CHAPTER 4

Activity-Based Costing

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

*1. Discuss the difference

between traditional costing

and activity-based costing.

1, 2, 3, 4, 5

1, 2

1

1, 2, 3, 4, 5,

10, 11

1A, 3A,

4A, 5A

*2. Apply activity-based

costing to a manufacturer.

6, 7, 9, 10,

11, 12

3, 4, 5, 6, 7

2

1, 3, 4, 5, 6,

7, 8, 9, 10,

11

1A, 2A, 3A,

4A, 5A

*3. Explain the benefits and

limitations of activity-based

costing.

8, 13, 14, 15,

16, 17, 19

8, 9, 10, 11,

12

3

9, 10, 11, 12,

13, 16

1A, 5A

*4. Apply activity-based

costing to service

9, 12

4

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Assign overhead using traditional costing and ABC;

compute unit costs; classify activities as value- or

non-value-added.

Moderate

35–45

2A

Assign overhead to products using ABC and evaluate

decision.

Moderate

25–35

Assign overhead costs using traditional costing and ABC;

Moderate

35–45

5A

Assign overhead costs to services using traditional

Moderate

35–45

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

*1. Discuss the difference

between traditional costing and

activity-based costing.

Q4-1

Q4-2

Q4-3

Q4-4

Q4-5

DI4-1

BE4-1

BE4-2

E4-1

E4-2

E4–10

E4–11

P4–1A

E4-3

E4-4

E4-5

P4–3A

P4–4A

P4–5A

*2. Apply activity-based costing to

a manufacturer.

Q4-6

Q4-7

Q4-9

Q4–10

Q4–11

Q4–12

BE4-3

BE4-4

BE4-5

BE4-6

BE4-7

DI4-2

E4-1

E4-9

E4–10

E4–11

P4–1A

P4–2A

E4-3

E4-4

E4-5

E4-6

E4-7

E4-8

P4–3A

P4–4A

P4–5A

**3. Explain the benefits and

limitations of activity-based

costing.

Q4-8

Q4–13

Q4–14

A4–15

Q4–16

Q4–17

Q4–19

DI4-3

BE4-11

BE4-12

E4-9

E4–10

E4–11

P4–1A

BE4-8

BE4-9

BE4–10

E4–12

E4–13

E4–16

P4–5A

*4. Apply activity-based costing to

service industries.

Q4–18

BE4-12

DI4-4

E4–14

E4–15

E4–17

BE4-9

P4–5A

*5. Explain just-in-time (JIT)

processing.

Q4–20

Broadening Your Perspective

BYP4-2

BYP4-3

BYP4-6

BYP4-1

BYP4-4

BYP4-7

BYP4-2

BYP4-5

ANSWERS TO QUESTIONS

1. Direct labor is a valid basis for allocating overhead when: (a) direct labor constitutes a significant

part of total product cost, and (b) there is a high correlation between direct labor and changes in

the amount of overhead costs.

2. The amount of direct labor in many industries has greatly decreased, due to advances in

computerized systems, technological innovation, global competition and automation.

3. In many automated manufacturing environments, machine hours is a more relevant basis on

which to allocate overhead.

4. Under a traditional volume-based costing system where overhead cost is allocated on the basis

of units of output, the high-volume product will undoubtedly absorb more overhead than the low-

volume product.

5. The principal differences are:

7. The four steps involved in developing an ABC system are:

1. Identify and classify the major activities involved in the manufacture of specific products, and

allocate manufacturing overhead costs to appropriate cost pools.

2. Identify the cost driver that has a strong correlation to the costs accumulated in the cost pool.

3. Compute the overhead rate for each cost driver.

4. Assign manufacturing overhead costs for each cost pool to products, using the overhead

rates (cost per driver).

Questions Chapter 4 (Continued)

11. A cost driver is accurate and appropriate if it measures the actual consumption of the activity in

manufacturing a product or rendering a service and the data relating to the cost driver is available

and easily obtained.

12. The formula for assigning activity cost pools to products is:

Activity-based overhead rate X Expected use of cost drivers per product

13. The primary benefit of ABC is more accurate product costing. This results from using more cost

pools and enhanced control over overhead costs, and leads to better management decisions.

16. Basic ABC has been enhanced by identifying activities as value-added and non-value-added.

17. Identifying non-value-added activities highlights for managers the activities that should be

reduced or eliminated because they are not essential and they add no value to the product.

18. The overall objective of ABC in service firms is no different than for manufacturing companies;

that is, improved costing of services rendered (by job, service, contract, or customer). The

general approach to costing is the same—analyze operations, identify activities, assign overhead

costs to activity cost pools, and identify and use cost drivers to assign the cost pools to the

services.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 4-1

(a)

Estimated annual overhead costs

= Predetermined overhead rate

Expected annual operating activity

(b)

92,000 direct labor hours X $9.75 = $897,000 overhead applied

BRIEF EXERCISE 4-2

Under ABC, overhead costs are shifted from the high-volume products to

the low-volume products. This shift results in more accurate costing for

two reasons:

1. Low-volume products often require more special handling, such

as more machine setups and inspections, than high-volume

As a result, for Finney, one of the products (Product RX3) may have been low

volume and therefore may have more overhead costs assigned to it under

an ABC system.

= $9.75 per direct labor hour

BRIEF EXERCISE 4-3

An appropriate cost driver for each activity is:

Activity

Cost Driver

Materials handling

Machine setups

Factory machine maintenance

Factory supervision

Quality control

Number of requisitions

Number of setups

Machine hours used

Number of employees

Number of inspections

BRIEF EXERCISE 4-4

(a) Number of parts or assemblies

(b) Number of setups

(c) Number of employees

BRIEF EXERCISE 4-5

Machining

$375,000 ÷ 25,000 = $15 per machine hour

$ 87,500 ÷ 1,750 = $50 per inspection

Machine setups

$150,000 ÷ 2,500 = $60 per setup

BRIEF EXERCISE 4-6

Activity Cost Pool

Estimated

Overhead

÷

Expected Use of

Cost Drivers per Activity

=

Activity-Based

Overhead Rates

Wrapping and packing

Designing

Sizing and cutting

$ 450,000

4,000,000

10,000 designer hours

160,000 machine hours

$45.00 per designer hour

$25.00 per machine hour

BRIEF EXERCISE 4-7

Activity Cost Pool

Estimated

Overhead

÷

Expected Use of

Cost Drivers per Activity

=

Activity-Based

Overhead Rates

Ordering and receiving

$ 84,000

12,000 orders

$7.00 per order

Cost Drivers

X

Overhead

Rates

=

Total Overhead

Applied

11,000 orders

$7.00

$ 77,000

BRIEF EXERCISE 4-8

Value-added

(a)

(b)

(c)

Non-value-added

Value-added

Non-value-added

BRIEF EXERCISE 4-9

Value-added Activities

Hours

(1)

Designing and drafting

3.0

Non-value-added Activities

Hours

(2)

Staff meetings

1

BRIEF EXERCISE 4-10

(a) Batch- or unit-level

(b) Unit-level

(c) Unit-level

(d) Batch- or unit-level

BRIEF EXERCISE 4-11

(a) Facility-level

(b) Unit-level

(c) Product-level

BRIEF EXERCISE 4-12

(a)

Initial concept formation

$40,000

= $2,000 per project change

20

= $2 per square foot

Construction oversight

= $1,000 per month

(b)

Initial concept formation—product-level

Design—unit-level

Construction oversight—batch-level

SOLUTIONS TO DO IT! REVIEW EXERCISES

DO IT! 4-1

(a) True

(b) False

DO IT! 4-2

(a) Computations of activity-based overhead rates per cost driver:

Activity Cost

Pools

Estimated

Overhead

Expected Use of Cost

Drivers per Activity

Activity-Based

Overhead Rates

5,000 machine hours

30,000

500 orders

(b) Assignment of each activity’s overhead cost to products using ABC:

BC113

AD908

Expected

Use of Cost

Expected Use of

Activity-Based

(c) Computation of overhead cost per unit:

