Chapter 04 – Cash and Internal Controls

4-1

Chapter 4

Cash and Internal Controls

INSTRUCTOR’S MANUAL

Learning Objectives

LO4-1 Discuss the impact of accounting scandals and the passage of the

Sarbanes-Oxley Act.

LO4-2 Identify the components, responsibilities, and limitations of internal control.

LO4-3 Define cash and cash equivalents.

LO4-4 Understand controls over cash receipts and cash disbursements.

LO4-5 Reconcile a bank statement.

LO4-6 Account for employee purchases.

LO4-7 Identify the major inflows and outflows of cash.

Analysis

LO4-8 Assess cash holdings by comparing cash to noncash assets.

Chapter 04 – Cash and Internal Controls

4-2

Teaching Suggestions

Chapter 4 uses a movie theatre theme to introduce students to the basics of internal controls.

Part A begins with a discussion of occupational fraud and accounting scandals. In some

instances, managers have acted unethically in reporting their companies’ performance. Most

students are surprised by the fact that published financial statements contain fraudulent amounts.

This discussion flows into the need for regulation, such as the Sarbanes-Oxley Act, and internal

controls as outlined by the Committee of Sponsoring Organizations (COSO) of the Treadway

Commission. The components of an internal control system are discussed for a movie theatre, a

business familiar to most students.

The discussion of general internal controls in Part A then moves to a discussion of cash

controls in Part B. One reason for the focus on cash is that cash is the most liquid of a company’s

assets and therefore may be the easiest to lose internal control over. Discussion of cash receipts

and cash disbursements are provided, including checks, debit cards, and credit cards. An

illustrated example of a bank reconciliation is also provided. Since most students are familiar

with cash, the different forms of cash payments, and bank statements, relating internal controls to

cash topics makes the purpose and operation of internal controls more apparent.

Given the focus on internal controls related to cash, Part C then provides a discussion of how

cash is reported to those outside the company. It is briefly mentioned that cash is reported as an

asset in the balance sheet, but the discussion primarily focuses on reporting cash in the statement

of cash flows. The statement of cash flows presented is that of Eagle Golf Academy discussed in

Chapters 1—4. [Note: The detailed discussion of the statement of cash flows is saved for Chapter

11. Here, the statement is introduced briefly.] A good way to explain amounts reported in the

statement of cash flows is to refer students back to the original 10 external transactions of Eagle

Golf Academy introduced in Chapter 2. Which of the 10 transactions involved cash? These are

the ones reported in the statement of cash flows (see Illustration 4-12). Since adjusting entries

never involve cash, the adjusting entries discussed in Chapter 3 do not affect amounts reported in

the statement of cash flows.

The final section of the chapter involves cash analysis by computing the ratio of cash to

noncash assets. To continue the movie theatre theme, the chapter compares Regal Entertainment

Group to Cinemark Holdings. These two companies have very different ratios of cash to noncash

assets. The reasons for the differences in these ratios are explained.

Chapter 04 – Cash and Internal Controls

4-3

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

ts

s

Questions

Learning

Objective(s)

Topic

Time

(Min.)

