Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-1

CHAPTER 4

Process Costing and Hybrid Product-Costing

Systems

ANSWERS TO REVIEW QUESTIONS

4-1 In a job-order costing system, costs are assigned to batches or job orders of

production. Job-order costing is used by firms that produce relatively small numbers

4-2 Process costing would be an appropriate product-costing system in the following

4-3 Process costing could be used in the following nonmanufacturing enterprises:

4-4 Product-costing systems are used for the following purposes:

(a) In financial accounting: Product costs are needed to value inventory on the

4-5 An equivalent unit is a measure of the amount of productive effort applied in the

4-2

4-6 The following four steps are used in process costing:

4-7 (a) Journal entry to enter direct-material costs into Work-in-Process Inventory

account:

4-8 Transferred-in costs are the costs assigned to partially completed products that

4-9 The $182,000 of transferred-in costs were incurred prior to January 1 and in the

4-10 The name ”weighted-average method” comes from the fact that the cost per

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-3

4-11 The difference between normal and actual costing lies in the calculation of the

manufacturing-overhead cost of the current period. Under actual costing, the

4-12 If manufacturing overhead were applied according to some activity base (or cost

4-13 Operation costing is a hybrid product-costing system that is used when conversion

activities are very similar across product lines, but the direct materials differ

4-14 The departmental production report is the key document in a process-costing

system rather than the job-cost sheet used in job-order costing. The departmental

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-4

SOLUTIONS TO EXERCISES

EXERCISE 4-15 (10 MINUTES)

The general formula for all three cases is the following:

Using this formula, the missing amounts are:

9,000 pounds

12,500 yards

72,000 liters

EXERCISE 4-16 (20 MINUTES)

CALCULATION OF EQUIVALENT UNITS: HEALTHY LIFE STYLES, INC.

Weighted-Average Method

Physical

Units

Percentage

of

Completion

with

Respect to

Direct

Material

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, January 1 ….

30,000

70%

50%

Units started during the year ..

140,000

Total units to account for ……..

170,000

Work in process, December 31

75%

20%

Total units accounted for ……..

170,000

_______

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-5

EXERCISE 4-17 (15 MINUTES)

