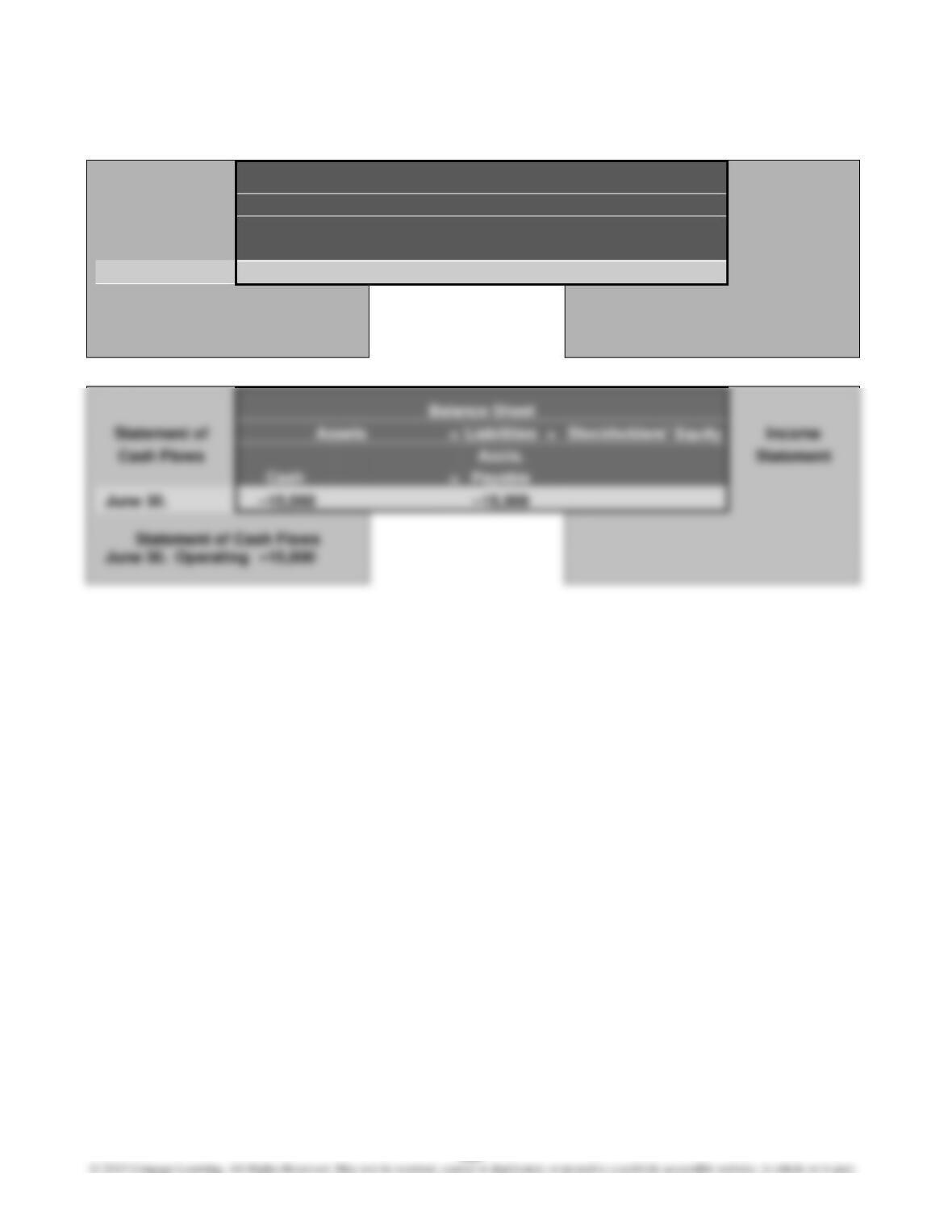

119

P4–1, Concluded

4. a. The multiple-step form of income statement contains various sections

for revenues and expenses, with intermediate balances, and concludes

with net income. In the single-step form, the total of all expenses is

P4–2

1.

AQUA CO.

Income Statement

For the Year Ended June 30, 20Y8

Revenues:

Net sales ……………………………………………………………. $3,567,000

Expenses:

Cost of merchandise sold …………………………………… $2,175,000

2.

AQUA CO.

Retained Earnings Statement

For the Year Ended June 30, 20Y8

Retained earnings, July 1, 20Y7 …………………………………. $253,800

Net income for the year …………………………………………….. $775,000

120

P4–3

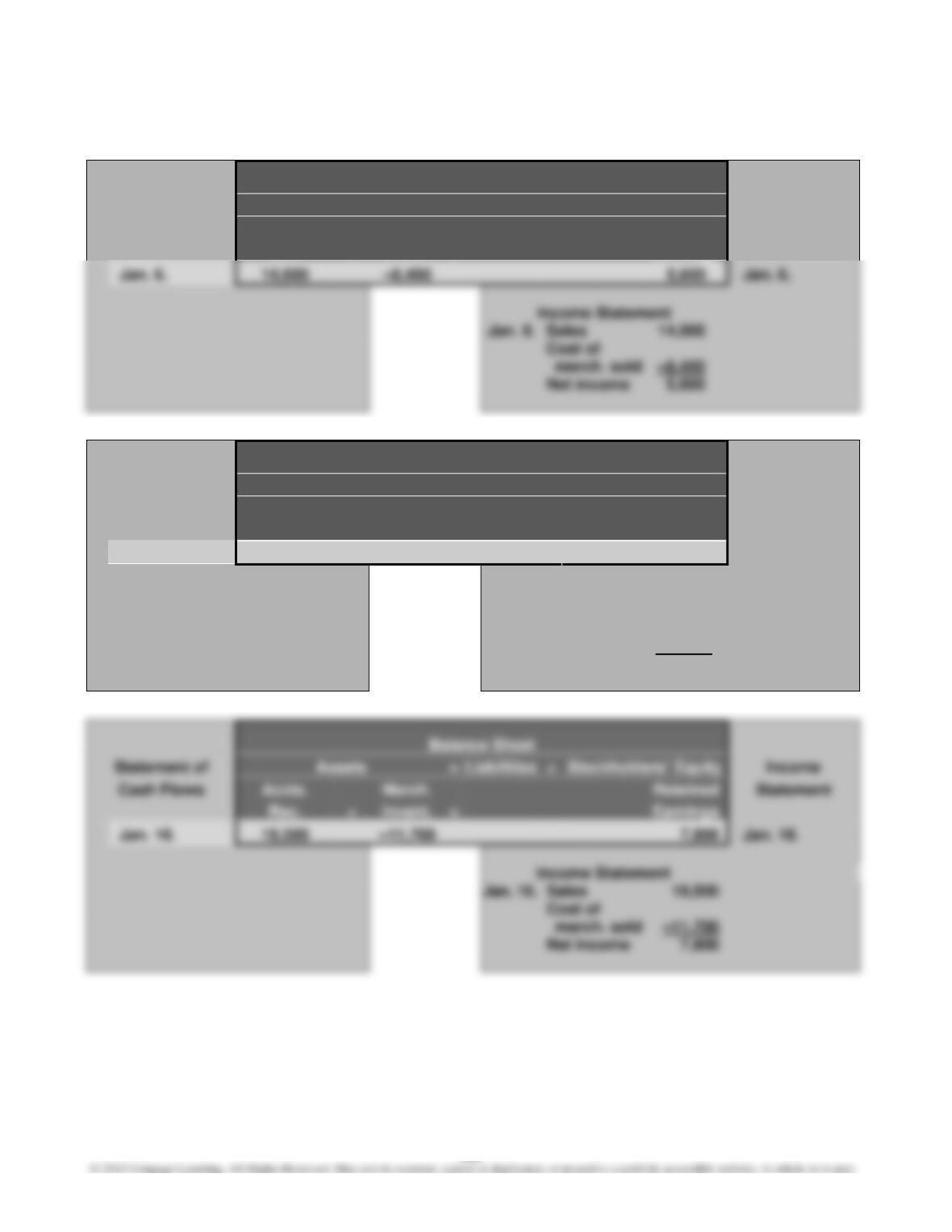

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Retained

Statement

Rec.

+

Invent.

=

Earnings

Jan. 6.

Jan. 6.

Income Statement

Jan. 6.

Sales

merch. sold

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Retained

Statement

Rec.

+

Invent.

=

Earnings

Jan. 8.

20,000

–14,000

6,000

Jan. 8.

Income Statement

Jan. 8.

Sales

20,000

Cost of

merch. sold

–14,000

Net income

6,000

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Retained

Statement

Rec.

+

Invent.

=

Earnings

Jan. 16.

–11,700

7,800

Jan. 16.

Income Statement

Jan. 16.

Sales

19,500

merch. sold

Net income

7,800

121

P4–3, Continued

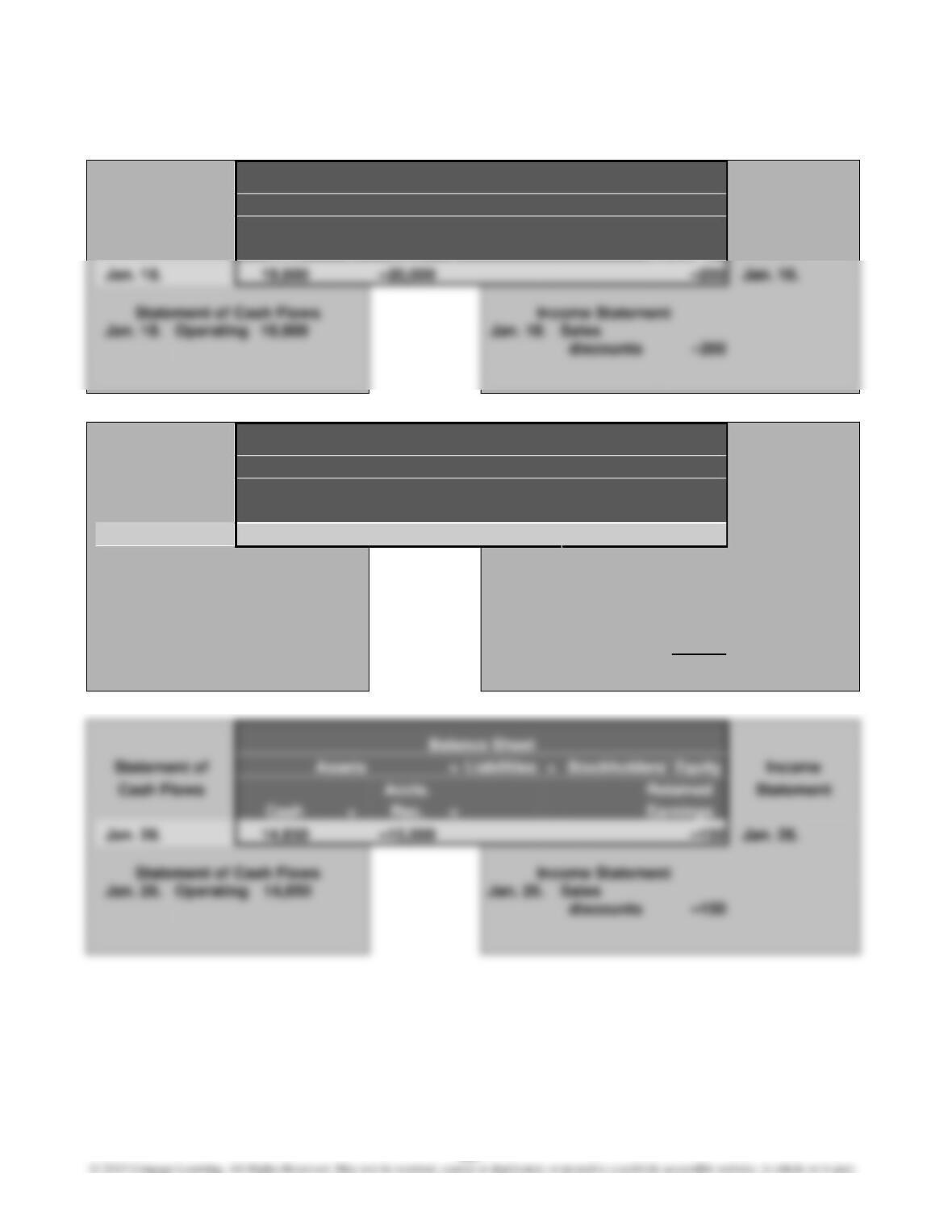

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Retained

Statement

Cash

+

Rec.

=

Earnings

Jan. 18.

Jan. 18.

Income Statement

Jan. 18.

Operating

Jan. 18.

Sales

discounts

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Retained

Statement

Rec.

+

Invent.

=

Earnings

Jan. 19.

–4,500

2,700

–1,800

Jan. 19.

Income Statement

Jan. 19.

Sales returns

& allow.

–4,500

Cost of

merch. sold

2,700

Net income

–1,800

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Retained

Statement

Cash

+

Rec.

=

Earnings

Jan. 26.

Jan. 26.

Income Statement

discounts

122

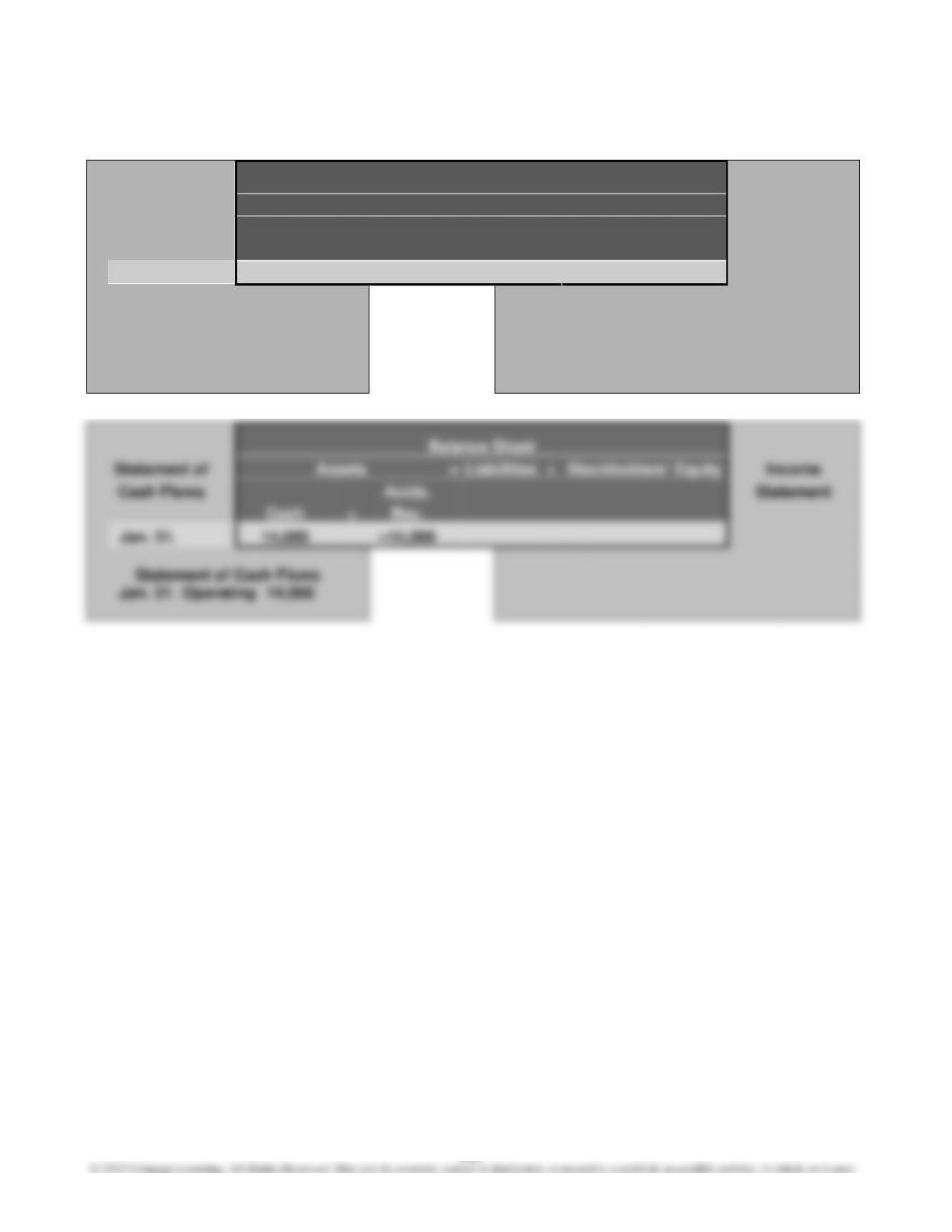

P4–3, Concluded

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Retained

Statement

Cash

=

Earnings

Jan. 31.

–3,000

–3,000

Jan. 31.

Statement of Cash Flows

Income Statement

Jan. 31.

Operating

–3,000

Jan. 31.

Delivery

exp.

–3,000

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Statement

Cash

Jan. 31.

Statement of Cash Flows

Jan. 31.

Operating

14,000

123

P4–4

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Invent.

=

Payable

Aug. 3.

33,400

33,400

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Invent.

=

Payable

Aug. 9.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Cash

+

Invent.

=

Payable

Aug. 10.

–600

25,600

25,000

Statement of Cash Flows

Aug. 10.

Operating

–600

124

P4–4, Concluded

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Statement

Cash

=

Payable

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Statement

Cash

=

Payable

125

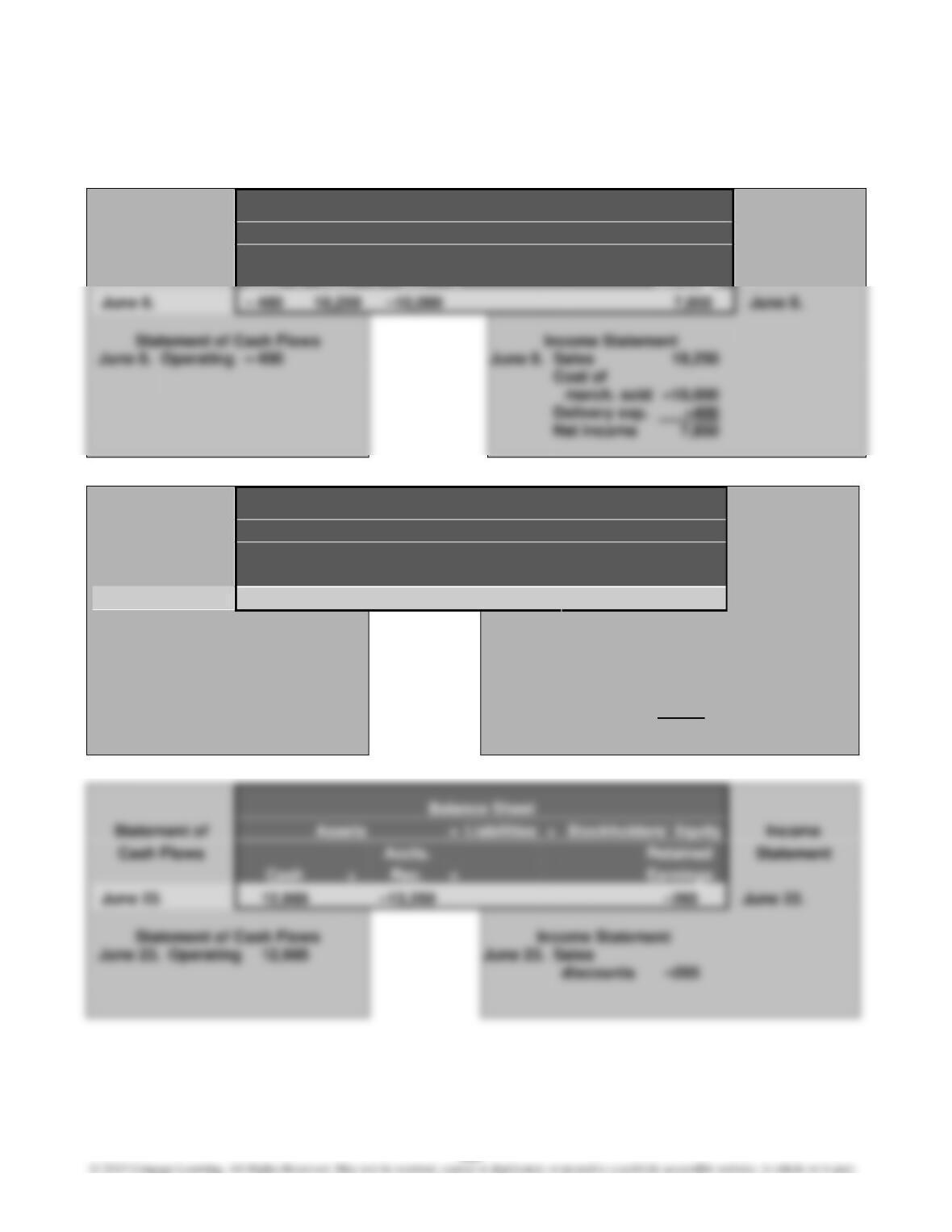

P4–5

1.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Retained

Statement

Cash

+

Rec.

+

Inv.

=

Earnings

June 8.

June 8.

Income Statement

June 8.

Operating

– 400

June 8.

Sales

Delivery exp.

Net income

7,850

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Retained

Statement

Rec.

+

Invent.

=

Earnings

June 12.

–5,000

3,000

–2,000

June 12.

Income Statement

June 12.

Sales returns

& allow.

–5,000

Cost of

merch. sold

3,000

Net income

–2,000

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Retained

Statement

+

=

Earnings

June 23.

June 23.

Income Statement

June 23.

Operating

12,985

June 23.

Sales

discounts

–265

126

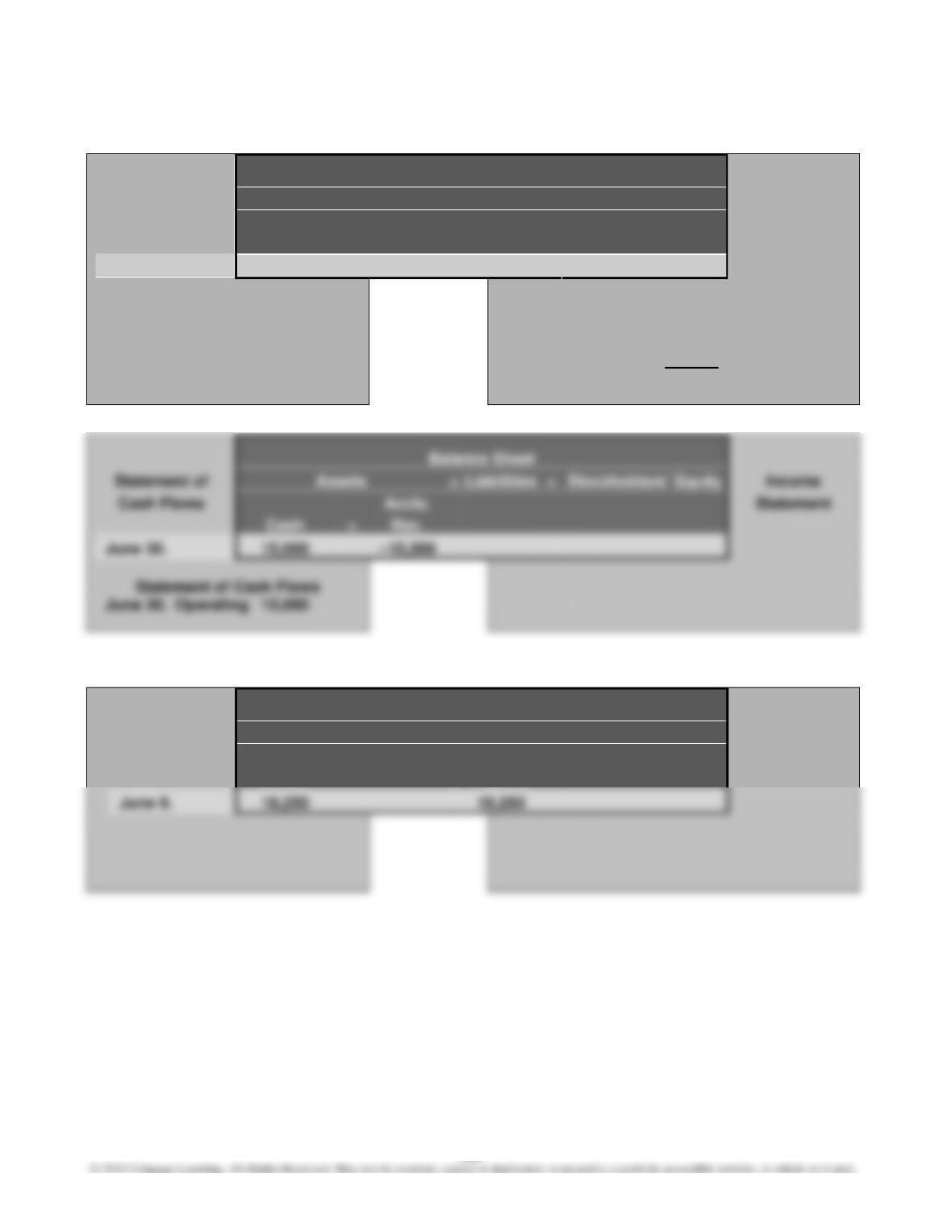

P4–5, Continued

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Retained

Statement

Rec.

+

Inventory

=

Earnings

June 24.

15,000

–9,000

6,000

June 24.

Income Statement

June 24.

Sales

15,000

Cost of

merch. sold

–9,000

Net income

6,000

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Statement

+

June 30.

15,000

June 30.

Operating

2.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Invent.

=

Payable

June 8.

18,250

127

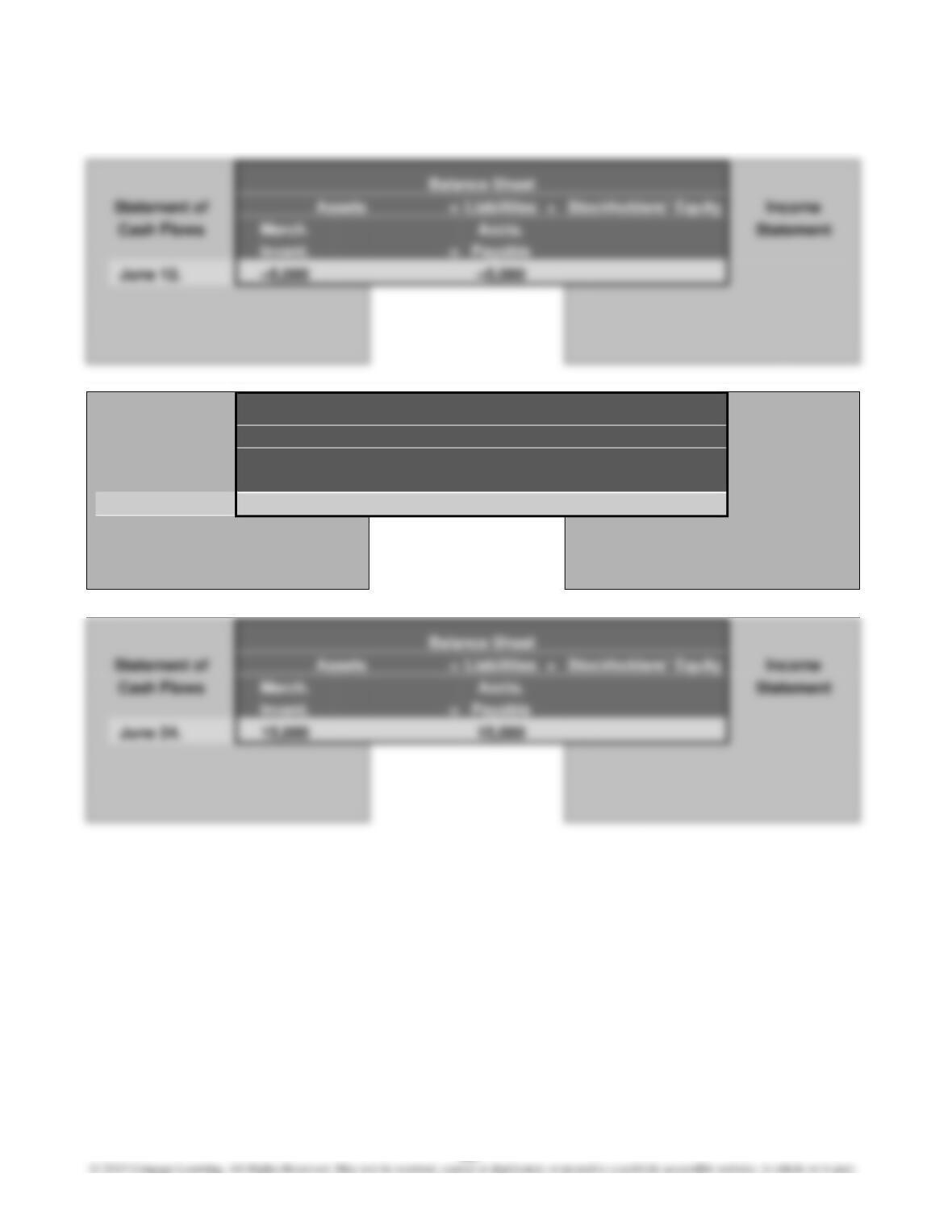

P4–5, Continued

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Statement

=

Payable

June 12.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Cash

+

Invent.

=

Payable

June 23.

–12,985

–265

–13,250

Statement of Cash Flows

June 23.

Operating

–12,985

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Statement

=

Payable

June 24.

128

P4–5, Concluded

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Statement

Cash

+

Inv.

June 26.

–375

375

Statement of Cash Flows

June 26.

Operating

–375

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Statement

Cash

=

Payable

June 30.

Statement of Cash Flows

June 30.

Operating

–15,000

129

P4–6 (Appendix)

1.

OMEGA SYSTEMS INC.

Statement of Cash Flows

For the Year Ended March 31, 20Y5

Cash flows from operating activities:

Decrease in prepaid insurance …………….. 525

Increase in accounts payable ………………. 12,225

Decrease in salaries payable ………………. (540)

Decrease in unearned rent ………………….. (900) (6,845)

Net cash flows from operating activities …… $ 98,605

2. Depreciation is added to net income in determining net cash flows from op-

erating activities. This is because depreciation is deducted in arriving at net

income, but it does not involve any cash payments.

130

FINANCIAL ANALYSIS

FA4–1

1. Year 2 Year 1

2. Average markup percent:

($20,561 ÷ $86,539) …………. 23.8%

($20,219 ÷ $75,559) …………. 26.8%

3. Ratio of sales to assets:

4. The gross profit percent declined 1.9% from 21.1% in Year 1 to 19.2% in Year

2. This is an unfavorable trend. Likewise, the average markup percent de-

clined 3.0% from 26.8% in Year 1 to 23.8% in Year 2. This is consistent with

131

FA4–2

The gross profit percent, average markup percent, and ratio of sales to assets for

CVS and Walgreen are summarized below.

Gross Profit Average Markup Ratio of Sales to

Percent Percent Average Assets

Walgreen:

Year 1 ………… 28.4% 39.6% 2.69

Year 2 ………… 28.4% 39.7% 2.35

Walgreen also uses its assets more efficiently to generate sales than does CVS.

In Year 2, Walgreen generated $2.69 of sales per dollar of invested asset while

CVS generated only $1.55 per invested asset. This could be due to CVS’s rapid

expansion of opening new stores. Sales of new stores could lag initially and then

grow more over time as the stores generate a customer base.

132

FA4–3

1. Year 2 Year 1

2. Average markup percent:

($11,149 ÷ $25,008) …………. 44.6%

($10,093 ÷ $21,919) …………. 46.0%

3. Ratio of sales to assets:

4. Deere & Company’s financial performance declined slightly from Year 1 to

Year 2. Deere’s gross profit percent decline 0.7% from 31.5% to 30.8%. Like-

wise, the average markup percent declined 1.4% from 46.0% in Year 1 to

44.6% in Year 2. This is consistent with the decline in the gross profit percent

and is a small unfavorable trend. Finally, the ratio of sales to assets declined

FA4–4

1. Year 2 Year 1

Gross profit percent:

($15,734 ÷ $60,138) …………. 26.2%

($11,307 ÷ $42,588) …………. 26.5%

2. Average markup percent:

3. Ratio of sales to assets:

4. Caterpillar Inc.’s gross profit percent declined 0.3% from 26.5% to 26.2%.

Likewise, the average markup percent declined 0.7% from 36.1% in Year 1 to

133

FA4–5

The gross profit percent, average markup percent, and ratio of sales to assets for

Deere and Caterpillar are summarized below.

Gross Profit Average Markup Ratio of Sales to

FA4–6

1. In order to earn a significant profit, companies with low gross profit and

markup percents must sell more merchandise. Thus, the ratio of sales to as-

2. Kroger Tiffany

Gross profit percent:

($18,880 ÷ $90,374) …………. 20.9%

($2,151 ÷ $3,643) …………….. 59.0%

3. The results in part (2) for Kroger and Tiffany support the prior statements.

Kroger has a lower gross profit percent of 20.9% and an average markup per-

cent of 26.4% than does Tiffany which has a gross profit percent of 59.0% and

an average markup percent of 144.2%. Likewise, Kroger has a ratio of sales to

assets of 3.85 compared to Tiffany’s 0.92.

CASES

Case 4–1

Standards of Ethical Conduct for Management Accountants requires manage-

ment accountants to perform in a competent manner and to comply with relevant

laws, regulations, and technical standards. If Mary Jasper intentionally subtracted

Case 4–2

Paul Laurel is correct. The accounts payable due suppliers could be included on

the balance sheet at an amount of $177,000 ($147,000 + $30,000). This is the

amount that will be expected to be paid to satisfy the obligation (liability) to sup-

Case 4–3

1. If Eric doesn’t need the stereo immediately (by the next day), Dynamic Sound

Systems offers the best buy, as shown below.

Dynamic Sound Systems:

List price ……………………………………………………………………. $899.99

Shipping and handling (not including next-day air) ………. 13.99

Sales tax (6%) …………………………………………………………….. 52.87

Total …………………………………………………………………………… $933.97

If Eric needs the stereo immediately (the next day), then First Audio has the

best price. This is because a shipping and handling charge of $44.99 would

be added to Dynamic Sound Systems’ price, as shown below.

Case 4–3, Concluded

First Audio price (see previous page) ………………………….. $943.40

Less first installment (down payment) …………………………. 314.47

Remaining balance ……………………………………………………… $628.93

The total interest savings would be $14.29 ($9.43 + $4.86), which would lower

First Audio’s price to $929.11, as shown below.

Classic Audio price (see above) …………………………………… $943.40

Less interest savings ………………………………………………….. 14.29

Total …………………………………………………………………………… $929.11

The interest savings, however, would not be enough to just offset the price

advantage of Dynamic Sound Systems. Dynamic Sound Systems still has a

price advantage of $15.13 ($929.11 – $913.98) over First Audio.

2. Other considerations in buying the stereo include the ability to have the

stereo repaired locally by First Audio. In addition, First Audio employees

Case 4–4

1.

HARBOR READY PARTS COMPANY

Projected Income Statement

For the Year Ended October 31, 20Y7

Revenues:

Net sales (a) ……………………………………………………….. $1,380,000

Interest revenue …………………………………………………. 15,000

Total revenues ………………………………………………… $1,395,000

Notes:

(a) Projected net sales

[$1,200,000 + (15% × $1,200,000)] ……………………… $1,380,000

(b) Projected cost of merchandise sold

($1,380,000 × 65%) …………………………………………… $ 897,000

Add: Increase in office supplies expense

($4,000 × 15%) …………………………………….. $ 600

Increase in miscellaneous administrative

expense ($2,000 × 15%) ……………………….. 300 900

Projected total administrative expenses ………………. $ 75,900

138

Case 4–4, Concluded

2. Yes. The proposed change will increase net income from $183,350 to

$290,000, a change of $106,650.

3. Possible concerns related to the proposed changes include the following:

The primary concern is with the accuracy of the estimates used for projecting

the effects of the proposed changes. If the increase in sales does not materi-

alize, Harbor Ready Parts Company could incur significant costs of carrying

Case 4–5

Note to Instructors: The purpose of this activity is to familiarize students with

the variety of possible purchase prices for a fairly common household item.

Students should report several alternative prices when they consider the

source of the purchase and the other factors that affect the purchase, e.g., de–

livery, financing, warranties, etc.