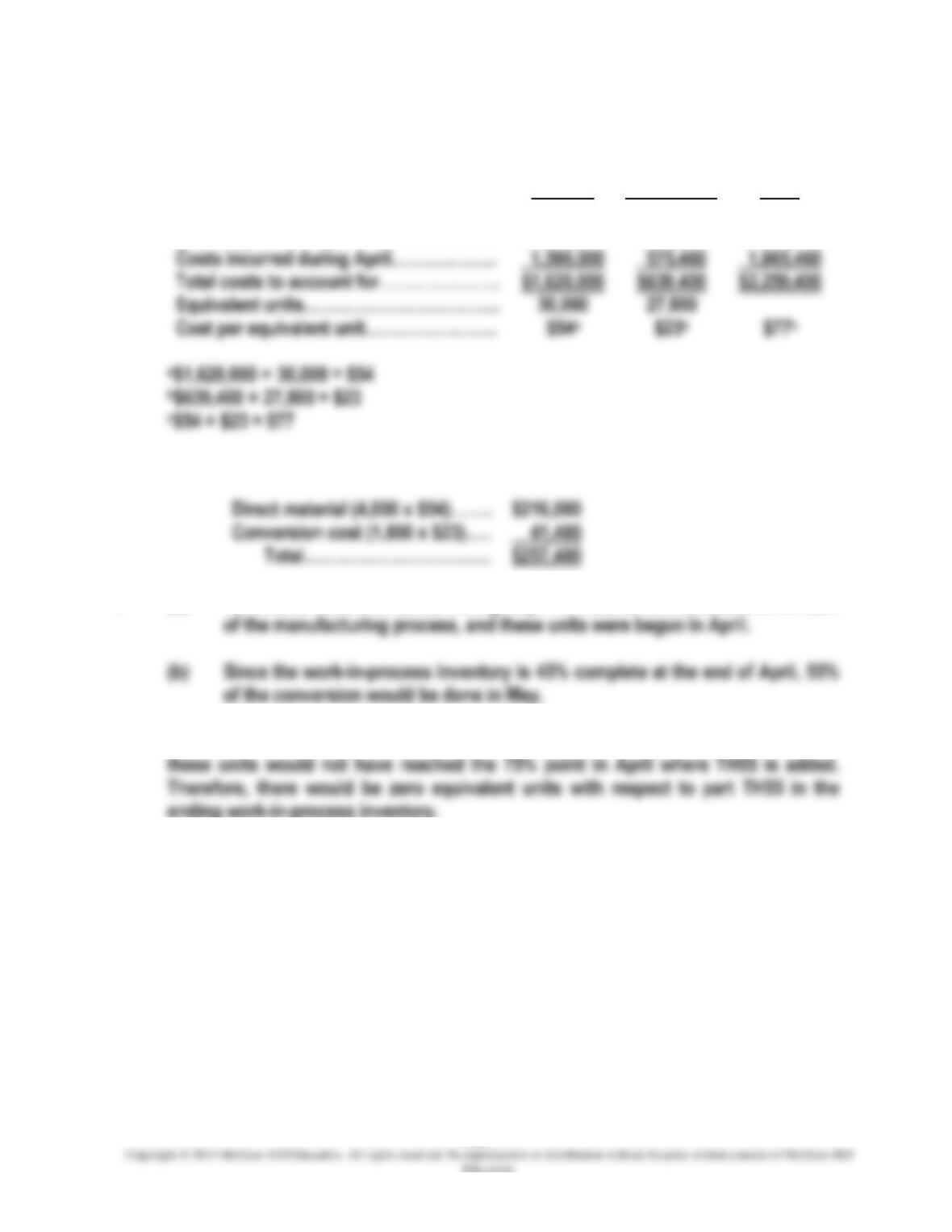

Direct

Material

Conversion

Total

Work in process, April 1……………………

$ 230,000

$ 63,940

$ 293,940

Costs incurred during April……………….

Total costs to account for………………….

$1,620,000

$639,400

$2,259,400

Equivalent units………………………………

Cost per equivalent unit……………………

3. The cost of the ending work-in-process inventory is $257,400:

Direct material (4,000 x $54)……..

$216,000

Conversion cost (1,800 x $23)…..

41,400

Total…………………………….

$257,400

4. (a) No material would be added during May. All material is introduced at the start

5. Given that the ending work-in-process inventory is at the 45% stage of completion,

4-25

PROBLEM 4-31 (50 MINUTES)

The missing amounts are shown below. A completed production report follows.

Work in process, October 1 (in units) …………………………………………………………

10,000

Units completed and transferred out during October …………………………………..

75,000

Total equivalent units: conversion ……………………………………………………………..

78,500

Work in process, October 1: conversion …………………………………………………….

$ 30,225

Costs incurred during October: direct material …………………………………………..

Cost per equivalent unit: conversion ………………………………………………………….