CALCULATION OF EQUIVALENT UNITS: PETROTECH COMPANY – AMARILLO PLANT

Weighted-Average Method

Physical

Units

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

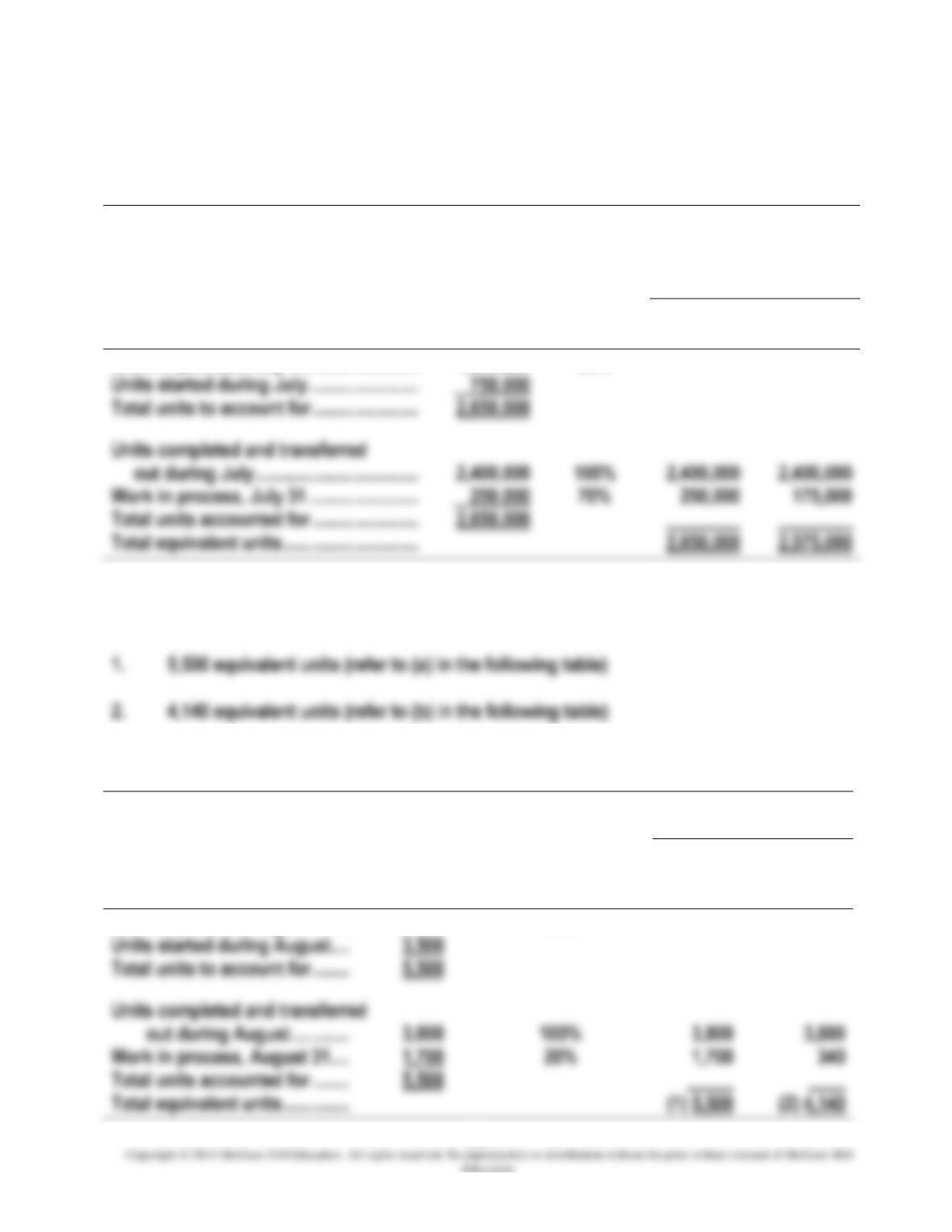

Work in process, July 1 ……………………..

1,900,000

30%

Units started during July ……………………

Total units to account for …………………..

2,650,000

Work in process, July 31 ……………………

70%

Total units accounted for …………………..

2,650,000

EXERCISE 4-18 (15 MINUTES)

5,500 equivalent units (refer to (a) in the following table)

CALCULATION OF EQUIVALENT UNITS: ANDROMEDA GLASS COMPANY

Weighted-Average Method

Physical

Units

Percentage

of

Completion with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, August 1 ……

2,000

60%

Units started during August ….

3,500

Total units to account for ……..

5,500

Work in process, August 31 ….

1,700

20%

340

4-6

EXERCISE 4-19 (30 MINUTES)

EXERCISE 4-20 (15 MINUTES)

CALCULATION OF COST PER EQUIVALENT UNIT: DULUTH GLASS COMPANY

Weighted-Average Method

Direct

Material

Conversion

Total

Work in process, February 1 ………………

$ 43,200

$ 40,300

$ 83,500

Costs incurred during February …………

Total costs to account for ………………….

$230,300

$408,500

Equivalent units ………………………………..

Costs per equivalent unit …………………..

EXERCISE 4-21 (15 MINUTES)

CALCULATION OF COST PER EQUIVALENT UNIT: MONTANA LUMBER COMPANY

Weighted-Average Method

Direct

Material

Conversion

Total

Work in process, June 1 ……………………….

$ 74,900

$167,000

$ 241,900

Costs incurred during June ………………….

Total costs to account for …………………….

$792,000

$1,247,600

Equivalent units …………………………………..

6,700

Costs per equivalent unit ……………………..

4-7

EXERCISE 4-22 (25 MINUTES)

TUSCALOOSA PAPERBOARD COMPANY

Weighted-Average Method

Direct

Material

Conversion

Total

Work in process, March 1 …………………..

$ 10,900

$ 28,950

$ 39,850

Costs incurred during March ………………

Total costs to account for …………………..

$123,600

$189,150

$312,750

Equivalent units …………………………………

Costs per equivalent unit ……………………

1.