1

LO4-1

Define occupational fraud

5

2

LO4-1

Explain internal control

5

3

LO4-1

Discuss what managerial stewardship means

5

4

LO4-1

Understand managers’ motivation to manipulate

5

5

LO4-1

Explain the fraud triangle

5

6

LO4-1

Outline the major provisions of the Sarbanes-Oxley

Act

5

7

LO4-2

Describe the components of internal control

5

8

LO4-2

Describe the difference between preventive controls

and detective controls

5

9

LO4-2

Explain separation of duties

5

10

LO4-2

Identify responsibility for internal control

5

11

LO4-2

Recognize limitations of internal control

5

12

LO4-2

Define collusion

5

13

LO4-2

Describe likelihood of fraud by top-level employees

5

14

LO4-3

Define cash and cash equivalents

5

15

LO4-3

Describe how to record a purchase with a check

5

16

LO4-4

Discuss controls for cash receipts

5

17

LO4-4

Describe how credit card sales are reported

5

18

LO4-4

Describe how debit card sales are reported

5

19

LO4-4

Discuss controls for cash disbursements

5

20

LO4-4

Understand a credit card

5

21

LO4-5

Identify the purpose of a bank reconciliation

5

22

LO4-5

Explain differences between the company’s and the

bank’s cash balance

5

23

LO4-5

Describe timing differences in the cash balance

5

24

LO4-5

Make adjustments related to the bank reconciliation

5

25

LO4-6

Explain purchase cards and a petty cash fund

5

26

LO4-6

Describe managerial control over employee

purchases with credit cards and the petty cash fund

5

27

LO4-7

Explain the relationship between the balance sheet

and statement of cash flows

5

28

LO4-7

Describe operating, investing, and financing cash

flows

5

29

LO4-8

Understand why analysis of the cash balance is

important

5

30

LO4-8

Compute the ratio of cash to noncash assets

5

Chapter 04 – Cash and Internal Controls

4-4

Brief

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

BE4-1

LO4-1

Identify terms associated with the Sarbanes-Oxley

Act

5

BE4-2

LO4-2

Identify terms associated with components of

internal control

5

BE4-3

LO4-2

Define control activities associated with internal

control

5

BE4-4

LO4-3

Identify cash and cash equivalents

5

BE4-5

LO4-4

Determine cash sales

5

BE4-6

LO4-4

Record cash expenditures

5

BE4-7

LO4-5

Identify terms associated with a bank reconciliation

5

BE4-8

LO4-5

Prepare a bank reconciliation

10

BE4-9

LO4-5

Reconcile timing differences in the bank’s balance

5

BE4-10

LO4-5

Reconcile timing differences in the company’s

balance

5

BE4-11

LO4-5

Record adjustments to the company’s cash balance

5

BE4-12

LO4-5

Prepare a bank reconciliation

5

BE4-13

LO4-6

Record employee purchases

5

BE4-14

LO4-7

Match types of cash flows with their definitions

5

BE4-15

LO4-7

Determine operating cash flows

5

BE4-16

LO4-7

Determine investing cash flows

5

BE4-17

LO4-7

Determine financing cash flows

5

BE4-18

LO4-8

Calculate the ratio of cash to noncash assets

5

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

E4-1

LO4-1

Answer true-or-false questions about occupational

fraud

15

E4-2

LO4-1

Answer true-or-false questions about the Sarbanes-

Oxley Act

15

E4-3

LO4-2

Answer true-or-false questions about internal

controls

15

E4-4

LO4-2

Determine control activity violations

15

E4-5

LO4-3

Calculate the amount of cash to report

15

E4-6

LO4-4

Discuss internal control procedures related to cash

receipts

10

E4-7

LO4-4

Discuss internal control procedures related to cash

disbursements

10

E4-8

LO4-4

Discuss internal control procedures related to cash

receipts

10

E4-9

LO4-5

Calculate the balance of cash using a bank

reconciliation

10

4-5

E4-10

LO4-5

Calculate the balance of cash using a bank

reconciliation

10

E4-11

LO4-5

Calculate the balance of cash using a bank

reconciliation

10

E4-12

LO4-6

Record transactions for employee purchases

10

E4-13

LO4-6

Record transactions for employee purchases

10

E4-14

LO4-7

Classify cash flows

10

E4-15

LO4-7

Calculate net cash flows

10

E4-16

LO4-7

Calculate operating cash flows

10

E4-17

LO4-7

Calculate investing cash flows

10

E4-18

LO4-7

Calculate financing cash flows

10

E4-19

LO4-7

Compare operating cash flows to net income

15

E4-20

LO4-8

Analyze the ratio of cash to noncash assets

15

Problems

Learning

Objective(s)

Topic

Time

(Min.)

P4-1A

LO4-4

Discuss control procedures for cash receipts

15

P4-2A

LO4-5

Prepare the bank reconciliation and record cash

adjustments

25

P4-3A

LO4-5

Prepare the bank reconciliation and record cash

adjustments

30

P4-4A

LO4-7

Prepare the statement of cash flows

15

P4-5A

LO4-7

Record transactions, post to the Cash T-account, and

prepare the statement of cash flows

40

P4-1B

LO4-4, 4-5

Prepare a bank reconciliation and discuss cash

procedures

20

P4-2B

LO4-5

Prepare the bank reconciliation and record cash

adjustments

25

P4-3B

LO4-5

Prepare the bank reconciliation and record cash

adjustments

30

P4-4B

LO4-7

Prepare the statement of cash flows

15

P4-5B

LO4-7

Record transactions, post to the Cash T-account, and

prepare the statement of cash flows

40

Additional

Perspectives

Topic

Time

(Min.)

