Student Name:

Class:

Labor cost Wage rate Labor hours

Model per unit per hour per unit

Incremental profit (loss) on special order:

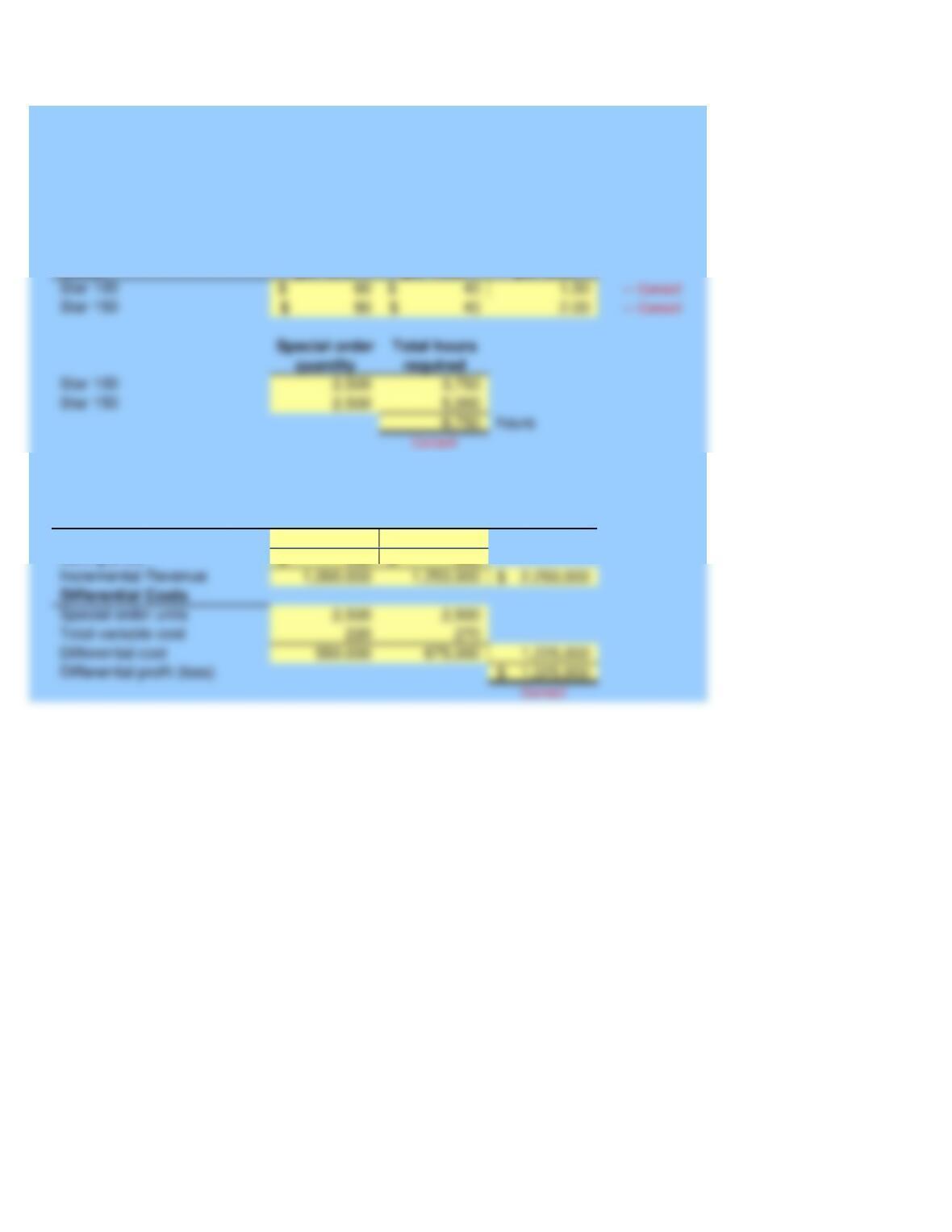

Star 100 Star 150 Total

Differential Costs

Total variable cost

Special order units

Incremental Revenue

Differential cost

Differential profit (loss)

2,500 2,500

400$ 500$

Differential Revenues

Special order units

Selling price

Problem 04-52

McGraw-Hill/Irwin

Instructor

Enter data in the shaded areas

Requirement a:

Labor hours required for special order:

UNTER COMPONENTS

Star 100

Star 150

Star 150

Labor hours

special order

Total

per unit quantity Hours

1.50 3,500 5,250.00

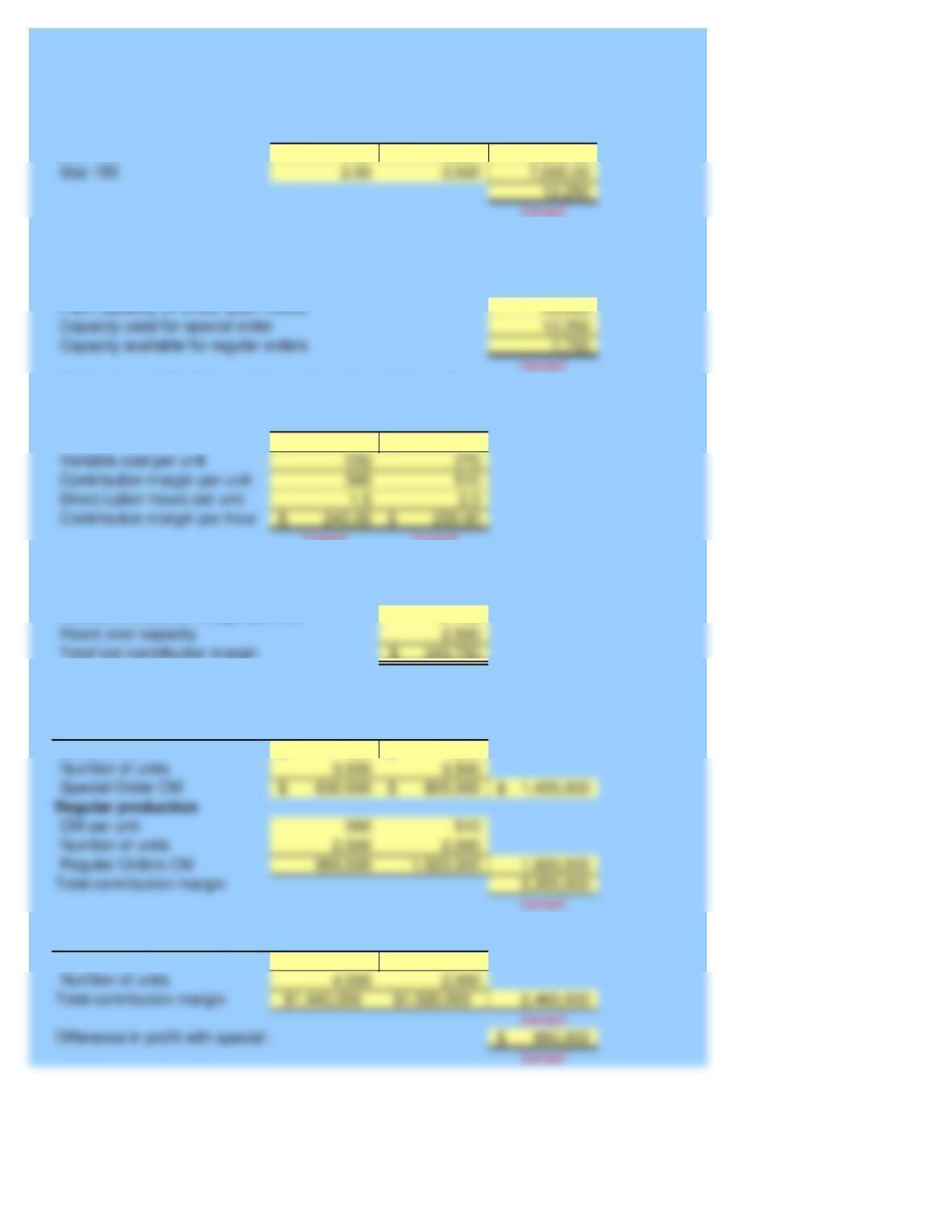

Capacity available for regular orders

Capacity used for special order

Plant capacity (in direct labor-hours)

Star 100 Star 150

Direct Labor-hours per unit

Contribution margin per hour

Contribution margin per unit

Variable cost per unit

580$ 780$

Hours over capacity

Total lost contribution margin

Correct! Correct!

137.50

343,750$

Star 100 Star 150

Regular production

Regular Orders CM

Number of units

CM per unit

Special Order CM

Number of units

180$ 230$

Star 100 Star 150

Number of units

$360 $510

Lowest contribution margin per hour

CM per unit

Regular production

Special Order

CM per unit

If labor hours for 3,500 units exceed capacity, production will need to

be reduced on the product with the lowest contribution margin.

Labor hours required for special order:

Requirement b.

Total contribution margin with the special order:

Compute contribution margin per hour for regular orders:

Compute contribution margin lost from regular sales:

Star 100

Revenue per unit

Star 150

Star 100 Star 150

180$ 230$

3,500 3,500

Special Order:

Compute the total contribution margin with the special order:

Requirement c.

