CHAPTER 4

SOLUTIONS TO EXERCISES—SET B

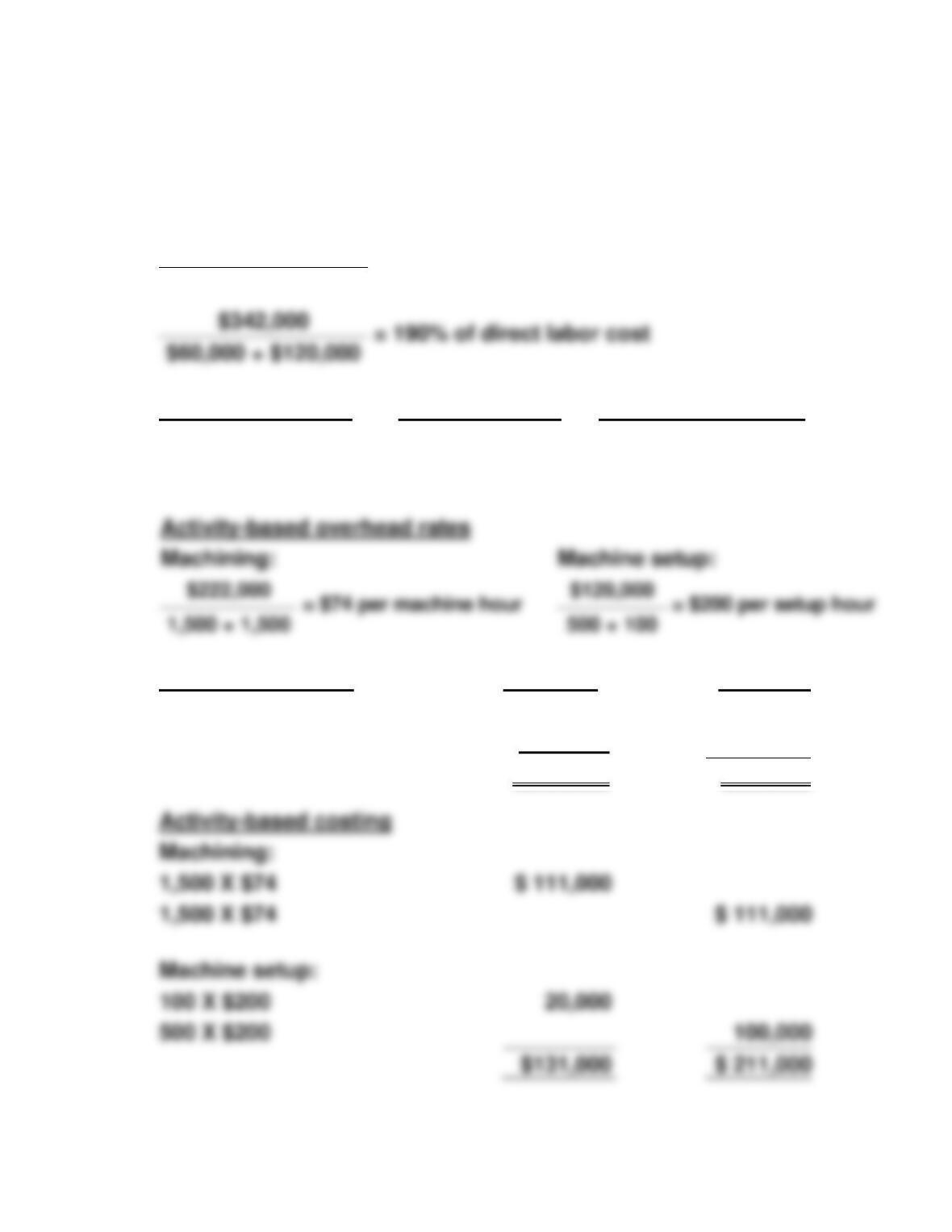

EXERCISE 4-1B

(a)

Estimated overhead

= Predetermined overhead rate

Direct labor costs

(b)

Activity cost pools

Cost drivers

Estimated overhead

Machining

Machine hours

$222,000

Machine setup

Set up hours

120,000

Activity-based overhead rates

Machining:

Machine setup:

(c)

Traditional costing

Standard

Custom

$60,000 X 190%

$ 114,000

$120,000 X 190%

$228,000

$ 114,000

$228,000

Activity-based costing

Machining:

1,500 X $74

1,500 X $74

Machine setup:

100 X $200

500 X $200

EXERCISE 4-2B

(a)

