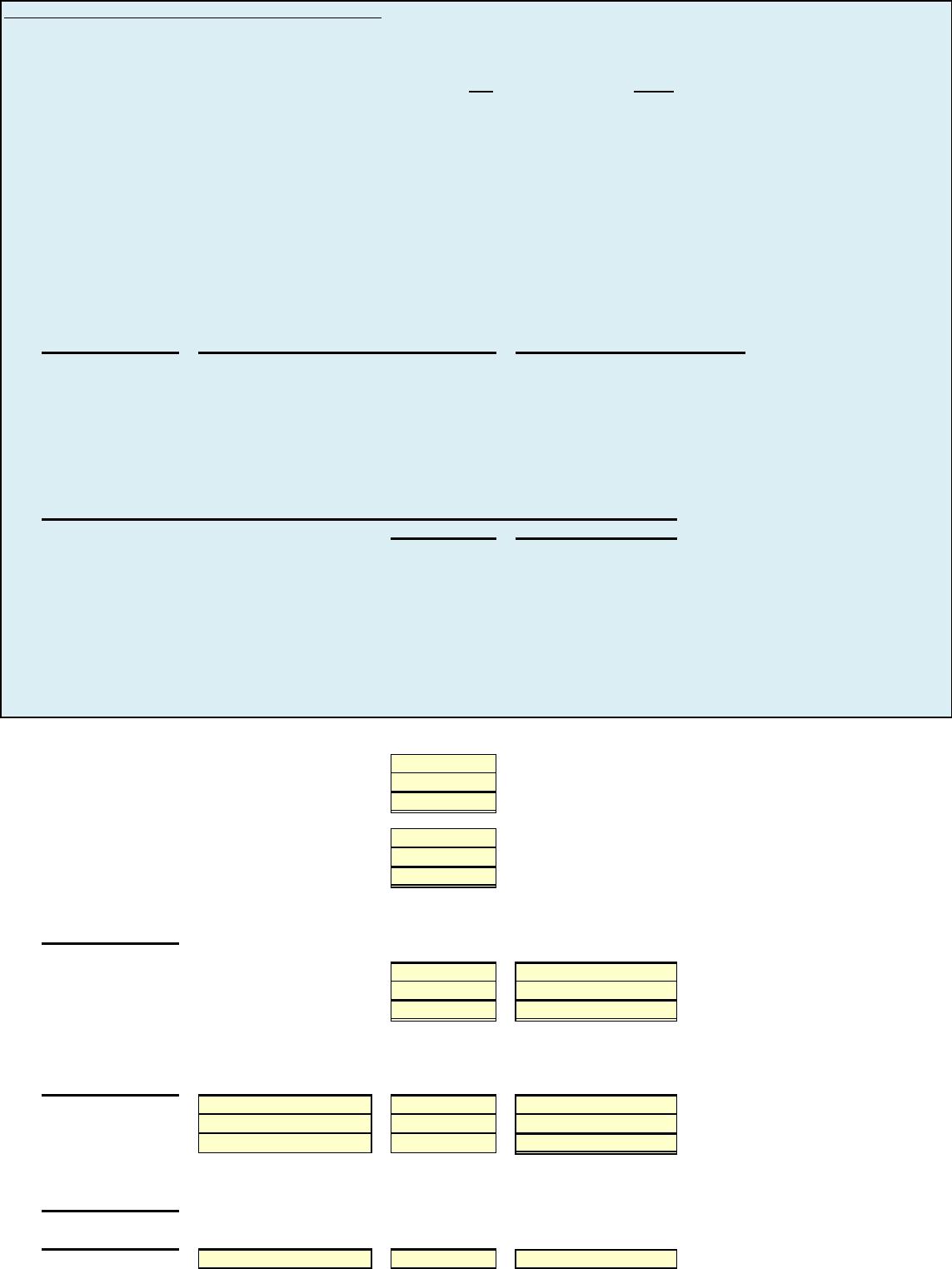

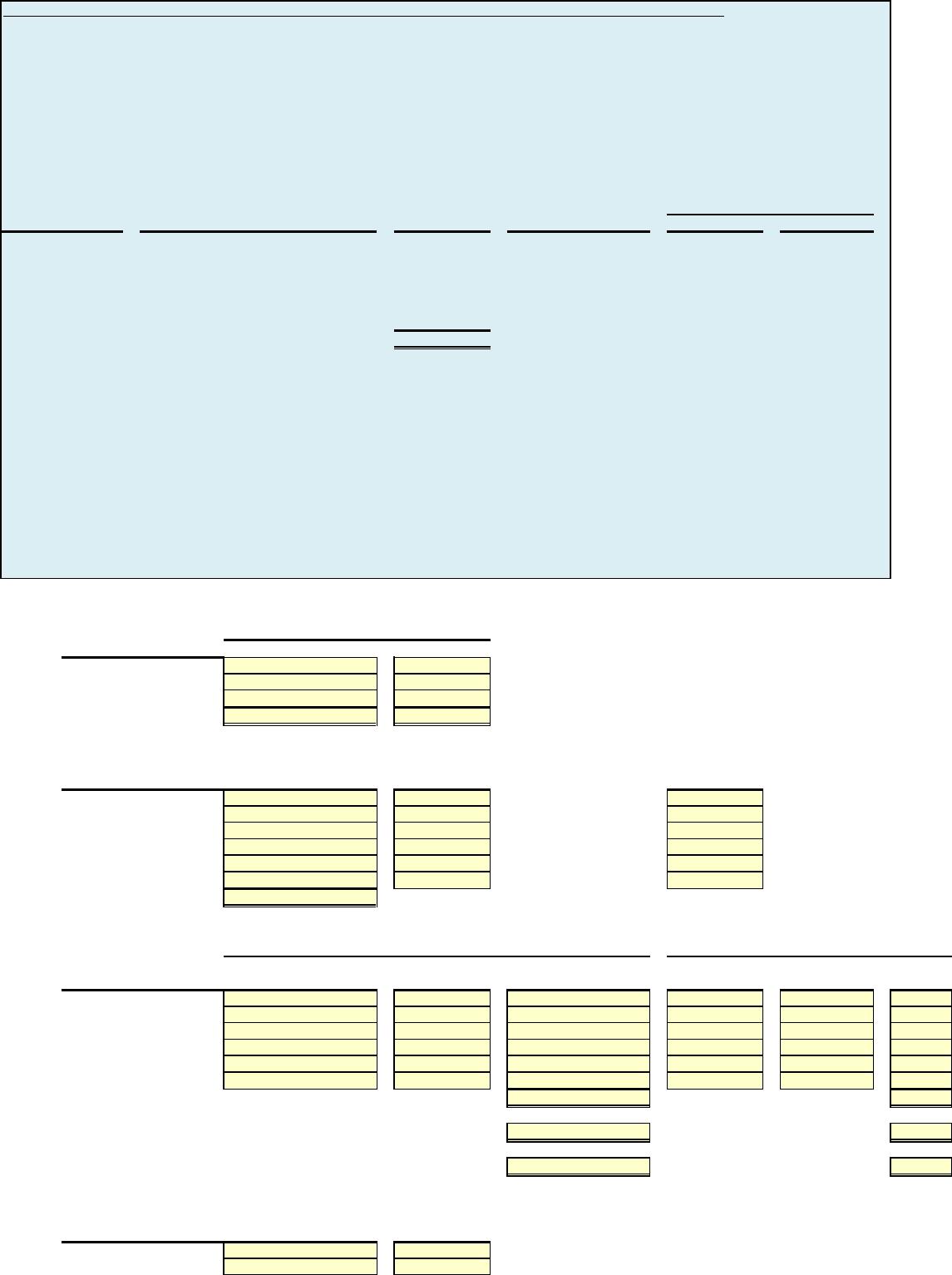

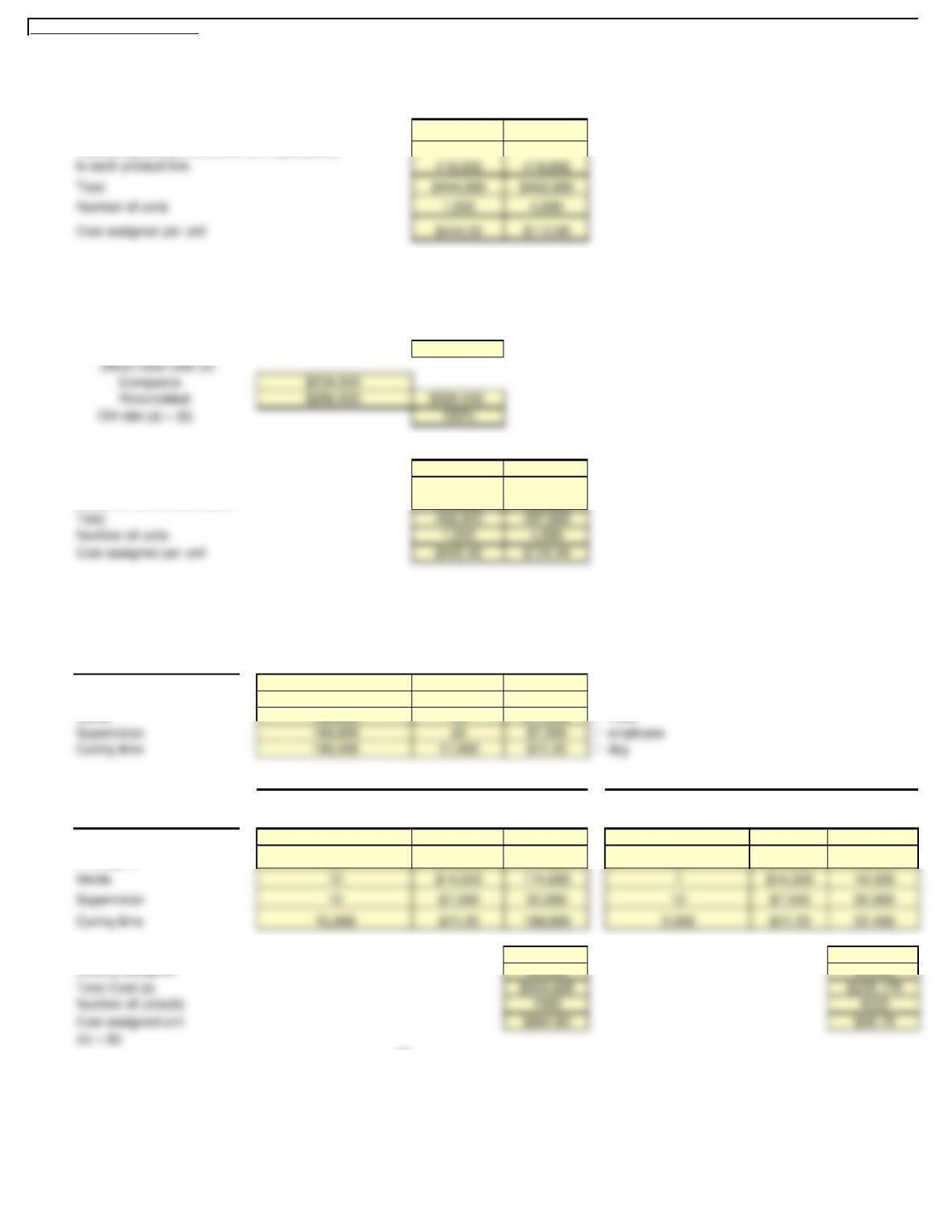

E4-1 Assign overhead using traditional costing and ABC

Saddle Inc. has two types of handbags: standard and custom. The controller has decided to use a plantwide

overhead rate based on direct labor costs. The president has heard of activity-based costing and wants to see how

the results would differ if this system was used. Two activity cost pools were developed: machining and machine

setup. Presented below is information related to the company’s operations.

Standard Custom

Direct labor costs $50,000 $100,000

Machine hours 1,000 1,000

Setup hours 100 400

Total estimated overhead costs are $240,000. Overhead cost allocated to the machining activity cost pool is

$140,000 and $100,000 is allocated to the machine setup activity cost pool.

Instructions

(a) Compute the overhead rate using the traditional (plantwide) approach.

(b) Compute the overhead rates using the activity-based costing approach.

(c) Determine the difference in allocation between the two approaches.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Estimated overhead = Predetermined overhead rate

Direct labor costs

= Value of direct labor cost

(b)

Machining

Machine setup

Machining:

= ? per machine hour

Machine setup:

= ? per setup hour

(c ) Traditional costing:

$50,000 x

POH rate

$100,000 x POH rate

Total OH allocation

Machining:

1,000 MH x OH rate

1,000 MH x OH rate

Machine setup:

100 Setup Hr x OH rate

400 Setup Hr x OH rate

?

?

Standard

Custom

?

?

?

?

?

Activity-based costing

Value

Value

Value

Standard

Custom

?

Machine hours

Setup hours

$140,000

100,000

Value

Activity-based overhead rates

Value

Value

Cost drivers

Activity cost pools

Estimated overhead

Total OH allocation

After you have completed E4-1, consider the additional question.

1. Assume that total estimated overhead costs are $285,000. Overhead cost allocated to the machining

activity cost pool is$150,000 and $135,000 is allocated to the machine setup activity cost pool.

Redo instructions (a) to (c).

?

?