Number of units

CM per unit

Additional variable overhead

Additional direct-labor costs

Regular production:

Total contribution margin

Total contribution margin

Incremental cost

Number of units

CM per unit

Star Star

100 150

130$ 150$

60 80

40$

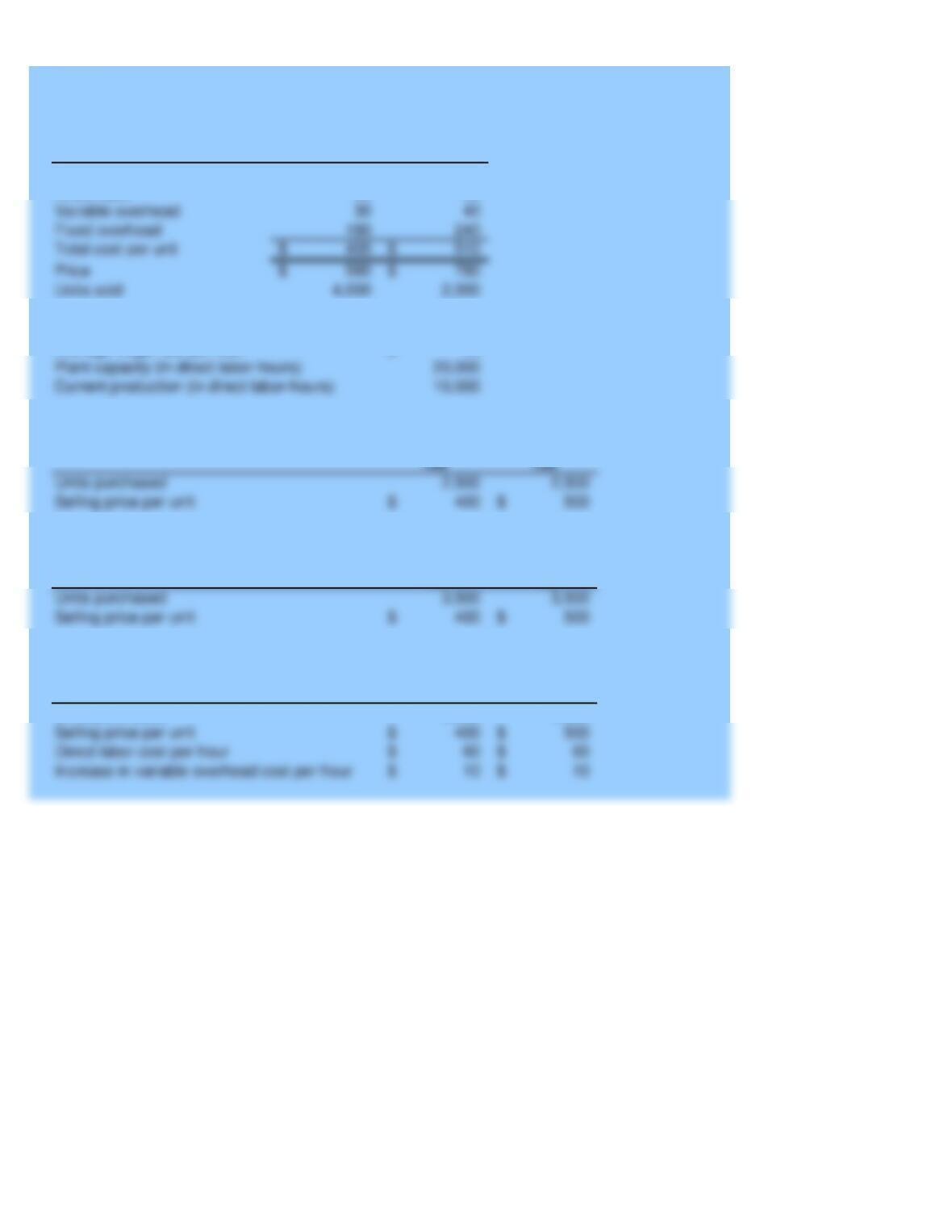

Current production (in direct labor-hours)

Plant capacity (in direct labor-hours)

Star Star

100 150

2,500 2,500

Units purchased

Selling price per unit

Star Star

100 150

3,500 3,500

Units purchased

Selling price per unit

Star Star

100 150

3,500 3,500

Increase in variable overhead cost per hour

Selling price per unit

Direct labor cost per hour

Direct materials

Direct labor

Given Data P04-52:

Units purchased

Requirement c. Information:

Requirement b. Information:

Requirement a. Information:

Additional Information: Variable overhead varies with quantity of direct labor-hours.

