4–55 Ch. 4—Problems

Problem 4-13, Continued

(2) Amortization Schedule

Account adjustments Annual Current Prior

to be amortized Life Amount Year Years Total Key

Buildings 20 $ 5,000 $ 5,000 $ 5,000 $10,000 A1

Equipment 5 10,000 10,000 10,000 20,000 A2

Intercompany Fixed Asset Profit Deferral

Parent Sub

Original profit ……………………………………….. $40,000 $24,000

Year of sale………………………………………….. 1 2

Subsidiary Salmon Company Income Distribution

Unrealized profit in Internally generated net

ending inventory … (EI) $ 4,800 income ………………….. $ 29,500

Equipment gain ……….. (F1) 24,000 Realized profit in beginning

Parent Purple Company Income Distribution

Unrealized profit in ending Internally generated net

inventory ……………….. (EI) $ 4,200 income ………………….. $155,000

80% of Salmon adjusted Realized profit in beginning

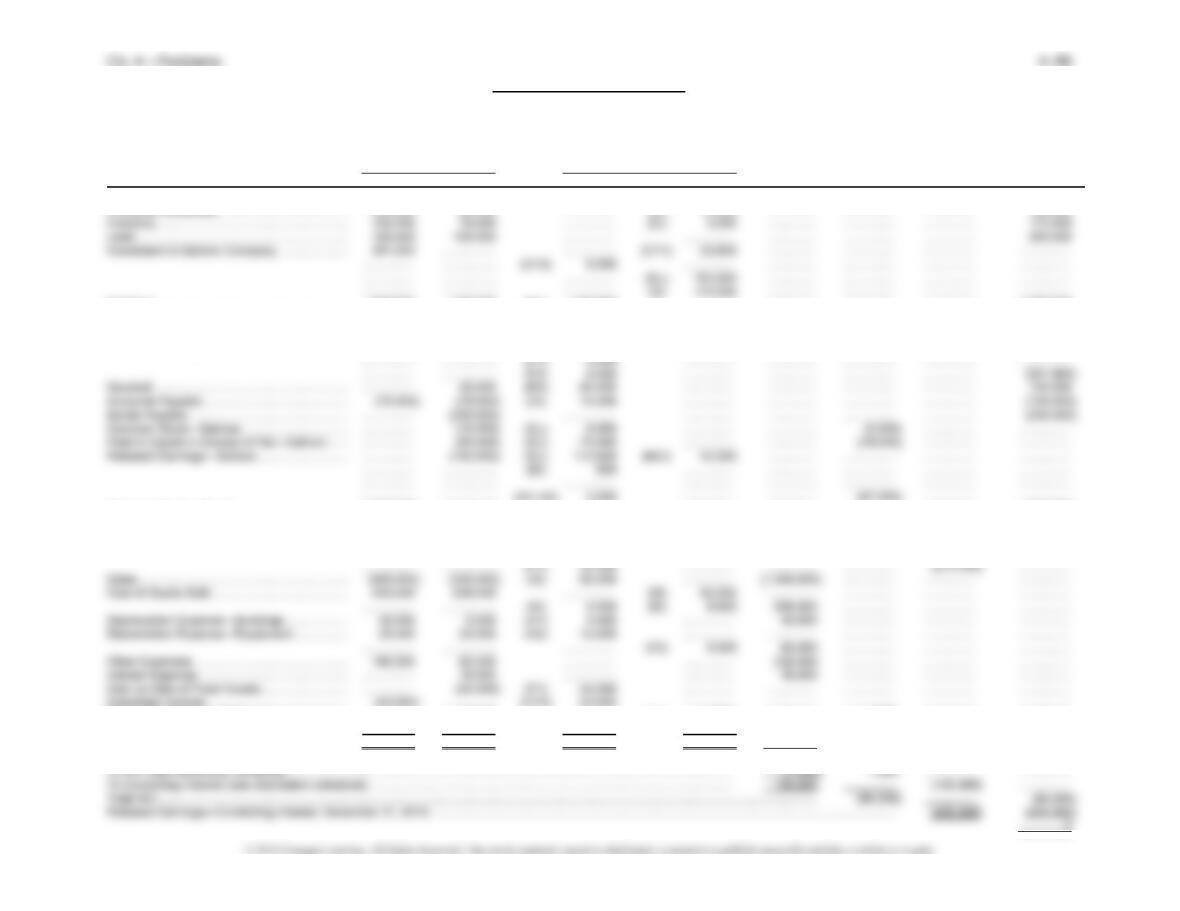

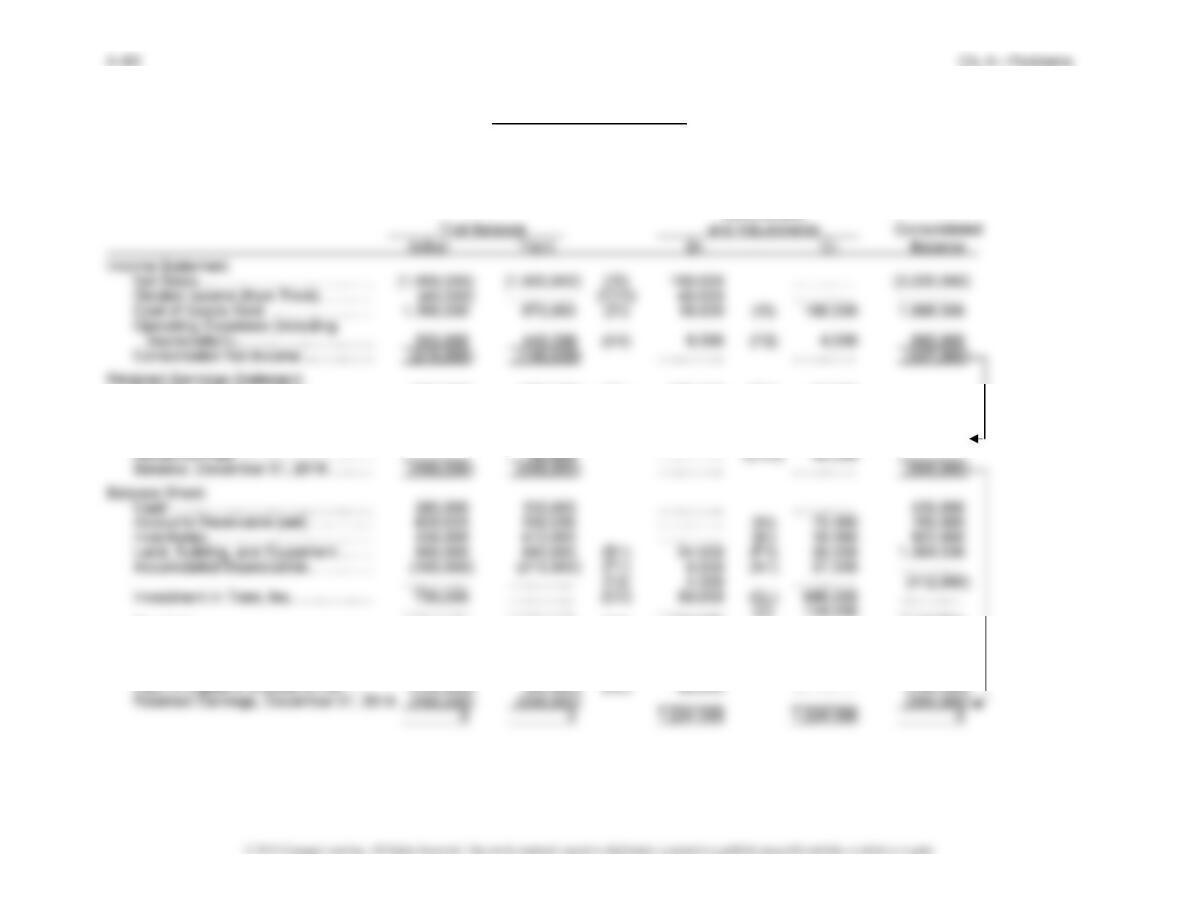

Problem 4-13, Continued

Purple Company and Subsidiary Salmon Company

Consolidated Income Statement

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Purple Salmon Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 92,400 57,500 …………… …………… …………… …………… …………… 149,900