AP4-1

Continuing Problem: Great Adventures

45

AP4-2

Financial Analysis: American Eagle Outfitters, Inc.

40

AP4-3

Financial Analysis: The Buckle, Inc.

40

AP4-4

Comparative Analysis: American Eagle Outfitters, Inc. vs. The

Buckle, Inc.

20

AP4-5

Ethics

20

AP4-6

Internet Research

30

AP4-7

Written Communication

25

Chapter 04 – Cash and Internal Controls

Chapter Quiz Questions

The following multiple-choice questions are 10 unique quiz questions that correspond to the 10

questions at the end of each chapter. Each question covers the same learning objective but with a

little different twist. The correct answer is highlighted in bold for each item.

LO4-1

1. Managers should act:

a. As creditors of the company.

LO4-1

2. Sarbanes-Oxley Act (SOX) was passed in response to:

a. Increasing inflation.

LO4-2

3. What is a direct purpose of internal controls?

LO4-3

4. Which of the following is considered cash for financial reporting purposes?

LO4-4

5. Which of the following generally would be considered a good internal control over cash

payments?

4-7

LO4-5

6. When preparing a bank reconciliation, nonsufficient funds (NSF) checks would be:

a. Added to the company’s cash balance.

LO4-5

7. When preparing a bank reconciliation, outstanding checks would be:

a. Added to the company’s cash balance.

LO4-6

8. At any given time, the amount of cash in the petty cash fund should equal:

a. All vouchers written during the accounting period.