Costs per unit

UNTER COMPONENTS

Average wage rate per hour

Variable overhead

Fixed overhead

Units sold

Student Name:

Class:

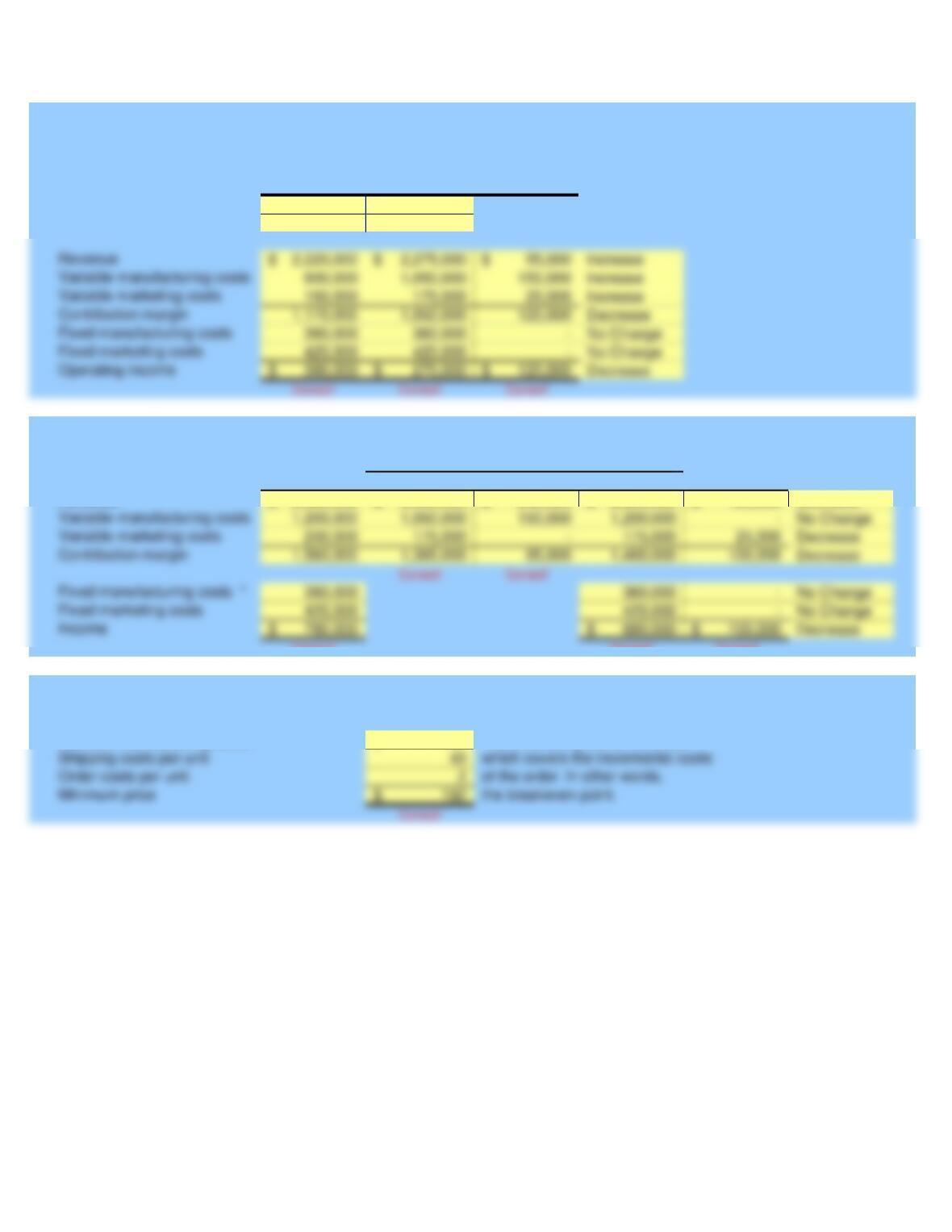

Before Price After Price

Reduction Reduction Impact

370$ 325$

6,000 7,000

Without

Government

Contract Regular Government Total Impact

Variable marketing costs

Contribution margin

Variable manufacturing costs

Fixed manufacturing costs *

Fixed marketing costs

Income

2,960,000$ 2,590,000$ 245,000$ 2,835,000$ 125,000$ Decrease

Shipping costs per unit

Order costs per unit

Minimum price

which covers the incremental costs

of the order. In other words,

the breakeven point.

Correct! Correct! Correct!

150$

Quantity

Requirement a.

Instructor

McGraw-Hill/Irwin

DAVIS KITCHEN SUPPLY

Problem 04-56

Sales price

Requirement b.

With Government Contract

Revenue

Compute minimum price:

Requirement c.