BC113

AD908

Total costs assigned

(a)

$41,000

$115,000

Total units produced

(b)

DO IT! 4-2 (Continued)

(d) These computations show that the total overhead assigned to Product

AD908 is more than two and a half times that assigned to BC113. On a

DO IT! 4-3

(a) unit-level

(b) product-level

DO IT! 4-4

(a) The activity based overhead rates would be:

Estimated

Overhead

Expected Use of

Cost Driver

Per Activity

Activity-Based

Overhead Rate

=

Loading and

unloading

$ 90,000

90,000

$1.00 per piece

Travel

$450,000

$0.75 per mile

Logistics

$ 75,000

3,000

$25 per hour

SOLUTIONS TO EXERCISES

EXERCISE 4-1

(a)

Estimated overhead

= Predetermined overhead rate

Direct labor costs

(b)

Activity cost pools

Cost drivers

Estimated overhead

Machining

Machine hours

$140,000

Machine setup

Set up hours

100,000

Activity-based overhead rates

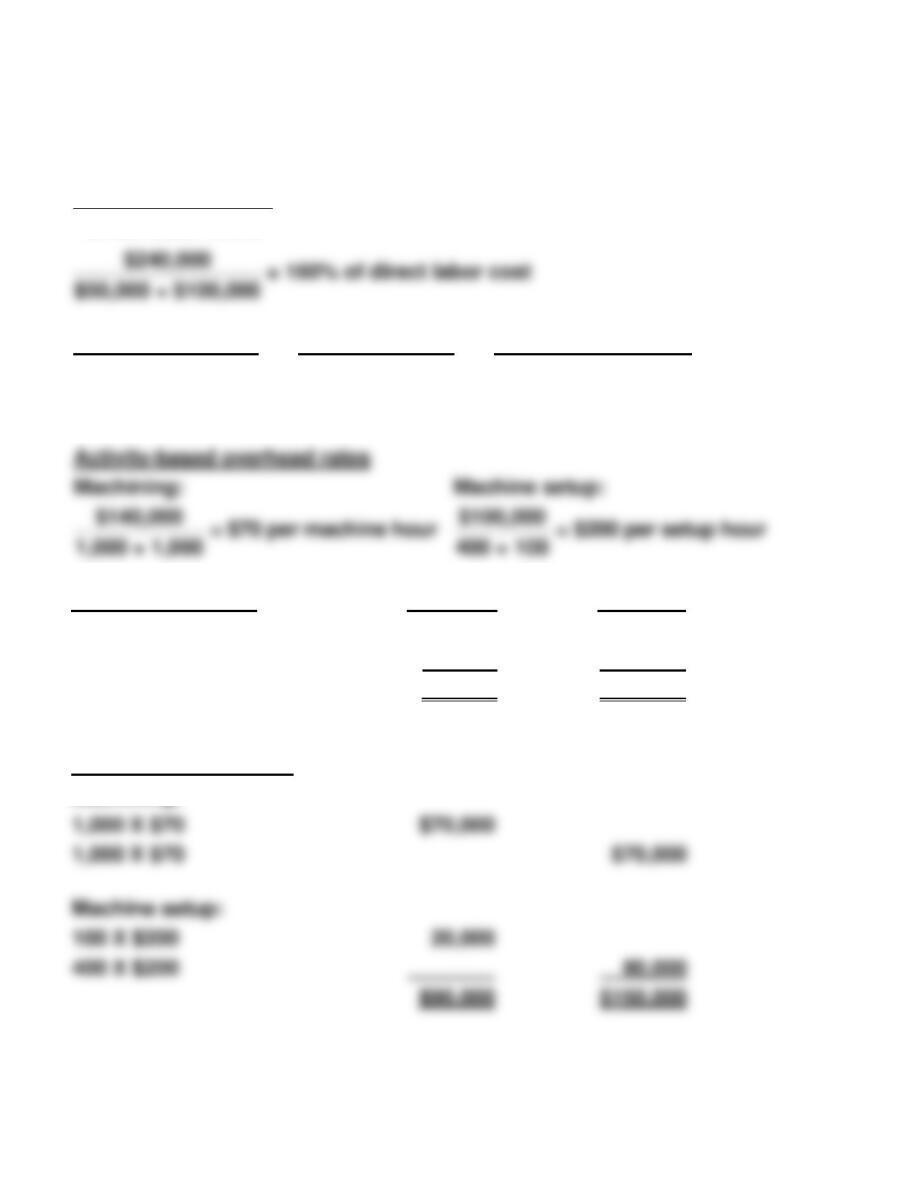

Machining:

Machine setup:

(c)

Traditional costing

Standard

Custom

$50,000 X 160%

$80,000

$100,000 X 160%

$160,000

$80,000

$160,000

Activity-based costing

Machining:

1,000 X $70

1,000 X $70

Machine setup:

100 X $200

400 X $200

$50,000 + $100,000

EXERCISE 4-2

(a)

Traditional costing system

Product 540X

Product 137Y

Product 249S

Sales

$180,000

$160,000

$70,000

(b)

Activity-based costing system

Product 540X

Product 137Y

Product 249S

Sales

$180,000

$160,000

$70,000

(c)

Product 540X:

($130,000 – $125,000) ÷ $125,000 = 4.00%

Product 137Y

($125,000 – $110,000) ÷ $110,000 = 13.64%

(d)

These costs are similar probably because the cost drivers are

EXERCISE 4-3

(a)

Activity cost pools

Cost drivers

Estimated overhead

Cutting

Machine hours

$360,000

Design

Number of setups

585,000

(b)

Estimated overhead

=

$945,000

= $2.10 per direct labor hour

Direct labors hours

450,000

Wool

Cotton

Traditional costing

The wool product line is allocated $97,500 ($570,000 – $472,500) more

overhead cost when an activity-based costing system is used. As a result,

the cotton product line is allocated $97,500 ($472,500 – $375,000) less.

