1. The end-of-period spreadsheet illustrates the flow of accounting information from the unadjusted

trial balance into the adjusted trial balance and into the financial statements. In doing so, the

spreadsheet illustrates the impact of the adjustments on the financial statements.

3. Current liabilities are liabilities that will be due within a short time (usually one year or less) and

that are to be paid out of current assets. Liabilities that will not be due for a comparatively long

time (usually more than one year) are called long-term liabilities.

4. Revenue, expense, and drawing accounts are generally referred to as temporary accounts.

5. Cash, Office Equipment

6. Closing entries are necessary at the end of an accounting period (1) to transfer the balances in

temporary accounts to permanent accounts and (2) to prepare the temporary accounts for use in

recording transactions for the next accounting period.

10. a. The financial statements are the most important output of the accounting cycle.

b. Yes. All companies have an accounting cycle that begins with analyzing and journalizing

transactions and ends with a post-closing trial balance. However, companies may differ in

how they implement the steps in the accounting cycle. For example, while most companies

use computerized accounting systems, some companies may use manual systems.

CHAPTER 4

COMPLETING THE ACCOUNTING CYCLE

DISCUSSION QUESTIONS

CHAPTER 4 Completing the Accounting Cycle

PE 4-1A

1. Balance sheet 5. Income statement

PE 4-1B

1. Balance sheet 5. Balance sheet

2. Balance sheet 6. Balance sheet

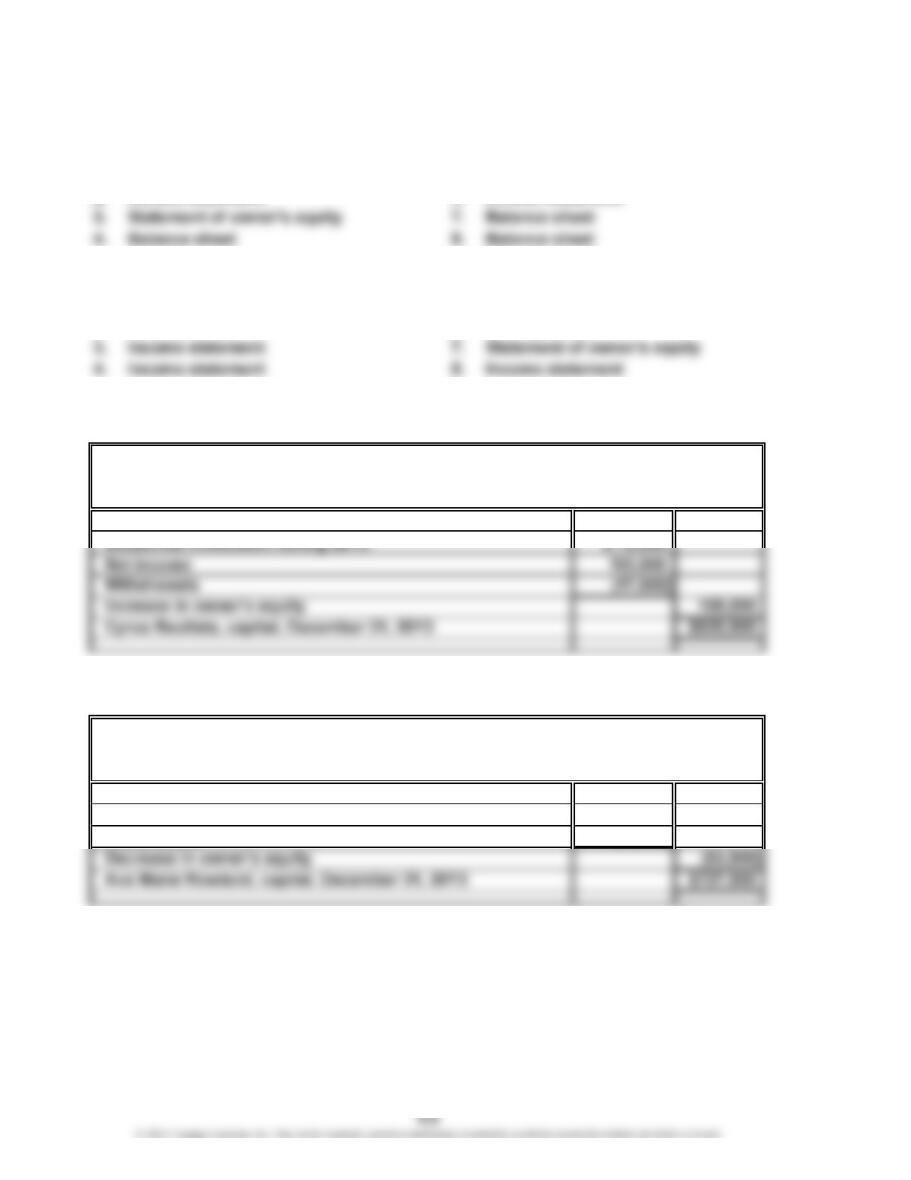

PE 4-2A

Cyrus Bautista, capital, January 1, 20Y3 $471,900

PE 4-2B

Ava Marie Rowland, capital, January 1, 20Y3 $781,000

Net loss $(34,500)

Withdrawals (19,000)