The minimum price is that price

Variable manufacturing costs

Revenue

Variable manufacturing costs

Operating income

Variable marketing costs

Contribution margin

Fixed manufacturing costs

Fixed marketing costs

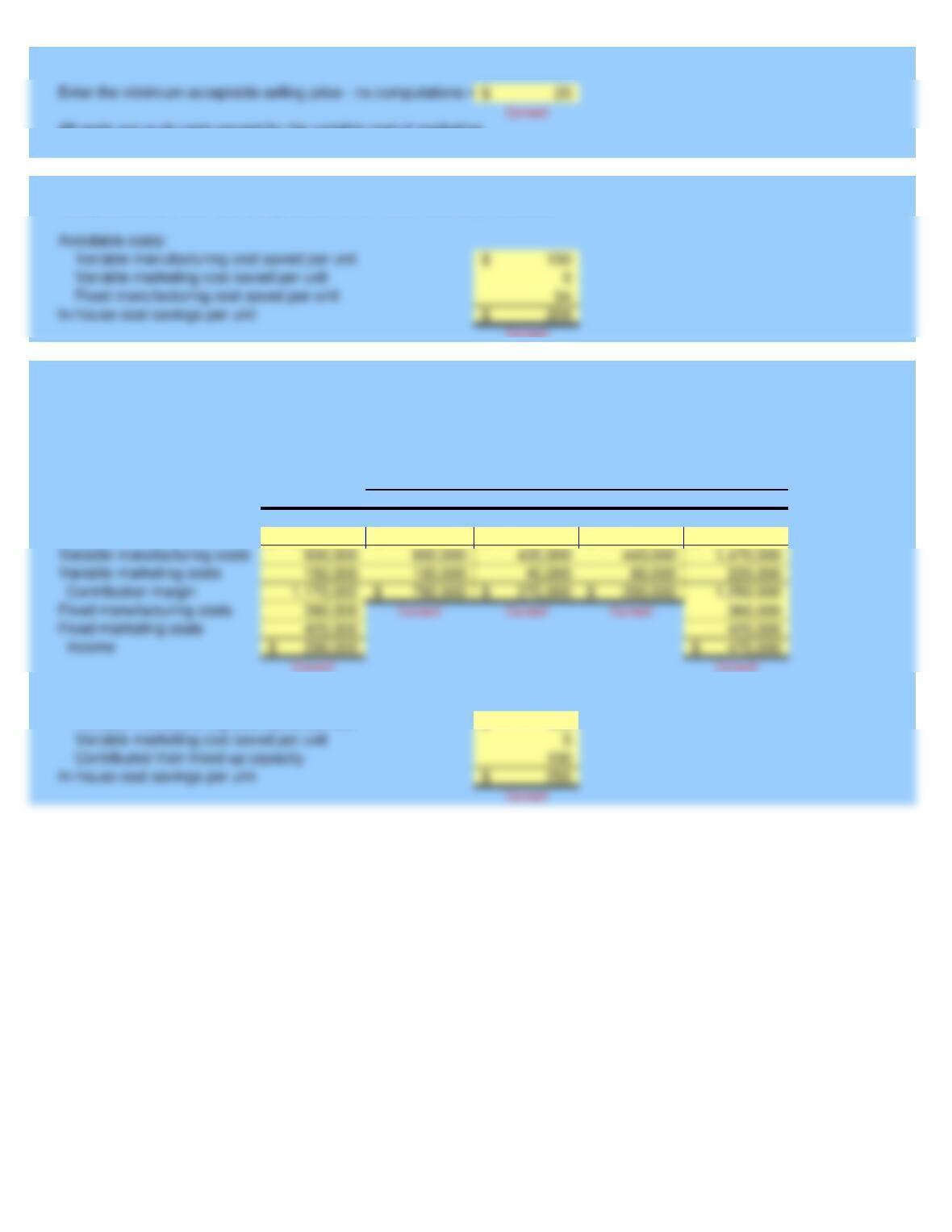

Enter the minimum acceptable selling price – no computations necessary

Correct!

6,000 regular

Stoves

Produced

In-house Regular (In)

Regular (Out)

Modified Total

Income

Variable manufacturing costs

Variable marketing costs

Contribution margin

Fixed manufacturing costs

Fixed marketing costs

2,220,000$ 1,480,000$ 740,000$ 720,000$ 2,940,000$

Variable marketing cost saved per unit

Contributed from freed-up capacity

In-house cost savings per unit

150$

Requirement d.

Contract 2,000 Regular Stoves

Computation of maximum price for outside contractor:

Requirement f.

Avoidable costs:

Variable manufacturing cost saved per unit

Revenue

All costs are sunk costs except for the variable cost of marketing.

Requirement e.

Computation of price that is equivalent to in-house cost of production:

Variable manufacturing cost saved per unit

Variable marketing cost saved per unit

Fixed manufacturing cost saved per unit

In-house cost savings per unit

Avoidable costs:

6,000

370$

7,000

325.00$

?

?