Accounts Receivable ……………………………….. 130,000 36,000 …………… (IA) 14,000 …………… ..…………. …………… 152,000

Buildings ………………………………………………… 800,000 150,000 (D1) 100,000 …………… …………… …………… …………… 1,050,000

Accumulated Depreciation ………………………… (250,000) (60,000) …………… (A1) 10,000 …………… .………….. …………… (320,000)

Equipment ………………………………………………. 210,000 220,000 (D2) 50,000 (F1) 64,000 …………… …………… …………… 416,000

Accumulated Depreciation ………………………… (115,000) (80,000) …………… (A2) 20,000 …………… .………….. …………… ……………

Common Stock—Purple …………………………… (100,000) ……………. …………… …………… …..………. …………… …………… (100,000)

Paid-In Capital in Excess of Par—Purple ……. (800,000) ……………. …………… …………… ………..…. …………… …………… (800,000)

Retained Earnings—Purple ………………………. (325,000) ……………. (A1–A2) 12,000 …………… …………… …………… …………… ……………

…………… ……………. (BI) 8,000 …………… …………… …………… …………… …..……….

Dividends Declared—Salmon ……………………. …………… 10,000 …………… (CY2) 8,000 …………… 2,000 …………… ……………

Dividends Declared—Purple ……………………… 20,000 ……………. …………… …………… …………… …………… 20,000 ……………

0

0 664,800 664,800 …………… …………… …………… ……………

Consolidated Net Income ………………………………………………………………………………………….………………………………………. (154,100) …………… …………… ……………

4–57 Ch. 4—Problems

Problem 4-13, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

(EL) Eliminate controlling interest in subsidiary equity.

(D)/(NCI) Distribute excess and NCI adjustment.

(A) Amortize excess.

PROBLEM 4-14

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ……………………………………. $375,000* $300,000 $75,000

