Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

ACR 4-4 (Continued)

(h)

Date

Account Titles

Debit

Credit

July 31 Service Revenue ...................................................... 39,120

Income Summary ........................................... 39,120

31 Income Summary .................................................... 32,350

Salaries and Wages Expense ........................ 22,000

Rent Expense .................................................. 4,000

(i)

GREEN RIVER COMPUTER CONSULTANTS

Post-Closing Trial Balance

July 31, 2017

Debit

Credit

Cash ...............................................................

$ 52,630

Accounts receivable .....................................

13,000

Accumulated depreciation—equipment ......

$ 500

Accounts payable .........................................

3,000

Interest payable ............................................

100

Salaries and wages payable ........................

11,000

Income taxes payable ...................................

1,200

CT 4-1 FINANCIAL REPORTING PROBLEM

(a) Items that may result in adjusting entries for deferrals are:

2. Other current assets (prepaid expenses).

4. Deferred revenue.

2. Accrued revenues (other income)

(c) Depreciation and amortization expense was $7,946 (millions) in 2014

(d) The statement of cash flows (at the bottom) reports income taxes paid

CT 4-2 COMPARATIVE ANALYSIS PROBLEM

Accounts that provide evidence of the use of accrual accounting are:

Balance Sheet

Income Statement

(a) Columbia Company

2.

4.

Prepaid expenses

Accrued liabilities

2.

4.

Insurance (or supplies) expense

Miscellaneous expense

(b) VFC

2.

4.

Accounts receivable, less allowance

for doubtful accounts

Deferred income taxes

2.

4.

Sales

Income tax expense

LO 1 BT: AN Difficulty: Medium TOT: 20 min. AACSB: Analytic AICPA FC: Reporting

CT 4-3 COMPARATIVE ANALYSIS PROBLEM

Accounts that provide evidence of the use of accrual accounting are:

Balance Sheet

Income Statement

(a) Amazon Company

1.

3.

Accounts receivable, net and other

Unearned revenue

1.

3.

Product or Service Sales

Product or Service revenue

(b) Wal-Mart

2.

4.

Accumulated depreciation

Accrued liabilities

2.

4.

Depreciation expense

Miscellaneous expense

CT 4-4 INTERPRETING FINANCIAL STATEMENTS

LASER RECORDING SYSTEMS

(a) Laser Recording is handling legal expense via an accrued expense

adjustment. This is explained by the fact that accrued professional

services increased during the year.

CT 4-5 REAL-WORLD FOCUS

(a) The SEC was created by Congress after the stock market crash of 1929.

The SEC was created to restore investor confidence in our capital

markets by providing more structure and government oversight.

(b) Division of Corporation Finance. The Division of Corporation Finance

oversees corporate disclosure of important information to the

investing public. Corporations are required to comply with regulations

pertaining to disclosure that must be made when stock is initially sold

Division of Trading and Markets. The Division of Trading and Markets

establishes and maintains standards for fair, orderly, and efficient markets.

It does this primarily by regulating the major securities market partici-

pants: broker-dealer firms; self-regulatory organizations (SROs), which

include the stock exchanges and the National Association of Securities

Dealers (NASD), Municipal Securities Rulemaking Board (MSRB), and

clearing agencies (SROs that help facilitate trade settlement); transfer

CT 4-5 (Continued)

Division of Enforcement. The Division of Enforcement investigates

possible violations of securities laws, recommends Commission action

when appropriate, either in a federal court or before an administrative

Division of Economic and Risk Analysis

The Division of Economic and Risk Analysis assists the Commission in

executing its mission to protect investors, maintain fair, orderly, and

efficient markets, and facilitate capital formation by integrating robust

economic analysis and rigorous data analytics into the work of the SEC.

There are two main functions for the Division. First, DERA staff provide

vital support in the form of economic analyses in support of Commission

rulemaking and policy development. Second, the Division also provides

( c ) Office of the Chief Accountant

The Chief Accountant is appointed by the Chairman to be the principal

adviser to the Commission on accounting and auditing matters. The Office

of the Chief Accountant assists the Commission in executing its

responsibility under the securities laws to establish accounting principles,

CT 4-5 (Continued)