Road Runner Delivery Services

Statement of Owner’s Equity

For the Year Ended December 31, 20Y3

PRACTICE EXERCISES

Aquarius Advertising Services

Statement of Owner’s Equity

For the Year Ended December 31, 20Y3

CHAPTER 4 Completing the Accounting Cycle

PE 4-3A

1. Property, plant, and equipment (b) 5. Current liability (c)

PE 4-3B

1. Current liability (c) 5. Owner’s equity (e)

PE 4-4A

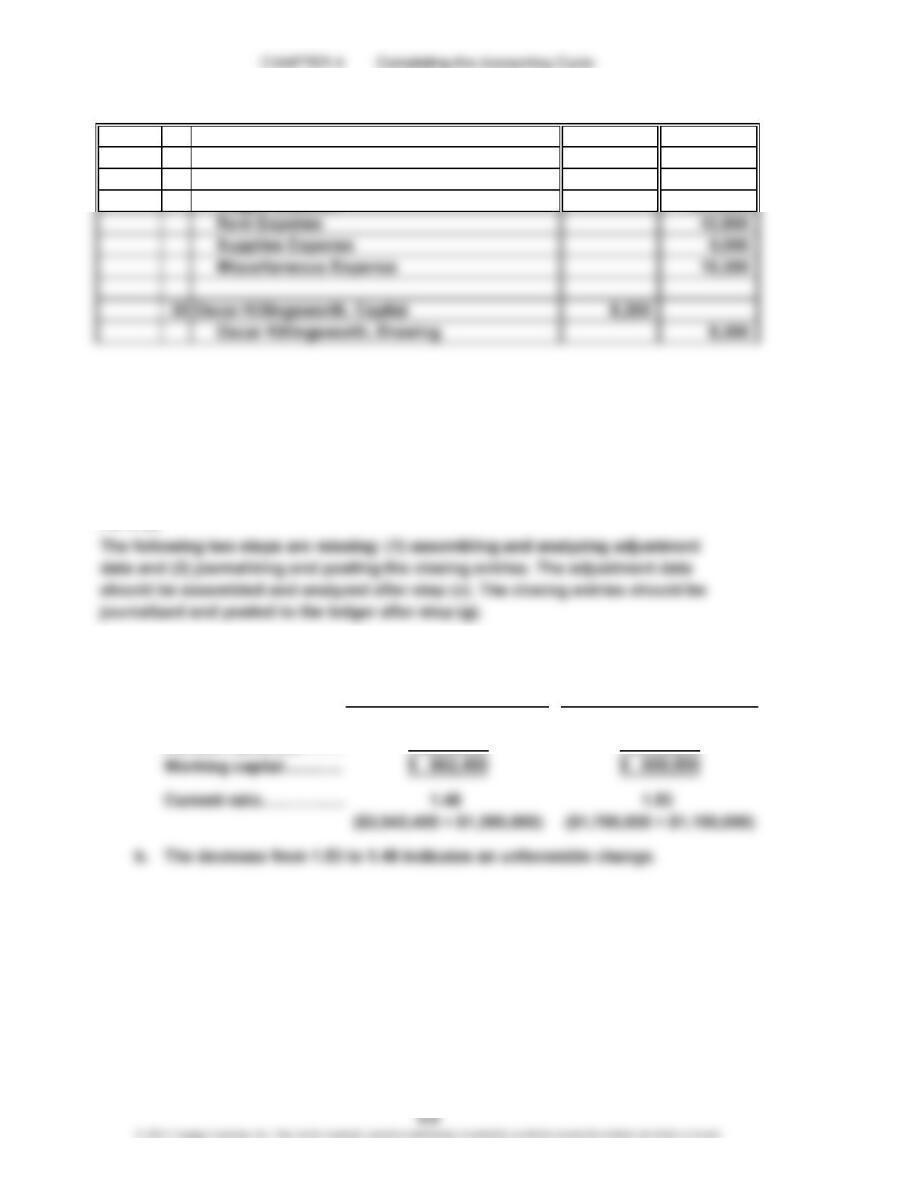

Dec. 31 Fees Earned 1,644,500

Wages Expense 1,239,200

Closing Entries

PE 4-4B

Apr. 30 Oscar Killingsworth, Capital 5,500

Fees Earned 279,100

PE 4-5A

The following two steps are missing: (1) posting the transactions to the ledger

and (2) preparing the financial statements. Transactions should be posted

to the ledger after step (a). The financial statements should be prepared after step (f).

PE 4-6A

a.

Current assets…………

…

…

1,150,000

Closing Entries

20Y9

$2,042,400

20Y8

$1,759,500

1,380,000

CHAPTER 4 Completing the Accounting Cycle

PE 4-6B

a.