LO4-7

9. Operating cash flows would include which of the following?

LO4-7

10. Financing cash flows would include which of the following?

Chapter 04 – Cash and Internal Controls

4-8

Alternate Let’s Review

Problem #1

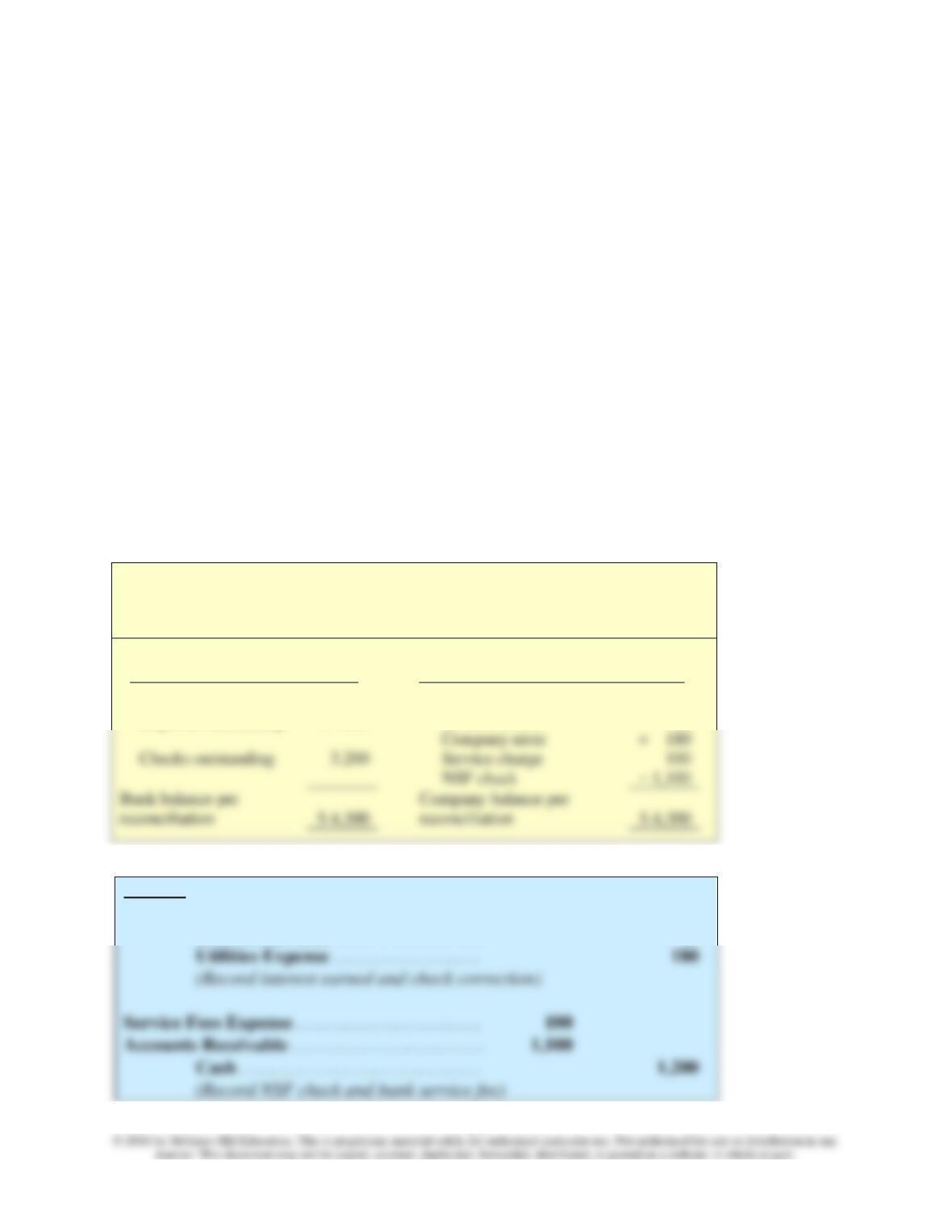

At the end of April, Classic Cinema’s accounting records show a cash balance of $5,240. The

April bank statement reports a cash balance of $6,700. The following information is gathered

from the bank statement and company records:

Checks outstanding $3,200 Customer’s NSF check $1,100

Deposits outstanding 800 Service fees 100

Interest earned 80

In addition, Classic discovered it correctly paid for utilities with a check for $350 but incorrectly

recorded the check in the company’s records for $530. The bank correctly processed the check

for $350.

Required:

1. Prepare a bank reconciliation for the month of April.

2. Adjust the balance of cash in the company’s records.

Solution:

1.

Classic Cinema

Bank Reconciliation

April 30

Bank’s Cash Balance

Company’s Cash Balance

Per bank statement

$ 6,700

Per general ledger

$ 5,240

Deposits outstanding

+ 800

Interest earned

+ 80

+ 180

Checks outstanding

Service charge

reconciliation

$ 4,300

reconciliation

$ 4,300

2.

April 30

Debit

Credit

Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

260

Interest Revenue . . . . . . . . . . . . . . . .

80

Chapter 04 – Cash and Internal Controls

4-9

Problem #2

A company reports in its current year each of the transactions listed below.

Required:

Indicate whether each transaction should be reported as an operating, investing, or financing cash

flow in the company’s statement of cash flows, and whether each is a cash inflow or outflow.

Transaction

Type of Cash Flow

Inflow or Outflow

1. Issue common stock for cash.

2. Receive cash from customers.

3. Sell equipment for cash.

4. Pay cash for advertising.

Solution:

Chapter 04 – Cash and Internal Controls

4-10

Key Points by Learning Objective

LO4-1 Discuss the impact of accounting scandals and the passage of the Sarbanes-Oxley

Act.

The accounting scandals in the early 2000s prompted passage of the Sarbanes-Oxley Act (SOX).

LO4-2 Identify the components, responsibilities, and limitations of internal control.

Internal control refers to a company’s plan to improve the accuracy and reliability of accounting

information and safeguard the company’s assets. Five key components to an internal control

LO4-3 Define cash and cash equivalents.

Cash includes currency, coins, balances in savings and checking accounts, and checks and

LO4-4 Understand controls over cash receipts and cash disbursements.

Because cash is the asset of a company most susceptible to employee fraud, controls over cash

LO4-5 Reconcile a bank statement.

In a bank reconciliation, we reconcile the bank’s cash balance for (1) cash transactions already

4-11

LO4-6 Account for employee purchases.

To make purchases on behalf of the company, some employees are allowed to use debit cards

LO4-7 Identify the major inflows and outflows of cash.

The statement of cash flows reports all cash activities for the period. Operating activities include

Analysis

LO4-8 Assess cash holdings by comparing cash to noncash assets.

