Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Brief

Exercises

B. Ex. 4.1

B. Ex. 4.2

B. Ex. 4.3

B. Ex. 4.4 Analysis

B. Ex. 4.5

B. Ex. 4.6

B. Ex. 4.7

B. Ex. 4.8

B. Ex. 4.9

B. Ex. 4.10

Learning

Objectives

4.1 4-1–4-9

4.2 4-1–4-6, 4-9

4.3 4-1-4-7

4.4 Deferred expenses and revenue 4-1-4-7 Analysis

4.5 Accrued revenue 4-1-4-7 Analysis

4.6 4-1, 4-2, 4-4 Analysis

4.7 Accruals and deferrals 4-1-6, 4-9 Analysis

4.8 Notes payable and interest 4-1, 4-2, 4-5 Analysis

4.9 4-1–4-7, 4-9

4.10

4-1, 4-3–4-5,

4-7

4.11 4-1, 4-4, 4-7

Deferred revenue

4.12 4-1–4-7, 4-9

4.13 Effects of adjusting entries 4-1–4-6 Analysis

4.14 4-1–4-8

4.15 4-1, 4-2

Accounting terminology

Analysis

Analysis

Analysis

Skills

Analysis, judgment

Communication, analysis

Communication, analysis

Analysis, judgment

Communication, analysis,

judgment

Analysis

Concept of materiality

Interpreting business transactions

4-8

Deferred expenses and revenue

Analysis

Accounting for supplies

Analysis

Accounting for depreciation

4-3

Adjustments and the balance sheet

Real World: Various firms

Accounting principles

Analyzing the adjusted trial balance

Real World: Home Depot Using

an annual report

Deferred revenue

Real World: American Airlines

Effects of adjusting entries

Exercises

4-6

Analysis

Analysis

Analysis

Analysis

Accrued taxes

Accrued revenue

Unearned revenue

4-4

Accrued salaries

4-5

4-5

Accrued interest

4-5

Judgment, communication,

analysis

Topic

CHAPTER 4

THE ACCOUNTING CYCLE:

ACCRUALS AND DEFERRALS

4-3, 4-4

Analysis

Deferred expenses and revenue

4-3

Topic

Objectives

Deferred expenses and revenue

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

Learning

Skills

4-3, 4-4

Analysis

Problems Learning

Sets A, B Objectives

4.1 A,B 4-1-4-7

4.2 A,B 4-1–4-6, 4-9

4.3 A,B Analysis of adjusted data 4-1–7, 4-9

4.4 A,B 4-1–7, 4-9

4-1–7, 4-9

4.5 A,B 4-1–7, 4-9

4-1–7, 4-9

4.6 A,B

Preparing and analyzing adjusting

entries

4-1–7, 4-9

4.7 A,B

Preparing and analyzing adjusting

entries

4-1–7, 4-9

4.8 A,B 4-1–7, 4-9

4.1 4-1–4-7

4.2

Real World: Avis

4-8

The concept of materiality

4.3 4-3, 4-7, 4-8

4.4

accounts involved in adjusting 4-1–4-6

Analysis

Analysis, communication

Analysis, communication

Skills

Preparing and analyzing adjusting

entries

Topic

Preparing and analyzing adjusting

entries

process (Internet)

Expense Manipulation (Ethics,

fraud & corporate governance)

Analysis, communication

Analyzing the effects of errors

Preparing and analyzing adjusting

entries

Analysis, communication

Preparing and analyzing adjusting

entries

Critical Thinking Cases

Real World: Hershey Identifying

Determining whether adjusting

entries are required

Communication, technology,

judgment, research

Analysis, communication

Analysis, communication

Analysis, judgment,

communication

Communication, judgment,

analysis

Analysis, judgment,

communication

Analysis

DESCRIPTIONS OF PROBLEMS AND CRITICAL THINKING CASES

Problems (Sets A and B)

4.1 A,B 20 Easy

4.2 A,B 40 Medium

4.3 A,B 25 Strong

4.4 A,B

4.5 A,B 30 Medium

4.6 A,B 30 Medium

Terrific Temps/Marvelous Music

Requires students to prepare adjusting entries and determine

amounts reported in the financial statements.