Traditional costing system

Product 440X

Product 137Y

Product 249S

Sales

$300,000

$180,000

$100,000

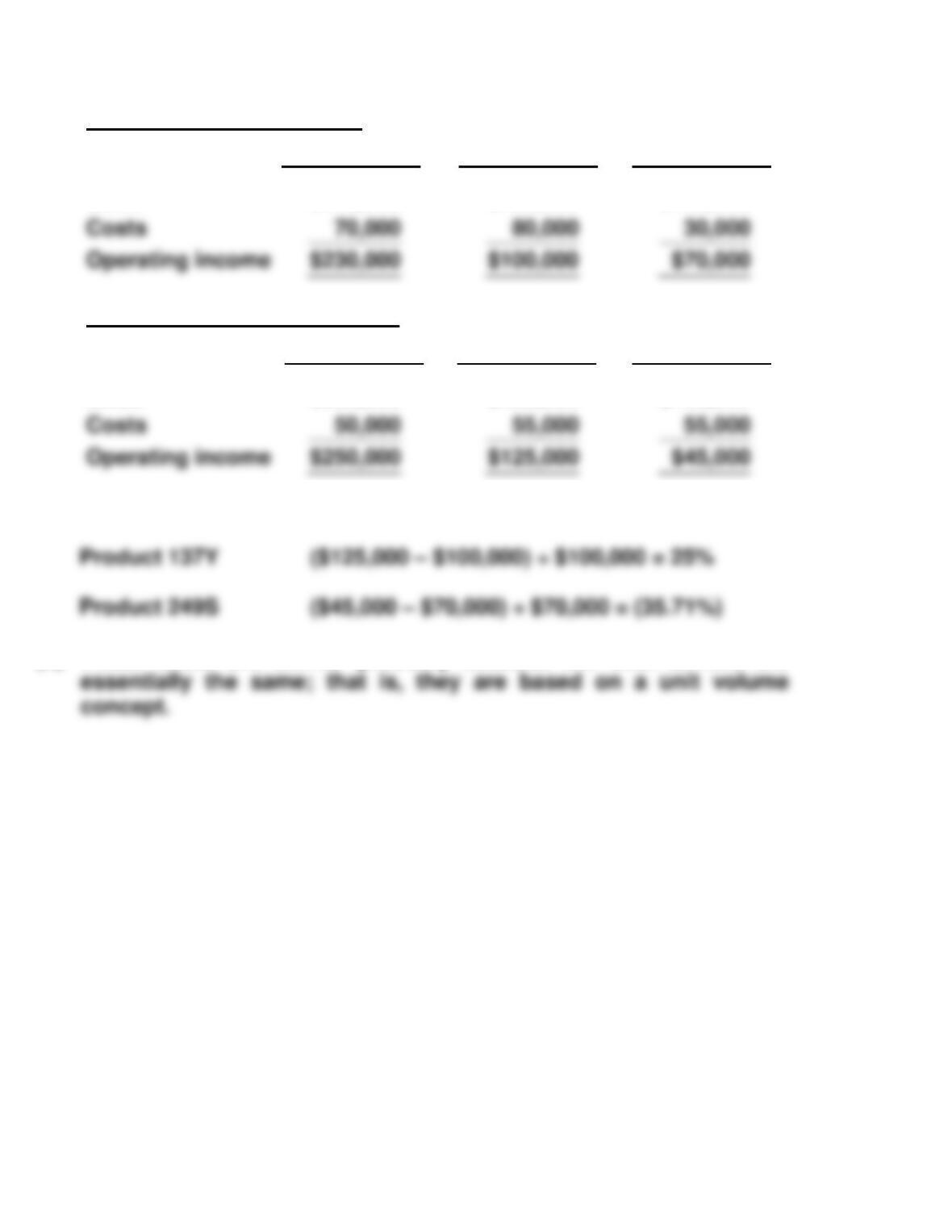

(b)

Activity-based costing system

Product 440X

Product 137Y

Product 249S

Sales

$300,000

$180,000

$100,000

Operating income

$125,000

(c)

Product 440X:

($250,000 – $230,000) ÷ $230,000 = 8.70%

Product 249S

($45,000 – $70,000) ÷ $70,000 = (35.71%)

(d)

These costs are similar probably because the cost drivers are

Operating income

$100,000

EXERCISE 4-3B

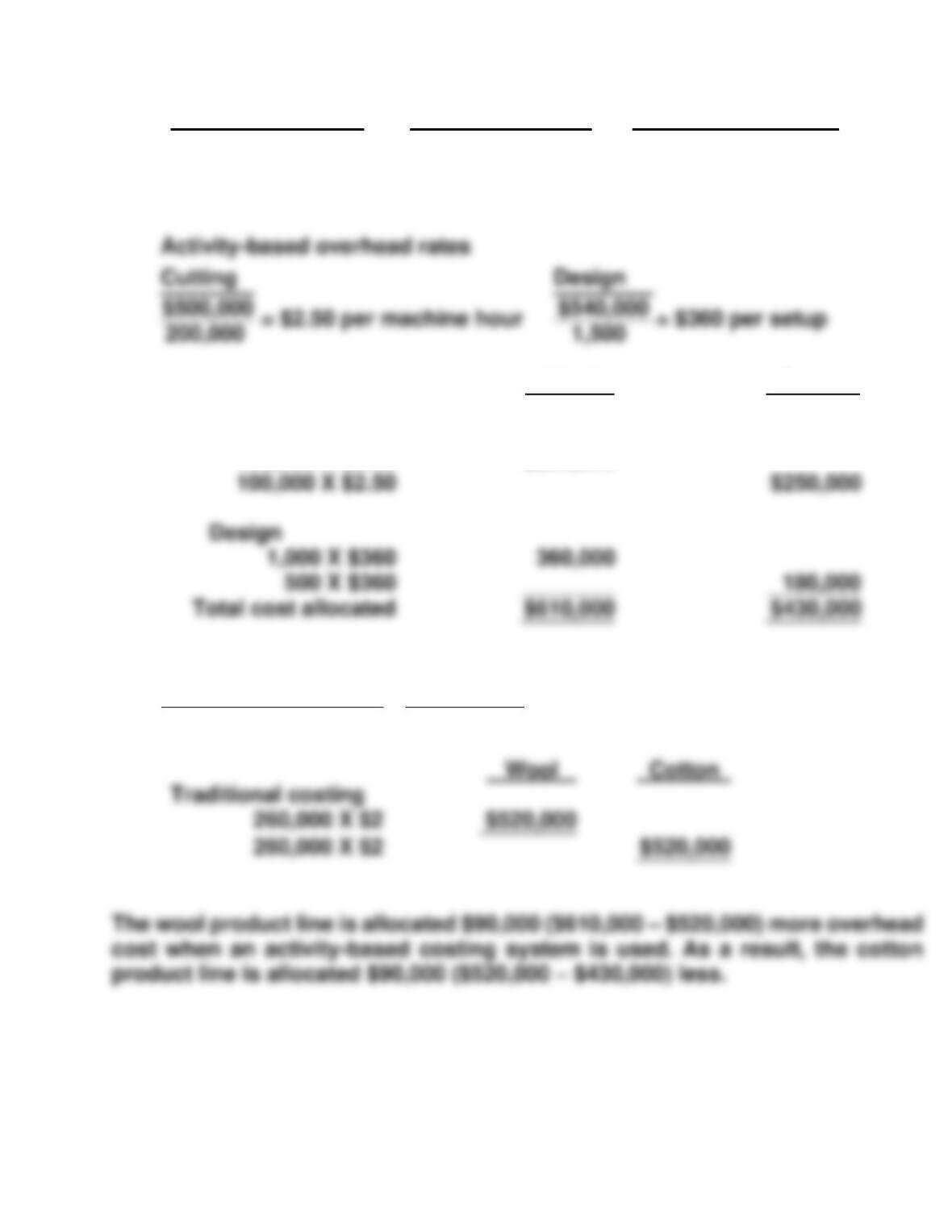

(a)

