6e Statement of Stockholders’ Equity Page 108 Chapter 4

ACTIVITY 34 CROSSWORD PUZZLE FOR CHAPTER 4

Across

4. Ratio measuring how expensive a company’s stock price

is compared to EPS (2 words)

7. Solvency ratio that measures how debt boosts ROA to

increase ROE (2 words)

11. Internal financing (2 words)

13. Statement reporting changes in shares outstanding,

earnings, and the distribution of earnings (2 words)

16. Maximum number of shares permitted to be issued

Down

1. Shares sold to investors

2. Shares receiving dividends before common shares;

3. Per share amount of dividends paid annually (2 words)

5. Amounts received in excess of par (4 words)

9. Total amount paid-in for shares of stock by investors

14. Shares held by investors; issued shares less treasury

shares

6e Statement of Stockholders’ Equity Page 109 Chapter 4

ACTIVITY 35 STATEMENT OF STOCKHOLDERS’ EQUITY—TYPES OF STOCK

Purpose: • Identify three types of stock.

• Identify the number of shares authorized, issued, and outstanding.

• Compute the total cost of contributed capital and the average cost per share.

The Statement of Stockholders’ Equity provides information about changes in a company’s stockholders’

equity, including contributed capital and retained earnings. It helps investors understand the structure of

a company’s ownership.

• Contributed capital (CC) includes amounts paid-in (contributed) by stockholders to purchase the

stock of a corporation. There are two types of stock: common stock and preferred stock. Each

corporation must issue common stock, whereas preferred stock is optional.

• When originally issued, amounts received from investors are recorded in two separate accounts—

the Par Value account and an Additional Paid-in-Capital account. Par Value is a legal value assigned

to each share of stock upon incorporation, which must be recorded separately in the financial

statements. Additional Paid-in-Capital (APIC) is the amount received in excess of par.

Par Value + Additional Paid-in-Capital = Total Issue Price of Stock

Refer to the Statement of Stockholders’ Equity for American Eagle Outfitters, Inc. and accompanying notes

on page 107 to answer the following questions.

Upon incorporation, a company is authorized (by the state of incorporation) to issue a designated

number of shares to investors. Sometimes corporations buy back shares of stock that have been issued;

these are referred to as Treasury Stock. Shares outstanding are the total number of shares actually held

by investors at a given time, equaling shares issued less shares of treasury stock.

Shares issued – Treasury shares = Shares outstanding

6e Statement of Stockholders’ Equity Page 110 Chapter 4

Why does the average cost of issued common shares differ from the average cost of treasury

shares?

6e Statement of Stockholders’ Equity Page 111 Chapter 4

ACTIVITY 36 STATEMENT OF STOCKHOLDERS’ EQUITY

Purpose: • Interpret an increase and decrease in Stockholders’ Equity.

• Understand preferred and common stock dividends.

• Compute shares outstanding after a stock split.

Retained earnings (RE) are net income earned by the company since its incorporation and not yet

distributed as dividends. It is increased by net income, the earnings of this accounting period, and

decreased by dividends, a distribution of earnings.

Beginning Retained Earnings + Net Income – Dividends = Ending Retained Earnings

Refer to the Statement of Stockholders’ Equity for American Eagle Outfitters (AEO), Inc. and accompanying

notes presented on page 107 to answer the following questions.

Q1 For fiscal year ended on January 28, 2012 for AEO:

business assets owned by shareholders.

Q3 Assume that AEO issued 1 million shares of preferred stock with a dividend rate of $5 per share.

Q4 a. A company has 170 million common shares outstanding.

Assume there is a two-for-one stock split, after the stock split there would be

wealth.

c. Under International Financial Reporting Standards (IFRS), preferred stock would be classified

6e Statement of Stockholders’ Equity Page 112 Chapter 4

Q5 For each of the following events, identify the effect on stockholders’ equity.

6e Statement of Stockholders’ Equity Page 113 Chapter 4

ACTIVITY 37 RATIO ANALYSIS: EARNINGS PER SHARE

Purpose: • Understand that EPS cannot be used to compare profitability among companies.

• Compute how treasury stock affects EPS.

• Identify EPS trends and compare EPS to Market Price to enhance meaning.

Earnings per Share (EPS) indicates the amount of net income

earned by each individual share of stock held by investors.

EPS

=

Net income – Preferred dividends

Average number of

common shares outstanding

Use the EPS information below for Athar and Wagdy Companies to answer the following questions.

Athar Company EPS = $0.50

Wagdy Company EPS = $2.00

Net income = $1,000,000

Avg. # of CShares OS 2,000,000

Net income = $1,000,000

Avg. # of CShares OS 500,000

Q1 Refer to the EPS information immediately above. Even though Wagdy Company reports

Athar Company EPS = $0.50

Wagdy Company EPS = $2.00

Year 1 Year 2 Year 3

EPS $0.10 $0.20 $0.50

Year 1 Year 2 Year 3

EPS $8 $4 $2

Q3 Refer to the EPS information immediately above. EPS for Athar Company has a/an

Athar Company EPS = $0.50

Wagdy Company EPS = $2.00

Market Price = $6/share = PE Ratio

EPS $0.50 of 12

Market Price $60/share = PE Ratio

EPS $2.00 of 30

Q4 Refer to the EPS and the Market Price information immediately above. The PE Ratio measures how

expensive a stock is; how much investors are willing to pay for each $1 of EPS. A PE below 10 is

considered a “bargain” stock, whereas a PE of more than 20 is considered “expensive.” Measured

6e Statement of Stockholders’ Equity Page 114 Chapter 4

Earnings per Share (EPS) indicates the amount of net income

earned by each individual share of stock held by investors.

EPS

=

Net income – Preferred dividends

Average number of

common shares outstanding

Use the EPS information below for Athar and Wagdy Companies to answer the following questions.

Athar Company EPS = $0.50

Wagdy Company EPS = $2.00

Net income = $1,000,000

Avg. # of CShares OS 2,000,000

Net income = $1,000,000

Avg. # of CShares OS 500,000

Q2 If Athar Company buys back 1 million shares of common stock, then treasury stock would

Athar Company EPS = $0.50

Wagdy Company EPS = $2.00

Year 1 Year 2 Year 3

EPS $0.10 $0.20 $0.50

Year 1 Year 2 Year 3

EPS $8 $4 $2

Athar Company EPS = $0.50

Wagdy Company EPS = $2.00

Market Price = $6/share = PE Ratio

EPS $0.50 of 12

Market Price $60/share = PE Ratio

EPS $2.00 of 30

Q4 Refer to the EPS and the Market Price information immediately above. The PE Ratio measures how

expensive a stock is; how much investors are willing to pay for each $1 of EPS. A PE below 10 is

ACTIVITY 38 RATIO ANALYSIS: FINANCIAL LEVERAGE

Purpose: • Understand how debt affects financial leverage and ROE.

• Compute ROS, Asset Turnover, ROA, Financial Leverage, ROE, and the Debt Ratio.

Q1 Review Corporations A through E on page 113. All corporations have the same amount of

Financial Leverage Ratio = Assets / SE

Debt Ratio = Liabilities / Assets

Because A = L + SE you can convert:

Financial Leverage Ratio = 1 / (1 – Debt Ratio)

risk.

Q5 In the Primary Driver chart on the previous page:

a. Circle the Primary Driver of ROA as either ROS or Asset Turnover.

b. Circle the Primary Driver of ROE as either ROA, Financial Leverage, or of equal (=)

contribution.

change.

Q7 What is the primary driver of ROE when the debt ratio is:

DUPONT ANALYSIS of ROE

Formula

CORP A

CORP B

CORP C

CORP D

CORP E

Sales revenue

$ 100

$ 100

$ 100

$ 100

$ 100

Net income

10

10

10

10

10

Assets

100

100

100

100

100

Liabilities

0

25

50

75

96

Stockholders’ equity

$ 100

$ 75

$ 50

$ 25

$ 4

Assets

Assets

PRIMARY DRIVER CHART

Primary

Driver

CORP A

CORP B

CORP C

CORP D

CORP E

6e Statement of Stockholders’ Equity Page 117 Chapter 4

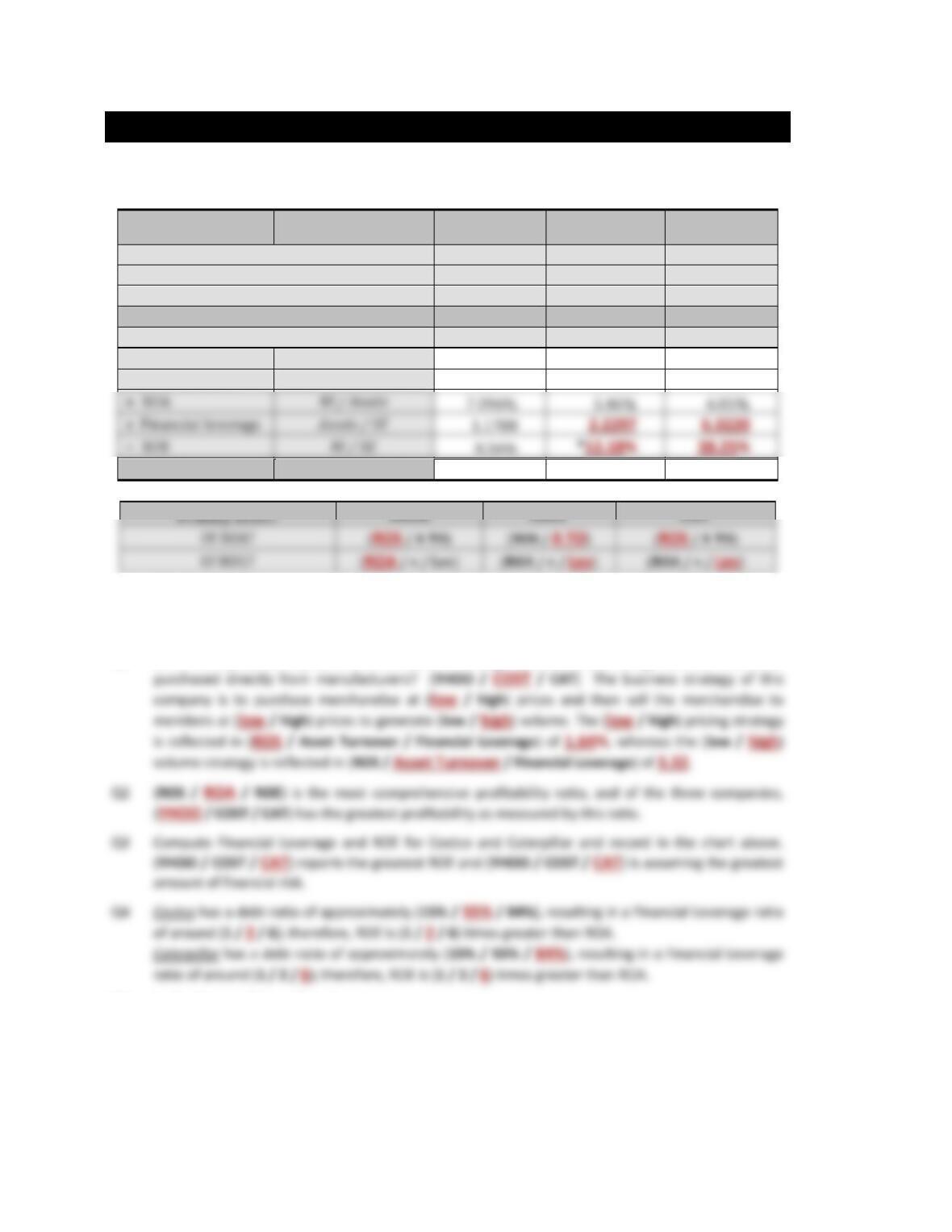

ACTIVITY 39 FINANCIAL LEVERAGE OF THREE COMPANIES

Purpose: • Understand how debt affects financial leverage and ROE.

• Compute Financial Leverage and ROE.

$ in Millions

Formula

YHOO

12/31/2011

COST

8/29/2011

CAT

12/31/2011

Sales revenue

4,984

88,915

60,138

Net income

1,049

1,462

4,928

Assets

14,783

26,761

81,446

Liabilities

2,242

14,759

68,563

Stockholders’ equity

12,541

12,002

12,883

ROS

NI / Sales Revenue

21.05%

1.64%

8.19%

x Asset turnover

Sales Revenue / Assets

0.3371

3.3226

0.7384

Debt ratio

Liabilities / Assets

15.17%

55.15%

84.18%

*Small rounding error.

Refer to the financial information above for Yahoo! Inc. (YHOO), Costco Wholesale Corporation (COST),

and Caterpillar Inc. (CAT) to answer the following questions.

Q1 Which company offers products to members in a range of merchandise categories that have been

Q5 In the Primary Driver chart above:

a. Circle the Primary Driver of ROA as either ROS or Asset Turnover.

b. Circle the Primary Driver of ROE as either ROA, Financial Leverage, or of approximately equal

(=) contribution.

7.096%

5.46%

6.05%

1.1788

6e Statement of Stockholders’ Equity Page 118 Chapter 4

Q6 Using only the financial information above, which company would you prefer to invest in?

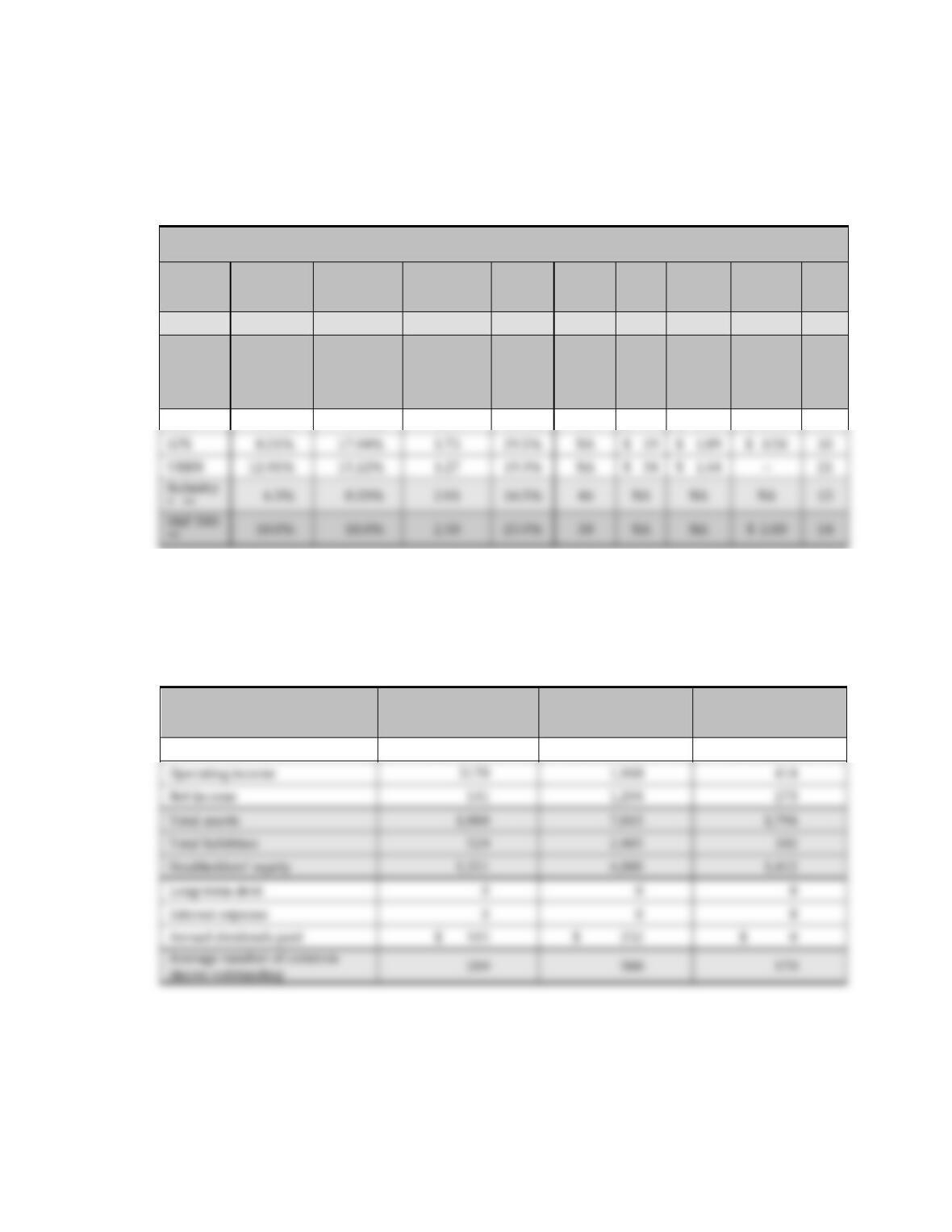

ACTIVITY 40 RATIO ANALYSIS

Purpose: • Review a number of ratios to better evaluate a company.

• Understand that the expected range of ratios varies by industry.

• Understand that comparing a ratio to industry norms enhances meaning.

Ratios reveal relationships.

Below are ratios with explanations introduced in this chapter. See Appendix B for additional ratios.

Financial Leverage is similar to the debt ratio, in the sense that the more debt a company has, the

higher the Financial Leverage. It measures how debt “boosts” return on assets to increase return on

equity.

Financial Leverage

=

Total assets

Stockholders’ equity

The Return on Equity (ROE) ratio measures how effectively stockholders’ equity is used to produce

net income. ROA x Financial Leverage = ROE

ROE

=

Net income

Stockholders’ equity

Times Interest Earned indicates a company’s ability to earn (cover) its periodic interest payments.

Times Interest Earned

=

Operating income

Interest expense

Earnings per Share (EPS) is the amount of net income (loss) earned by each individual share of stock

held by investors.

EPS

=

Net income – Preferred dividends

Average number of common shares outstanding

The Dividend Rate is the amount of dividends paid annually for each share of stock held by investors.

Dividend Rate

=

Annual common stock dividends paid

Investors use the Price Earnings (PE) ratio to measure how “expensive” a company’s stock is

compared to EPS. Regrettably, it does not explain why a stock is expensive or cheap.

Market price per share

EPS

6e Statement of Stockholders’ Equity Page 120 Chapter 4

Below are ratios and selected financial information for three companies within the Retail Apparel industry:

American Eagle Outfitters, Inc. (AEO), GAP Inc. (GPS), and Urban Outfitters Inc.(URBN).

RATIOS for the fiscal year ended January 29, 2011

RATIO

ROS

ROA x

Financial

Leverage

= ROE

Times

Interest

Earned

Market

Price

EPS

Dividend

Rate

PE

Ratio

Type

Profit

Profit

Solvency

Profit

Solvency

Invest

Profit

Invest

Invest

Formula

NI /

Sales

Revenue

NI /

Total Assets

Total Assets/

SE

NI / SE

Operating

Income /

Interest

Expense

NA

NI –

Preferred

Div / Avg #

of CShares

OS

Annual Div

paid / Avg #

of CShares

OS

Market

Price /

EPS

AEO

4.75%

7.50%

1.39

10.4%

NA

$ 14

$ 0.91

$ 0.44

15

* Industry Averages for Apparel Stores—Industry and S&P 500 ratio averages from moneycentral.msn.com

** There are no official rules governing how these ratios are calculated. Therefore, the ratio formulas used may

differ from the formulas in the text.

For the fiscal year ended

January 29, 2011

(In Millions)

American Eagle

Outfitters (AEO)

Gap

(GPS)

Urban Outfitters

(URBN)

Sales revenue

$ 2,968

$ 14,664

$ 2,274

Operating income

Net income

Total assets

Total liabilities

Long-term debt

Interest expense

Annual dividends paid

GPS

8.21%

17.04%

1.73

29.5%

NA

$ 1.89

$ 0.50

10

URBN

1.27

19.3%

NA

$ 34

$ 1.64

21

6e Statement of Stockholders’ Equity Page 121 Chapter 4

Refer to the ratios and selected financial information for three companies within the Retail Apparel

Industry: American Eagle Outfitters, Inc. (AEO), GAP Inc. (GPS), and Urban Outfitters Inc. on the previous

page to answer the following questions.

Apparel Store Industry.

S&P 500.

Bargain PE < PE Ratio of 10 to 20 < Expensive PE

6e Statement of Stockholders’ Equity Page 122 Chapter 4

6e Statement of Stockholders’ Equity Page 123 Chapter 4

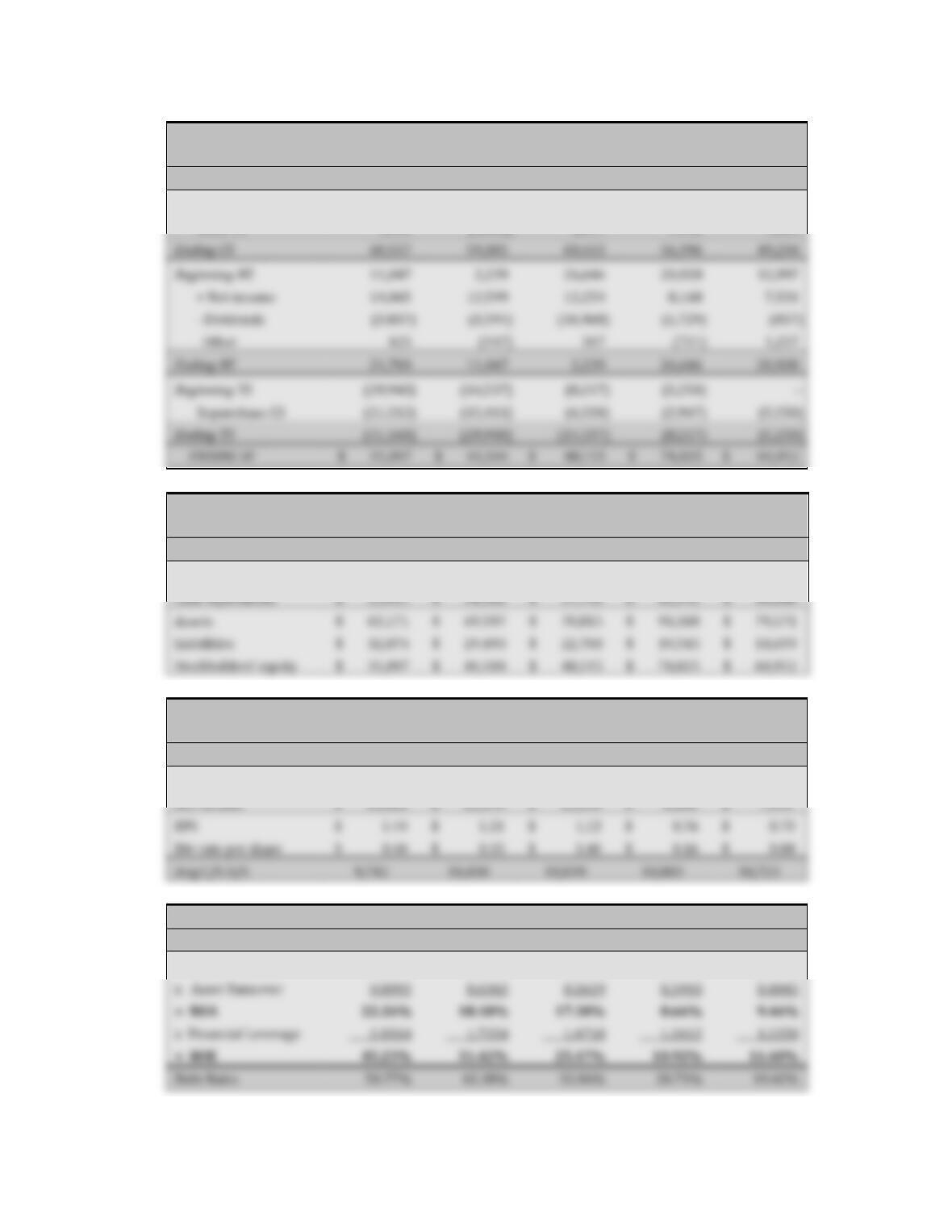

ACTIVITY 41 TEST YOUR UNDERSTANDING

Purpose: • Identify reasons for change in cash, total liabilities, and stockholders’ equity

• Explain how changes in the balance sheet and income statement affect ROA and ROE

• Explain the effect of a huge cash dividend payment

Refer to the financial statement and ratio information for Microsoft on page 119 to answer the following

questions.

Q1 Study the Statement of Stockholders’ Equity for the five years presented.

a. During fiscal year ended (FYE) 6/30/2003 stockholders’ equity increased primarily as a result

6e Statement of Stockholders’ Equity Page 124 Chapter 4

MICROSOFT

STATEMENT OF STOCKHOLDERS’ EQUITY

Adapted from the Form 10-K, $ in millions

6/30/2007

6/30/2006

6/30/2005

6/30/2004

6/30/2003

Beginning CS

$ 59,005

$ 60,413

$ 56,396

$ 49,234

$ 41,845

Issue CS

1,552

(1,408)

4,017

7,162

7,389

MICROSOFT

BALANCE SHEET

Selected Amounts in Millions

6/30/2007

6/30/2006

6/30/2005

6/30/2004

6/30/2003

Cash/Assets

37.06%

49.08%

53.31%

64.21%

61.64%

Cash equivalents

$ 23,411

$ 34,161

$ 37,751

$ 60,592

$ 49,048

Assets

$ 63,171

$ 69,597

$ 70,815

$ 94,368

$ 79,571

Liabilities

$ 32,074

$ 29,493

$ 22,700

$ 19,543

$ 14,659

$ 31,097

$ 40,104

$ 48,115

$ 74,825

$ 64,912

MICROSOFT

INCOME STATEMENT

Selected Amounts in Millions, Except per Share Data

Fiscal year ended…

6/30/2007

6/30/2006

6/30/2005

6/30/2004

6/30/2003

Revenue

$ 51,122

$ 44,282

$ 39,788

$ 36,835

$ 32,187

Net income

$ 14,065

$ 12,599

$ 12,254

$ 8,168

$ 7,531

EPS

$ 1.44

$ 1.21

$ 1.13

$ 0.76

$ 0.70

Div rate per share

$ 0.40

$ 0.35

$ 3.40

$ 0.16

$ 0.08

Avg C/S O/S

MICROSOFT

DUPONT ANALYSIS of ROE

6/30/2007

6/30/2006

6/30/2005

6/30/2004

6/30/2003

ROS

27.51%

28.45%

30.80%

22.17%

23.40%

x Asset Turnover

22.26%

18.10%

17.30%

45.23%

31.42%

25.47%

10.92%

11.60%

Ending CS

Beginning RE

2,239

+ Net income

8,168

7,531

– Dividends

(3,837)

(3,594)

(1,729)

Other

1,257

Ending RE

2,239

Beginning TS

(8,217)

(5,250)

Repurchase CS

(6,320)

(2,967)

(5,250)

Ending TS

(8,217)

6e Statement of Stockholders’ Equity Page 125 Chapter 4

Q5 Review the DuPont Analysis of ROE for the five years presented.

a. Asset turnover = Sales revenue / Total assets. During FYE 6/30/2005 revenue

c. Financial Leverage = SE / Total Assets. During FYE 6/30/2005 liabilities

Q6 What might have prompted this special one-time dividend?

Q7 Review the financial information presented for Microsoft. Explain how the special one-time $3

dividend affected each of the following items.

a. Cash, Asset Turnover, and ROA

6e Statement of Stockholders’ Equity Page 126 Chapter 4

Q9 Review the financial information presented for Microsoft. Explain how the purchase of common

stock (treasury stock) affected each of the following items.

a. Cash, Asset Turnover, and ROA

b. Debt Ratio, Financial Leverage, and ROE