Current assets……………

…

20Y9

$2,133,800

20Y8

$1,613,300

…

CHAPTER 4 Completing the Accounting Cycle

Ex. 4-1

1. Income statement: 5, 8, 9

2. Statement of owner’s equity: 4

3. Balance sheet: 1, 2, 3, 6, 7, 10

Ex. 4-2

a. Asset: 1, 2, 5, 6, 10

EXERCISES

CHAPTER 4 Completing the Accounting Cycle

Ex. 4-3

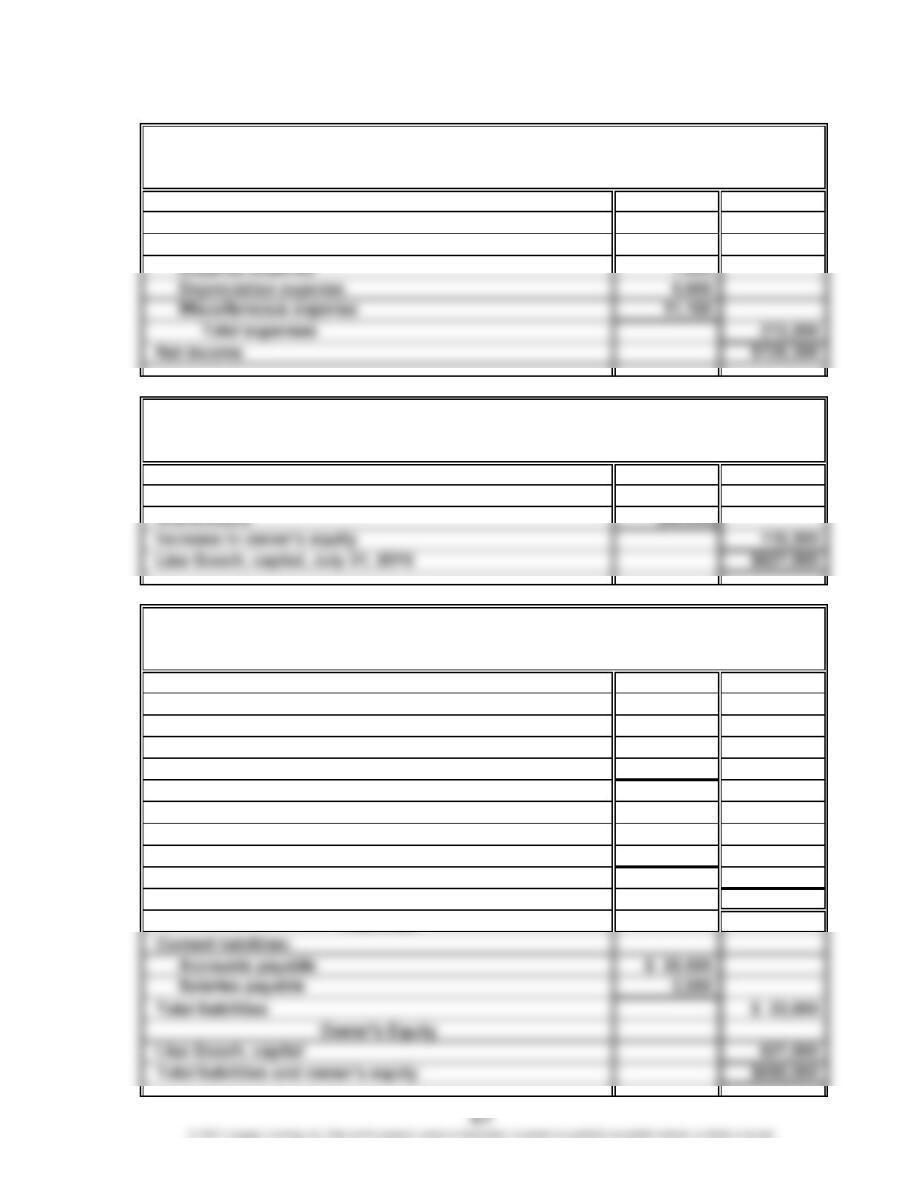

Fees earned $348,500

Expenses:

Salary expense $189,000

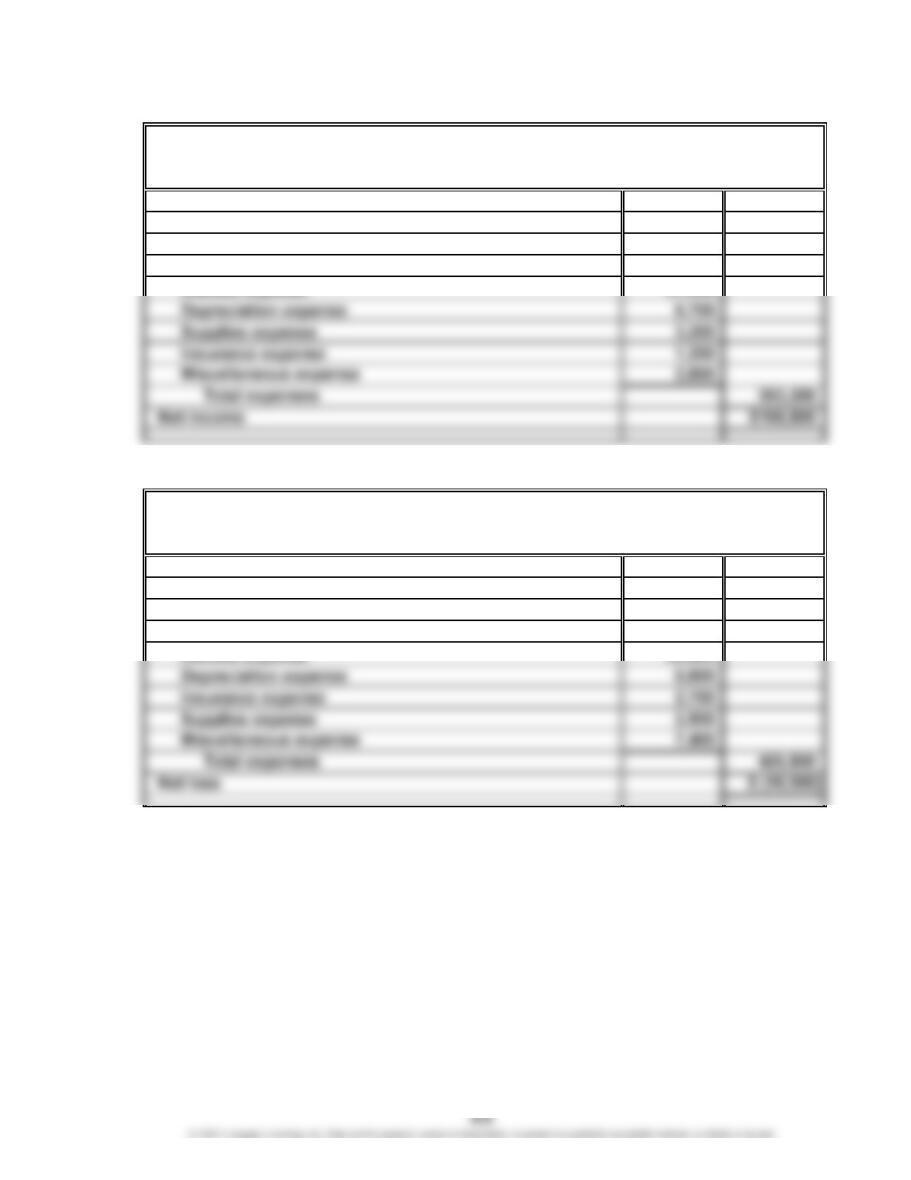

Lisa Gooch, capital, August 1, 20Y4 $516,700

Net income $135,300

Current assets:

Cash $ 58,000

Accounts receivable 106,200

Supplies 4,400

Total current assets $168,600

Property, plant, and equipment:

Office equipment $515,000

Less accumulated depreciation 33,600

Total property, plant, and equipment 481,400

Total assets $650,000

Bamboo Consulting

Income Statement

For the Year Ended July 31, 20Y5

Assets

Bamboo Consulting

Statement of Owner’s Equity

For the Year Ended July 31, 20Y5

Bamboo Consulting

Balance Sheet

July 31, 20Y5

CHAPTER 4 Completing the Accounting Cycle

Ex. 4-4

Fees earned $60,000

Expenses:

Salary expense $32,375

Jayson Neese, capital, July 1, 20Y5 $ 82,200

Net income $22,025

Withdrawals (2,000)

Current assets:

Cash $27,000

Accounts receivable 53,500

Supplies 900

Total current assets $ 81,400

Property, plant, and equipment:

Office equipment $30,500

Less accumulated depreciation 6,000

Total property, plant, and equipment 24,500

Total assets $105,900

Assets

Elliptical Consulting

Income Statement

For the Year Ended June 30, 20Y6

Elliptical Consulting

Statement of Owner’s Equity

For the Year Ended June 30, 20Y6

Elliptical Consulting

Balance Sheet

June 30, 20Y6

CHAPTER 4 Completing the Accounting Cycle

Ex. 4-5

Fees earned $522,000

Expenses:

Salaries expense $260,900

Rent expense 46,500

Ex. 4-6

Service revenue $407,900

Expenses:

Wages expense $327,500

Rent expense 49,100

Income Statement

For the Year Ended February 28, 20Y0

Capstone Messenger Service

Income Statement

For the Year Ended April 30, 20Y7

Guardian Health Services Co.

CHAPTER 4 Completing the Accounting Cycle

Ex. 4-7

Revenues $65,450

Expenses:

Salaries and employee benefits $23,207

Purchased transportation 15,101

Rentals and landing fees 3,361

Ex. 4-8

Farhan Wasti, capital, January 1, 20Y1 $1,502,000

Net income $385,000

Statement of Owner’s Equity

For the Year Ended December 31, 20Y1

FedEx Corporation

Income Statement

For the Year Ended May 31

(in millions)

Serenity Systems Co.

CHAPTER 4 Completing the Accounting Cycle

Ex. 4-9

Angelo Phelps, capital, May 1, 20Y1 $537,100

Net loss $(35,200)

Withdrawals (9,200)

Decrease in owner’s equity (44,400)

Angelo Phelps, capital, April 30, 20Y2 $492,700

Masterpiece Arts

Statement of Owner’s Equity

For the Year Ended April 30, 20Y2

CHAPTER 4 Completing the Accounting Cycle

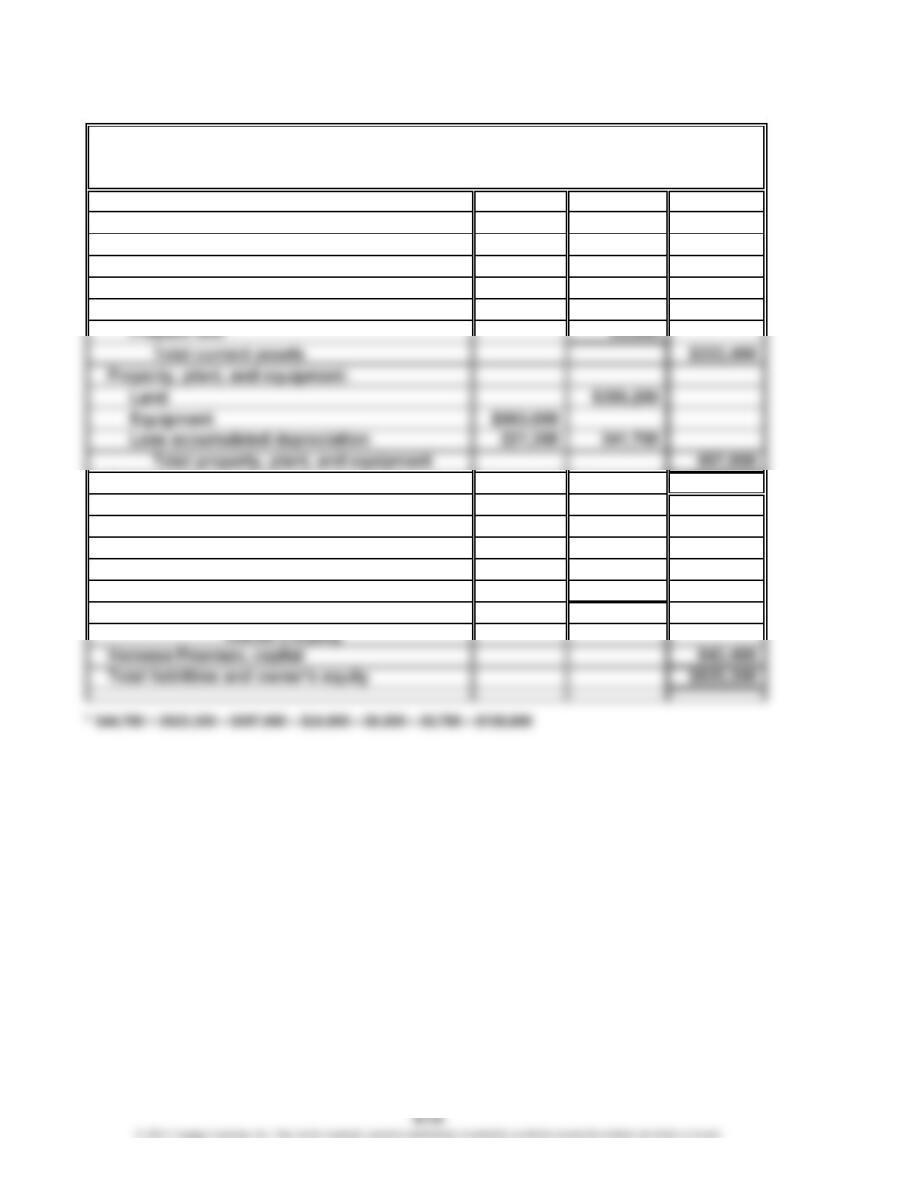

Ex. 4-12

Current assets:

Cash* $ 44,700

Accounts receivable 138,600

Supplies 5,700

Prepaid insurance 8,500

Total assets $920,300

Current liabilities:

Accounts payable $ 44,800

Salaries payable 10,700

Unearned fees 21,400

Total liabilities $ 76,900

MaxFit Weight Loss Co.