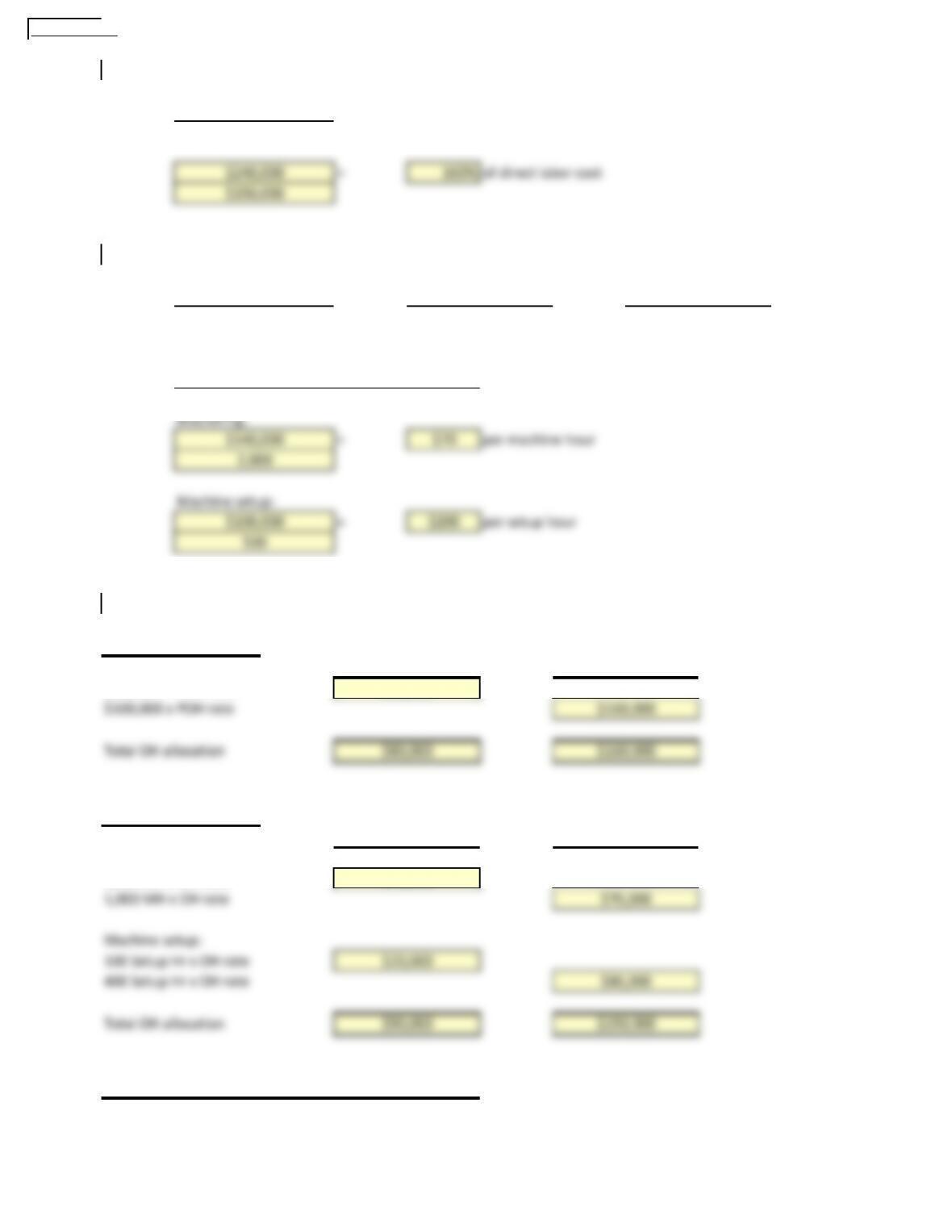

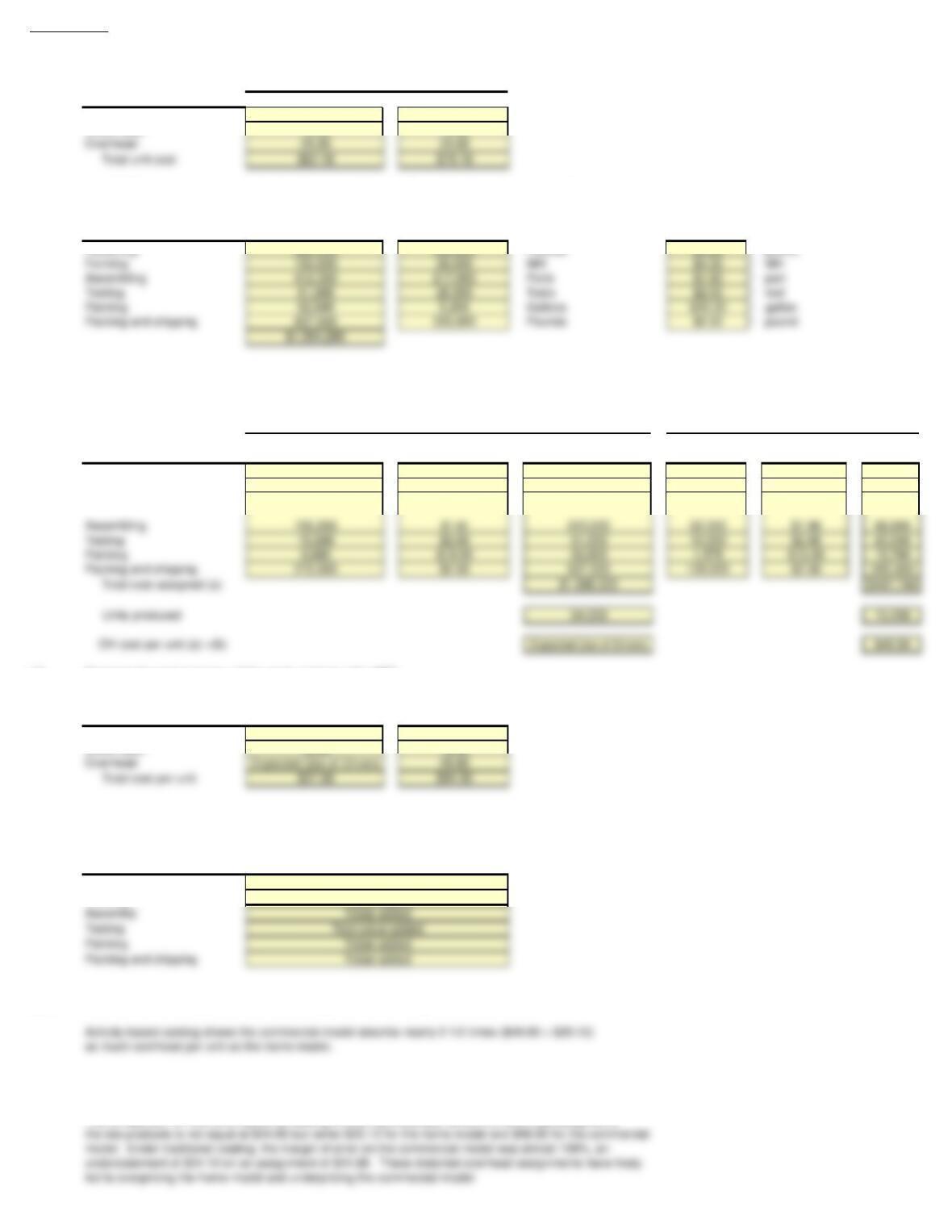

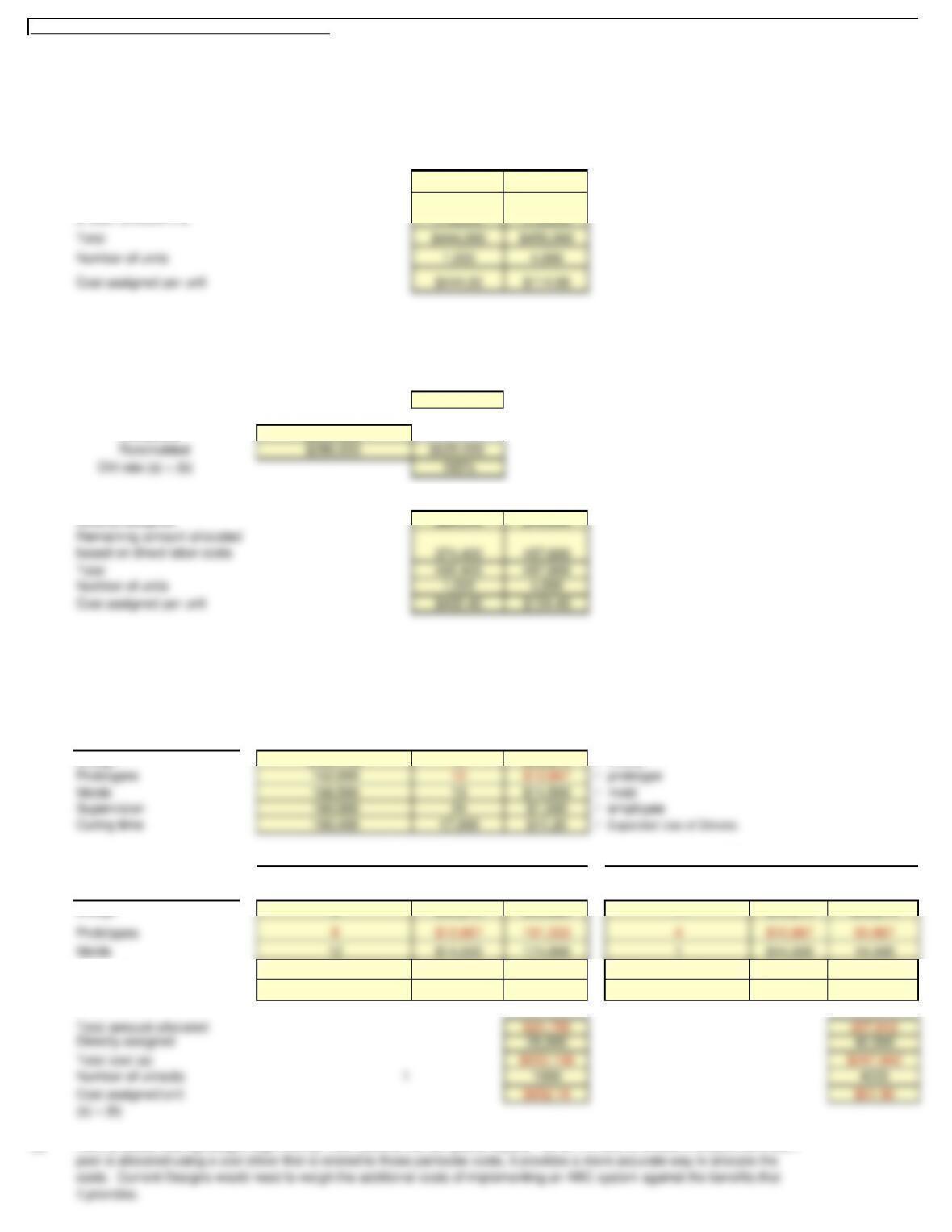

E4-1 Solution

(a) Compute the overhead rate using the traditional (plantwide) approach.