Fair value of net assets excluding goodwill …… 270,000** 216,000 54,000

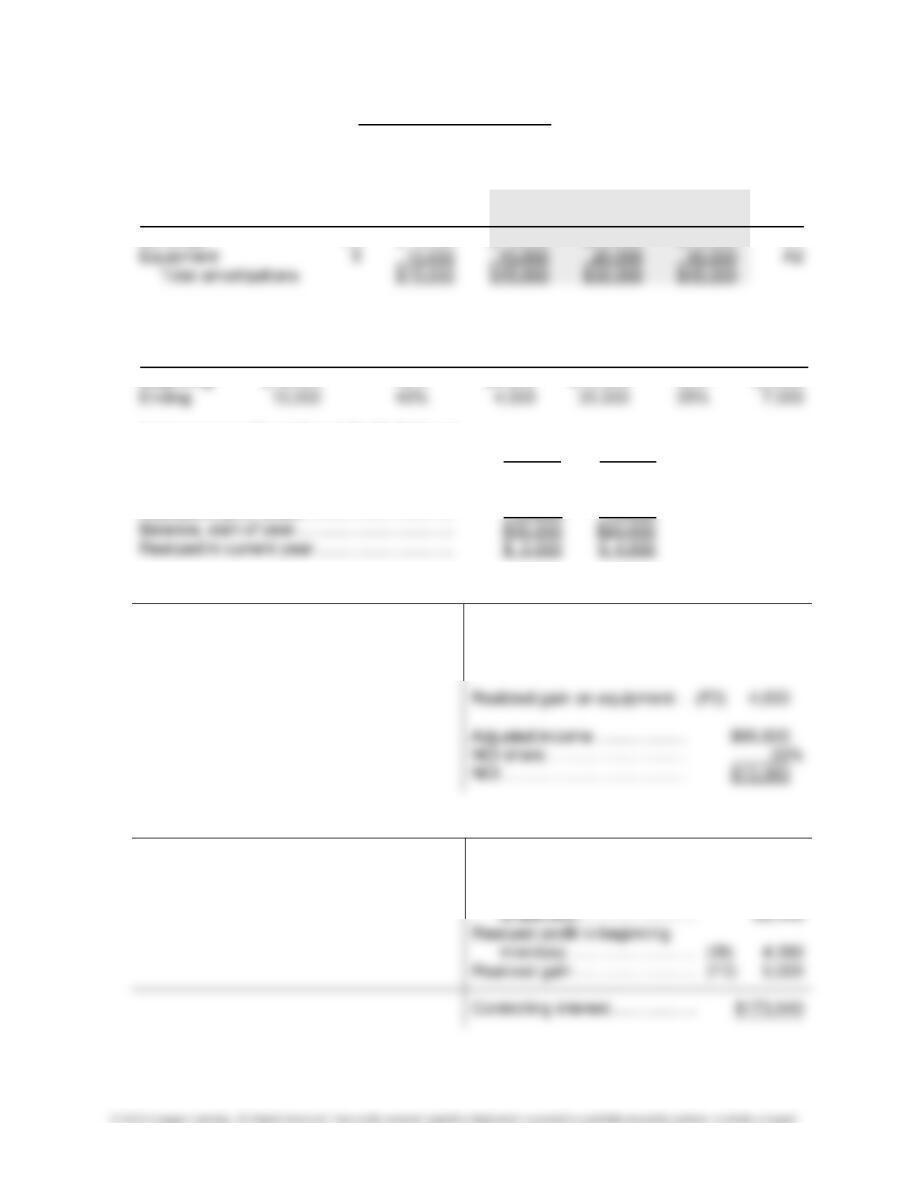

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Price paid for investment …………. $375,000 $300,000 $ 75,000

Less book value of interest acquired:

Common stock …………………. $ 10,000

Paid-in capital in excess of par 90,000

Adjustment of identifiable accounts:

Worksheet Amorti-

Adjustment Key Periods zation

Buildings ……………………………… $100,000 debit D1 20 $ 5,000

4–59 Ch. 4—Problems

Problem 4-14, Continued

(2) Amortization Schedule

Year of consolidation 3

Account adjustments Annual Current Prior

to be amortized Life Amount Year Years Total Key

Buildings 20 $ 5,000 $ 5,000 $10,000 $15,000 A1

Intercompany Inventory Profit Deferral

Parent Parent Sub Sub Sub

Parent Amount % Profit Amount % Profit

Beginning $12,000 35% $4,200 $16,000 30% $4,800

Intercompany Fixed Asset Profit Deferral

Parent Sub

Original profit ……………………………………….. $40,000 $24,000

Year of sale………………………………………….. 1 2

Realized in prior years …………………………… 10,000 4,000

Subsidiary Salmon Company Income Distribution

Ending inventory profit … (EI) $ 7,000 Internally generated net

Amortizations …………….. (A1–A2) 15,000 income ……………………….. $80,000

Beginning inventory profit …… (BI) 4,800

Parent Purple Company Income Distribution

Unrealized profit in ending Internally generated net

inventory ……………… (EI) $4,000 income …………………………. $115,000

80% of Salmon adjusted income

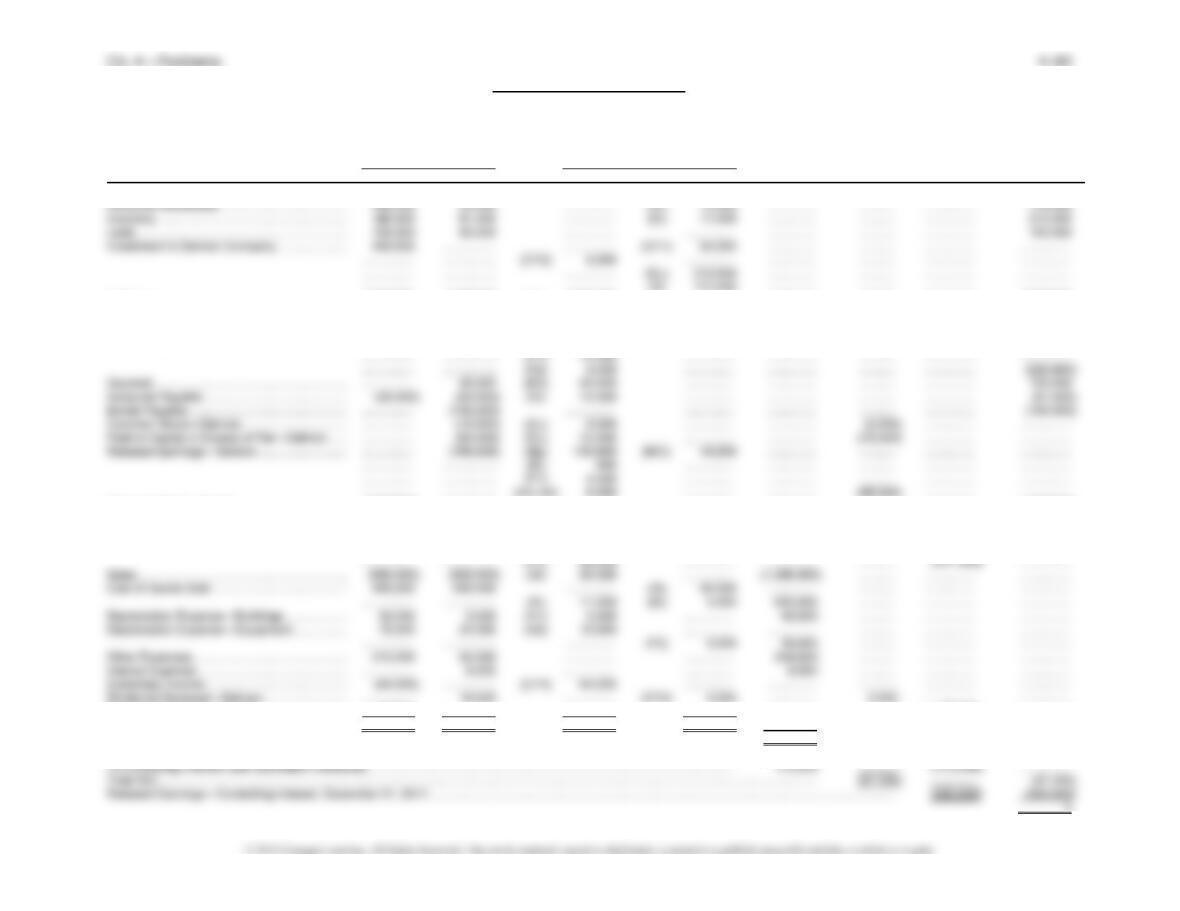

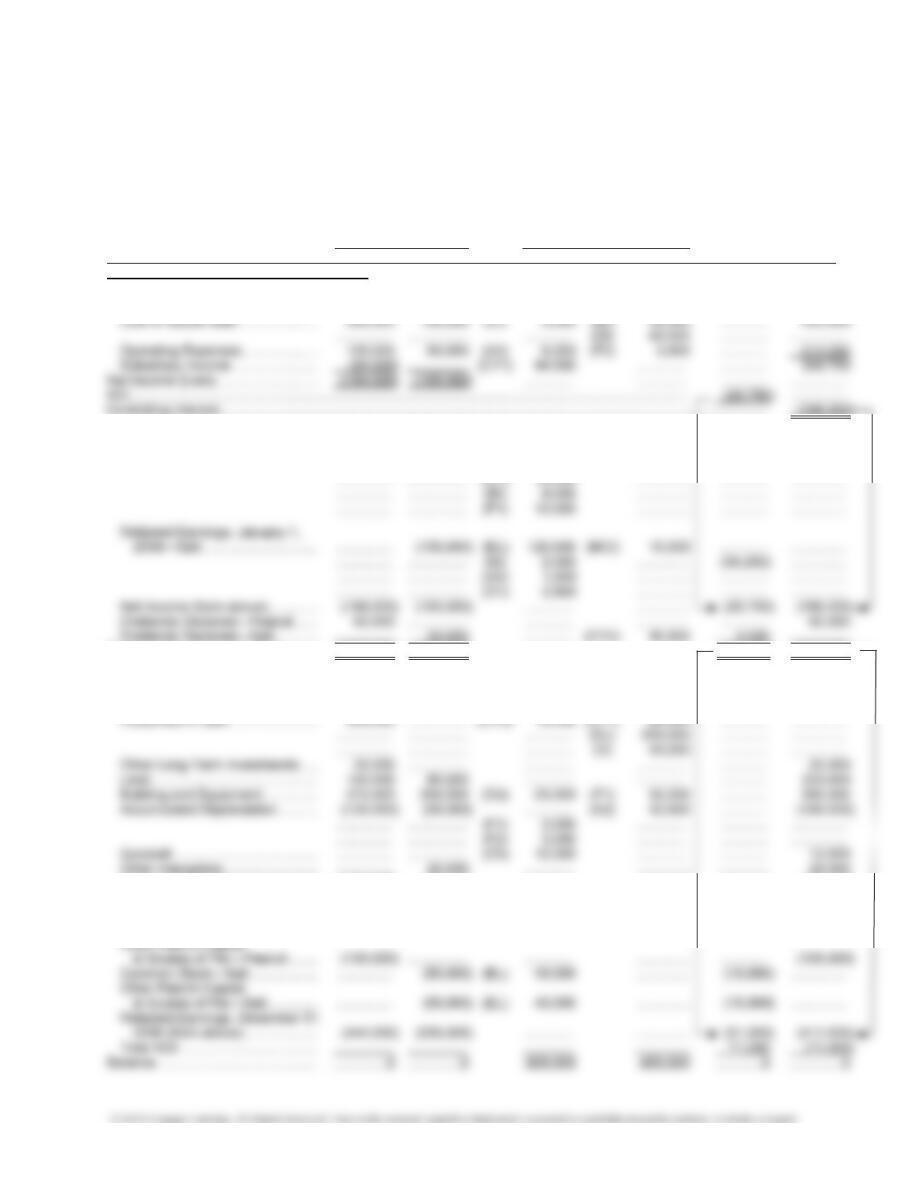

Problem 4-14, Continued

Purple Company and Subsidiary Salmon Company

Consolidated Income Statement

For Year Ended December 31, 2017

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Purple Salmon Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 195,400 53,500 …………… …………… ..…………. ……….. …………… 248,900

…………… ……………. …………… (D) 172,000 …………… ……….. …………… ……..…….

Buildings ………………………………………………… 800,000 150,000 (D1) 100,000 …………… …………… ……….. …………… 1,050,000