Cost of goods completed and

transferred out during March:

2.

Cost remaining in March 31 work

in process:

Total ……………………………………….

*Equivalent units in March 31 work in process:

Direct

Material

Conversion

Total equivalent units (weighted average) …………………..

103,000

97,000

Units completed and transferred out ………………………….

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-8

EXERCISE 4-23 (25 MINUTES)

RALEIGH TEXTILES COMPANY

Weighted-Average Method

Direct

Material

Conversion

Total

Work in process, November 1 ……………….

$ 85,750

$ 16,900

$ 102,650

Costs incurred during November ………….

Total costs to account for …………………….

$284,200

Equivalent units …………………………………..

Costs per equivalent unit ……………………..

$3.90

1.

Cost of goods completed and

transferred out during November:

2.

Cost remaining in November 30

work in process:

Total ………………………………………

*Equivalent units in November 30 work in process:

Direct

Material

Conversion

Total equivalent units (weighted average) ……………………

Units completed and transferred out …………………………..

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-9

EXERCISE 4-24 (45 MINUTES)

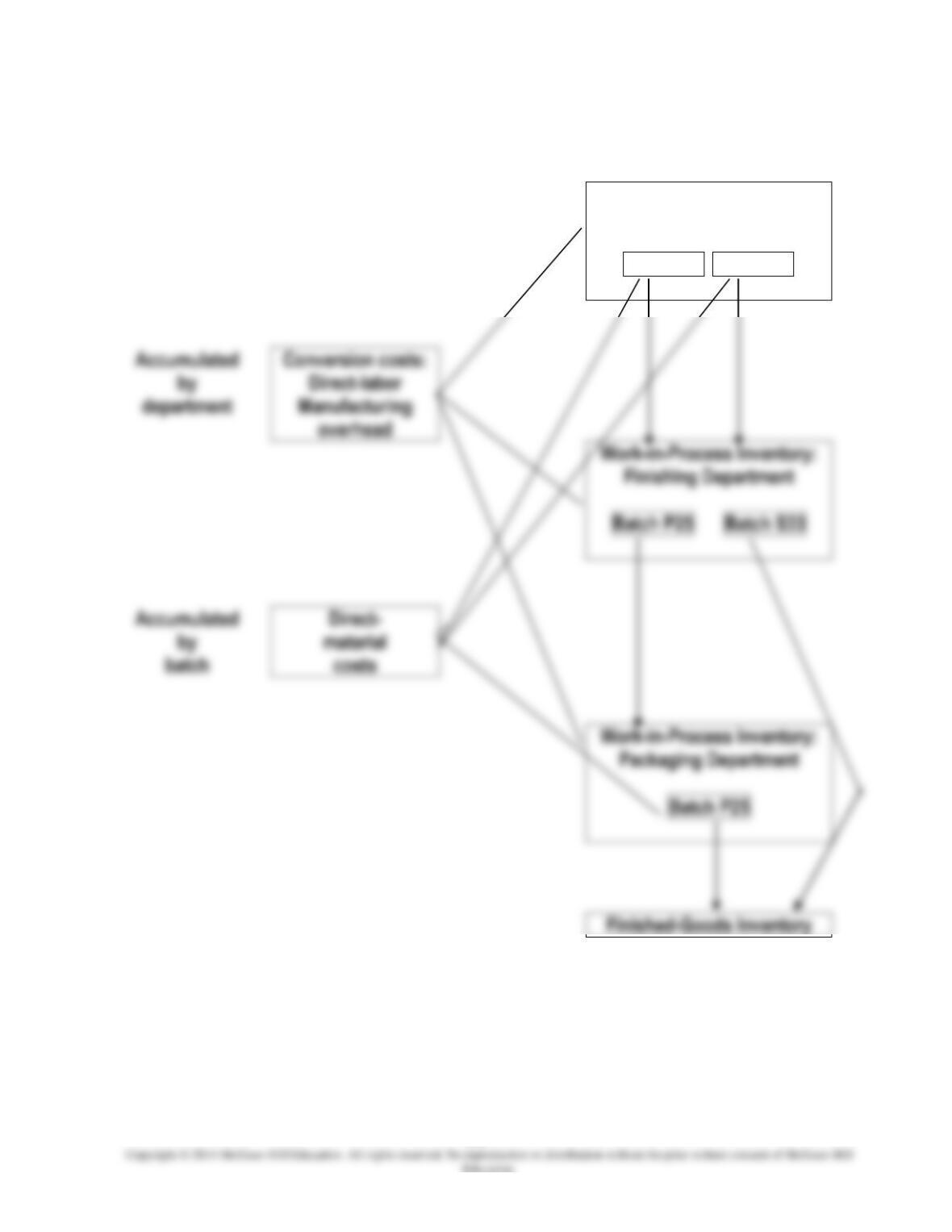

1. Diagram of production process:

Work-in-Process Inventory:

Preparation Department

Batch P25 Batch S33

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-10

EXERCISE 4-24 (CONTINUED)

2. The product cost for each basketball is computed as follows:

Professional

Scholastic

Direct material: …………………………………………………………..

Batch P25 ($42,000 ÷ 2,000) ……………………………………

$21.00

Batch S33 ($45,000 ÷ 4,000) ……………………………………

*Conversion: Packaging Department …………………………..

3.

Journal entries:

Work-in-Process Inventory: Preparation Department ……….

39,500*

Raw-Material Inventory ………………………………………….

39,500

Work-in-Process Inventory: Preparation Department ……….

45,000*

Raw-Material Inventory ………………………………………….

45,000

*Direct-material cost for batch S33.

Work-in-Process Inventory: Preparation Department ……….

45,000*

Applied Conversion Costs ……………………………………..

45,000

Work-in-Process Inventory: Finishing Department …………..

Work-in-Process Inventory: Preparation Department

*$129,500 = $39,500 + $45,000 + $45,000