Activity-based costing

Cutting

Design

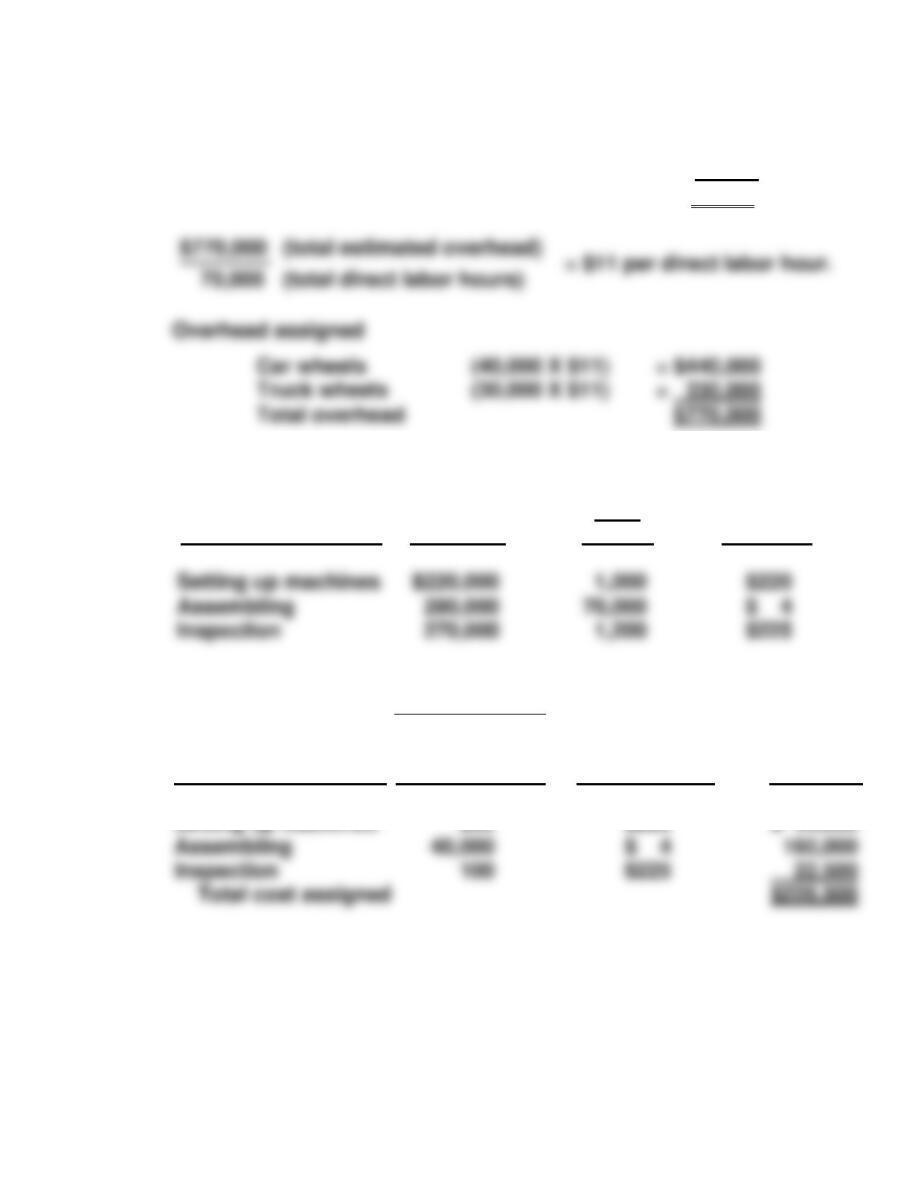

EXERCISE 4-4

(a)

Direct labor hours for car wheels

(40,000 X 1)

= 40,000

Direct labor hours for truck wheels

(10,000 X 3)

= 30,000

Total direct labor hours

70,000

(b)

Activity Cost Pool

Estimated

Overhead

÷

Expected

Use of

Cost

Drivers

=

ABC

Overhead

Rate

Assembling

(c)

Car Wheels

Activity Cost Pools

Expected Use

of Cost Driver

per Product

X

Activity-Based

Overhead

Rates

=

Cost

Assigned

Total overhead

EXERCISE 4-4 (Continued)

(c)

Truck Wheels

Activity Cost Pools

Expected use

of Cost Driver

per Product

X

Activity-

Based

Overhead

Rates

=

Cost

Assigned

Setting up machines

800

$220

$176,000

(d) Assuming that the cost drivers are a reasonable representation of

what is occurring in the two product lines, it seems appropriate to

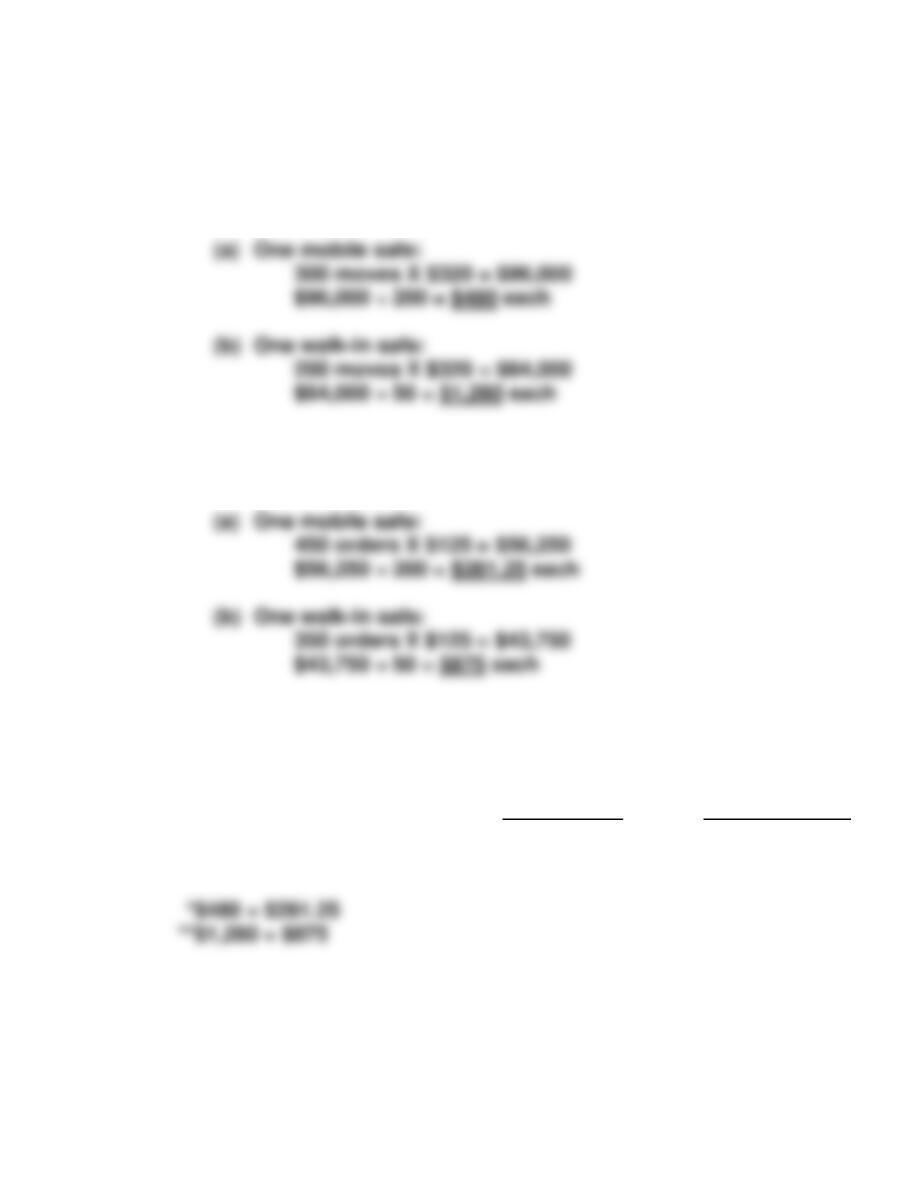

EXERCISE 4-5

(a) Traditional costing:

$260,000 ÷ 2,500 (800 + 1,700) hours

= $104 per direct labor hour

EXERCISE 4-5 (Continued)

(b) Activity-based costing:

(1) Material handling costs

$160,000 ÷ 500 (300 + 200) moves = $320 per move

(2) Purchasing activity costs

$100,000 ÷ 800 (450 + 350) orders = $125 per order

(c) The total amount of overhead allocated to each unit of the two products

under the two allocation approaches is:

Traditional

Costing

Activity-Based

Costing

Mobile safe

Walk-in safe

$ 416

$3,536

** $761.25**

$ 2,155**

EXERCISE 4-6

Budgeted Costs

Activity Cost Pool

Cost Driver

Engineering design

Engineering prototypes

Engineering

Engineering hours

Machine hours

EXERCISE 4-7

The following cost drivers might be used to assign overhead:

Gallons of juice

1.

2.

3.

Labor hours

Labor hours

Labor hours

9.

10.

11.