Accumulated Depreciation ………………………… (280,000) (65,000) …………… (A1) 15,000 …………… .………. …………… (360,000)

Equipment ………………………………………………. 150,000 220,000 (D2) 50,000 (F1) 64,000 …………… .………. …………… 356,000

Accumulated Depreciation ………………………… (115,000) (103,000) …………… (A2) 30,000 …………… ……….. …………… ……………

Common Stock—Purple …………………………… (100,000) ……………. …………… …………… …..………. ……….. …………… (100,000)

Paid-In Capital in Excess of Par—Purple ……. (800,000) ……………. …………… …………… ………..…. ……….. …………… (800,000)

Retained Earnings—Purple ………………………. (510,000) ……………. (A1–A2) 24,000 …………… …………… ……….. …………… ……………

…………… ……………. (BI) 8,040 …………… …………… ……….. …………… ……………

Dividends Declared—Purple ……………………… 40,000 ……………. …………… …………… …………… ……….. 40,000 ……………

0

0 744,600 744,600 …………… ……….. …………… ……………

Consolidated Net Income ………………………………………………………………………………………….………………………………………. (187,000) ……….. …………… ……………

To NCI (see distribution schedule) ……………………………………………………………………………………………………………….…….. 13,360 (13,360) …………… ……………

4–61 Ch. 4—Problems

Problem 4-14, Concluded

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

(EL) Eliminate controlling interest in subsidiary equity.

(D)/(NCI) Distribute excess and NCI adjustment.

(A) Amortize excess.

(IS) Eliminate intercompany sales during current period.

Ch. 4—Problems 4–62

APPENDIX PROBLEMS

PROBLEM 4A-1

Determination and Distribution of Excess Schedule

Company Parent

Implied Price NCI

Fair Value (100%) Value

Fair value of subsidiary ………………… $750,000 $750,000

Less book value of interest acquired:

Common stock ………………………. $400,000

Paid-in capital in excess of par … 80,000

Problem 4A-1, Continued

Arther Corporation and Subsidiary Trent, Inc.

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2018

Eliminations

Balance, January 1, 2018 …………….. (250,000) (206,000) (EL) 206,000 (CV) 50,000 ……………

……………. ……………. (A1) 18,000 …………… ……………

……………. ……………. (F1) 24,000 …………… (258,000)

Net Income ………………………………… (210,000) (190,000) ……………. …………… (337,000)

Goodwill …………………………………….. ……………. ……………. (D2) 60,000 …………… 60,000

Accounts Payable and Accrued

Expenses ………………………………… (670,000) (544,000) (IA) 75,000 …………… (1,139,000)

Common Stock ($10 par) …………….. (1,200,000) (400,000) (EL) 400,000 …………… (1,200,000)

Problem 4A-1, Concluded

Eliminations and Adjustments:

(CV) Convert to equity method as of January 1, 2018, 100% × $50,000 increase.

(CY2) Eliminate intercompany dividends.

(EL) Eliminate subsidiary equity against investment account.

(D) Distribute excess $54,000 to land, building, and equipment and $60,000 to goodwill.

(A1) Amortize excess applicable to machine for two prior years and current year.

(F2) Correct depreciation for intercompany profit, $4,000.

Subsidiary Trent, Inc. Income Distribution

Unrealized profit in ending Internally generated net

inventory…………………….. (EI) $18,000 income ………………………. $190,000

Parent Arther Corporation Income Distribution

Internally generated net

income ………………………. $170,000

100% × Trent adjusted income

4–65 Ch. 4—Problems

PROBLEM 4-A2

Peanut Company and Subsidiary Salt Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Financial Eliminations

Statements

and Adjustments Consolidated

Peanut Salt Dr. Cr. NCI Balance

Income Statement:

Net Sales ………………………………. (600,000) (315,000) (IS) 40,000 …………. …………. (875,000)

Controlling Interest …………………………………………………………………………………………….…………………………………. (186,000)

Retained Earnings:

Retained Earnings, January 1,

2016—Peanut …………………….. (320,000) ……………. (A2) 5,000 ………….. …………. (285,000)

Balance, December 31, 2016 ………. (444,000) (235,000) …………. …………. (51,000) (411,000)

Consolidated Balance Sheet:

Inventory, December 31 ………….. 130,000 50,000 …………. (EI) 5,000 …………. 175,000

Other Current Assets ………………. 241,000 235,000 …………. …………. …………. 476,000

Current Liabilities ……………………. (150,000) (70,000) …………. ………….. …………. (220,000)

Bonds Payable ………………………. …………… (100,000) …………. ………….. …………. (100,000)

Other Long-Term Liabilities ……… (200,000) (50,000) …………. ………….. …………. (250,000)

Common Stock—Peanut …………. (200,000) ……………. …………. ………….. …………. (200,000)

Problem 4A-2, Continued

Eliminations and Adjustments:

(CY1) Eliminate the current-year subsidiary income recorded by the parent.

(CY2) Eliminate intercompany dividends.

(A2) Amortize the equipment write-up over four years, with $5,000 (80% × $6,250) for 2015

charged to the parent’s retained earnings and $1,250 to the subsidiary’s retained

earnings, and $6,250 for 2016 to operating expenses.

Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ………………………………………….. $250,000* $200,000 $50,000