Activity cost pools

Cost drivers

Estimated overhead

Cutting

Machine hours

$500,000

Design

Number of setups

540,000

Wool

Cotton

Activity-based costing

Cutting

100,000 X $2.50

$250,000

Design

(b)

Estimated

overhead

=

$1,040,000

= $2 per direct labor hour

Direct labors hours

520,000

Traditional costing

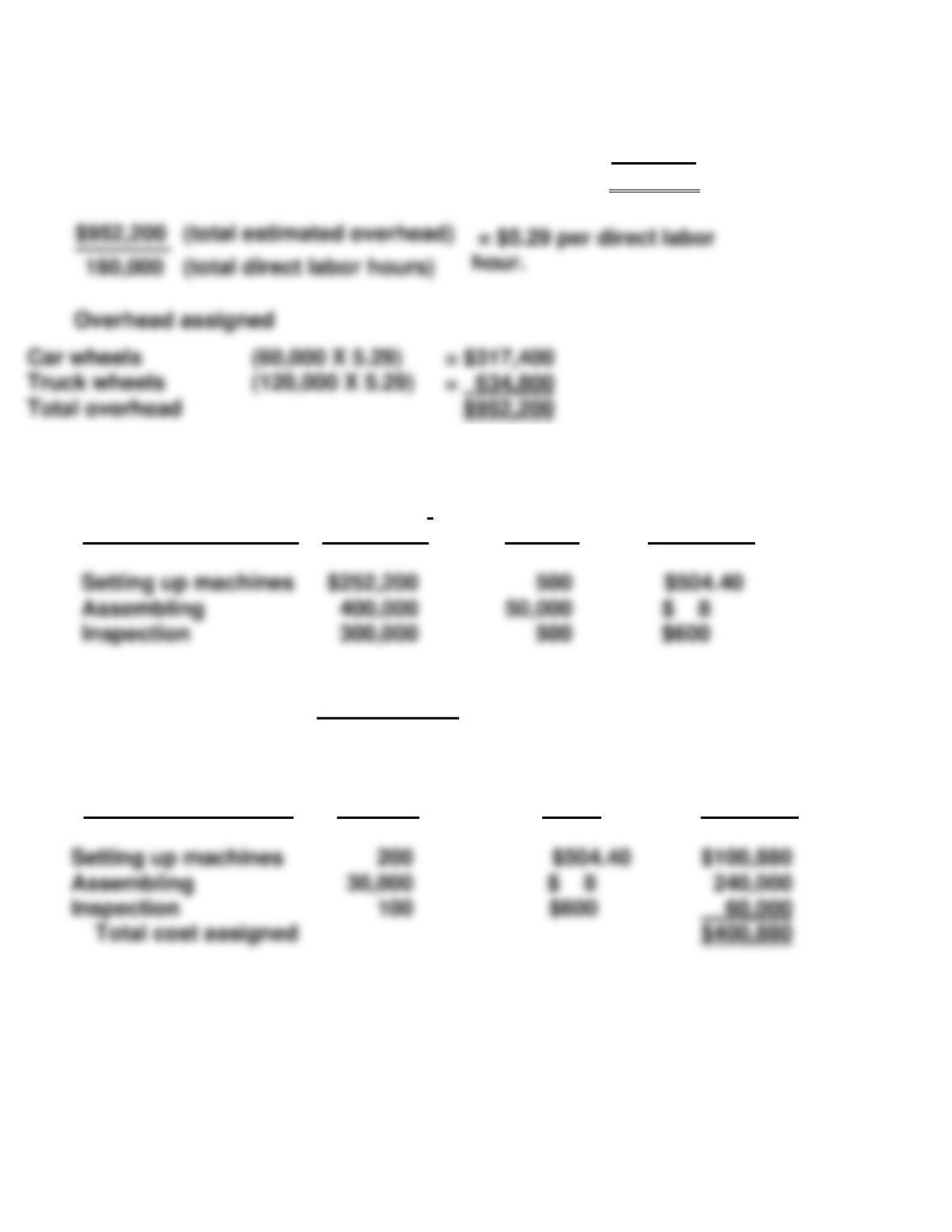

EXERCISE 4-4B

(a)

Direct labor hours for car wheels

(30,000 X 2)

= 60,000

Direct labor hours for truck wheels

(20,000 X 6)

= 120,000

Total direct labor hours

180,000

(b)

Activity Cost Pools

Estimated

Overhead

÷

Expected

Use of

Cost

Drivers

=

ABC

Overhead

Rate

Assembling

Inspection

(c)

Car Wheels

Activity Cost Pools

Expected Use

of Cost

Driver per

Product

X

Activity-Based

Overhead

Rates

=

Cost

Assigned

Total cost assigned

$400,880

Car wheels

(60,000 X 5.29)

Total overhead

EXERCISE 4-4B (Continued)

(c)