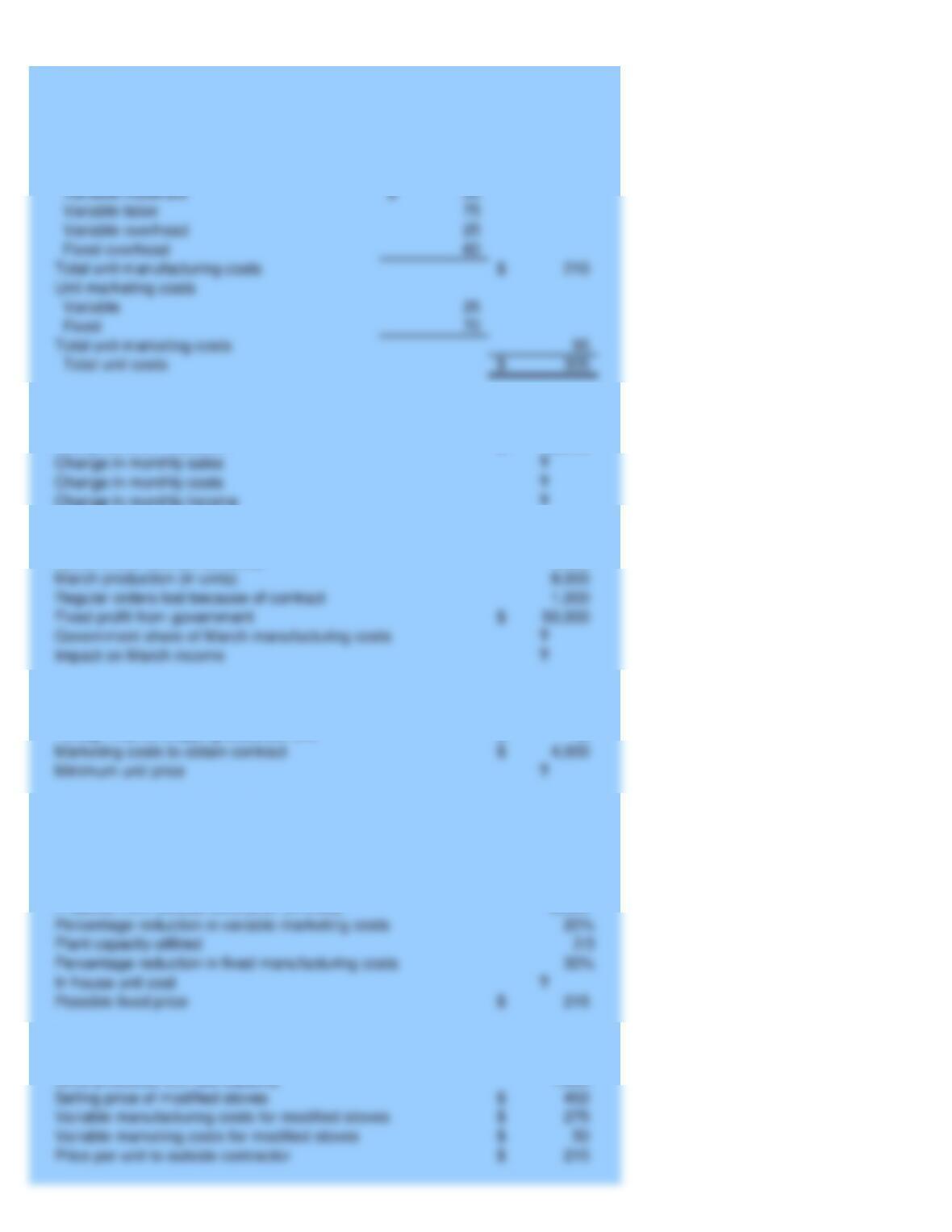

Change in monthly sales

Change in monthly costs

?

1,000

?

?

March production (in units)

Regular orders lost because of contract

Fixed profit from government

Government share of March manufacturing costs

Impact on March income

2,000

?

Marketing costs to obtain contract

Minimum unit price

40$

460

?

2,000

?

Percentage reduction in variable marketing costs

Plant capacity utilized

Percentage reduction in fixed manufacturing costs

In house unit cost

Possible fixed price

Selling price of modified stoves

Variable manufacturing costs for modified stoves

Variable marketing costs for modified stoves

Price per unit to outside contractor

1,600

Units manufactured per month

Unit manufacturing costs

New price after reduction

Regular selling price per unit

Requirement f. information:

Minimum acceptable selling price per unit

Requirement b. information:

Requirement c. information:

Requirement d. information:

Change in monthly income

Government contract (in units)

Foreign market order (in units)

Given Data P04-56:

Requirement a. information:

Increase in volume (in units)

DAVIS KITCHEN SUPPLY

Foreign market shipping costs per unit

Number of obsolete units in inventory

Requirement e. information:

Proposal from outside contractor (in units)

Use information from requirement e. plus:

Units produced with idle capacity

Variable materials

Variable overhead

Variable labor

Total unit marketing costs

Fixed

Variable

Unit marketing costs

Total unit manufacturing costs

Fixed overhead

Student Name:

Class:

Basic Classic Formal

600,000$ 640,000$ 5,700,000$

Correct!