Balance Sheet

November 30, 20Y4

Assets

Liabilities

CHAPTER 4 Completing the Accounting Cycle

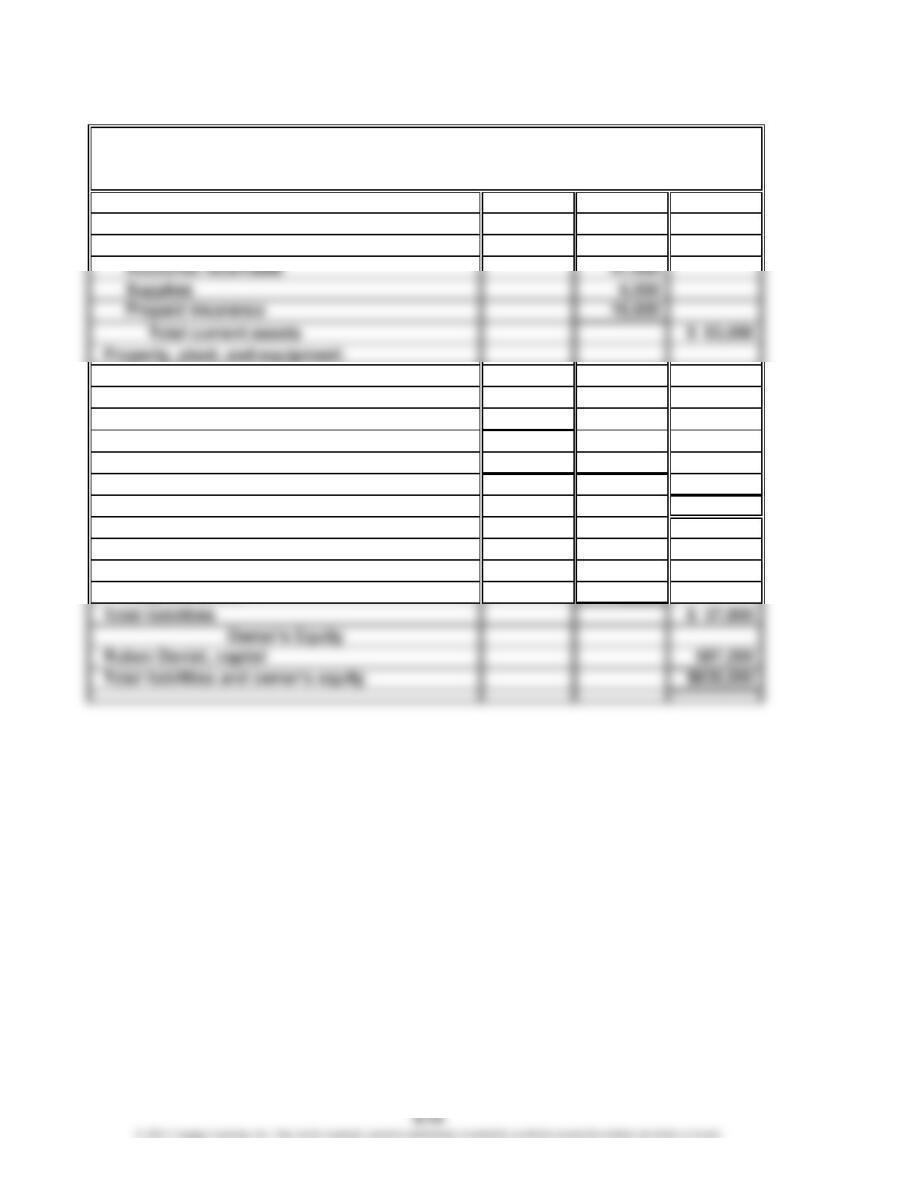

Ex. 4-13

1. The date of the statement should be “August 31, 20Y3” and not “For the Year

3. Land should be classified as property, plant, and equipment.

4. “Accumulated depreciation” should be deducted from the related fixed asset.

5. An adding error was made in determining the amount of the total property,

plant, and equipment.

6. Accounts receivable should be a current asset.

CHAPTER 4 Completing the Accounting Cycle

Ex. 4-13 (Concluded)

Current assets:

Cash $ 18,500

Land $225,000

Building $400,000

Less accumulated depreciation 155,000 245,000

Equipment $ 97,000

Less accumulated depreciation 25,000 72,000

Total property, plant, and equipment 542,000

Total assets $625,000

Current liabilities:

Accounts payable $ 31,300

Wages payable 6,500

Liabilities

Labyrinth Services Co.