4-11

EXERCISE 4-24 (CONTINUED)

Work-in-Process Inventory: Finishing Department …………..

36,000*

Applied Conversion Costs ……………………………………..

36,000

Work-in-Process Inventory: Packaging Department …………

66,500*

Finished-Goods Inventory ………………………………………………

Work-in-Process Inventory: Finishing Department ….

These are the costs accumulated for batch P25 only.

These are the costs accumulated for batch S33 only.

Work-in-Process Inventory: Packaging Department …………

Raw-Material Inventory ………………………………………….

Applied Conversion Costs ……………………………………..

*Cost of packaging material for batch P25.

Finished-Goods Inventory ………………………………………………

70,000*

Work-in-Process Inventory: Packaging Department ..

70,000

*$70,000 = $66,500 + $3,500

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-12

SOLUTIONS TO PROBLEMS

PROBLEM 4-25 (45 MINUTES)

1.

Physical flow of units:

Physical

Units

Work in process, June 1 …………………………………………………………………

40,000

Units started during June ……………………………………………………………….

Total units to account for ………………………………………………………………..

Units completed and transferred out during June …………………………….

Work in process, June 30 ……………………………………………………………….

2.

Equivalent units:

Physical

Units

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, June 1 ……….

40,000

38%

Units started during June ……..

Total units to account for ………

Units completed and transferred

180,000

Work in process, June 30 ……..

Total units accounted for ………

3.

Costs per equivalent unit:

Direct

Material

Conversion

Total

Work in process, June 1 ……………

$110,500

$ 22,375

$132,875

Costs incurred during June ………

Total costs to account for …………

$540,500

$342,375

$882,875

Equivalent units ……………………….

Costs per equivalent unit ………….

$2.35

4-13

PROBLEM 4-25 (CONTINUED)

4.

Cost of goods completed and transferred out during June:

Cost remaining in June 30 work-in-process inventory:

Direct material:

number of

cost per

Conversion:

number of

cost per

Total cost of June 30 work in process ……………………………………………….

$162,875

Check: Cost of goods completed and transferred out …………………………

$720,000

Cost of June 30 work-in-process inventory …………………………….