In addition to its responsibility for accounting standards, the Commission

is responsible for the approval or disapproval of auditing rules put forward

by the Public Company Accounting Oversight Board, a private-sector

regulator established by the Sarbanes-Oxley Act to oversee the auditing

profession. The Commission also has thorough-going oversight

responsibility for all of the activities of the PCAOB, including approval of

CT 4-6 GROUP DECISION CASE

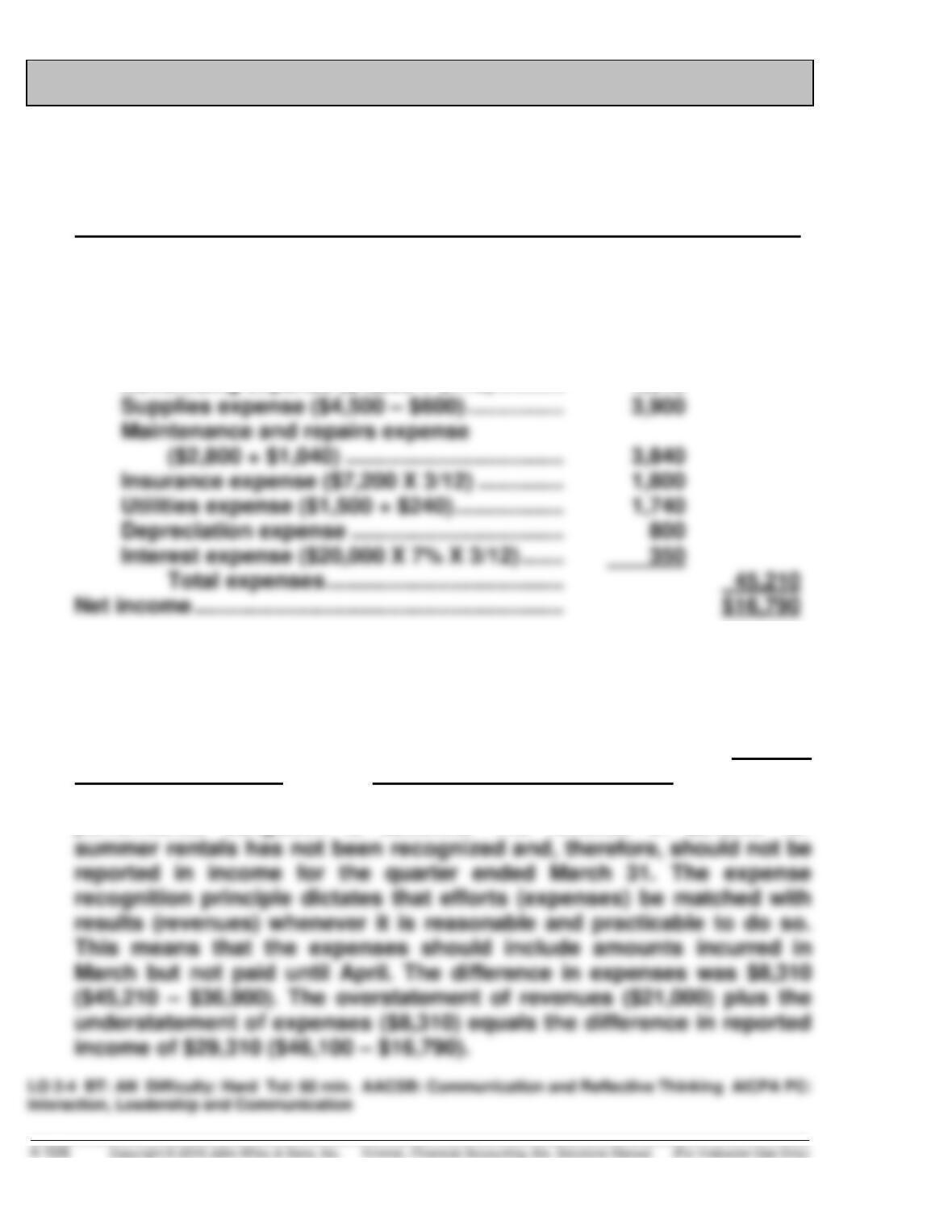

(a) ABBEY PARK

Income Statement

For the Quarter Ended March 31, 2017

Revenues

Rent revenue ($83,000 – $21,000) ................ $62,000

Expenses

Salaries and wages expense

[$27,600 + ($290 X 3)] ............................. $28,470

Advertising expense ($4,200 + $110) ........... 4,310

(Revenues are recognized when a service has been provided and expenses are recognized

when an asset is used up or a service is used)

(b) The generally accepted accounting principles pertaining to the income

statement that were not recognized by Trudy were the revenue

recognition principle and the expense recognition principle. The revenue

recognition principle states that revenue is recognized when the

performance obligation is satisfied. The revenue of $21,000 for

CT 4-7 COMMUNICATION ACTIVITY

(a) Accrual-basis accounting records the events that change an entity’s

financial statements in the periods in which the events occur, rather than

in the periods in which the entity receives or pays cash. Information

presented on an accrual-basis is useful because it reveals relationships

(b) Politicians might desire a cash-basis accounting system over an accrual-

basis system because if an accrual accounting system is used, it could

(c) Dear Senator,

It is my understanding, after having taken a beginning course in account-

ing principles, that the federal government uses a cash-basis

accounting system rather than an accrual-basis accounting system.

CONCERNED STUDENT

LO 1 BT: S Difficulty: Hard TOT: 45 min. AACSB: Communication and Reflective Thinking AICPA PC:

Communication AICPA BB: Critical Thinking

CT 4-8 ETHICS CASE

(a) The stakeholders in this situation are:

(b) 1. It is unethical for the president to place pressure on Tim to mis-

state net income by requesting him to prepare incorrect adjusting

entries.

(c) Tim can accrue revenues and defer expenses through the preparation

of adjusting entries and be ethical so long as the entries reflect

CT 4-9 ALL ABOUT YOU ACTIVITY

The following is a personal balance sheet using the classified presentation.

Note that the earnings from the part-time job as well as the tuition costs are

not listed since neither of those items is an asset, liability, or equity item.

Assets

Current assets

Cash .................................................................. $1,200

Money market account .................................... 1,800

Property, plant, and equipment

Automobile ....................................................... 7,000

Liabilities and Owner’s Equity

Current liabilities

Current portion of automobile loan ................ $1,500

Current portion of credit card payable ........... 150

Equity

M. Y. Own, Capital ($15,350 – $12,300) ........... 3,050

CT 4-10 FASB CODIFICATION ACTIVITY

(a) Revenues are “inflows or other enhancements of assets of an entity or

settlements of its liabilities (or a combination of both) from delivering

IFRS 4-1 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) Note 1.25 states that revenue includes shipment and transportation

costs re-billed to customers only when these costs are included in

products’ selling prices as a lump sum. Revenue is presented net of all

(b) Note 1.25 state that revenue and the corresponding trade receivables

are reduced by the estimated amount of such returns, and a

(c) Louis Vuitton could have adjustments for prepayments such as:

Depreciation expense, Amortisation of intangible assets, Deferred tax

assets.