Alpine Expeditions/Mate Ease

Requires students to prepare adjusting entries, determine

amounts reported in the financial statements, and interpret

certain deferrals.

Requires students to prepare adjusting entries and interpret

financial information.

Below are brief descriptions of each problem and case. These descriptions are accompanied by the

estimated time (in minutes) required for completion and by a difficulty rating. The time estimates

assume use of the partially filled-in working papers.

30 Medium

Campus Theater/Off-Campus Playhouse

Requires students to prepare adjusting entries, analyze financial

information, and interpret differences between income taxes

expense and income taxes payable.

Gunflint Adventures/River Rat

Requires students to prepare adjusting entries, classify them as

accruals or deferrals, and discuss the difference between the

book value of an asset and its fair market value.

Requires students to prepare adjusting entries, classify them as

accruals or deferrals, analyze their effects on the financial

statements, and report assets at book value in the balance sheet.

Florida Palms Country Club/Georgia Gun Club

Enchanted Forest/Big Oaks

Problems (continued)

Ken Hensley Enterprises, Inc./Stillmore Investigations 60 Strong

Requires students to journalize adjusting entries, prepare an adjusted trial

balance, and understand various relationships among financial statement

elements.

Coyne Corporation/Stephen Corporation

Requires students to analyze the effects of errors on financial statement

elements.

Critical Thinking Cases

Judgments and Year-End Adjustments

The Concept of Materiality

Expense Manipulation

Ethics, Fraud & Corporate Governance

Identifying Accounts

Internet

4.7 A,B

4.8 A,B

20 Strong

Students are asked to identify accounts in Hershey’s balance sheet that

were most likely to have been involved in the company’s year-end

adjusting entry process.

4.4

10 Easy

Requires students to exercise judgment regarding the need for adjusting

entries.

Discusses the concept of materiality. The purchase of automobiles by

Avis for its rental fleet is used to illustrate how the cumulative effect of

many immaterial transactions can become material.

Students must determine whether the capitalization of advertising

expenditures was in compliance with generally accepted accounting

principles, and whether the decision to do so was ethical.

10 Easy

4.3

30 Medium

4.2

25 Medium

4.1

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

1.

2.

3.

4.

5.

6.

The purpose of making adjusting entries is to recognize certain revenue and expenses that

All adjusting entries affect both an income statement account and a balance sheet account.

Making adjusting entries requires a better understanding of accrual accounting than does the

Under accrual accounting, an expense is defined as the cost of goods and services used in

Accrual accounting requires that revenue be recognized in the accounting records when it is

The term, unearned revenue, describes amounts that have been collected from customers in

7.

8.

9.

10.

11.

15.

Carnival Corporation accounts for customer deposits as deferred, or unearned, revenue. As

Materiality refers to the relative importance of an item or an event to the users of financial

statements. An item is “material” if knowledge of it might reasonably influence the decisions

of financial statement users.

12.

Deferred revenue (also referred to as unearned revenue or customer deposits) is reported in the

The realization principle governs the timing of revenue recognition. The principle states that

A $1,000 expenditure is not considered material to all businesses. Most large enterprises

Deferred expenses are those assets reported in the balance sheet that will later become

The matching principle governs the manner in which revenue is offset by the expenses

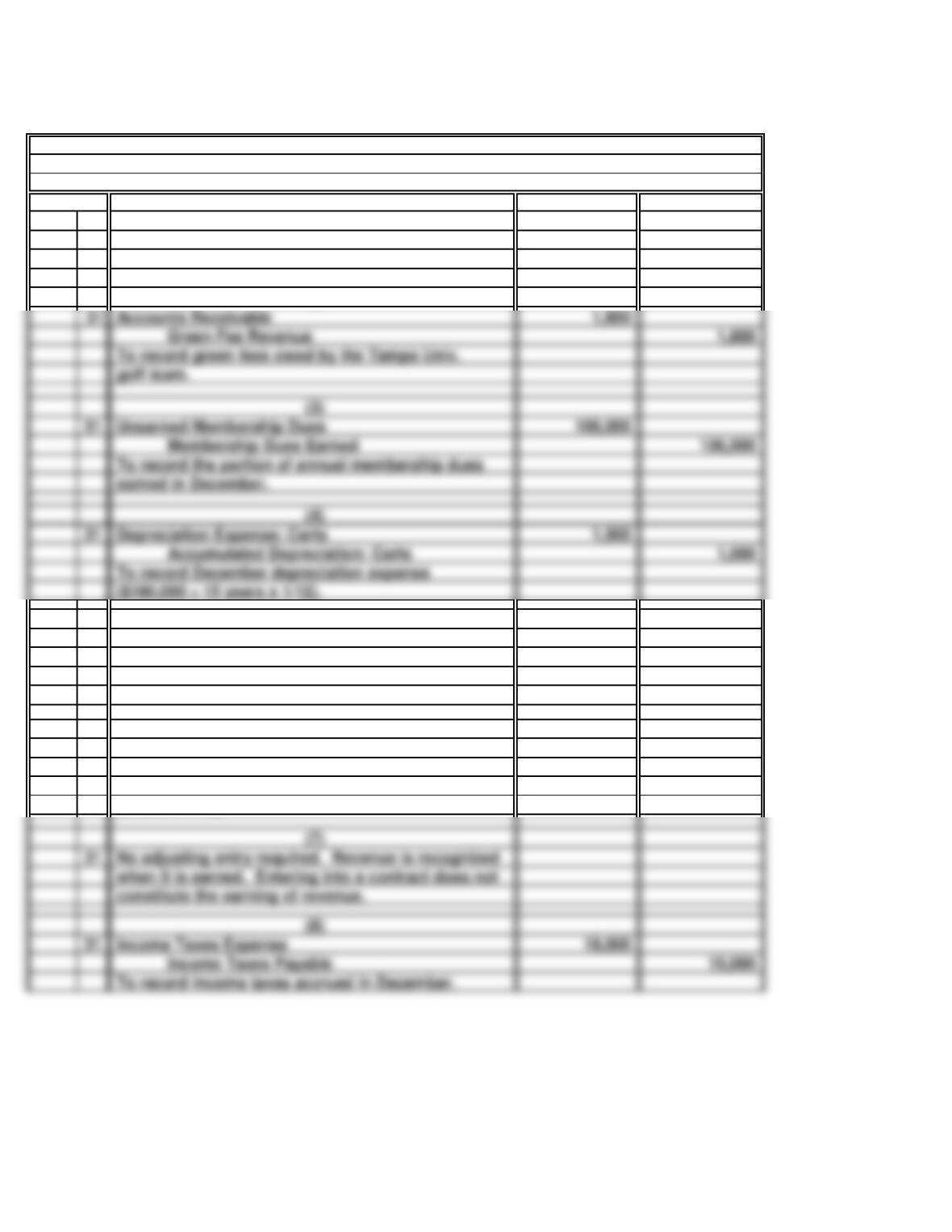

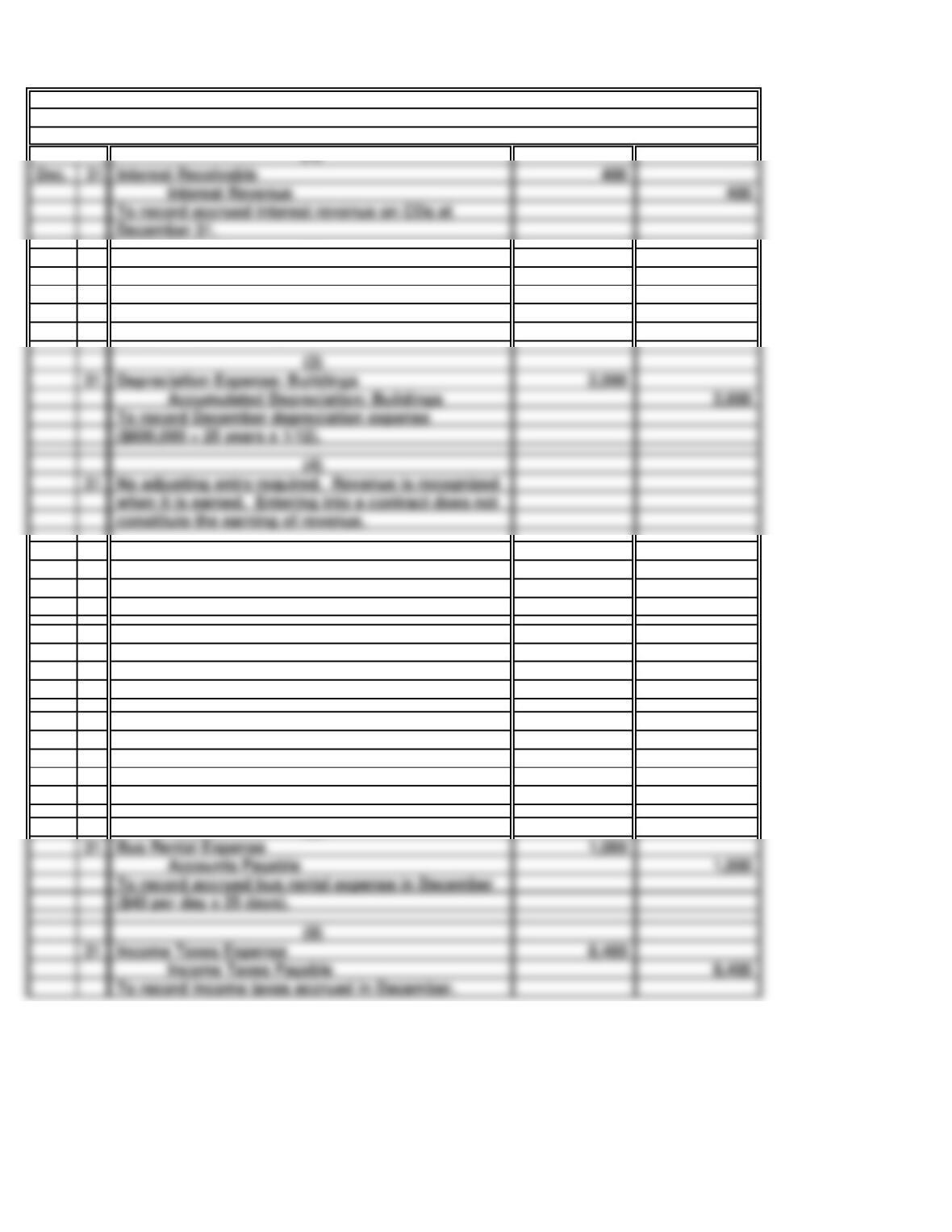

B. Ex. 4.1 a. Nov. 30 750

Unexpired Insurance …………………….

750

B. Ex. 4.2 a. Feb. 28 300

Prepaid Rent ………………………………………………

300

B. Ex. 4.3 Mar 31 1,300

B. Ex. 4.4 a. Dec. 31 1,800

Accumulated Depreciation: Equipment …………………………………….

1,800

B. Ex. 4.5 3,250

Client Service Revenue ………………………………………

3,250

Insurance Expense ……………………………………………………..

Rent Expense …………………………………………………

Office Supplies Expense ………………………………………………….……….

Depreciation Expense: Equipment…………………………….

Accounts Receivable ………………………………………….

B. Ex. 4.6 a. 2,500

Client Revenue Earned …………………

2,500

B. Ex. 4.7 a. Dec. 31 210,000

Salaries Payable ………………………………………………

210,000

B. Ex. 4.8 a. Dec. 31 200

B. Ex. 4.9 a. Dec. 31 15,000

Income Taxes Payable………………………………………

15,000

Unearned Client Revenue ……………………………………………………..

Interest Expense ………………………………………………….……….

Salaries Expense …………………………………………………

Income Taxes Expense ………………………………………….

B. Ex. 4.10 a.

b.

c.

1.

Materiality refers to the relative importance of an item. An item is material if

knowledge of it might reasonably influence the decisions of users of financial

Whether a specific dollar amount is “material” depends upon the (1) size of the

amount and (2) nature of the item. In evaluating the size of a dollar amount,

accountants consider the amount in relation to the size of the organization.

Two ways in which the concept of materiality may save time and effort for

accountants are:

Adjusting entries may be based upon estimated amounts if there is little or no

Ex 4.1 a.

Ex. 4.2

Revenue -Expenses = Assets -Liabilities =

NE I D D NE D

Ex. 4.3 1. 250,000

2. 750,000

Unearned Ticket Revenue ……………………………………………..