Gallons of wine or months of aging

Number of bottles

Number of bottles

Depreciation, machinery

Electricity, machinery

Machinery

Machine hours

Electricity, plant lighting

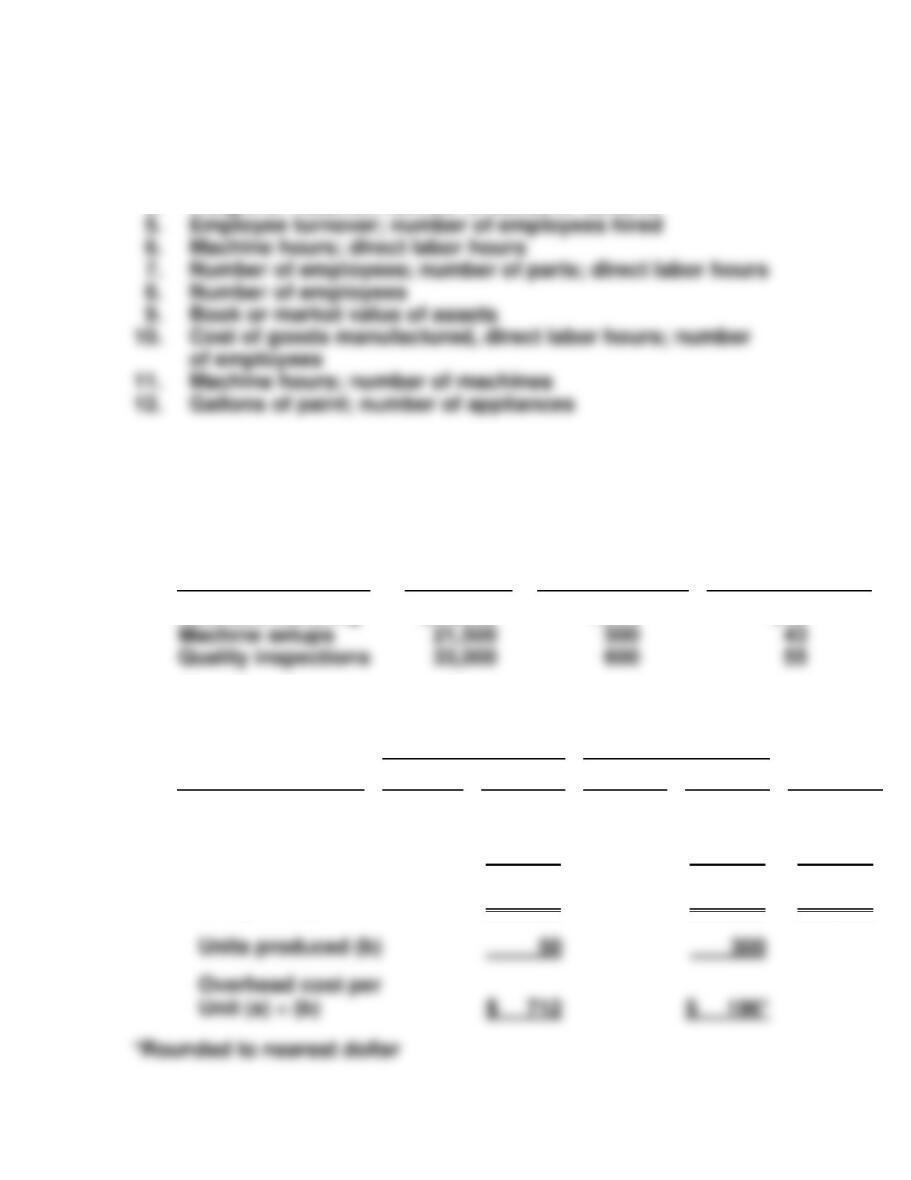

EXERCISE 4-8

1. Number of engineering change orders; hours of designing

2. Number of orders processed

3. Number of parts in stock

4. Weight of material; number of boxes or cartons

EXERCISE 4-9

(a) The overhead rates are:

Activity Cost Pools

Estimated

Overhead

÷

Expected Use

of Cost Drivers

per Activity

=

Activity-Based

Overhead Rates

Machine setups

Materials handling

$40,000

1,000

$40

(b) The assignment of the overhead costs to products is as follows:

Instruments

Gauges

Cost

Assigned

Cost Driver

Number

Cost

Number

Cost

Requisitions ($40)

Machine setups ($43)

Inspections ($55)

Total costs

assigned (a)

400

200

200

$16,000

8,600

11,000

$35,600

600

300

400

$24,000

12,900

22,000

$58,900

$40,000

21,500

33,000

$94,500

EXERCISE 4-9 (Continued)

(c) MEMO

To: President, Air United, Inc.

From: Student

Re: Benefits of activity-based costing (ABC)

ABC focuses on the activities performed in producing a product.

Overhead costs are assigned to products based on cost drivers that

measure the activities performed on the product.

EXERCISE 4-10

(a) (1) Traditional product costing system:

(2) Activity-based costing system:

Activity Cost Pools

Cost Drivers

Used

X

Activity-

Based

Overhead

Rates

=

Overhead Cost

Assigned

Credit and collection

Sales commissions

Advertising—TV

$900,000

250

$.05

$300

$ 45,000

75,000

(b) As compared to ABC, traditional costing grossly undercosts the selling

EXERCISE 4-11

(a) 1. Traditional product costing system:

2. Activity-based costing system:

Activity Cost Pools

Cost Drivers

Used

X

Activity-

Based

Overhead

Rate

=

Overhead Cost

Assigned

Inspections of material received

6,000

$ .90

$ 5,400

(b) As compared to ABC, the traditional costing system undercosts the

quality-control overhead cost assigned to the low-calorie breakfast line

(c) All three activities, as quality-control related activities, are non-value-

added activities.

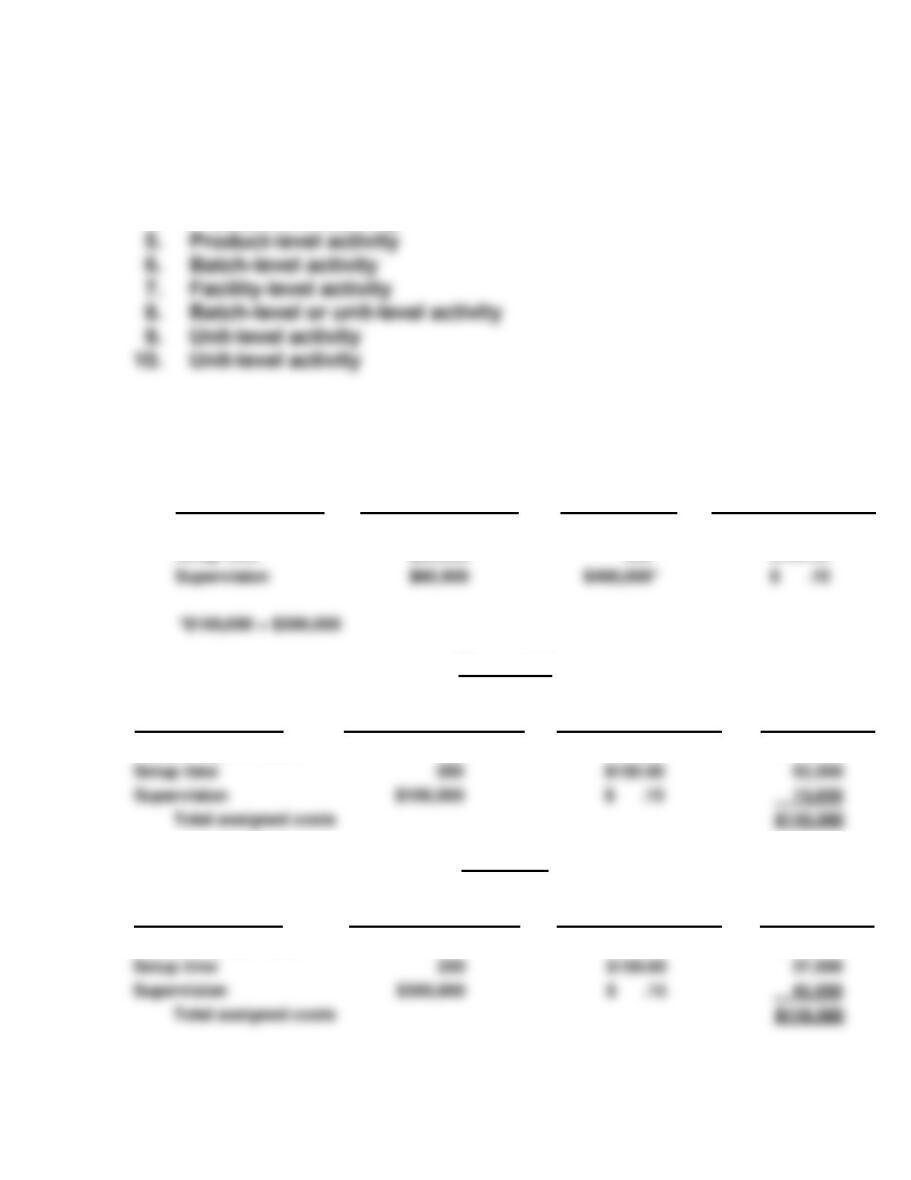

EXERCISE 4-12

Activity Cost Pools

Activity Level

Facility-level

Engineering

Machinery

Machine setup

Product-level

Unit-level

Batch-level

EXERCISE 4-13

1. Facility-level activity

2. Product-level activity

3. Batch-level activity

4. Product-level activity

EXERCISE 4-14

(a)