Estimated overhead = Predetermined overhead rate

Direct labor costs

(b) Compute the overhead rates using the activity-based costing approach.

Machining

Machine setup

(c) Determine the difference in allocation between the two approaches.

$50,000 x POH rate

$70,000

$20,000

$80,000

Machining:

1,000 MH x OH rate

The ABC method of OH allocation results in $10,000 ( $90,000 – $80,000) more in OH allocation to standard handbags

and $10,000 ($150,000 – $160,000) less OH allocation to custom handbags.

Difference between traditional costing and ABC:

Activity-based costing

Standard

Custom

$70,000

Standard

Custom

$80,000

Traditional costing:

Machine hours

$140,000

Activity cost pools

Cost drivers

Estimated overhead

Setup hours

100,000

Activity-based overhead rates

E4-1 Solution to Additional Question

1. Assume that total estimated overhead costs are $285,000. Overhead cost allocated to the machining

activity cost pool is $150,000 and $135,000 is allocated to the machine setup activity cost pool.

Redo instructions (a) to (c).

(a) Compute the overhead rate using the traditional (plantwide) approach.

Estimated overhead = Predetermined overhead rate

Direct labor costs

(b) Compute the overhead rates using the activity-based costing approach.

(c) Determine the difference in allocation between the two approaches.

$50,000 x

$75,000

$27,000

POH rate

Machining:

1,000 MH x OH rate

Difference between traditional costing and ABC:

$75,000

Standard

Custom

Traditional costing:

Standard

Custom

$95,000

Activity-based costing

Estimated overhead

Activity cost pools

Cost drivers

Activity-based overhead rates

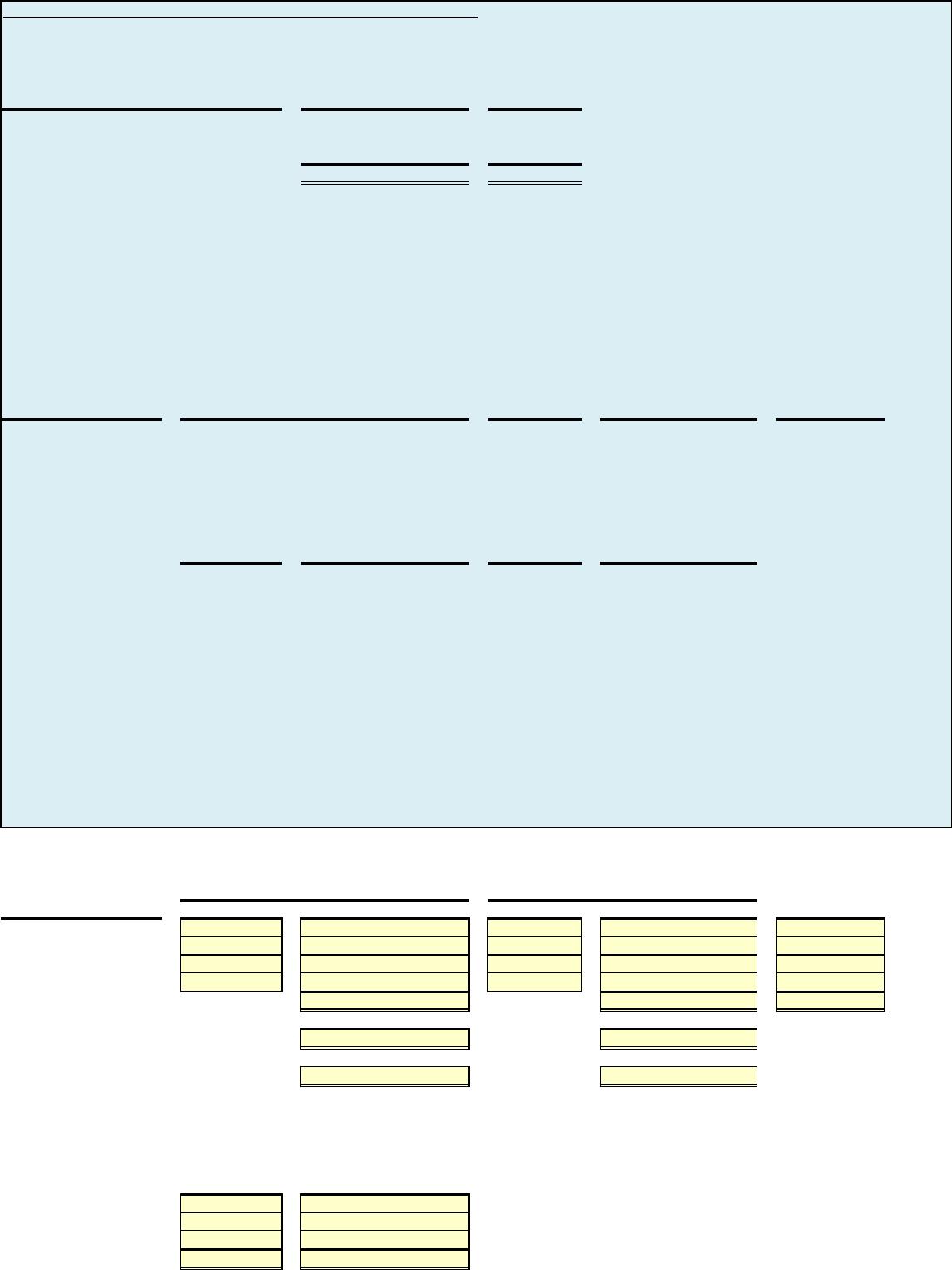

E4-4 – Assign overhead using traditional costing and ABC

Altex Inc. manufactures two products: car wheels and truck wheels. To determine the amount of overhead to

assign to each product line, the controller, Robert Hermann, has developed the following information.

Car Truck

Estimated wheels produced 40,000 10,000

Direct labor hours per wheel 1 3

Total estimated overhead costs for the two product lines are $770,000.

Instructions

(a) Compute the overhead cost assigned to the car wheels and truck wheels, assuming that direct labor hours

is used to allocate overhead costs.

(b) Hermann is not satisfied with the traditional method of allocating overhead because he believes that most

of the overhead costs relate to the truck wheels product line because of its complexity. He therefore develops

the following three activity cost pools and related cost drivers to better understand these costs.

Setting up machines

Assembling

Inspection

Compute the activity-based overhead rates for these three cost pools.

(c) Compute the cost that is assigned to the car wheels and truck wheels product lines using an activity-based

costing system, given the following information.

Car Truck

Number of setups 200 800

Direct labor hours 40,000 30,000

Number of inspections 100 1,100

(d) What do you believe Hermann should do?

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Direct labor hours for car wheels Value

Direct labor hours for truck wheels Value

Total Direct labor hours

?

Total estimated overhead Value Expected Use of Drivers

Total direct labor hours Value

OH rate/DLH ?

Car wheels Truck wheels

Direct labor hours ? ?

Overhead rate / direct labor hour ? ?

Total OH assigned ? ?

Expected Use ABC OH

(b) 0 ÷ of Cost Drivers = Rate

Setting up machines

Value Value ? /setup

Assembling Value Value ? /labor hour

Inspection Value Value ? /inspection

(c )

Expected Use of ABC OH Cost

Cost Driver/Unit Rates Assigned

Setting up machines

Value Value ?

=

Overhead assigned:

Activity Cost Pool

Activity Cost Pool

Car Wheels

x

Expected Use of Cost Drivers per Product

Expected Use of

Activity Cost Pools

Estimated Overhead

Costs

1,000 setups

70,000 labor hours

1,200 inspections

$220,000

280,000

270,000

Cost Drivers

Assembling Value Value ?

Inspection Value Value ?

Total cost assigned ?

Expected Use of ABC OH Cost

Cost Driver/Unit Rates Assigned

Setting up machines

Value Value ?