Balance Sheet

August 31, 20Y3

Assets

CHAPTER 4 Completing the Accounting Cycle

Ex. 4-14

d. Depreciation Expense

e. Fees Earned

Ex. 4-15

$1,447,000 ($8,315,000 – $6,460,000 – $408,000)

Ex. 4-16

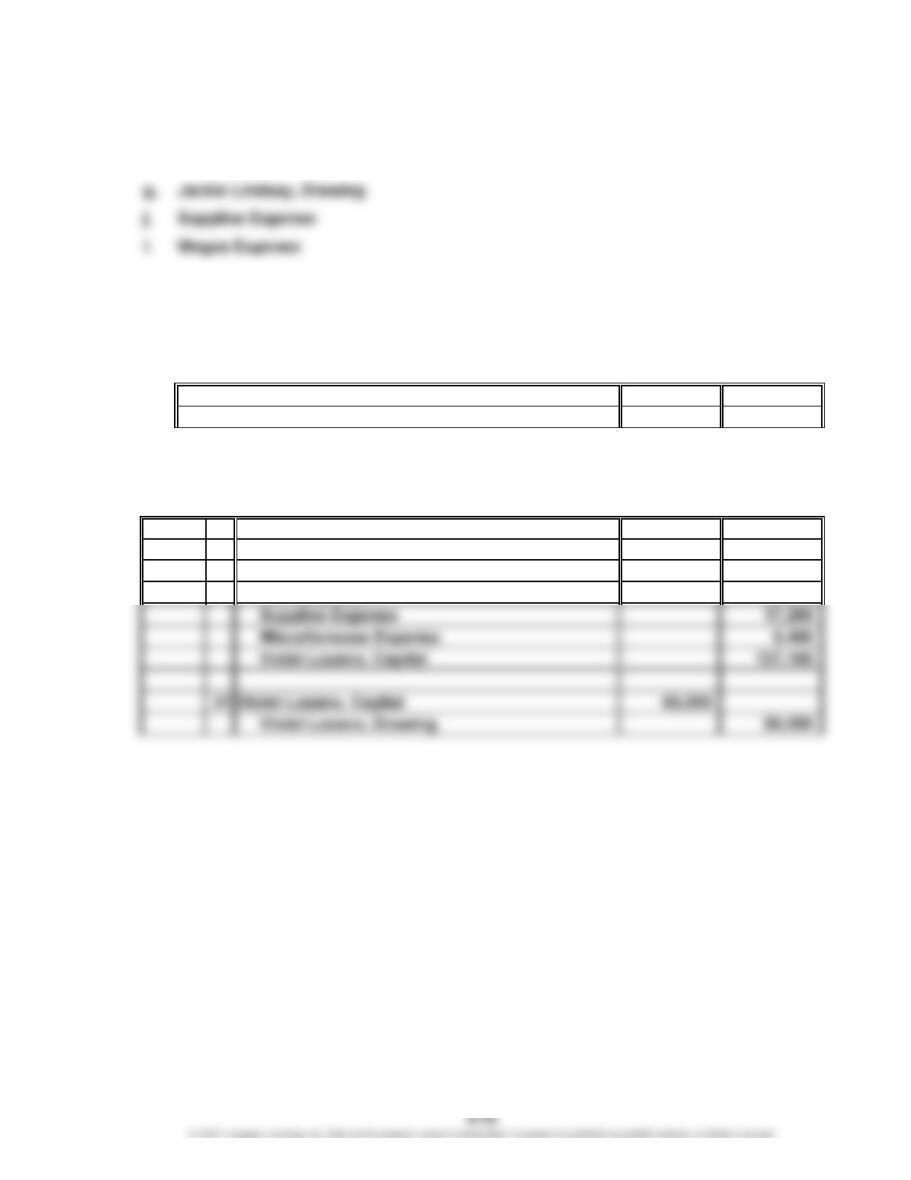

a. Teresa Schafer, Capital 770,000

Teresa Schafer, Drawing 770,000

b. $1,955,000 ($1,885,000 + $3,190,000 – $2,350,000 – $770,000)

Ex. 4-17

July 31 Fees Earned 545,000

Wages Expense 342,400

Rent Expense 52,900

Closing Entries

CHAPTER 4 Completing the Accounting Cycle

Ex. 4-18

a. Accounts Receivable

b. Cash

e. Doug Woods, Capital

Ex. 4-19

Debit Credit

Balances Balances

Cash 46,540

Accounts Receivable 122,260

Supplies 4,000

Equipment 127,200

Ex. 4-20

a. Transactions are analyzed and recorded in the journal (Step 1).

g. An optional end-of-period spreadsheet is prepared (Step 5).

f. Adjusting entries are journalized and posted to the ledger (Step 6).

e. An adjusted trial balance is prepared (Step 7).

La Casa Services Co.