Activity Cost Pools

Estimated Overhead

÷

Expected use

of Cost Drivers

=

ABC Overhead Rates

Scheduling and travel

$85,000

1,250

$ 68.00

Setup time

$90,000

600

$150.00

$60,000

Commercial

Activity Cost Pools

Expected use of Cost

Drivers per Product

X

ABC Overhead Rates

=

Cost Assigned

Scheduling and travel

750

$ 68.00

$ 51,000

Setup time

$ .15

15,000

Total assigned costs

Residential

Activity Cost Pools

Expected use of Cost

Drivers per Product

X

ABC Overhead Rates

=

Cost Assigned

Scheduling and travel

500

$ 68.00

$ 34,000

Setup time

250

Total assigned costs

EXERCISE 4-14 (Continued)

(b)

Commercial

Residential

Revenues

$300,000

$480,000

Direct material costs

$ 30,000

$ 50,000

(c) Assuming that the cost drivers are a reasonable representation of

what is occurring in the two product lines, it seems appropriate to

EXERCISE 4-15

The following activities might be identified at Snap Prints Company from

your analysis of its operations and a discussion with the owner-manager,

Terry Morton.

1. Hiring and training personnel

2. Purchasing supplies and materials

Operating income (loss)

EXERCISE 4-16

Value-Added Activities

Hours

Writing contracts and letters

Taking depositions

1.5

1.0

Non-Value-Added Activities

Hours

Attending staff meetings

Doing research

0.5

1.0

Questionable Classifications

Writing contracts is value-added; writing letters may be value-added if

related to a specific case or it may be non-value-added if it is billing a client

EXERCISE 4-17

(a) The predetermined overhead rate under traditional costing would be:

(b) The amount of overhead allocated to the average residential job

would be:

(c) The activity-based overhead rates for each cost pool would be

Activity Cost Pools

Estimated Overhead

Expected Use of Cost

Drivers per Activity

Activity Based

Overhead Rate

Plowing

$0.19 per square yard

Snowthrowing

$0.08 per linear foot

(d) The amount of overhead allocated to the average residential job under

activity based costing would be:

Expected use of

Cost Driver Per Job

Activity Based

Overhead Rate

=

Cost

Allocated

Plowing

Snowthrowing

(e) The amount of overhead allocated to the average residential job under

traditional costing is $14, versus $8.60 under ABC. This means that

SOLUTIONS TO PROBLEMS

PROBLEM 4-1A

(a) Computation of unit costs—traditional costing.

Products

Manufacturing Costs

Home Model

Commercial Model

(b)

Activity Cost Pool

Estimated

Overhead

÷

Expected

Use of Cost Drivers

=

Activity-Based

Overhead Rate

Receiving

Forming

$ 80,400

150,500

335,000 Pounds

35,000 Machine hours

$ .24 per pound

$ 4.30 per machine hour

(c)

Home Model

Commercial Model

Activity Cost Pool

Expected

Use of

Drivers

X

Activity-

Based

Overhead

Rates

=

Cost

Assigned

Expected

Use of

Drivers

X

Activity-

Based

Overhead

Rates

=

Cost

Assigned

Receiving

Forming

215,000

27,000

$ .24

$ 4.30

$ 51,600

116,100

120,000

8,000

$ .24

$ 4.30

$ 28,800

34,400

Total unit cost

PROBLEM 4-1A (Continued)

(d)

ABC Manufacturing Costs

Home Model

Commercial Model

Direct materials

$18.50

$26.50

(e)

Activity

Value- vs. Non-Value-Added

Assembling

Packing and shipping

Receiving

Forming

Non-value-added

Value-added

(f) (1) Activity-based costing shows the commercial model absorbs

(2) The comparison of ABC and traditional costing shows that the

proper amount of overhead assigned to the two products is not

Total cost per unit

PROBLEM 4-2A

(a) The allocation of total manufacturing overhead using activity-based

costing is as follows:

Royale

Majestic

Overhead Rate

Drivers

Used

Cost

Assigned

Drivers

Used

Cost

Assigned

Total

Overhead

Purchase orders @ $30

17,000

$ 510,000

23,000

$ 690,000

$1,200,000

(b) The cost per unit and gross profit of each model under ABC costing

were:

Royale

Majestic

Direct materials

$ 700.00

$ 420.00

(c) Management’s future plans for the two television models are not

sound. Under ABC costing, the Royale model is $195.10 ($618.60 –

$423.50) per unit more profitable than the Majestic model. If any

PROBLEM 4-3A

(a) Predetermined overhead rate using machine hours:

(b) Manufacturing cost per stairway under traditional costing:

Direct materials ……………………………………………………… $ 103,600

Direct labor ……………………………………………………………. 112,000

(c) Manufacturing cost per stairway under activity-based costing:

Computation of Activity-Based Overhead Rates

Activity Cost Pools

Estimated

Overhead

÷

Expected Use of Cost

Drivers per Activity

=

Activity-Based

Overhead Rate

180,000

Purchasing

Handling materials

Production

$ 75,000

82,000

210,000

600 Orders

8,000 Moves

100,000 D/L Hours

$125 per order

$10.25 per move

$2.10 per D/L hour

Activity Cost Pools

Expected Use of

Cost Drivers

X

Activity-Based

Overhead Rates

=

Cost Assigned

8,000 Sq. ft.

Purchasing

Handling materials

60 Orders

800 Moves

$125

$10.25

$ 7,500

8,200

PROBLEM 4-3A (Continued)

Total manufacturing cost per stairway under ABC:

Direct materials ……………………………………………………………. $ 103,600

(d) The difference between the traditional cost and the activity–based cost

per unit, $1,365.84 versus $1,139.80, is not great in amount but $226.04

($1,365.84 – $1,139.80) is 19.8% of the more correct ABC cost per

PROBLEM 4-4A

(a) Computation of unit costs—traditional costing

Overhead cost per direct labor hour is $1,241,660 ÷ (150,000 + 27,000) =

$7.015

Products

Manufacturing Costs

CoolDay

LiteMist

Direct materials

$0.400

$1.200

(b)

Activity Cost Pools

Estimated

Overhead

÷

Expected Use

of Cost Drivers

=

Activity-Based

Overhead Rates

equipment

Grape processing

Aging

$ 145,860

396,000

6,600

6,600,000

$22.10 per cart

$ 0.06 per month

(c)

CoolDay

LiteMist

Activity Cost Pools

Expected

Use of

Cost

Drivers

X

Activity-

Based

Overhead

Rates

=

Cost

Assigned

Expected

Use of

Cost

Drivers

X

Activity-

Based

Overhead

Rates

=

Cost

Assigned

Grape processing

6,000

$22.10

$132,600

600

$22.10

$ 13,260

PROBLEM 4-4A (Continued)

(d)

Products

Manufacturing Costs

CoolDay

LiteMist

Direct materials

$0.400

$1.200

(e) To: Mr. Jack Eller

From: Student

Subject: Product costs using traditional approach versus ABC

The memorandum covers the following points:

a. ABC allocates overhead costs as a function of each product’s use

of cost drivers. Thus, ABC results in overhead allocation that

more closely approximates each product’s generation of overhead

costs.

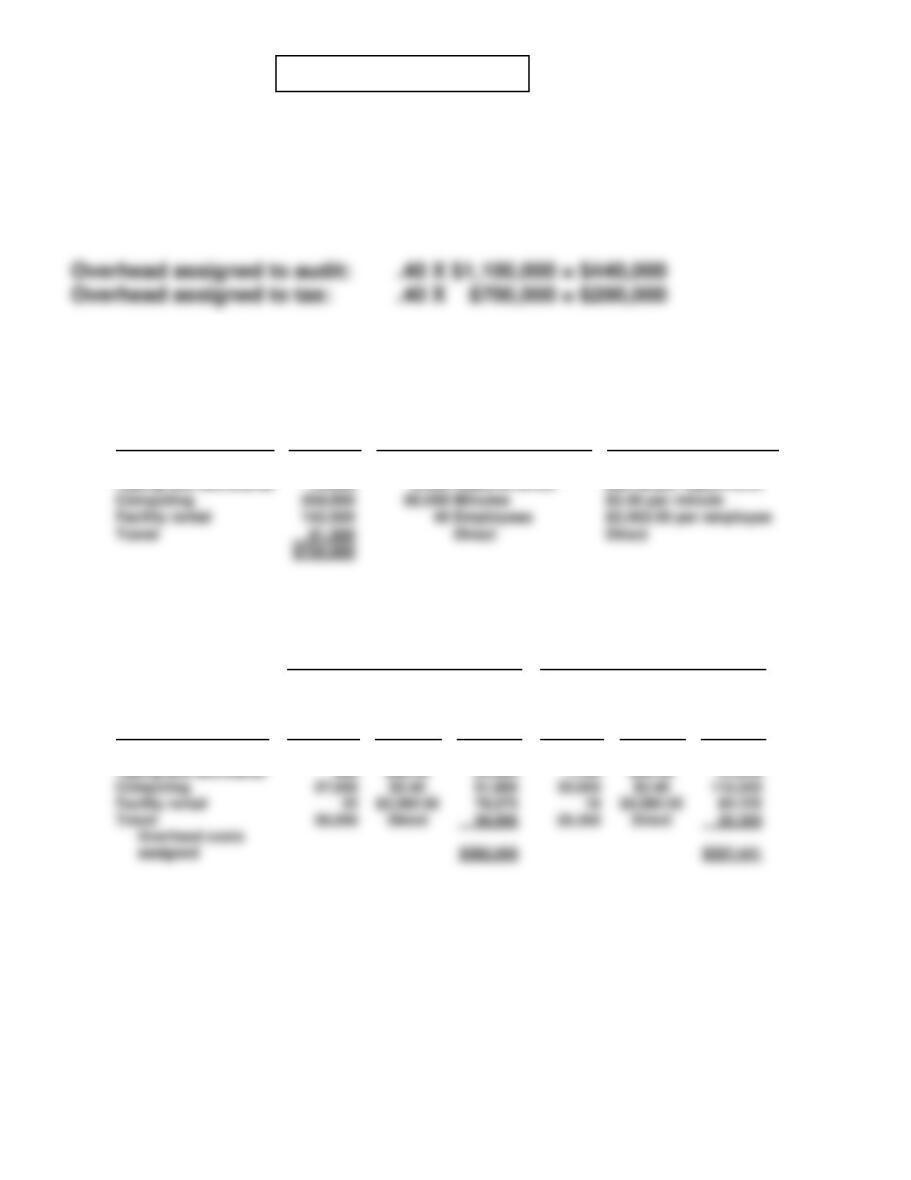

PROBLEM 4-5A

(a) Computation of assigned overhead under traditional costing (“direct

labor dollars” appears in the first line of the schedule of overhead data):

Predetermined overhead rate X direct labor dollars

(b) (1) Computation of activity-based overhead rates:

Activity Cost Pools

Estimated

Overhead

÷

Expected Use of

Cost Drivers per Activity

=

Activity-Based

Overhead Rates

Employee training

$216,000

$1,800,000 Direct labor dollars

$.12 per DL dollar

(2) Assignment of overhead to audit and tax services:

Audit

Tax

Activity Cost Pools

Expected

Use of

Cost

Driver

X

Activity-

Based

Overhead

Rate

=

Cost

Assigned

Expected

Use of

Cost

Driver

X

Activity-

Based

Overhead

Rate

=

Cost

Assigned

Employee training

$1,100,000

$.12

$132,000

$700,000

$.12

$ 84,000

PROBLEM 4-5A (Continued)

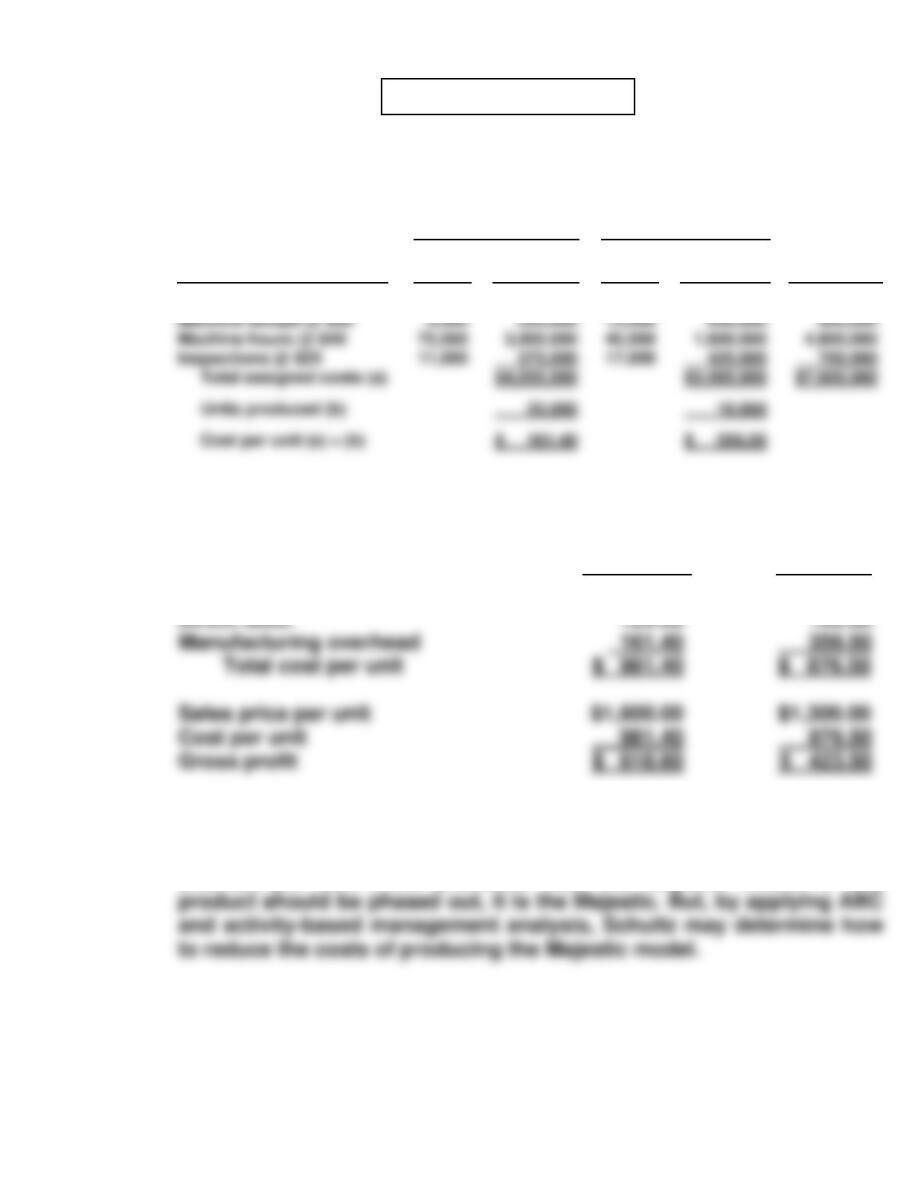

(c) Overhead is assigned to the two service lines as follows:

Audit

Tax

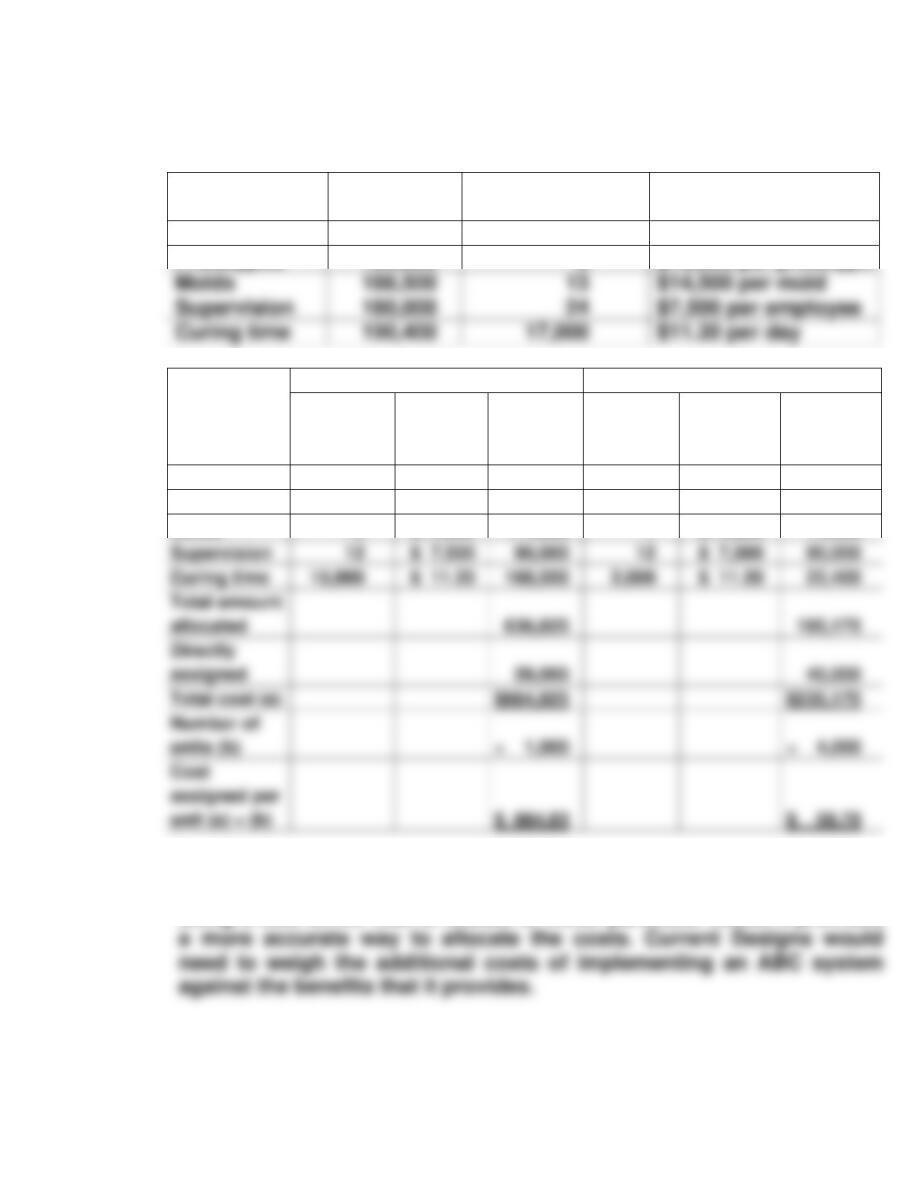

CD4 CURRENT DESIGNS

(a)

Composite

Rotomolded

Directly assigned

$ 28,000

$ 40,000

Remaining amount ($832,000) allocated

50% to each product line

$416,000

$416,000

(b)

Composite

Rotomolded

Directly assigned

$ 28,000

$ 40,000

Remaining amount ($832,000) allocated

based on direct labor costs

$374,400*

$457,600**

Total

$402,400

$497,600

Number of units

Cost assigned per unit

$ 402.40

$ 124.40

Total

Number of units

Cost assigned per unit

CD4 (Continued)