Basic Classic Formal

60,000$ 116,000$ 570,000$

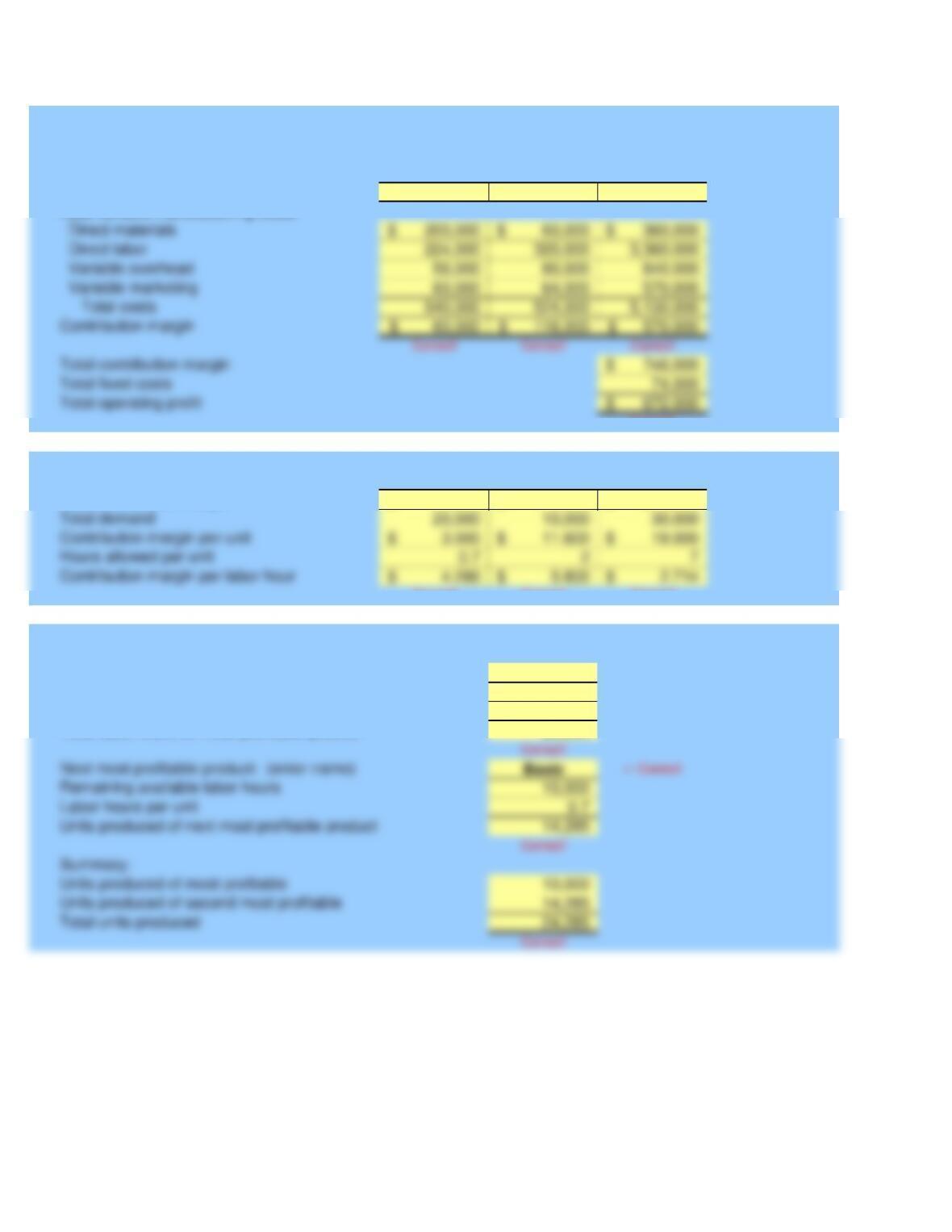

Total demand

Contribution margin per unit

Hours allowed per unit

Contribution margin per labor hour

Correct! Correct! Correct!

Classic «- Correct!

Next most profitable product: (enter name)

Remaining available labor hours

Labor hours per unit

Units produced of next most profitable product

Units produced of most profitable

Total units produced

10,000

2

20,000

AUSTIN ENTERPRISES

Problem 04-62

McGraw-Hill/Irwin

Instructor

Requirement c:

Requirement b:

Requirement a:

Total revenue

Less variable manufacturing costs:

Total contribution margin

Most profitable product per labor hour: (enter name):