Cost of goods completed and transferred out during October ……………………..

Cost remaining in ending work-in-process inventory: direct material …………..

PRODUCTION REPORT: FANTASIA FLOUR MILLING COMPANY

Weighted-Average Method

Percentage

of

Completion

with

Equivalent Units

Physical

Respect to

Direct

Units

Conversion

Material

Conversion

Work in process, October 1 ……….

10,000

15%

Units started during October ……..

70,000

Total units to account for …………..

80,000

Units completed and transferred

out during October …………..

75,000

75,000

75,000

Work in process, October 31 ……..

70%

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-26

PROBLEM 4-31 (CONTINUED)

Direct

Material

Conversion

Total

Work in process, October 1 ……….

$112,000

$ 30,225

$ 142,225

Costs incurred during October …..

Total costs to account for ………….

$712,000

$1,642,225

Equivalent units ………………………..

80,000

Costs per equivalent unit …………..

$20.75**

*$8.90 = $712,000 ÷ 80,000

**$20.75 = $8.90 + $11.85

4-27

PROBLEM 4-31 (CONTINUED)

Cost of goods completed and transferred out during October:

Cost remaining in October 31 work-in-process inventory:

Direct material:

percost

of number

Conversion:

percost

of number

Total cost of October 31 work-in–process ……………………………………………….. $85,975

Check: Cost of goods completed and transferred out …… $1,556,250

Cost of October 31 work-in-process inventory ….. 85,975

Total costs accounted for ………………………………… $1,642,225

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-28

PROBLEM 4-32 (30 MINUTES)

Physical

Units

Percentage

Of

Completion

With

Respect to

Conversion

Equivalent Units

__________________

Direct

Material Conversion

________

__________

______

__________

Work in process, June 1……………….

200

25%

Units started during June……………..

800

Total units to account for………………

1,000

Units completed and transferred

during June…………………………..

600

100%

600

600

Work in process, June 30………………

400

75%

Total units accounted for………………

1,000

Total equivalent units…………………..

Direct

Material

Conversion

Total

_______

__________

______

Work in process, June 1……………………

$12,000

$ 6,000

$18,000

Costs incurred during June……………….

Total costs to account for………………….

$55,000

$36,000

$91,000

Equivalent units………………………………

Cost per equivalent unit…………………….

3. The cost of the June 30 work-in-process inventory is $34,000:

Direct material (400 x $55)………

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-29

PROBLEM 4-32 (CONTINUED)

4. Equivalent units measure the amount of manufacturing activity (i.e., for direct

material or conversion) that has been applied to a batch of physical units. If, for

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-30

PROBLEM 4-33 (30 MINUTES)

1.

a. Equivalent units:

Percentage

of

Completion

with Respect

Tax

to

Returns

Conversion

(physical

(labor and

Equivalent Units

units)

overhead)

Labor

Overhead

Returns in process, February 1 …..

300

20%

Returns started in February ………..

Total returns to account for ………..

Returns completed

during February ……………………

800

Returns in process, February 28 …

75%

Total returns accounted for ………..

b. Costs per equivalent unit:

Labor

Overhead

Total

Returns in process, February 1 ……………….

£ 3,500

£ 4,000

£ 7,500

Costs incurred during February ………………

Total costs to account for ……………………….

Equivalent units ……………………………………..

1,100

Costs per equivalent unit ………………………..

£50.00

2.

Cost of returns in process on February 28:

Labor: equivalent units cost per equivalent unit

Overhead: equivalent units cost per equivalent unit

Total cost of returns in process on February 28 …………………………………..

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-31

PROBLEM 4-34 (50 MINUTES)

The missing amounts are shown below. A completed production report follows.

Units started during January ……………………………………………………………………..

55,000

Units completed and transferred out during January …………………………………..

60,000

Total equivalent units: conversion ……………………………………………………………..

66,000

Work in process, January 1: conversion …………………………………………………….

Costs incurred during January: direct material …………………………………………..

Cost per equivalent unit: conversion ………………………………………………………….

Cost of goods completed and transferred out during January ……………………..

Cost remaining in ending work-in-process inventory: direct material …………..

PRODUCTION REPORT: CANANDAIGUA CARPET COMPANY

Weighted-Average Method

Physical

Units

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, January 1 …………

25,000

25%

Units started during January ……….

55,000

Total units to account for …………….

80,000

Work in process, January 31 ……….

20,000

30%

Total units accounted for …………….

80,000

4-32

PROBLEM 4-34 (CONTINUED)

Direct

Material

Conversion

Total

Work in process, January 1 …………………………

$232,000

$110,600

$ 342,600

Costs incurred during January …………………….

Total costs to account for …………………………...

$930,600

$1,562,600

Equivalent units ………………………………………….

Costs per equivalent unit …………………………….

Cost of goods completed and transferred out during January:

Cost remaining in January 31 work-in-process inventory:

Direct material:

percost

of number

Conversion:

percost

of number

Total cost of January 31 work in process ………………………………………..

Check: Cost of goods completed and transferred out ..

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-33

PROBLEM 4-35 (45 MINUTES)

1.

PRODUCTION REPORT: MIXING DEPARTMENT

(Weighted-Average Method)

November 20×5

Percentage

of

Completion

with

Equivalent Units

Physical

Respect to

Direct

Units

Conversion

Material

Conversion

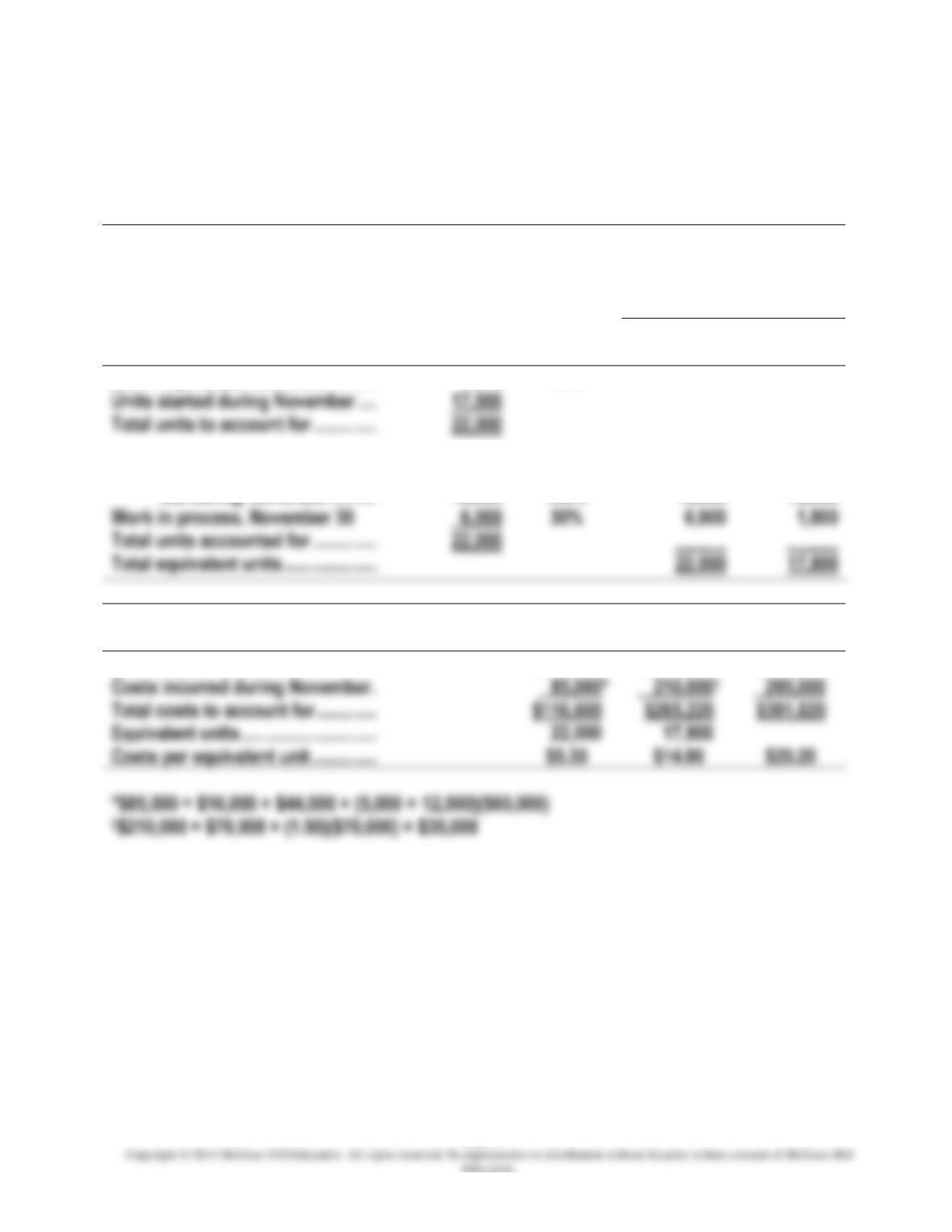

Work in process, November 1 …….

5,000

70%

Units started during November ….

17,000

Total units to account for …………..

22,000

Units completed and transferred

out during November ……….

16,000

100%

16,000

16,000

Work in process, November 30

30%

Total units accounted for …………..

22,000

____ _

_ ____

Direct

Material

Conversion

Total

Work in process, November 1 …….

$ 31,600

$ 55,220

$ 86,820

Costs incurred during November .

Total costs to account for ………….

$381,820

Equivalent units ………………………..

Costs per equivalent unit …………..

$5.30

*$85,000 = $16,000 + $44,000 + (5,000 ÷ 12,000)($60,000)