Balance Sheet

Owners'

Equity

Net

Income

Rent Expense ………………………………………………………….

Income Statement

SOLUTIONS TO EXERCISES

Book value

a.

Adjusting

Entry

Ex. 4.4 a.

b. 2,400,000

c. 48,000,000

d.

Ex. 4.5 a. (1) 375

Ex. 4.6 a.

At the time cash is collected by Delta Airlines for advance ticket sales, the entire

amount is accounted for as unearned revenue. The liability created represents the

The adjusting entry that results in the most significant expense in the

Customer Deposits ………………………………………………….

Prepaid Advertising is reported in the balance sheet as an asset as a component of

Advertising Expense ……………………………………………….

Interest Expense ………………………………………………….

Ex. 4.7 1,500

1,500

9,000

9,000

Ex. 4.8 a.

c.

150,000

Notes Payable ……………………………………………

150,000

The total interest expense over the life of the note is $4,500 ($150,000 x .06 x 6/12 =

$4,500).

Yr. 1

Oct.

31

Cash ……………………………………………………………..

Marketing Revenue Earned …………………………………..

5.

Unearned Revenue ………………………………………………………..

a. 1.

Interest Expense ………………………………………………………

Interest Payable ……………………………………………………

Ex. 4.9 a. May 1 600,000

Notes Payable …………………………….

600,000

b. May 1 86,400

Cash ………………………………………………

86,400

Paid rent for six months at $14,400 per month.

Cash ……………………………………………………..

Prepaid Rent …………………………………………………

c.

b.

Delta Air Lines: As passengers complete their flights or as the ticket expires unused.

Ex. 4.11

a.

When the company receives cash from its customer prior to earning any revenue it

Delta Air Lines.: Air Traffic Liability

Ex. 4.12 5,000

Fees Earned………………………………

5,000

50

Interest Payable…………………………..

50

Accounts Receivable………………………………………

To record accrued but uncollected revenue.

To record accrued but unpaid interest expense.

Interest Expense……………………………………

Ex. 4.13

Adjustment Net Owners'

Type Revenue Expenses Income Assets Liabilities Equity

Type I NE I D D NE D

Ex. 4.14 a.

Ex. 4.15

•

None (or Materiality). Accounting for immaterial items is not "wrong" or

Accounts requiring adjusting entries may include:

Receivables

20 Minutes, Easy

a.

Dec. 31 9,600

Salaries Payable 9,600

31 300

Interest Payable 300

31 650

Unexpired Insurance 650

SOLUTIONS TO PROBLEMS SET A

FLORIDA PALMS COUNTRY CLUB

(Adjusting Entries)

(1)

(2)

PROBLEM 4.1A

General Journal

To record December insurance expense

($7,800 x 1/12).

(5)

(6)

($45,000 x 8% x 1/12).

FLORIDA PALMS COUNTRY CLUB

Interest Expense

Salaries Expense

To record accrued salaries at December 31.

Insurance Expense

To record accrued interest expense in December

b.

1.

c.

The clubhouse was built in 1925 and has been fully depreciated for financial accounting

Accruing unpaid expenses.

PROBLEM 4.1A

FLORIDA PALMS COUNTRY CLUB (concluded)

40 Minutes, Medium

31 85

Interest Payable 85

31 1,250

Salaries Payable 1,250

31 2,400

Camper Revenue 2,400

31 900

Camper Revenue 900

advance ($5,400 ÷ 6 months).

(8)

a.

(Adjusting Entries)

General Journal

To record accrued interest expense in December

PROBLEM 4.2A

(7)

To record revenue earned from campers that paid in

To record camper revenue earned in December.

($12,000 x 8.5% x 1/12).

(5)

(6)

ENCHANTED FOREST

Unearned Camper Revenue

Camper Revenue Receivable

To record accrued salary expense in December.

Interest Expense

(1)

(2)

Salaries Expense

b.

1.

c.

Owners’

Revenue -Expenses = Assets = Liabilities + Equity

INE I I NE I

e.

PROBLEM 4.2A

Accruing uncollected revenue.

ENCHANTED FOREST (concluded)

Net

Income

Income Statement

Balance Sheet

1.

Adjustment

Original cost of buildings …………………………………………………

600,000$