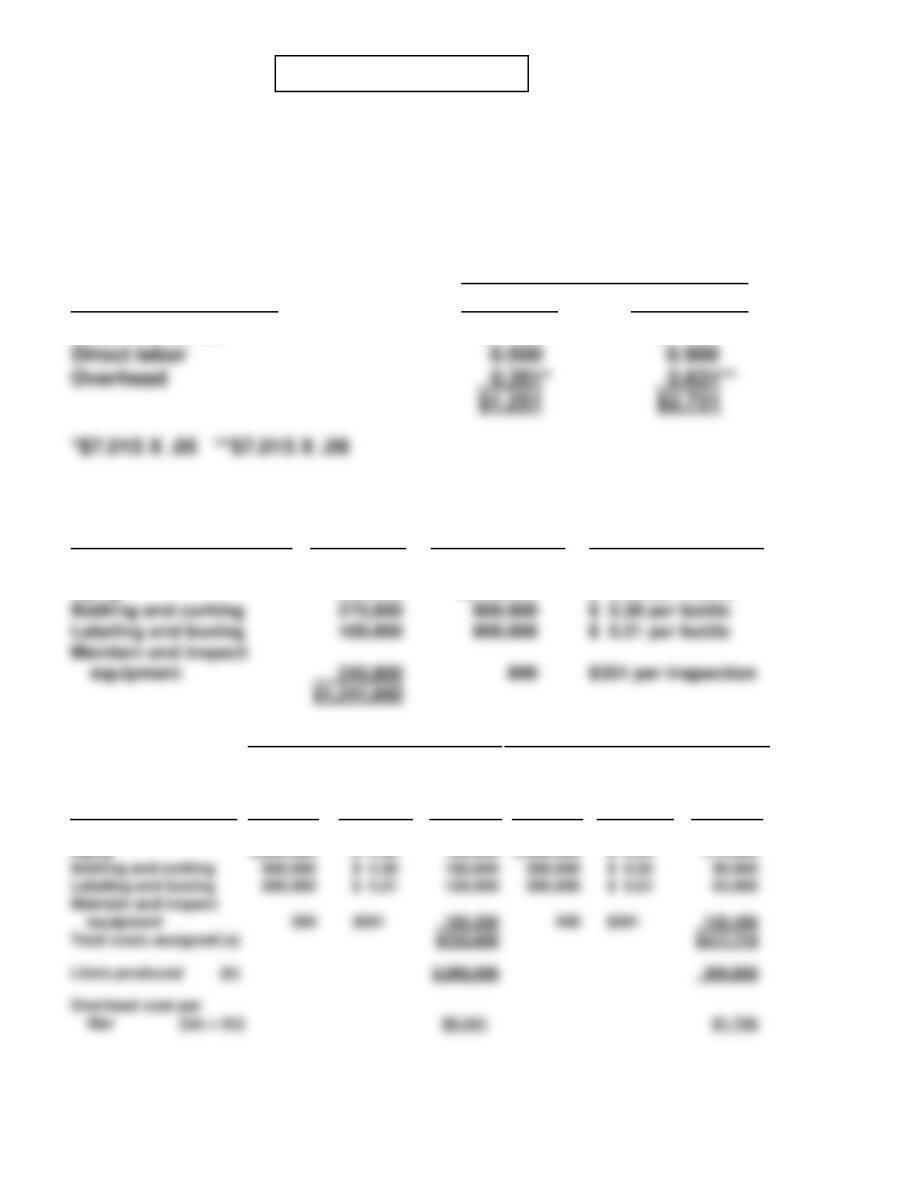

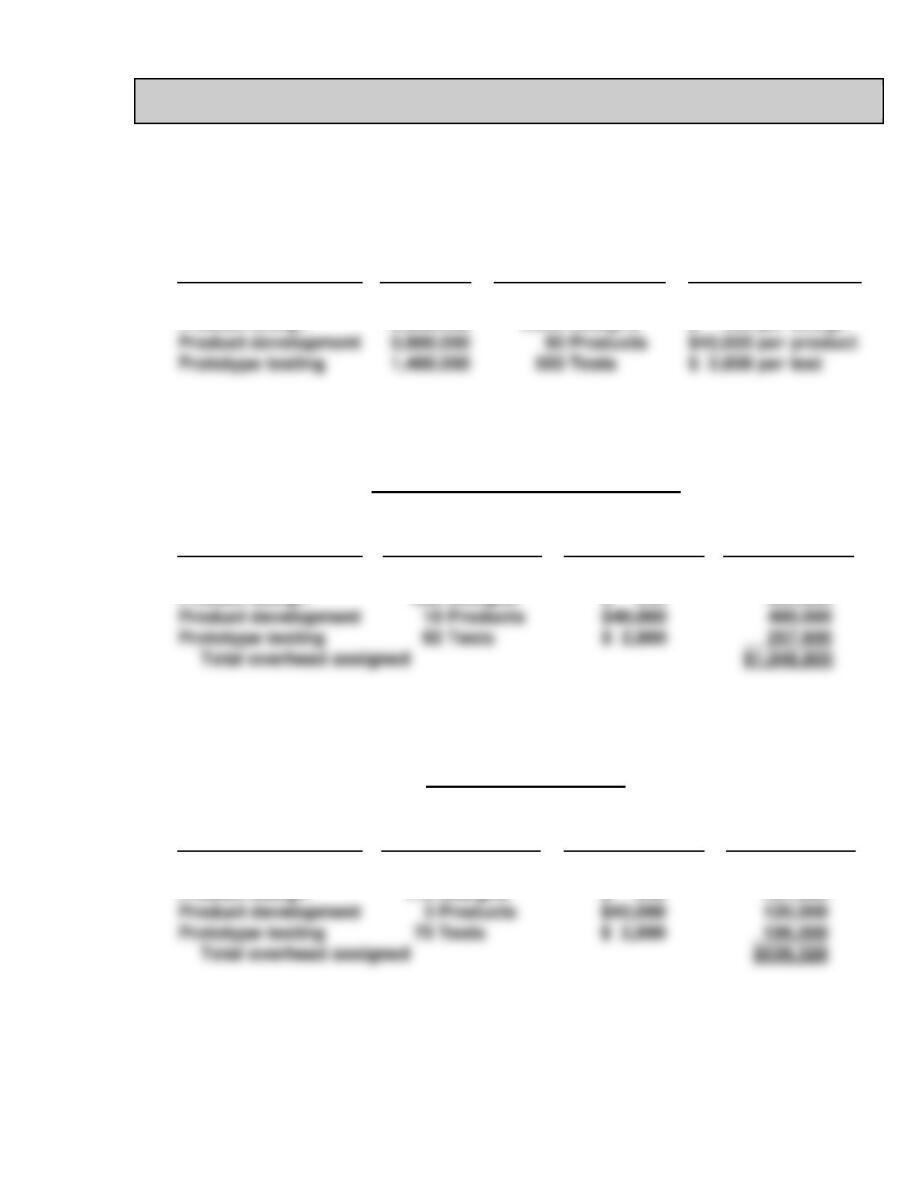

(c)

Activity Cost

Pools

Estimated

Overhead

Expected Use of

Cost Drivers

Activity-Based

Overhead Rates

Design

$121,100

4

$30,275 per model

Prototypes

152,000

8

$19,000 per prototype

Activity Cost

Pool

Composite

Rotomolded

Expected

Use of

Drivers

Overhead

Rates

Cost

Assigned

Expected

Use of

Drivers

Overhead

Rates

Cost

Assigned

Design

3

$30,275

$ 90,825

1

$30,275

$ 30,275

Prototypes

6

$19,000

114,000

2

$19,000

38,000

Molds

12

$14,500

174,000

1

$14,500

14,500

Supervision

90,000

90,000

168,000

22,400

allocated

195,175

assigned

28,000

40,000

$664,825

$235,175

÷ 1,000

÷ 4,000

(d) Activity-based costing assigns significantly more costs to the composite

kayaks. Since the cost is divided into pools and each pool is allocated

using a cost driver that is related to those particular costs, it provides

Molds

$14,500 per mold

Supervision

180,000

$7,500 per employee

Curing time

$11.20 per day

BYP 4-1 DECISION-MAKING ACROSS THE ORGANIZATION

The following activities and cost drivers might be submitted:

(a) Activities

(b) Cost Drivers

Laundering

Housekeeping

Dietary

Computing information

technology

Pounds of linen

Square footage; number of beds

Number of meals

Minutes of computer usage; or number of

work stations

BYP 4-2 MANAGERIAL ANALYSIS

(a) Computation of activity-based overhead rate:

Activity Cost Pools

Total

Estimated

Overhead

÷

Expected Use of

Cost Drivers

Per Activity

=

Activity-Based

Overhead Rates

Market analysis

Product design

$1,050,000

2,350,000

15,000 Hours

2,500 Designs

$ 70 per hour

$ 940 per design

(b) Charges to in-house manufacturing department:

In-House Manufacturing Department

Activity Cost Pools

Cost Drivers Used

X

Activity-Based

Overhead Rates

=

Cost Assigned

Market analysis

Product design

1,800 Hours

280 Designs

$ 70

$ 940

$ 126,000

263,200

(c) Charges to outside R & D contractor:

Outside Contract Costs

Activity Cost Pools

Cost Drivers Used

X

Activity-Based

Overhead Rates

=

Cost Assigned

$ 2,800

Market analysis

Product design

800 Hours

178 Designs

$ 70

$ 940

$ 56,000

167,320

BYP 4-2 (Continued)

(d) Activity-based costing permits the company to identify its R&D costs

by the activities that cause the costs; that is, ABC allows closer

scrutiny of the causes for cost incurrences; hence, greater control. By

BYP 4-3 REAL-WORLD FOCUS

(a) Some of the benefits of ABC for the financial services industry include:

Identification of the most profitable customers

More accurate product and service pricing

(b) Three things that the company’s original costing method did not take

into account were:

(1) The same servicing and administrative expenses were applied

equally to all accounts, including fixed and adjustable rate

(c) Some of the cost drivers used under the new approach were:

Average number of accounts that were at least 60 days delinquent.

BYP 4-4 REAL-WORLD FOCUS

(a) According to the authors, “ABC loses power in large-scale operations,

and can be difficult to implement and maintain.” They suggest, though,

that ABC should not be abandoned but, rather, improved because it

provides many potential benefits.

(b) One way to estimate practical capacity is to simply use a rule of thumb,

such as practical capacity is 80 to 85% of theoretical capacity. The

authors suggest that estimates for people be put at the lower end of

(c) After practical capacity is determined in terms of total time available,

the cost per unit of time is determined by dividing the total cost of that

capacity by the total capacity in units of time. This results in a cost per

BYP 4-4 (Continued)

(d) One of the primary benefits of the report provided by “ABC, the Time–

Driven Way” is that it highlights the difference between capacity

supplied and capacity used. This enables management to evaluate its

effectiveness in its use of the company’s resources and to evaluate

decisions regarding increasing or decreasing capacity.

BYP 4-5 ETHICS CASE

(a) The stakeholders (parties affected by Curtis’s and Ed’s actions) in this

case are:

• Curtis as cost accountant.

• Ed and all personnel employed in the production of the Supercut

Model of lawn tractor.

(b) The objective of cost accounting is to provide useful, accurate informa–

tion for decision making by managers. Ed is coercing Curtis to

(c) Curtis is a management accountant employed by Hi-Power Mower

Company. His first job responsibility is to his employer to: (1) communi-

BYP 4-6 ALL ABOUT YOU

(a) The three main tools for time management for students are:

Term calendar—records quizzes, exams, project due dates and other

major events.

(b) Studies show that students are most inclined to waste time during the

morning and afternoon. Your brain is best prepared for learning during

day-light hours. Therefore, it is important to schedule your time so that

you tackle your most difficult topics during daylight hours.

BYP 4-7 CONSIDERING YOUR COSTS AND BENEFITS

Discussion guide: In part, the response to this question depends on how

broadly you apply the term “value–added activity” when looking at one’s life.

For example, some value-added activities relate to goals and objectives for

school and work. It is important to try to manage your time effectively to

maximize your chance of achieving these objectives. But it is also important

to identify the other things in life that are important. These would include