Assembling Value Value ?

Inspection Value Value ?

Total cost assigned ? ? ?

(d) What do you believe Hermann should do?

After you have completed E4-4, consider the additional question.

1. Assume that total estimated overhead costs changed to $850,000 and the estimated overhead for

Setting up machines and Assembly changed to $260,000 and $320,000 respectively. Redo instruction

(a) to (c). Round overhead rates to two decimal points.

Truck Wheels

x

=

Activity Cost Pool

E4-4 Solution

(a) Compute the overhead cost assigned to the car wheels and truck wheels, assuming that direct labor hours

is used to allocate overhead costs.

Direct labor hours for car wheels 40,000

Car wheels Truck wheels

Direct labor hours 40,000 30,000

(b) Compute the activity-based overhead rates for these three cost pools.

Expected Use ABC OH

Estimated OH ÷ of Cost Drivers = Rate

Setting up machines

$220,000 1,000 $220 /setup

(c) Compute the cost that is assigned to the car wheels and truck wheels product lines using an activity-based

costing system.

Expected Use of ABC OH Cost

Cost Drive/unit Rates Assigned

Setting up machines

200 $220 $44,000

Expected Use of Drivers

Expected Use of ABC OH Cost

Cost Drive/unit Rates Assigned

Setting up machines

800 $220 $176,000

(d) What do you believe Hermann should do?

Assuming that the cost drivers are a reasonable representation of what is occurring in the two product lines, it

seems appropriate to switch to activity-based costing. By using this system, more accurate cost information is

developed which should lead to better allocation of resources and pricing decisions in the future.

120,000

Truck Wheels

x

=

Activity Cost Pool

Overhead assigned:

Activity Cost Pool

Car Wheels

x

=

Activity Cost Pool

E4-4 Solution to Additional Question

1. Assume that total estimated overhead costs changed to $850,000 and the estimated overhead for

Setting up machines and Assembly changed to $260,000 and $320,000 respectively. Redo instructions

(a) to (c ) and round overhead rates to two decimal points.

(a) Compute the overhead cost assigned to the car wheels and truck wheels, assuming that direct labor hours

is used to allocate overhead costs.

Direct labor hours for car wheels 40,000

Direct labor hours for truck wheels 30,000

(b) Compute the activity-based overhead rates for these three cost pools.

Expected Use ABC OH

Estimated OH ÷

of Cost Drivers

= Rate

Setting up machines

$260,000 1,000 $260.00 /setup

(c) Compute the cost that is assigned to the car wheels and truck wheels product lines using an activity-based

costing system.

Expected Use of

ABC OH Cost

Cost Driver/unit

Rates Assigned

Setting up machines

200 $260.00 $52,000

Expected Use of

ABC OH Cost

Cost Drive/unit Rates Assigned

Setting up machines

800 $260.00 $208,000

(d) What do you believe Hermann should do?

=

Assuming that the cost drivers are a reasonable representation of what is occurring in the two product lines, it

seems appropriate to switch to activity-based costing. By using this system, more accurate cost information is

developed which should lead to better allocation of resources and pricing decisions in the future.

Truck Wheels

x

=

Activity Cost Pool

Activity Cost Pool

Car Wheels

x

=

Activity Cost Pool

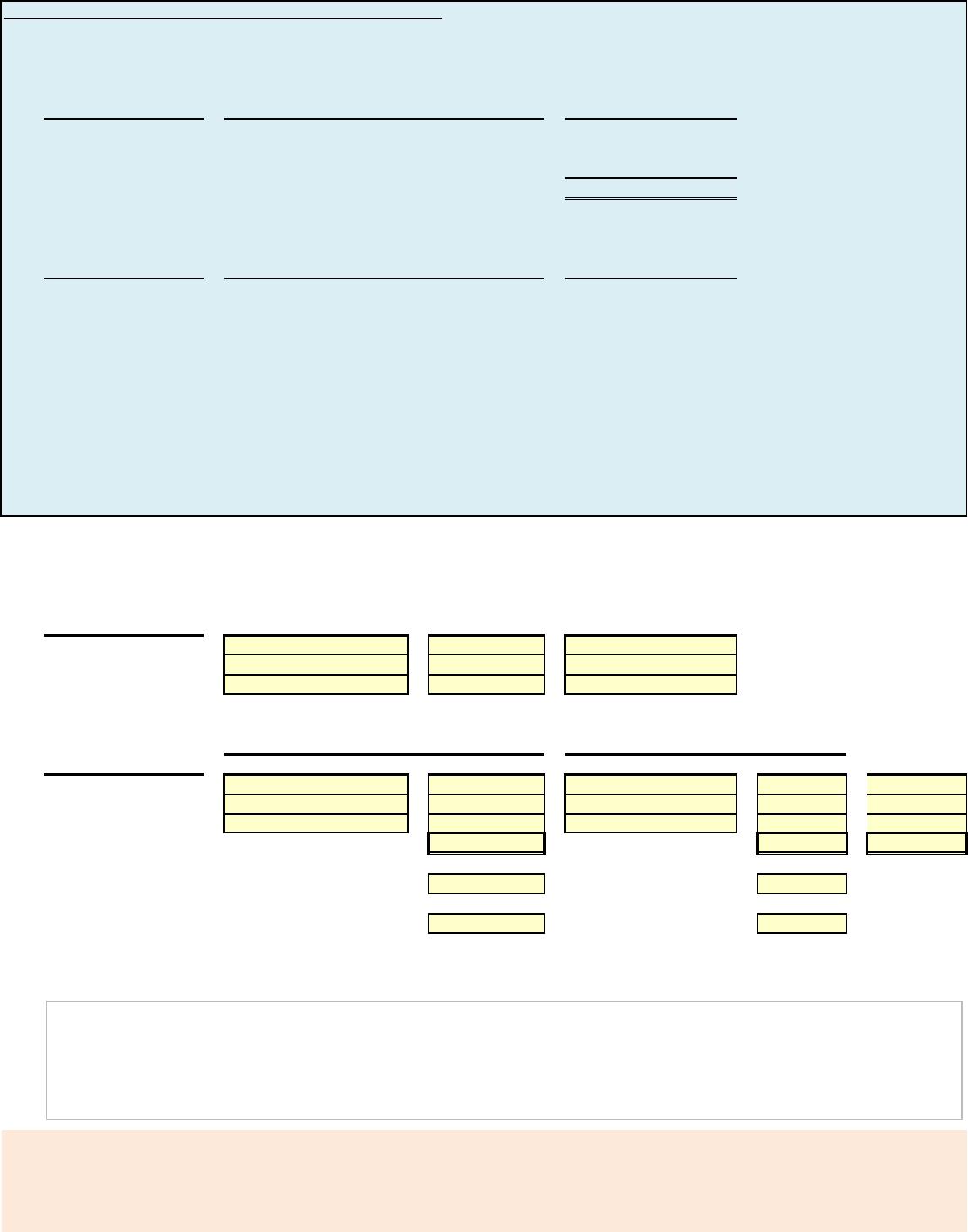

E4-9 Compute overhead rates and assign overhead using ABC

Air United, Inc. manufactures two products: missile range instruments and space pressure gauges. During April,

50 range instruments and 300 pressure gauges were produced, and overhead costs of $94,500 were estimated. An

analysis of estimated overhead costs reveals the following activities.

Total Cost

1. Materials handling Number of requisitions $40,000

2. Machine setups Number of setups 21,500

3. Quality inspections Number of inspections 33,000

$94,500

The cost driver volume for each product was as follows.

Instruments Gauges Total

Number of requisitions 400 600 1,000

Number of setups 200 300 500

Number of inspections 200 400 600

Instructions

(a) Determine the overhead rate for each activity.

(b) Assign the manufacturing overhead costs for April to the two products using activity-based costing.

and compute the overhead cost per unit.

(c) Write a memorandum to the president of Air United explaining the benefits of activity-based costing.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) The overhead rates are:

Expected Use

Estimated ÷ of Cost Driver/ = Activity-Based

Overhead Activity OH Rates

Materials Handling Value Value ? / requisition

Machine Setups Value Value ? / setup

Quality inspections Value Value ? / inspection

(b) The assignment of overhead costs to products is as follows:

Cost

Number Cost Number Cost Assigned

Requisitions Value ? Value ? ?

Machine setups Value ? Value ? ?

Inspections Value ? Value ? ?

Total costs assigned ? Expected Use of Drivers ? ?

Units produced Value Value

OH cost per unit ? ?

`

(c ) Write a memorandum to the president of Air United explaining the benefits of activity-based costing.

0

After you have completed E4-9, consider the additional question.

1. Assume that total estimated overhead costs changed to $190,000 and the estimated overhead for

materials handling, machine setup and quality inspection changed to $105,000, $38,000 and

$47,000 respectively. Redo instructions (a) to (b) and round overhead rates to two decimal points.

Cost Driver

Instruments

Gauges

Activities

Cost Drivers

Cost Drivers

Activity Cost Pools

E4-9 Solution

(a) Determine the overhead rate for each activity.

The overhead rates are:

Expected Use

Estimated ÷ of Cost Driver/ = Activity-Based

Overhead Activity OH Rates

Materials Handling $40,000 1,000 $40 / requisition

(b) Assign the manufacturing overhead costs for April to the two products using activity-based costing.

The assignment of overhead costs to products is as follows:

Cost

Number Cost Number Cost Assigned

Requisitions 400 $16,000 600 $24,000 $40,000

Machine setups 200 $8,600 300 $12,900 $21,500

`

(c ) Write a memorandum to the president of Air United explaining the benefits of activity-based costing.

To: President, Major Instrument, Inc.

From: Student

Re: Benefits of activity-based costing (ABC)

Activity Cost Pools

Instruments

Gauges

Cost Driver

MEMO

E4-9 Solution to Additional Question

1. Assume that total estimated overhead costs changed to $190,000 and the estimated overhead for

materials handling, machine setup and quality inspection changed to $105,000, $38,000 and

$47,000 respectively. Redo instructions (a) to (b) and round overhead rates to two decimal points.

(a) Determine the overhead rate for each activity.

Expected Use

Estimated ÷ of Cost Driver/ = Activity-Based

Overhead Activity OH Rates

Activity Cost Pools

(b) Assign the manufacturing overhead costs for April to the two products using activity-based costing.

The assignment of overhead costs to products is as follows:

Cost

Cost Driver Number Cost Number Cost Assigned

(c) Write a memorandum to the president of Air United explaining the benefits of activity-based costing.

MEMO

To: President, Major Instrument, Inc.

From: Student

Re: Benefits of activity-based costing (ABC)

ABC focuses on the activities performed in producing a product. Overhead costs are assigned to

products based on cost drivers that measure the activities performed on the product.

The primary benefit of ABC is more accurate and meaningful product costing. This improved

Gauges

The overhead rates are:

Instruments

P4-1A Assign overhead using traditional costing and ABC; compute unit costs; classify activities as value- or non-value-added

Combat Fire, Inc. manufactures steel cylinders and nozzles for two models of fire extinguishers: (1) a home fire extinguisher

and (2) a commercial fire extinguisher. The home model is a high-volume (54,000 units), half-gallon cylinder that holds 2 1/2

pounds of multi-purpose dry chemical at 480 PSI. The commercial model is a low-volume (10,200 units), two-gallon cylinder

that holds 10 pounds of multi-purpose dry chemical at 390 PSI. Both products require 1.5 hours of direct labor for completion.

Therefore, total annual direct labor hours are 96,300 or [1.5 hours x (54,000 + 10,200)]. Expected annual manufacturing

overhead is $1,584,280. Thus, the predetermined overhead rate is $16.45 or ($1,584,280 ÷ 96,300) per direct labor hour.

The direct materials cost per unit is $18.50 for the home model and $26.50 for the commercial model. The direct labor cost

is $19 per unit for both the home and the commercial models.

The company’s managers identified six activity cost pools and related cost drivers and accumulated overhead by cost pool

as follows.

Estimated

Estimated Use of Cost

Overhead Drivers Home Commercial

Receiving Pounds $80,400 335,000 215,000 120,000

Forming Machine hours 150,500 35,000 27,000 8,000

Assembling Number of parts 412,300 217,000 165,000 52,000

Testing Number of tests 51,000 25,500 15,500 10,000

Painting Gallons 52,580 5,258 3,680 1,578

Packing and shipping Pounds 837,500 335,000 215,000 120,000

$1,584,280

Instructions

(a) Under traditional product costing, compute the total unit cost of each product. Prepare a simple comparative

schedule of the individual costs by product (similar to Illustration 4-3 on page 5).

(b) Under ABC, prepare a schedule showing the computations of the activity-based overhead rates (per cost driver).

(c) Prepare a schedule assigning each activity‘s overhead cost pool to each product based on the use of cost drivers.

(Include a computation of overhead cost per unit, rounding to the nearest cent.)

(d) Compute the total cost per unit for each product under ABC.

(e) Classify each of the activities as a value-added activity or a non-value-added activity.

(f) Comment on (1) the comparative overhead cost per unit for the two products under ABC, and (2) the comparative

total costs per unit under traditional costing and ABC.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Manufacturing Costs Home Model Commercial Model

Direct materials Value Value

Direct labor Value Value

Overhead Value Value

Total unit cost ? ?

Expected Use of Drivers

Estimated ÷

Expected Use of

= Activity-Based

(b) Overhead Cost Drivers OH Rate

Receiving Value Value Pounds ?

Forming Value Value MH ?

Assembling Value Value Parts ?

Testing Value Value Tests ?

Painting Value Value Gallons ?

Packing and shipping Value Value Pounds ?

?

(c)

MH x Activity-Based = Cost Expected Use x

Activity-Based

= Cost

of Drivers OH Rates Assigned of Drivers OH Rates Assigned

Receiving Value Value ? Value Value ?

Forming Value Value ? Value Value ?

Assembling Value Value ? Value Value ?

Testing Value Value ? Value Value ?

Painting Value Value ? Value Value ?

Packing and shipping Value Value ? Value Value ?

Total cost assigned (a) ? ?

Units produced Value Value

OH cost per unit (a) +(b) ? ?

Home Commercial

(d) Model Model

Direct materials Value Value

Direct labor Value Value

Commercial Model

Expected Use of

Drivers by Product

ABC Manufacturing Costs

Products

Activity Cost Pool

Activity Cost Pools

Activity Cost Pool

Home Model

Cost Drivers

Overhead Value Value

Total cost per unit ? ?

(e )

Receiving

Forming

Assembly

Testing

Painting

Packing and shipping

(f) Comment on (1) the comparative overhead cost per unit for the two products under ABC, and (2) the comparative

total costs per unit under traditional costing and ABC.

After you have completed P4-1A, consider the additional question.

1. Assume that total estimated overhead costs for Receiving, Assembly and Painting changed to

$110,400, $425,000, and $72,600 respectively. Redo instructions (a) to (c ) and round overhead

rates to two decimal points.

classification

classification

classification

classification

classification

classification

Activity

Value- vs. Non-Value-Added

P4-1A Solution

(a) Under traditional product costing, compute the total unit cost of each product. Prepare a simple comparative

schedule of the individual costs by product (similar to Illustration 4-3 on page 5).

Manufacturing Costs Home Model Commercial Model

Direct materials $18.50 $26.50

Direct labor 19.00 19.00

(b) Under ABC, prepare a schedule showing the computations of the activity-based overhead rates (per cost driver).

Estimated ÷ Expected Use of = Activity-Based

Overhead Cost Drivers OH Rate

Receiving $80,400 335,000 Pounds $0.24 / pound

(c ) Prepare a schedule assigning each activity’s overhead cost pool to each product based on the use of cost drivers.

(Include a computation of overhead cost per unit, rounding to the nearest cent.)

Expected Use x Activity-Based = Cost Expected Use x

Activity-Based

Value-added

Value-added

Non-value-added

= Cost

of Drivers OH Rates Assigned of Drivers OH Rates Assigned

Receiving 215,000 $0.24 $51,600 120,000 $0.24 $28,800

Forming 27,000 $4.30 116,100 8,000 $4.30 34,400

(d) Compute the total cost per unit for each product under ABC.

Home Commercial

Model Model

Direct materials $18.50 $26.50

Direct labor 19.00 19.00

0

(e ) Classify each of the activities as a value-added activity or a non-value-added activity.

Receiving

Forming

(f)(1) Comment on the comparative overhead cost per unit for the two products under ABC

(f)(2) Comment on the comparative total costs per unit under traditional costing and ABC.

The comparison of ABC and traditional costing shows that the proper amount of overhead assigned to

the two products is not equal at $24.68 but rather $20.12 for the home model and $48.80 for the commercial

Activity

Value- vs. Non-Value-Added

Non-value-added

Value-added

ABC Manufacturing Costs

Products

Activity Cost Pool

Home Model

Commercial Model

Activity Cost Pool

P4-1A Solution to Additional Question

1. Assume that total estimated overhead costs for Receiving, Assembly and Painting changed to

$110,400, $425,000, and $72,600 respectively. Redo instructions (a) to (c ) and round overhead

rates to two decimal points.

(a) Under traditional product costing, compute the total unit cost of each product. Prepare a simple comparative

schedule of the individual costs by product (similar to Illustration 4-3 on page 5).

Manufacturing Costs Home Model Commercial Model

Direct materials $18.50 $26.50

Direct labor 19.00 19.00

(b) Under ABC, prepare a schedule showing the computations of the activity-based overhead rates (per cost driver).

Estimated ÷ Expected Use of = Activity-Based

Overhead Cost Drivers OH Rate

Receiving $110,400 335,000 Pounds $0.33 /pound

Forming 150,500 35,000 MH $4.30 / MH

(c ) Prepare a schedule assigning each activity’s overhead cost pool to each product based on the use of cost drivers.

(Include a computation of overhead cost per unit, rounding to the nearest cent.)

Expected Use x Activity-Based = Cost Expected Use x

Activity-Based

= Cost

of Drivers OH Rates Assigned of Drivers OH Rates Assigned

Receiving 215,000 $0.33 $70,854 120,000 $0.33 $39,546

Forming 27,000 $4.30 116,100 8,000 $4.30 34,400

Value-added

Non-value-added

(d) Compute the total cost per unit for each product under ABC.

Home Commercial

Model Model

Direct materials $18.50 $26.50

Direct labor 19.00 19.00

(e ) Classify each of the activities as a value-added activity or a non-value-added activity.

Receiving

Forming

Assembly

(f)(1) Comment on the comparative overhead cost per unit for the two products under ABC

(f)(2) Comment on the comparative total costs per unit under traditional costing and ABC.

The comparison of ABC and traditional costing shows that the proper amount of overhead assigned to

the two products is not equal at $24.68 but rather $20.92 for the home model and $50.74 for the commercial

Activity

Value- vs. Non-Value-Added

Non-value-added

Value-added

Value-added

ABC Manufacturing Costs

Products

Activity Cost Pool

Home Model

Commercial Model

Activity Cost Pool

P4-2A Assign overhead to products using ABC and evaluate decision

Schultz Electronics manufactures two ultra high-definition television models: the Royale which sells for $1,600 and

a new model, the Majestic, which sells for $1,300. The production cost computed per unit under traditional costing

for each model in 2017 as follows.

Royale Majestic

Direct materials $700 $420

Direct labor ($20 per hours)

120 100

Manufacturing overhead ($38 per DLH) 228 190

Total per unit cost $1,048 $710

In 2017, Schultz manufactured 25,000 units of the Royale and 10,000 units of the Majestic. The overhead rate of

$38 per direct labor hour was determined by dividing total expected manufacturing overhead of $7,600,000 by the

total direct labor hours (200,000) for the two models.

Under traditional costing, the gross profit on the models was Royale 552 ($1,600 – $1,048) and Majestic $590

($1,300 – $710). Because of this difference, management is considering phasing out the Royale model and increasing

the production of the Majestic model.

Before finalizing its decision, management asks Schultz’s controller to prepare an analysis using activity-based

costing (ABC). The controller accumulates the following information about overhead for the year ended December 31, 2017.

Activity Estimated Estimated Use Activity-Based

Cost Pools Overhead of Cost Drivers

Overhead

Rates

Purchasing Number of orders $1,200,000 $30/order

Machine setups Number of setups 900,000 $50/setup

Machining Machine hours 4,800,000 $40/hour

Quality control Number of inspections 700,000 $25/inspection

The cost drivers used for each product were:

Cost Drivers Royale Majestic Total

Purchase orders 17,000 23,000 40,000

Machine setups 5,000 13,000 18,000

Machine hours 75,000 45,000 120,000

Inspections 11,000 17,000 28,000

Instructions

(a) Assign the total 2017 manufacturing overhead costs to the two products using activity-based costing (ABC) and

determine the overhead cost per unit.

(b) What was the cost per unit and gross profit of each model using ABC costing?

(c) Are management’s future plans for the two models sound? Explain.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

Expected Use of Drivers

(a) The allocation of total manufacturing overhead using activity-based costing is as follows:

Total

Overhead Rate Drivers Used Cost Assigned Drivers Used Cost Assigned Overhead

Purchase order@$30 Value ?Value ? ?

Machine setups @$50 Value ?Value ? ?

Machine hours @$40 Value ?Value ? ?

Inspections @$25 Value ?Value ? ?

Total assigned costs (a) ? ? ?

Units produced (b) Value Value

$0

Cost per unit (a) ÷ (b) ? ?

(b) The cost per unit and gross profit of each model under ABC costing were:

Royale Majestic

Direct materials Value Value

Direct labor Value Value

Manufacturing overhead Value Value

Total cost per unit ? ?

Royale

Majestic

Traditional Costing

28,000

40,000

18,000

120,000

Cost Drivers

Sales price per unit Value Value

Cost per unit Value Value

Gross profit per unit ? ?

(c) Are management’s future plans for the two models sound? Explain.

After you have completed P4-2A, consider the additional question.

1. Assume that the purchase orders used by Royale and Majestic changed to 19,000 and 21,000 respectively.

Also assume that the number of inspections used by Royale and Majestic models changed to 12,000 and 16,000

respectively. Redo instsructions (a) to (c ) and round cost and gross profit per unit to two decimal points.

P4-2A Solution

(a) The allocation of total manufacturing overhead using activity-based costing is as follows:

Total

Drivers Used Cost Assigned Drivers Used Cost Assigned Overhead

Purchase order@$30 17,000 $510,000 23,000 $690,000 $1,200,000

Machine setups @$50 5,000 250,000 13,000 650,000 900,000

(b) The cost per unit and gross profit of each model under ABC costing were:

Royale Majestic

Direct materials $700.00 $420.00

Direct labor 120.00 100.00

(c ) Are management’s future plans for the two models sound? Explain.

Royale

Majestic

Overhead Rate

P4-2A Solution to Additional Question

1. Assume that the purchase orders used by Royale and Majestic changed to 19,000 and 21,000 respectively.

Also assume that the number of inspections used by Royale and Majestic models changed to 12,000 and 16,000

respectively. Redo instsructions (a) to (c ) and round cost and gross profit per unit to two decimal points.

(a) The allocation of total manufacturing overhead using activity-based costing is as follows:

Total

Drivers Used Cost Assigned Drivers Used Cost Assigned Overhead

Purchase order@$30 19,000 $570,000 21,000 $630,000 $1,200,000

Units produced (b) 25,000 10,000

(b) The cost per unit and gross profit of each model under ABC costing were:

Royale Majestic

Direct materials $700.00 $420.00

Direct labor 120.00 100.00

(c ) Are management’s future plans for the two models sound? Explain.

Royale

Majestic

Overhead Rate

Management’s future plans for the two television models are not sound.

Under ABC costing, the Royale model is $183.20 per unit ($615.20 –

CD4 – Excel Tutorial

As you learned in the previous chapters, Current Designs has two main product lines – composite kayaks, which are handmade and

very labor-intensive, and rotomolded kayaks, which require less labor but employ more expensive equipment. Current Design’s

controller, Diane Buswell, is now evaluating several different methods of assigning overhead to these products. It is important to

ensure that costs are appropriately assigned to the company’s products. At the same time, the system that is used must not be so

complex that its costs are greater than its benefits.

Diane has decided to use the following activities and costs to evaluate the methods of assigning overhead.

Cost

Designing new models $121,000

Creating and testing prototypes 152,000

Creating molds for kayaks 188,500

Operating oven for the rotomolded kayaks 40,000

Operating the vacuum line for the composite kayaks 28,000

Supervising production employees 180,000

Curing time :(the time that is needed for the chemical

processes to finish before the next step in

the production process; many of these

costs are related to the space required in

the building) 190,500

Total $900,000

As Diane examines the data, she decides that the cost of operating the oven for the rotomolded kayaks and the cost of operating

the vacuum line for the composite kayaks can be directly assigned to each of these products lines and do not need to be allocated

with the other costs.

Instructions

For purpose of this analysis, assume that Current Designs uses $234,000 in direct labor costs to produce 1,000 composite kayaks

and $286,000 in direct labor costs to produce 4,000 rotomolded kayaks each year.

(a) One method of allocating overhead would allocate the common costs to each product line by using a allocation basis such as

the number of employees working on each type of kayak or the amount of factory space used for the production of each type of kayak.

Diane knows that about 50% of the area of the plant and 50% of the employees work on the composite kayaks, and the remaining space

and other employees work on the rotomolded kayaks. Using this information and remembering that the cost of operating the oven

and vacuum line have been directly assigned, determine the total amount to be assigned to the composite kayak line and the

rotomolded kayak line, and the amount to be assigned to each of the units in each line.

(b) Another method of allocating overhead is to use direct labor dollars as an allocation basis. Remembering that the costs of the

oven and the vacuum line have been assigned directly to the product lines, allocate the remaining costs using direct labor

dollars as the allocation basis. Then, determine the amount of overhead that should be assigned to each unit of each product

line using this method.

(c) Activity-based costing requires a cost driver for each cost pool. Use the following information to assign the costs to the product

Expected Use of Drivers

lines using the activity-based costing approach.

Designing new models Number of models

Creating and test prototypes Number of prototypes

Creating molds for kayaks Number of molds

Supervising production kayaks Number of employees

Curing time Number of days of curing time

What amount of overhead should be assigned to each composite kayak using this method? What amount of overhead

should be assigned to each rotomolded kayak using this method?

Composite Kayaks

(d) Which of the three methods do you think Current Designs should use? Why?

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Determine the total amount to be assigned to the composite kayak line and the rotomolded kayak line, and the amount to be

assigned to each of the units in each of the units in each line.

Composite Rotomolded

Directly assigned Value Value

Remaining amount allocated 50%

to each product line

Total ? ?

Number of units Value Value

Cost assigned per unit ? ?

(b) Determine the amount of overhead that should be assigned to each unit of each product using direct labor dollars as an allocation basis.

Value

Value

3

6

12

12

15,000

1

2

1

12

2,000

Driver Amount for

Rotomolded Kayaks

Activities

Activity Cost Pools

Cost Drivers

Driver Amount for

Composite Kayaks

Overhead Rate

Total OH costs (a)_ Value

Direct labor cost (b)

Composite Value

Rotomolded Value ?

OH rate (a) ÷ (b) ?

Composite Rotomolded

Directly assigned Value Value

Remaining amount allocated

based on direct labor costs

Total ? ?

Number of units Value Value

Cost assigned per unit ? ?

(c) What amount of overhead should be assigned to each composite kayak and rotomolded kayak using the activity-based costing method?

Activity Cost Pools Estimated Overhead

Estimated Use

of Cost Drivers

Activity-Based

OH Rates

Design Value Value ? / model

Prototypes Value Value ? / prototype

Molds Value Value ? / mold

Supervision Value Value ? / employee

Curing time Value Value ? / day

Activity Cost Pools Expected Use of Drivers

Overhead

Rates

Cost

Assigned

Expected Use of

Drivers

Overhead

Rates

Cost

Assigned

Design Value Value ?Value Value ?

Prototypes Value Value ?Value Value ?

Molds Value Value ?Value Value ?

Supervision Value Value ?Value Value ?

Curing time Value Value ?Value Value ?

Total amount allocated ? ?

Directly assigned ? ?

Total Cost (a) ? ?

Number of units(b) Value Value

Cost assigned/unit ? ?

(a) ÷ (b)

(d) Which of the three methods do you think Current Designs should use? Why?

After you have completed CD4, consider the additional question.

1. Assume that the number of prototypes created for composite kayaks and rotomolded kayaks changed to 8 and 4 respectively.

Redo instruction (c) and round cost assigned /unit to two decimal points.

Rotomolded

?

?

Composite

CD4 – Excel Tutorial Solution

(a) Determine the total amount to be assigned to the composite kayak line and the rotomolded kayak line, and the amount to be

assigned to each of the units in each of the units in each line.

Composite Rotomolded

Directly assigned $28,000 $40,000

Remaining amount allocated 50% ($832,000)

(b) Determine the amount of overhead that should be assigned to each unit of each product using direct labor dollars as an allocation basis.

Overhead Rate

Total OH costs (a) $832,000

Composite Rotomolded

Directly assigned $28,000 $40,000

Remaining amount allocated

to each product line

based on direct labor costs

(c ) What amount of overhead should be assigned to each composite kayak and rotomolded kayak using the activity-based costing method?

Activity Cost Pools Estimated Overhead

Estimated Use

of Cost Drivers

Activity-Based

OH Rates

Design $121,100 4 $30,275 / model

Prototypes 152,000 8 $19,000 / prototype

Molds 188,500 13 $14,500 / mold

Activity Cost Pools Expected Use of Drivers

Overhead

Rates

Cost

Assigned

Expected Use of Drivers

Overhead

Rates

Cost Assigned

Design 3 $30,275 $90,825 1 $30,275 $30,275

Prototypes 6 $19,000 114,000 2 $19,000 38,000

Total amount allocated 636,825 195,175

Directly assigned 28,000 40,000

12

(d) Activity based costing assigns significantly more costs to the composite kayaks. Since the cost is divided into pools and each

pool is allocated using a cost driver that is related to those particular costs, it provides a more accurate way to allocate the

costs. Current Designs would need to weigh the additional costs of implementing an ABC system against the benefits that

it provides.

374,400

457,600

Composite

Rotomolded

416,000

416,000

374,400

457,600

CD4 – Excel Tutorial Solution to Additional Question

1. Assume that the number of prototypes created for composite kayaks and rotomolded kayaks changed to 8 and 4 respectively.

Redo instruction (c) and round cost assigned /unit to two decimal points.

(a) Determine the total amount to be assigned to the composite kayak line and the rotomolded kayak line, and the amount to be

assigned to each of the units in each of the units in each line.

Composite Rotomolded

Directly assigned $28,000 $40,000

Remaining amount allocated 50% ($832,000)

to each product line

(b) Determine the amount of overhead that should be assigned to each unit of each product using direct labor dollars as an allocation basis.

Overhead Rate

Total OH costs (a) $832,000

Direct labor cost (b)

Composite $234,000

Composite Rotomolded

Directly assigned $28,000 $40,000

(c ) What amount of overhead should be assigned to each composite kayak and rotomolded kayak using the activity-based costing method?

Activity Cost Pools Estimated Overhead

Estimated Use

of Cost Drivers

Activity-

Based OH

Rates

Design $121,100 4 $30,275 / model

Activity Cost Pools Expected Use of Drivers

Overhead

Rates

Cost

Assigned

Expected Use of

Drivers

Overhead

Rates

Cost Assigned

Design 3 $30,275 $90,825 1 $30,275 $30,275

Supervision 12 $7,500 90,000 12 $7,500 90,000

Curing time 15,000 $11.20 168,000 2,000 $11.20 22,400

(d) Activity based costing assigns significantly more costs to the composite kayaks. Since the cost is divided into pools and each

Rotomolded

416,000

416,000

Composite