Truck Wheels

Activity Cost Pools

Expected use

of Cost

Driver per

Product

X

Activity-

Based

Overhead

Rates

=

Cost

Assigned

Setting up machines

300

$504.40

$151,320

(d) Assuming that the cost drivers are a reasonable representation of what is

occurring in the two product lines, it seems appropriate to switch to

EXERCISE 4-5B

(a) Traditional costing:

$210,000 ÷ 2,500 (500 + 2,000) hours

= $84.00 per direct labor hour

Assembling

Inspection

Total cost assigned

EXERCISE 4-5B (Continued)

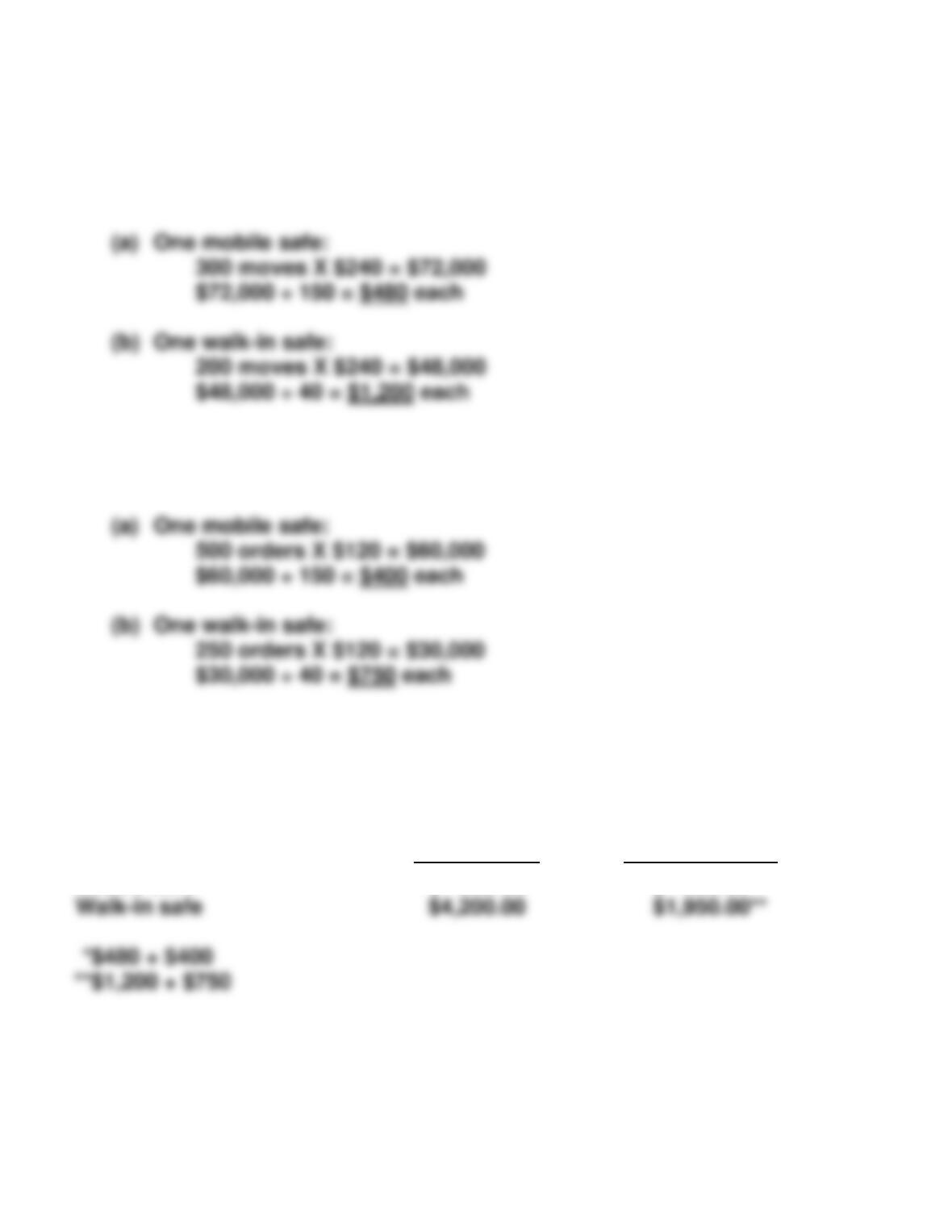

(b) Activity-based costing:

(1) Material handling costs

$120,000 ÷ 500 (300 + 200) moves = $240 per move

(2) Purchasing activity costs

$90,000 ÷ 750 (500 + 250) orders = $120 per order

(c) The total amount of overhead allocated to each unit of the two products

under the two allocation approaches is:

Traditional

Costing

Activity-Based

Costing

Mobile safe

$ 280.00

**$ 880.00**

EXERCISE 4-6B

(a) The overhead rates are:

Activity Cost Pools

Estimated

Overhead

÷

Expected Use

of Cost Drivers

per Activity

=

Activity-Based

Overhead Rates

Materials handling

$36,000

1,200

$30

(b) The assignment of the overhead costs to products is as follows:

Instruments

Gauges

Cost

Assigned

Cost Driver

Number

Cost

Number

Cost

Units produced (b)

300

Overhead cost per

$590

Materials handling

($30)

Machine setups ($62)

Quality inspections

400

150

$12,000

9,300

800

300

$24,000

18,600

$36,000

27,900

Machine setups

EXERCISE 4-6B (Continued)

(c) MEMO

To: President, Flair Instruments

From: Student

EXERCISE 4-7B

(a) (1) Traditional product costing system:

(2) Activity-based costing system:

Activity Cost Pools

Cost Drivers

Used

X

Activity-

Based

Overhead

Rates

=

Overhead Cost

Assigned

Catalogs

Credit and collection

Sales commissions

Advertising—TV/Radio

$920,000

250

$.04

$300

$ 36,800

75,000

(b) As compared to ABC, traditional costing grossly undercosts the selling

costs assigned to the “high intensity” product line. The difference of

EXERCISE 4-8B

(a) (1) Traditional product costing system:

(2) Activity-based costing system:

Activity Cost Pools

Cost Drivers

Used

X

Activity-

Based

Overhead

Rate

=

Overhead Cost

Assigned

$ .35

Inspections of material received

6,000

$ .85

$ 5,100

(b) As compared to ABC, the traditional costing system undercosts the

quality-control overhead cost assigned to the low-calorie dessert product

(c) All three activities, as quality-control related activities, are non-value–

EXERCISE 4-9B

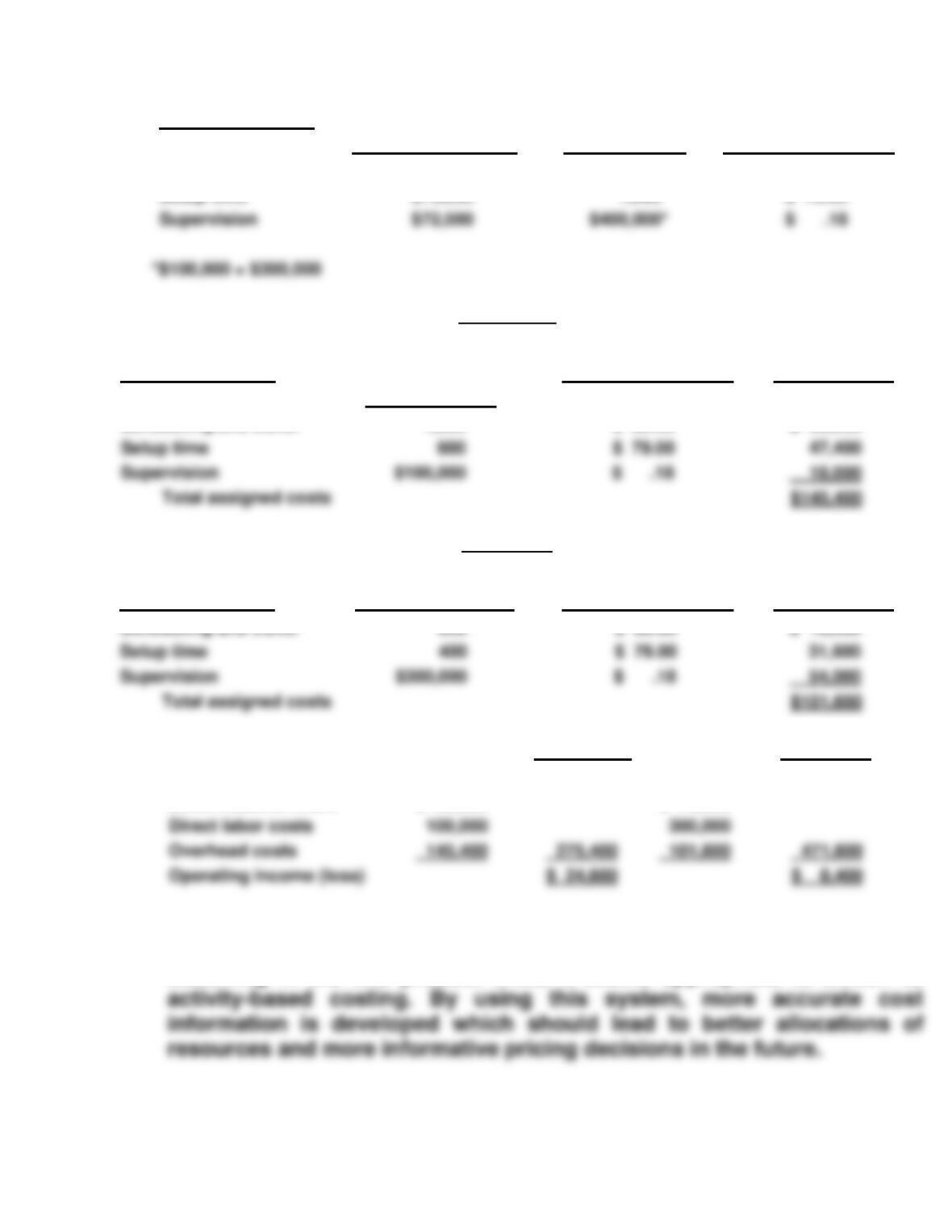

(a)

Activity Cost Pools

Estimated Overhead

÷

Expected use

of Cost Drivers

=

ABC Overhead Rates

Scheduling and travel

$96,000

1,200

$ 80.00

Setup time

$79,000

1,000

$ 79.00

Commercial

Activity Cost Pools

Expected use of

Cost Drivers per

Product

X

ABC Overhead Rates

=

Cost Assigned

Scheduling and travel

1,000

$ 80.00

$ 80,000

Setup time

Supervision

$100,000

Total assigned costs

$145,400

Residential

Activity Cost Pools

Expected use of Cost

Drivers per Product

X

ABC Overhead Rates

=

Cost Assigned

Scheduling and travel

200

$ 80.00

$ 16,000

Setup time

Supervision

54,000

Total assigned costs

(b)

Commercial

Residential

Revenues

$300,000

$480,000

Direct material costs

$ 30,000

$ 70,000

Direct labor costs

100,000

300,000

Overhead costs

Operating income (loss)

(c) Assuming that the cost drivers are a reasonable representation of what is

occurring in the two product lines, it seems appropriate to switch to

Supervision

$72,000

$ .18

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 4-1C

(a) Computation of unit costs—traditional costing.

Velocity, Inc.

Products

Manufacturing Costs

Deluxe Model

Standard Model

Direct materials

$11

$42

(b) Velocity, Inc.

Activity Cost Pool

Estimated

Overhead

÷

Expected

Use of Cost Drivers

=

Activity-Based

Overhead Rate

Packing and shipping

$ 2.50 per pound

Purchasing

Receiving

$130,000

30,000

650 Orders

20,000 Pounds

$200.00 per order

$ 1.50 per pound

(c) Velocity, Inc.

Deluxe Model

Standard Model

Activity Cost Pool

Expected

Use of

Drivers

X

Overhead

Rates

=

Cost

Assigned

Expected

Use of

Drivers

X

Overhead

Rates

=

Cost

Assigned

50,000

Overhead cost per unit

Purchasing

Receiving

Assembling

150

4,000

20,000

$200.00

$ 1.50

$ 5.00

$ 30,000

6,000

100,000

500

16,000

54,000

$200.00

$ 1.50

$ 5.00

$ 100,000

24,000

270,000

Total unit cost

PROBLEM 4-1C (Continued)

(d) Computation of Units Costs – ABC

Velocity, Inc.

Manufacturing Costs

Deluxe Model

Standard Model

Direct materials

$11.00

$42.00

(e)

Activity

Value- vs. Non-value-added

Purchasing

Non-value-added

(f) (1) Activity-based costing shows the standard model absorbs more

(2) The comparison of ABC and traditional costing shows that, ABC

costing will provide a significant difference as overhead is allocated

Total cost per unit

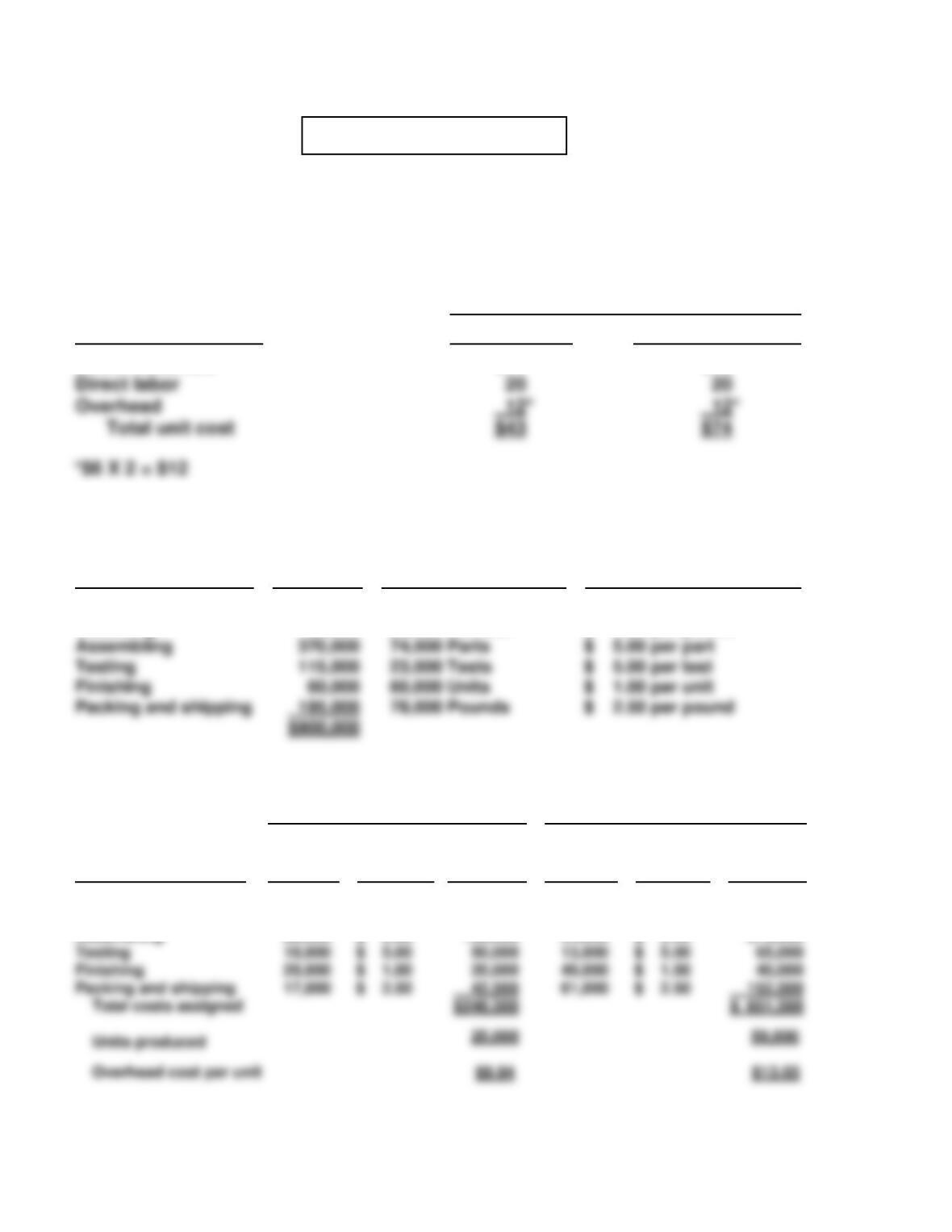

PROBLEM 4-2C

(a) The allocation of total manufacturing overhead using activity-based

costing is as follows:

Xtra

Preferred

Overhead Rate

Drivers

Used

Cost

Assigned

Drivers

Used

Cost

Assigned

Total

Overhead

Purchase orders @ $15

20,000

$ 300,000

30,000

$ 450,000

$ 750,000

(b) The cost per unit and gross profit of each model under ABC costing were:

Xtra

Preferred

Gross profit

Direct materials

Direct labor

$ 500

100

$ 350

80

(c) Management’s future plans for the two television models are not sound.

Under ABC costing, the Xtra model is $227.50 per unit more profitable than

PROBLEM 4-3C

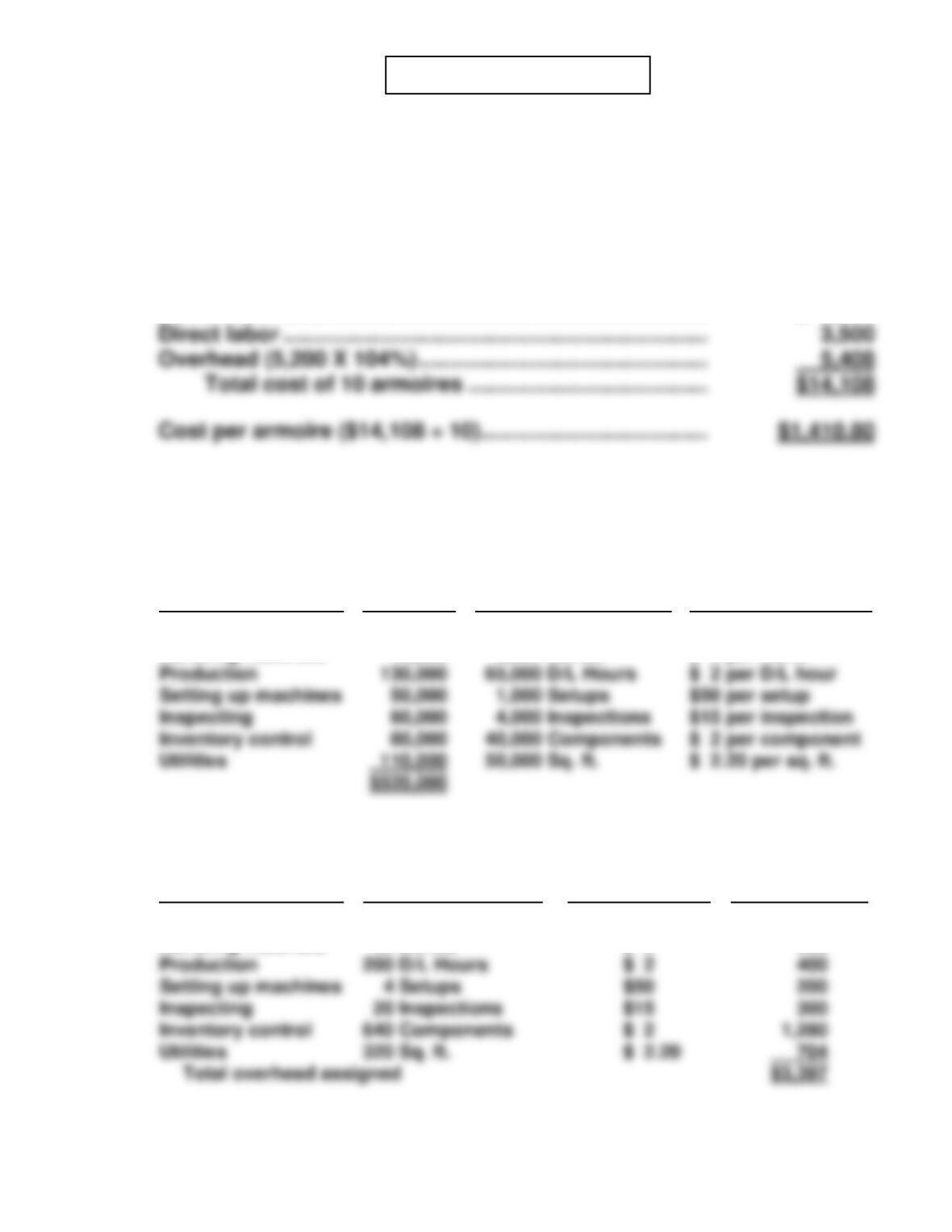

(a) Predetermined overhead rate using materials cost:

$520,000 ÷ $500,000 = 104% of materials cost

(b) Manufacturing cost per armoire under traditional costing:

Direct materials …………………………………………………….. $ 5,200

(c) Manufacturing cost per armoire under activity-based costing:

Computation of Activity-Based Overhead Rate

Activity Cost Pools

Estimated

Overhead

÷

Total

Estimated Drivers

=

Activity-Based

Overhead Rate

Utilities

50,000 Sq. ft.

$ 2.20 per sq. ft.

Purchasing

Handling materials

$ 45,000

45,000

600 Orders

5,000 Moves

$75 per order

$ 9 per move

Assignment of Overhead to Order of 10 armoires

Activity Cost Pools

Expected Use of

Drivers

X

Activity-Based

Overhead Rate

=

Cost Assigned

Inventory control

640 Components

Purchasing

Handling materials

3 Orders

32 Moves

$75

$ 9

$ 225

288

PROBLEM 4-3C (Continued)

Total manufacturing cost per armoire under ABC:

Direct materials ……………………………………………………….…… $ 5,200

Direct labor ………………………………………………………………….. 3,500

(d) The difference between the traditional cost and the activity-based cost per

unit, $1,410.80 versus $1,209.70, is not great in amount but $201.10 or

PROBLEM 4-4C

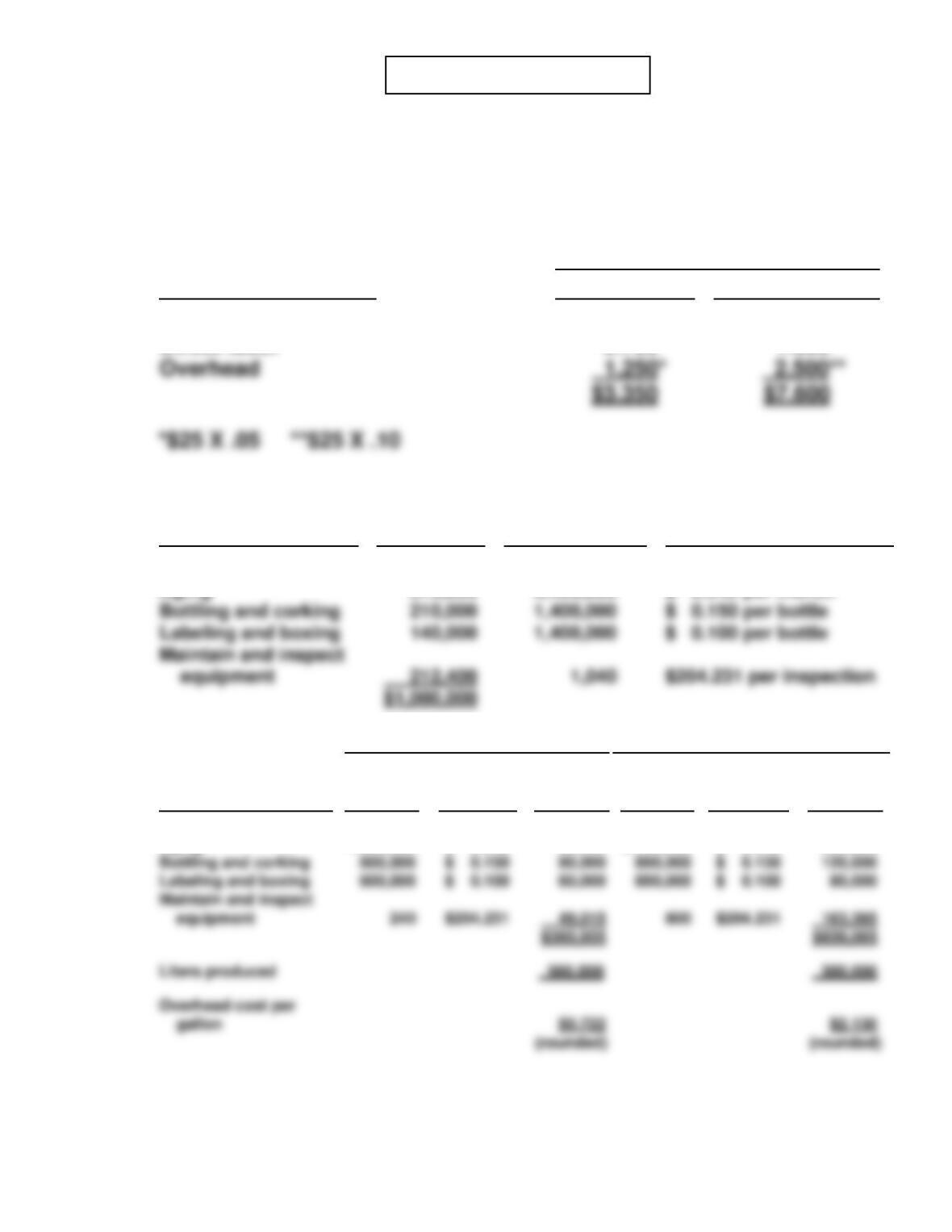

(a) Computation of unit costs—traditional costing

Overhead cost per labor hour is $1,000,000 ÷ (35,000 + 5,000) =$25

Products

Manufacturing Costs

Valley Fresh

Vargas Valley

Direct materials

Direct labor

$1.350

0.750

$3.600

1.500

(b)

Activity Cost Pools

Estimated

Overhead

Expected Use

of Cost Drivers

Activity-Based

Overhead Rate

equipment

$204.231 per inspection

Grape processing

Aging

$ 124,000

313,600

10,000

6,400,000

$ 12.40 per cart

$ 0.049 per month

(c)

Valley Fresh

Vargas Valley

Activity Cost Pool

Expected

Use of

Drivers

X

Overhead

Rates

=

Cost

Assigned

Expected

Use of

Drivers

X

Overhead

Rates

=

Cost

Assigned

(rounded)

(rounded)

Grape processing

Aging

8,000

1,280,000

$ 12.40

$ 0.049

$ 99,200

62,720

2,000

5,120,000

$ 12.40

$ 0.049

$ 24,800

250,880

PROBLEM 4-4C (Continued)

(d)

Products

Manufacturing Costs

Valley Fresh

Vargas Valley

Direct materials

Direct labor

$1.350

0.750

$3.600

1.500

(e) To: Mr. Vincent Vargas

From: Student

Subject: Product costs using traditional approach versus ABC

The memorandum covers the following points:

a. ABC allocates overhead costs as a function of each product’s use of

b. Traditional approaches that allocate costs as a function of volume

tend to be biased toward allocating too much overhead to high

PROBLEM 4-4C (Continued)

d. The total cost of the two products under the two approaches was as

follows:

Valley Fresh

Vargas Valley

Traditional approach

$3.350

$7.600

PROBLEM 4-5C

(a) Computation of assigned overhead under traditional costing (“direct labor

dollars” appears in the first line of the schedule of overhead data):

Predetermined overhead rate X direct labor dollars

Overhead assigned to corporate:.322 X $900,000 = $289,800

(b) (1) Computation of activity-based overhead rate:

Activity Cost Pool

Estimated

Overhead

÷

Total Expected

Use of Cost Drivers

=

Activity-Based

Overhead Rates

Employee training

$120,000

$1,500,000 Direct labor dollars

$.08 per DL dollar

(2) Assignment of overhead to corporate and individual services:

Corporate

Individual

Activity Cost Pool

Expected

Use of

Driver

Overhead

Rate

Cost

Assigned

Expected

Use of

Driver

Overhead

Rate

Cost

Assigned

Computing

Facility rental

Travel

Overhead assigned

Employee training

$900,000

$.08

$ 72,000

$600,000

$.08

$ 48,000

PROBLEM 4-5C (Continued)

(c)

Activity

Value-Added vs. Non-value-Added

Employee training

Typing and secretarial

Non-value-added

Value-added

(d) Overhead is assigned to the two service lines as follows:

Corporate

Individual

Difference

Traditional costing

$289,800

$193,200

Computing

Travel

Value-added

Non-value-added