Units produced to meet demand

Labor hours per unit

Total labor hours for most profitable product

60,000$ 116,000$ 570,000$

Direct materials

Direct labor

Variable overhead

Variable marketing

Total costs

Contribution margin

Total contribution margin

Total operating profit

Basic Classic Total

428,550$ 640,000$ 1,068,550$

142,850$ 60,000$ 202,850$

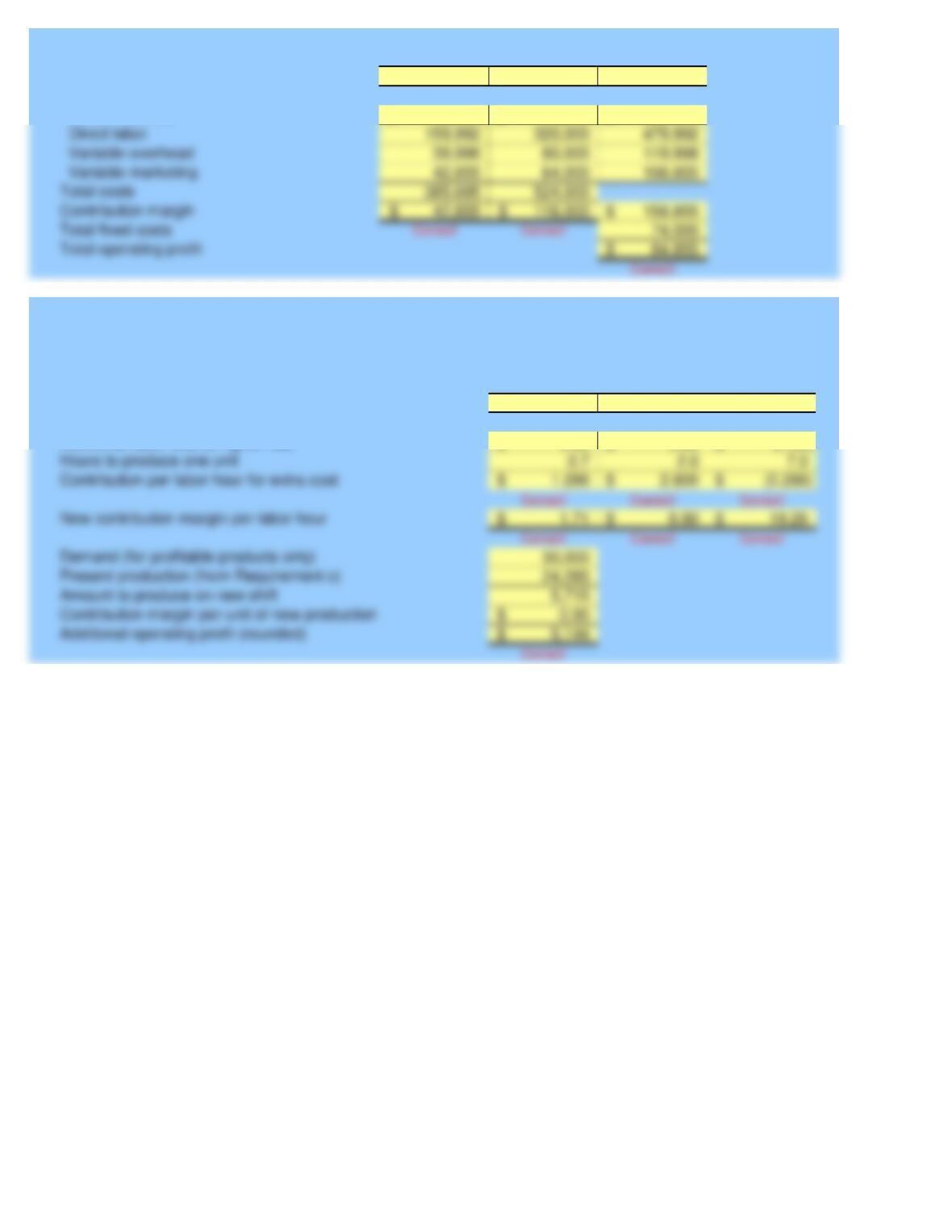

Basic Classic Formal

Hours to produce one unit

Contribution per labor hour for extra cost

New contribution margin per labor hour

Demand (for profitable products only)

Present production (from Requirement c)

Amount to produce on new shift

Contribution margin per unit of new production

Additional operating profit (rounded)

3.00$ 11.60$ 19.00$

Correct! Correct! Correct!

0.90$ 5.60$ (2.00)$

Decision to add shift to product more Basic and/or Formal

Requirement e:

Requirement d:

Total revenue

Less variable manufacturing costs:

Direct materials

Contribution margin per unit

Additional labor cost at higher rate

Direct labor

Variable overhead

Variable marketing

Total costs

Contribution margin

Total fixed costs

Total operating profit

Basic Classic Formal

30$ 64$ 190$

20,000 10,000 30,000

0.5 0.3 0.6

0.7 2.0 7.0

Input requirement per unit

Maximum annual demand (units)

Sales price

Given Data P04-62:

AUSTIN ENTERPRISES

Direct labor (hours)

Direct material (yards)

Product information:

Manufacturing

Marketing

Factory overhead (per direct-labor hour)

Marketing (percent of sales price)

Variable costs

Materials (per yard)

Direct labor (per hour)

Administration

Direct labor costs per hour including extra shift

Additional production hours provided by running extra shift

Requirement e:

Maximum direct labor-hours per year

Additional Information: