CHAPTER 4

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 4-1B

(a) Computation of unit costs—traditional costing.

VideoPlus, Inc.

Products

Manufacturing Costs

Standard Model

Deluxe Model

Total unit cost

Direct materials

Direct labor

$11

18

$42

18

(b) VideoPlus, Inc.

Activity Cost Pool

Estimated

Overhead

÷

Expected

Use of Cost Drivers

=

Activity-Based

Overhead Rate

Packing and shipping

$ 2.4375 per pound

Purchasing

Receiving

$ 126,000

30,000

400 Orders

20,000 Pounds

$315.00 per order

$ 1.50 per pound

(c) VideoPlus, Inc.

Standard Model

Deluxe Model

Activity Cost Pool

Expected

Use of

Drivers

X

Overhead

Rates

=

Cost

Assigned

Expected

Use of

Drivers

X

Overhead

Rates

=

Cost

Assigned

Purchasing

Receiving

Assembling

100

4,000

20,000

$315.00

$ 1.50

$ 6.00

$ 31,500

6,000

120,000

300

16,000

54,000

$315.00

$ 1.50

$ 6.00

$ 94,500

24,000

324,000

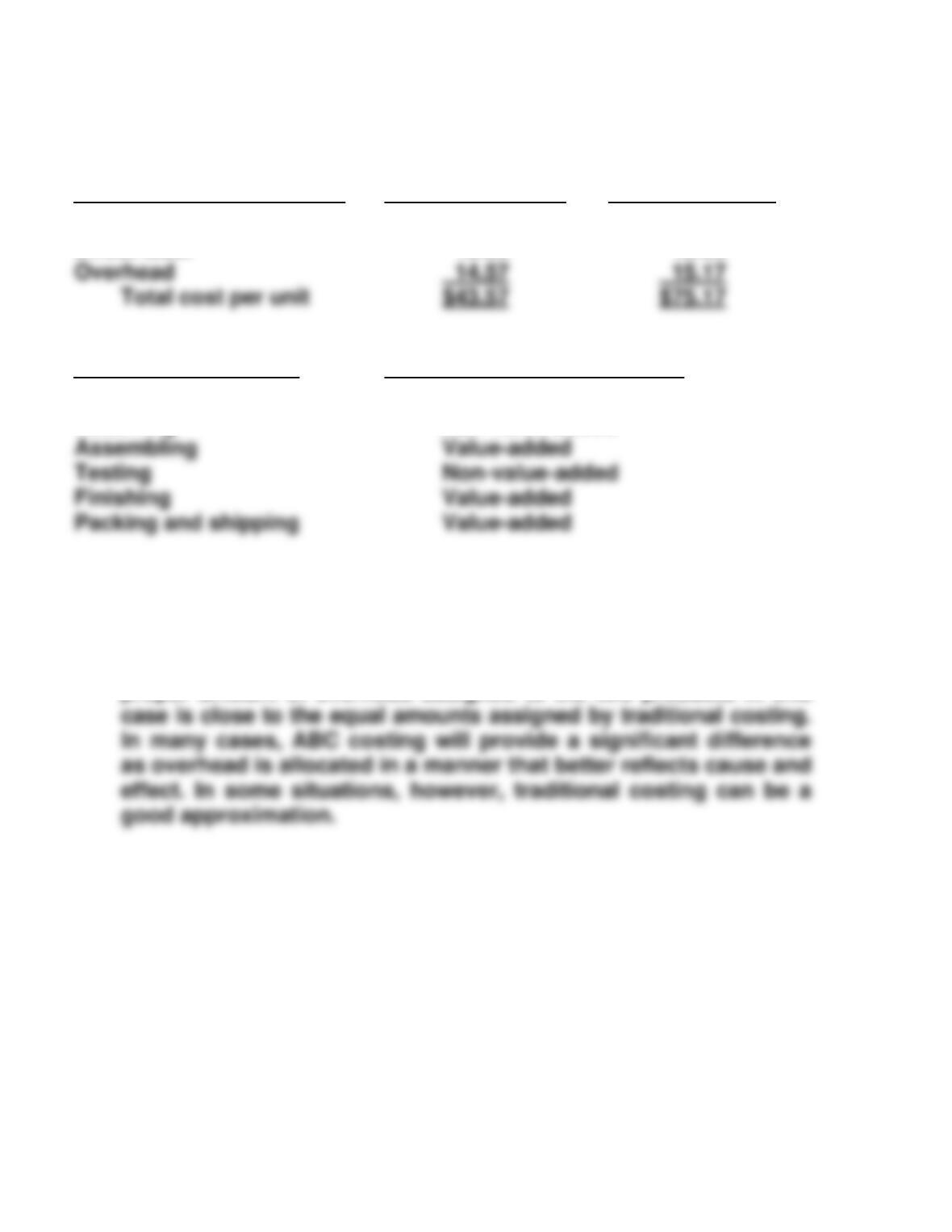

Overhead cost per unit

$15.17

PROBLEM 4-1B (Continued)

(d) VideoPlus, Inc.

ABC Manufacturing Costs

Standard Model

Deluxe Model

Direct materials

Direct labor

$11.00

18.00

$42.00

18.00

(e)

Activity

Value- vs. Non-value-added

Testing

Purchasing

Receiving

Non-value-added

Non-value added

(f) (1) Activity-based costing shows the standard model absorbs about

the same overhead per unit as the deluxe model.

(2) The comparison of ABC and traditional costing shows that the

proper amount of overhead assigned to the two products in this

Total cost per unit

PROBLEM 4-2B

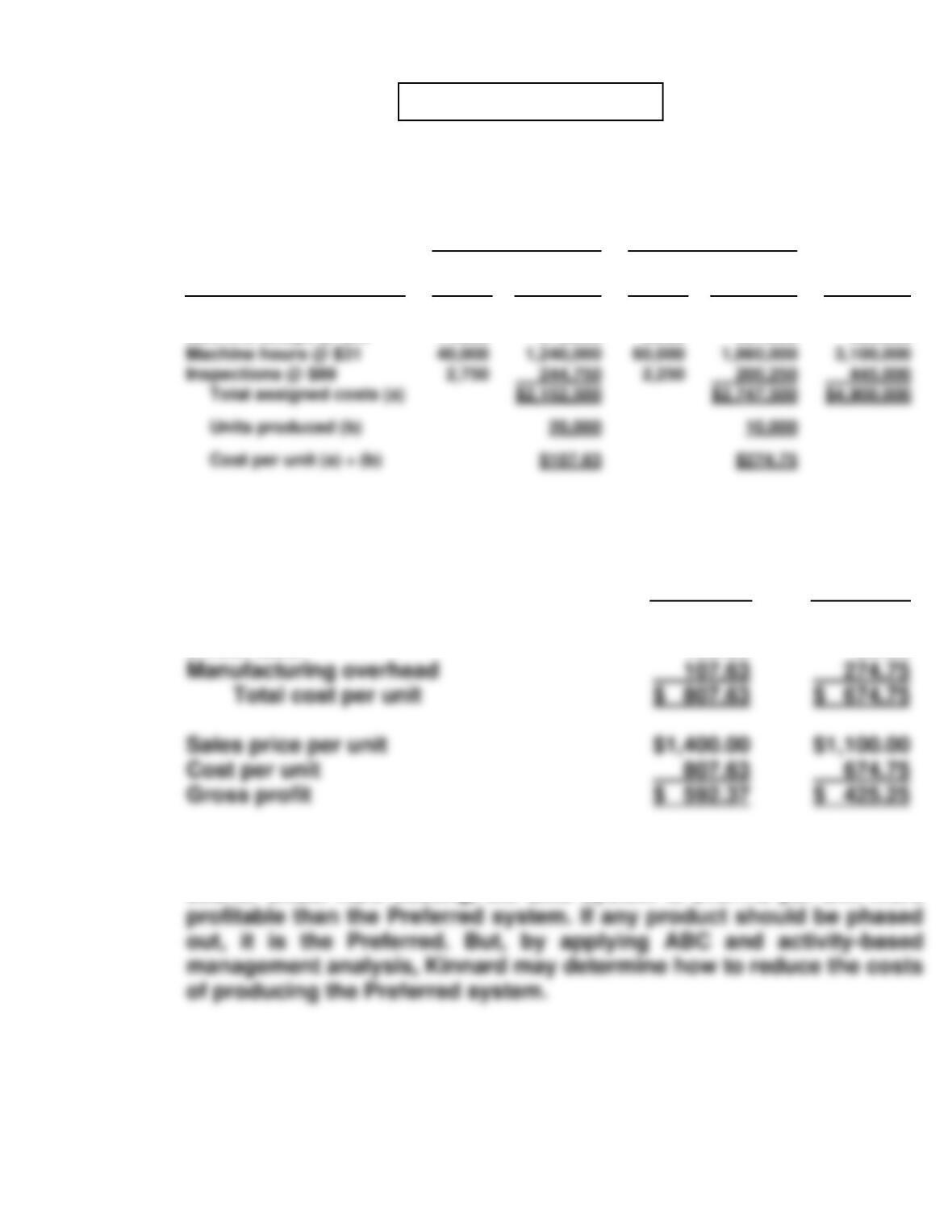

(a) The allocation of total manufacturing overhead using activity-based

costing is as follows:

Elite

Preferred

Overhead Rate

Drivers

Used

Cost

Assigned

Drivers

Used

Cost

Assigned

Total

Overhead

Purchase orders @ $31

Machine setups @ $29

11,250

11,000

$ 348,750

319,000

13,750

9,000

$ 426,250

261,000

$ 775,000

580,000

(b) The cost per unit and gross profit of each model under ABC costing

were:

Elite

Preferred

Direct materials

Direct labor

$ 600.00

100.00

$ 320.00

80.00

(c) Management’s future plans for the two home theater systems are not

sound. Under ABC costing, the Elite system is $167.12 per unit more

Cost per unit (a) ÷ (b)

$107.63

$274.75

PROBLEM 4-3B

(a) Predetermined overhead rate using materials cost:

(b) Manufacturing cost per armoire under traditional costing:

Direct materials ……………………………………………………… $ 5,200

Direct labor ……………………………………………………………. 3,500

(c) Manufacturing cost per armoire under activity-based costing:

Computation of Activity-Based Overhead Rate

Activity Cost Pools

Estimated

Overhead

÷

Total

Estimated Drivers

=

Activity-Based

Overhead Rate

Utilities

50,000 Sq. ft.

$ 2 per sq. ft.

Purchasing

Handling materials

$ 45,000

50,000

500 Orders

5,000 Moves

$90 per order

$10 per move

Activity Cost Pools

Expected Use of

Drivers

X

Activity-Based

Overhead Rate

=

Cost Assigned

Purchasing

Handling materials

3 Orders

32 Moves

$90

$10

$ 270

320

PROBLEM 4-3B (Continued)

Total manufacturing cost per armoire under ABC:

Direct materials ……………………………………………………………. $ 5,200

Direct labor ………………………………………………………………….. 3,500

(d) The difference between the traditional cost and the activity-based cost

per unit, $1,201.67 versus $1,020.83, is not great in amount but $180.84

or ($1,201.67 – $1,020.83) is 17.7% of the more correct ABC cost per

PROBLEM 4-4B

(a) Computation of unit costs—traditional costing

Overhead cost per labor hour is $1,150,000 ÷ (30,000 + 20,000) =$23

Products

Manufacturing Costs

Valley Fresh

Merando Valley

Direct materials

$1.35

$3.60

(b)

Activity Cost Pools

Estimated

Overhead

Expected Use

of Cost Drivers

Activity-Based

Overhead Rates

$225.00 per inspection

Grape processing

Aging

$ 146,000

420,000

8,000

3,000,000

$ 18.25 per cart

$ 0.14 per month

(c)

Valley Fresh

Merando Valley

Activity Cost Pool

Expected

Use of

Drivers

X

Overhead

Rates

=

Cost

Assigned

Expected

Use of

Drivers

X

Overhead

Rates

=

Cost

Assigned

gallon [(a) ÷ (b)]

Grape processing

Aging

6,000

600,000

$ 18.25

$ 0.14

$109,500

84,000

2,000

2,400,000

$ 18.25

$ 0.14

$ 36,500

336,000

PROBLEM 4-4B (Continued)

(d)

Products

Manufacturing Costs

Valley Fresh

Merando Valley

Direct materials

$1.350

$3.600

(e) To: Mr. Frankie Merando

From: Student

Subject: Product costs using traditional approach versus ABC

The memorandum covers the following points:

a. ABC allocates overhead costs as a function of each product’s use

of cost drivers. Thus, ABC results in overhead allocation that

more closely approximates each product’s generation of overhead

costs.

PROBLEM 4-4B (Continued)

d. The total cost of the two products under the two approaches was

as follows:

Valley Fresh

Merando Valley

Traditional approach

$3.25

$7.40

ABC

PROBLEM 4-5B

(a) Computation of assigned overhead under traditional costing (“direct

labor dollars” appears in the first line of the schedule of overhead

data):

Predetermined overhead rate X direct labor dollars

(b) 1. Computation of activity-based overhead rates:

Activity Cost Pool

Estimated

Overhead

÷

Total Expected

Use of Cost Drivers

=

Activity-Based

Overhead Rates

Employee training

Typing and secretarial

$120,000

60,000

$1,600,000 Direct labor dollars

2,000 Reports/forms

$.075 per DL dollar

$30 per report/form

2. Assignment of overhead to corporate and individual services:

Corporate

Individual

Activity Cost Pool

Expected

Use of

Driver

Overhead

Rate

Cost

Assigned

Expected

Use of

Driver

Overhead

Rate

Cost

Assigned

Computing

Facility rental

Travel

Overhead assigned

Employee training

Typing and secretarial

$900,000

500

$.075

$30

$ 67,500

15,000

$700,000

1,500

$.075

$30

$ 52,500

45,000

PROBLEM 4-5B (Continued)

(c) Overhead is assigned to the two service lines as follows:

Corporate

Individual

Traditional costing

$270,000

$210,000