Total costs accounted for ………………………………………………………

$882,875

4-14

PROBLEM 4-26 (45 MINUTES)

1. Physical flow of units:

Physical

Units

Work in process, April 1 …………………………………………………………………

10,000

Units started during April ……………………………………………………………….

Total units to account for ……………………………………………………….………

Units completed and transferred out during April …………………………….

80,000

Work in process, April 30 ……………………………………………………………….

2.

Equivalent units:

Physical

Units

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, April 1 ………………

10,000

20%

Units started during April …………….

Total units to account for …………….

Units completed and

Work in process, April 30

30,000

Total units accounted for …………….

3.

Cost per equivalent unit:

Direct

Material

Conversion

Total

Work in process, April 1 …………………………..

$ 22,000

$ 4,500

$ 26,500

Costs incurred during April …………………………

Total costs to account for …………………………..

Equivalent units ………………………………………….

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-15

PROBLEM 4-26 (CONTINUED)

4.

Cost of goods completed and transferred out during April:

Cost remaining in April 30 work-in-process inventory:

Direct material:

Conversion:

Total cost of April 30 work-in–process ……………………………………………

$78,100

Check: Cost of goods completed and transferred out ……………………

Cost of April 30 work-in-process inventory ……………………….

Total costs accounted for ………………………………………………..

4-16

PROBLEM 4-27 (50 MINUTES)

1.

Physical flow of units:

Physical

Units

Work in process, 1/1/x4 …………………………………………………………………

210,000

Units started during 20×4 ………………………………………………………………

Total units to account for ………………………………………………………………

Units completed and transferred out during 20×4 …………………………..

Work in process, 12/31/x4 ……………………………………………………………..

2.

Equivalent units:

Physical

Units

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, 1/1/x4 ……………

Units started during 20×4 …………

Total units to account for …………

Units completed and transferred

out during 20×4 …………………..

Work in process, 12/31/x4 ………..

Total units accounted for …………

4-17

PROBLEM 4-27 (CONTINUED)

3.

Costs per equivalent unit:

Direct

Material

Conversion

Total

Work in process, 1/1/x4…………………………….

$ 300,000

$ 620,800a

Total costs to account for …………………………

Equivalent units ……………………………………….

Costs per equivalent unit ………………………….

$

aConversion cost

=

direct labor + overhead

=

direct labor + (100% direct labor)

200% direct labor

=

$620,800

bConversion cost

=

200% direct labor

200% $1,700,000

=

$3,400,000

c$1.30 = $1,703,000 ÷ 1,310,000

4-18

PROBLEM 4-27 (CONTINUED)

4.

Cost of ending inventories:

Cost of goods completed and transferred out:

Cost remaining in 12/31/x4 work-in-process inventory:

Direct material:

Conversion:

Total cost of 12/31/x4 work in process ……………………………………………..

Check: Cost of goods completed and transferred out ………………………

Cost of 12/31/x4 work-in-process inventory …………………………

Total costs accounted for ……………………………………………………

The cost of the ending work-in–process inventory is $923,800.

Ending finished-goods inventory: Of the 1,000,000 units completed during 20×4,

250,000 units remain in finished-goods inventory on December 31, 20×4. Therefore:

The cost of the ending finished-goods inventory is $1,200,000.

4-19

PROBLEM 4-28 (40 MINUTES)

1.

Equivalent units:

Physical

Units

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, August 1 …………..

40,000

80%

Units started during August …………

Total units to account for ……………..

Work in process, August 31 …………

30%

Total units accounted for ……………..

2.

Costs per equivalent unit:

Direct

Material

Conversion

Total

Costs per equivalent unit

$11.43*

Total costs to account for

$138,000

$1,089,680

3.

Cost of goods completed and transferred out during August:

4-20

PROBLEM 4-28 (CONTINUED)

4.

Cost remaining in August 31 work-in-process inventory:

Direct material:

percost

of number

Conversion:

percost

of number

Total cost of August 31 work in process …………………………………………….

Check: Cost of goods completed and transferred out …………………………

Total costs accounted for ………………………………………………………

5.

Journal entry:

Finished-Goods Inventory …………………………………………

Work-in-Process Inventory ……………………………….