Chapter 04 – Cash and Internal Controls

4-12

Common Mistakes

Common Mistake

debit card will result in a decrease in your cash account. The term debit card refers to the bank’s

The term debit card can cause some confusion for someone in the first accounting course.

Throughout this course, we refer to an increase in cash as a debit to cash. However, using your

Common Mistake

deposit, it views this as an increase to cash, so it records a debit to the Cash account. However,

the bank views this same deposit as an increase in the amount owed to the company, or a

liability, which is recorded as a credit. Similarly, a withdrawal of cash from the bank is viewed

Notice that bank statements refer to an increase (or deposit) in the cash balance as a credit and a

decrease (or withdrawal) as a debit. This terminology is the opposite of that used in financial

accounting, where debit refers to an increase in cash and credit refers to a decrease in cash. The

Common Mistake

its balance of cash downward to reverse the increase in cash it recorded at the time of deposit.

Students sometimes mistake an NSF check as a bad check written by the company instead of one

written to the company. When an NSF check occurs, the company has deposited a customer’s

Common Mistake

Some students try to update the Cash account for deposits outstanding, checks outstanding, or a

Chapter 04 – Cash and Internal Controls

4-13

Decision Points

Question

Accounting Information

Analysis

Does the company

maintain adequate

Management’s discussion,

auditor’s opinion

If management or the auditor notes

any deficiencies in internal controls,

Question

Accounting Information

Analysis

Should the company

allow its customers to

pay by using credit

Credit sales, service fee

expense, internal controls

When the benefits of credit card use

(increased sales, reduced handling of

cash by employees) exceed the costs

Question

Accounting Information

Analysis & Decision

Is the company able to

generate enough cash

from internal sources

Statement of cash flows

Cash flows generated from internal

sources include operating and

investing activities. For established

Chapter 04 – Cash and Internal Controls

4-14

Career Corner

Career Corner

Financial analysts offer investment advice to their clients—banks, insurance companies, mutual

funds, securities firms, and individual investors. This advice usually comes in the form of a

formal recommendation (buy, hold, or sell). Before giving an opinion, analysts develop a

Chapter 04 – Cash and Internal Controls

4-15

Ethical Dilemma

Ethical Dilemma

Suppose that you were sent to prison for a crime you did not commit. While in prison, the

warden learns that you have taken financial accounting and are really good at “keeping the

books.” In fact, you are so good at accounting that you offer to teach other inmates basic

financial skills that they’ll use someday after being released.

However, the warden plans to use his position of authority at the prison to steal money.

He uses prisoners as low-cost labor to do projects around town. Because other legitimate

companies cannot compete with these low costs, they bribe the warden not to bid on jobs. The

warden asks you to use your accounting skills to participate in a financial scam by falsifying

documents and creating a false set of accounting records that will allow the warden’s bribes to go

undetected by state prison authorities. In other words, he wants you to “cook the books.”

When you object to helping with this scam, the warden threatens to end your tutoring

sessions with other inmates and sentence you to solitary confinement. To further sway your

decision, he promises that if you’ll help, he’ll make your prison life easy by giving you special

meals and other favors.

What would you do in this situation? If you help the warden steal money, you benefit

personally and the other prisoners benefit by your continued tutoring sessions. However, the

warden often physically abuses the other prisoners, and helping him steal money means that he’ll

remain in his position for a long time, continuing his abusive behavior.

To see how Tim Robbins’s character handled this situation, check out the movie The

Shawshank Redemption.

Key Issues

• Benefitting personally vs. seeing others abused

Option 1: Continue to falsify the accounting records

• You need to take care of yourself in prison. Prison life has a different set of rules.

• You are not the one actually taking the bribes. You are merely following orders.

• You are not the one abusing other inmates.

• If you continue falsifying documents, you can continue to teach other inmates valuable

financial skills that will one day be essential when they are released from prison. This

serves a greater purpose.

Option 2: Discontinue falsifying the accounting records

• By falsifying documents, you are just as guilty as the person (warden) stealing the

money.

• If the state authorities discover this scheme, you could receive additional jail time.

• You are directly involved in helping the warden to force bribes from local companies.

This directly affects the finances of those companies (and their families).

Chapter 04 – Cash and Internal Controls

4-16

• By assisting the warden, you are directly linked to his abusive behavior of other inmates.

While you are not committing the physical abuse, you are helping to provide a setting

where it can continue.