Post-Closing Trial Balance

March 31, 20Y6

CHAPTER 4 Completing the Accounting Cycle

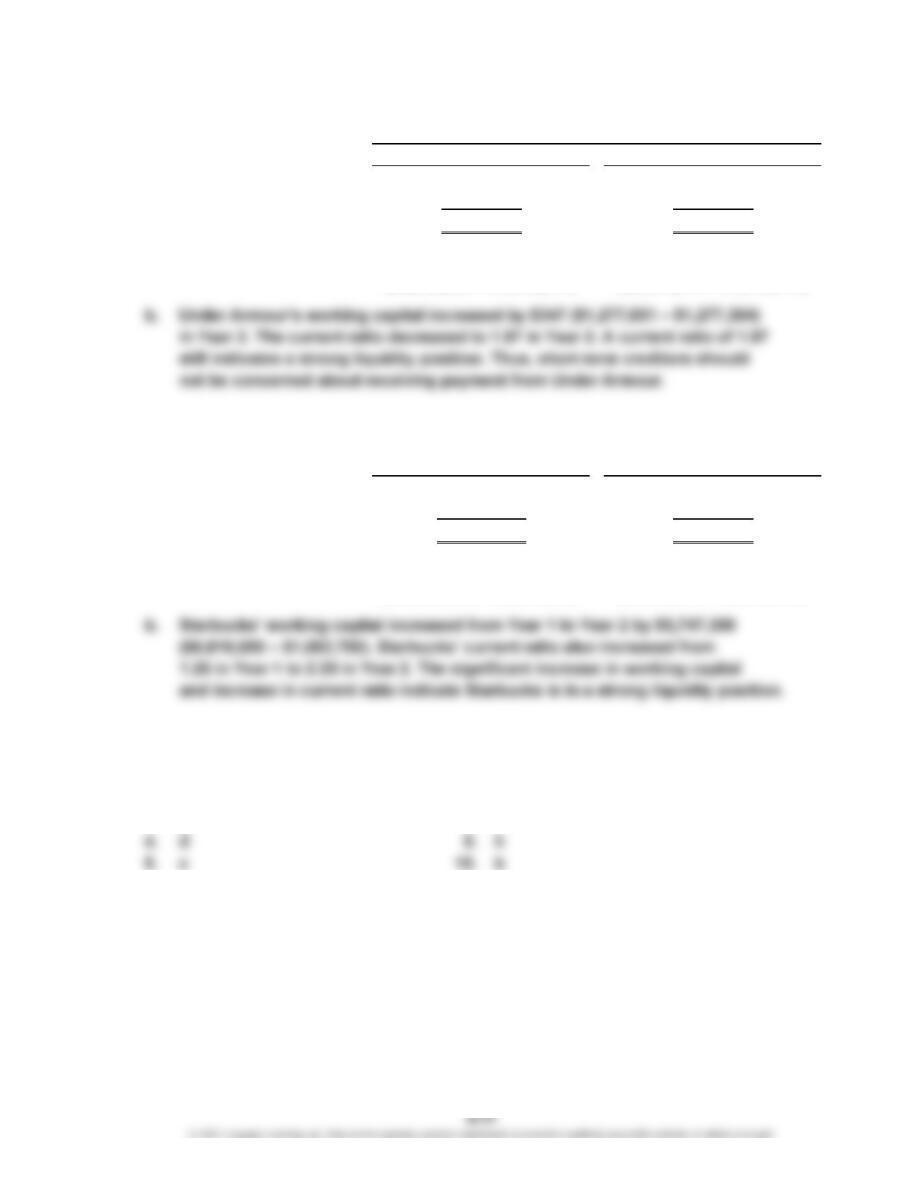

Ex. 4-21

a.

Current assets……………

Current liabilitites………

…

Working capital…………

…

Current ratio……………

…

Ex. 4-22

a.

Current assets……………

Current liabilitites………

…

Working capital…………

…

Current ratio……………

…

Appendix 1 Ex. 4-23

1. i 6. f

2. a 7. j

3. g 8. e

5,684,200 4,220,700

($12,494,200 ÷ $5,684,200)

$1,277,304

2.20

($2,337,679 ÷ $1,060,375)

$12,494,200 $5,283,400

($5,283,400 ÷ $4,220,700)

$ 6,810,000 $1,062,700

2.20 1.25

December 31

Year 2 Year 1

1.97

($2,593,628 ÷ $1,315,977)

Year 1Year 2

$2,593,628

1,315,977

$1,277,651

$2,337,679

1,060,375

CHAPTER 4 Completing the Accounting Cycle

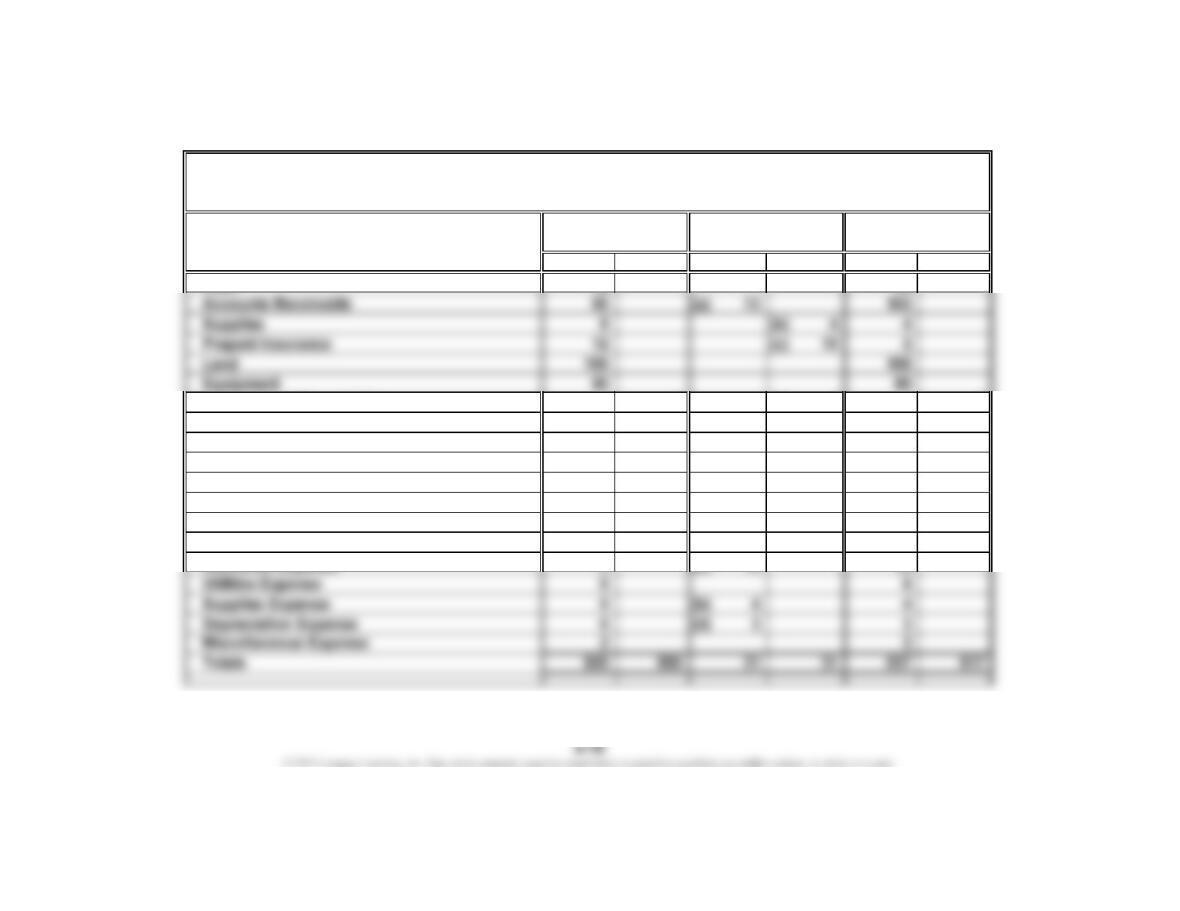

Appendix 1 Ex. 4-24

Account Title Debit Credit Debit Credit

Accumulated Depreciation 4 (d) 3 7

Accounts Payable 36 36

Wages Payable 0 (e) 1 1

Brenda Schultz, Capital 260 260

Brenda Schultz, Drawing 8 8

Fees Earned 200 (a) 13 213

Wages Expense 110 (e) 1 111

Rent Expense 12 12

Alert Security Services Co.

End-of-Period Spreadsheet (Work Sheet)

For the Year Ended October 31, 20Y5

Unadjusted Adjusted

Debit Credit

Trial Balance Adjustments Trial Balance

CHAPTER 4 Completing the Accounting Cycle

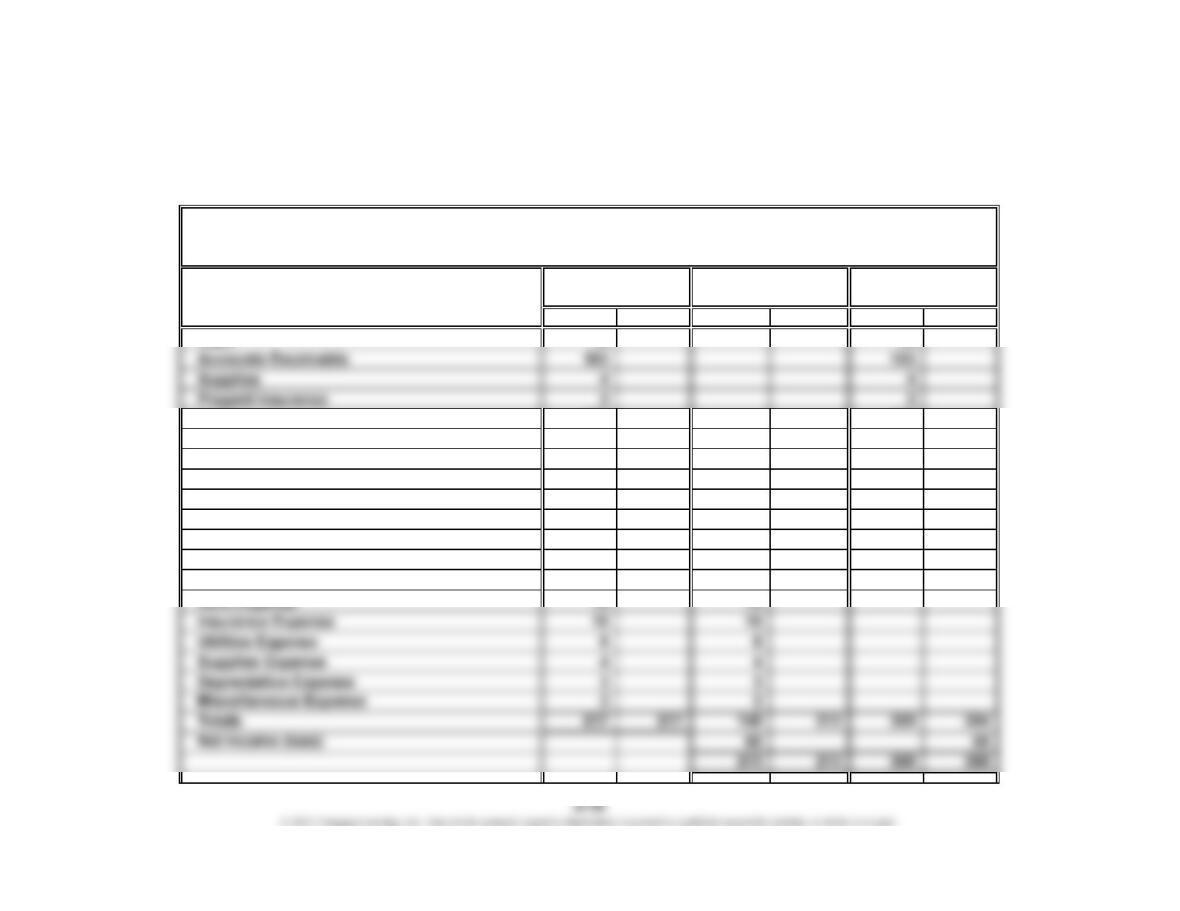

Appendix 1 Ex. 4-25

Account Title Debit Credit Debit Credit

Land 190 190

Equipment 50 50

Accumulated Depreciation 7 7

Accounts Payable 36 36

Wages Payable 1 1

Brenda Schultz, Capital 260 260

Brenda Schultz, Drawing 8 8

Fees Earned 213 213

Wages Expense 111 111

Alert Security Services Co.

End-of-Period Spreadsheet (Work Sheet)

For the Year Ended October 31, 20Y7

Adjusted BalanceIncome

Debit Credit

Trial Balance Statement Sheet

CHAPTER 4 Completing the Accounting Cycle

Appendix 1 Ex. 4-26

Fees earned $213

Expenses:

Wages expense $111

Rent expense 12

Brenda Schultz, capital, November 1, 20Y6 $260

Net income $65

Statement of Owner’s Equity

For the Year Ended October 31, 20Y7

Alert Security Services Co.

Income Statement

For the Year Ended October 31, 20Y7

Alert Security Services Co.