4–67 Ch. 4—Problems

Problem 4A-2, Concluded

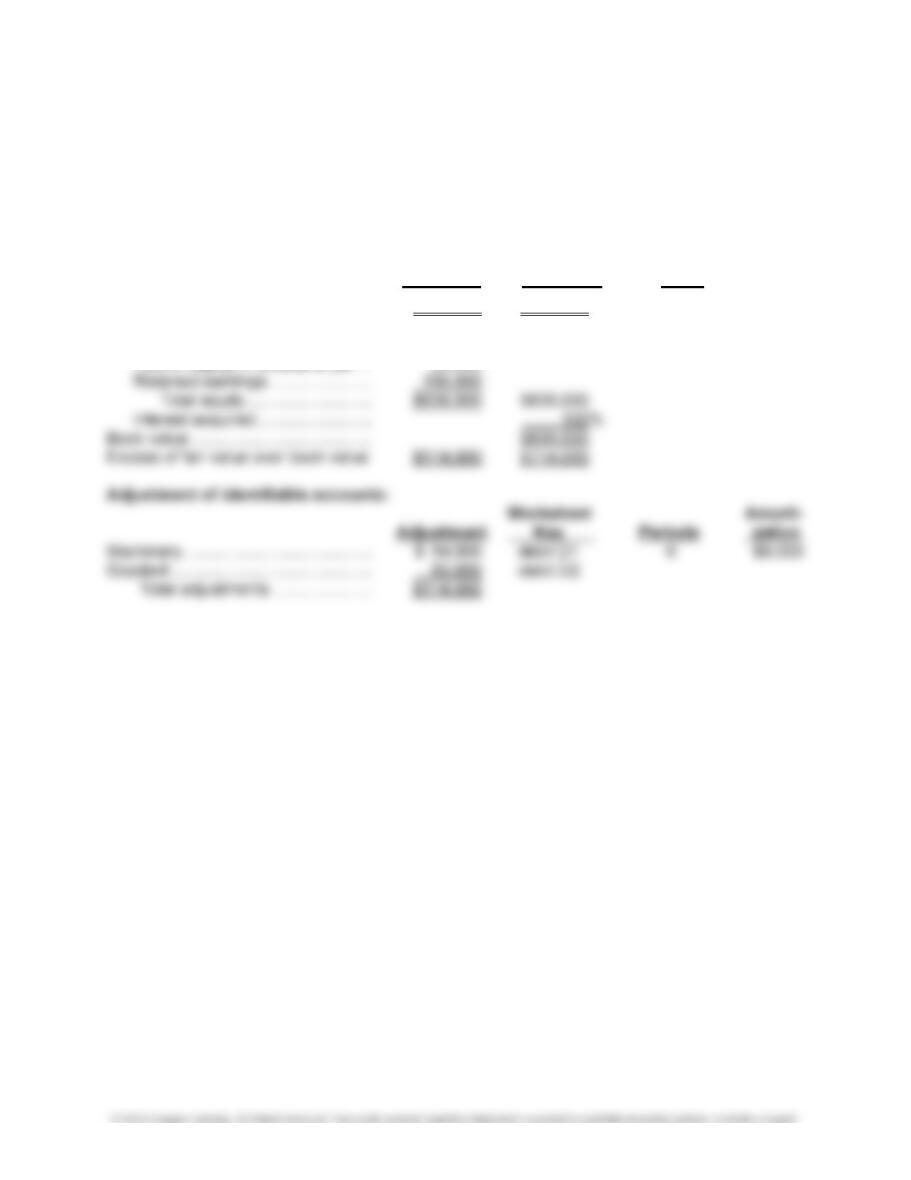

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Price paid for investment ……………… $250,000 $200,000 $ 50,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amorti-

Adjustment Key Periods zation

Inventory ……………………………………. $12,500 debit D1 1 $12,500

Equipment ………………………………….. 25,000 debit D2 4 6,250

Goodwill …………………………………….. 12,500 debit D3

Total adjustments …………………. $50,000

Subsidiary Salt Company Income Distribution

Ending inventory profit ……………. (EI) $5,000 Internally generated net

Amortizations ………………………… (A2) 6,250 income ………………………. $105,000

Parent Peanut Company Income Distribution

Internally generated net

income ……………………….. $100,000

Realized gain on equipment

Sale ……………………………. (F2) 3,000

CASE 4-1

To: Harvey Henderson

From: Student

Concerning: Cool Glass accounting issues

Harvey, you are a minority shareholder and can look only to the income statement of the sepa-

rate Henderson Window Company. You have no claim on the assets of the consolidated com-

pany. The controlling interest may well take actions that are wise for the consolidated controlling

interest, but they may not be in your best interest.

The price charged for glass is a direct part of Henderson’s cost of sales. A higher price reduces

Henderson income and thus the 30% of Henderson income available to Henderson sharehold-

ers. The higher price increases the income of Cool Glass, all the benefits of which go to Cool

Glass shareholders. In consolidation, the price charged is eliminated; only the purchases from

the outside and the sales to the outside remain in the consolidated statements. The distribution