CHAPTER 4 Completing the Accounting Cycle

Comp. Prob. 1 (Continued)

5. Optional (Appendix)

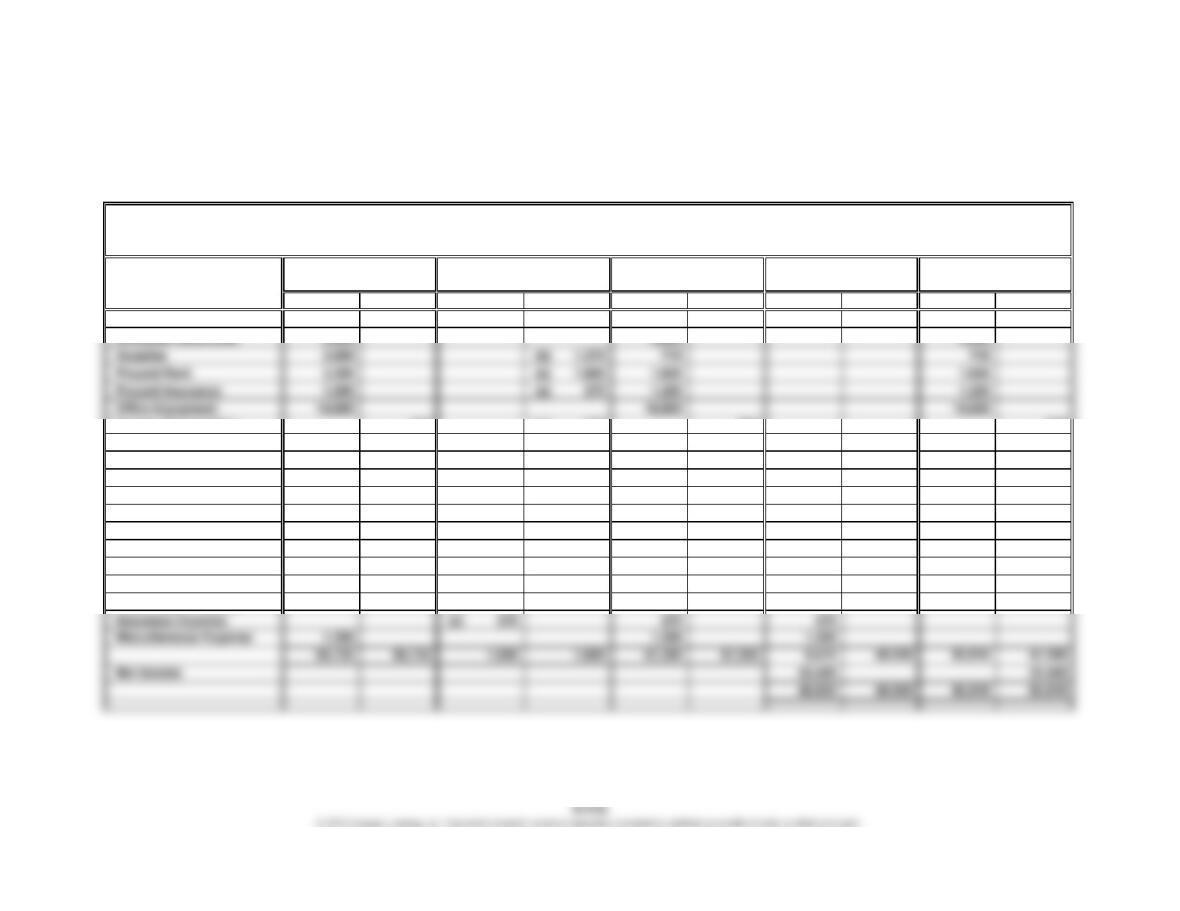

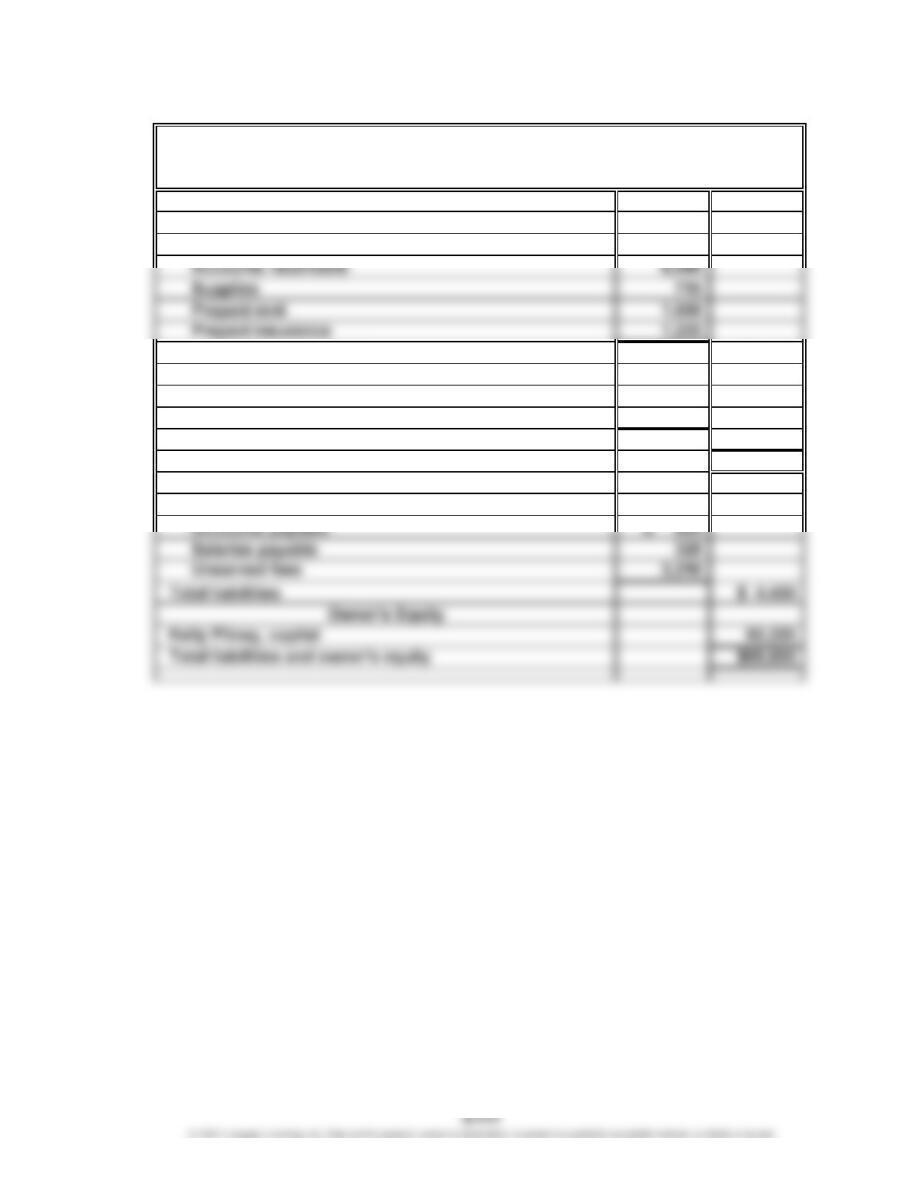

Account Title Debit Credit Debit Credit Debit Credit Debit Credit

Cash 44,195 44,195 44,195

Accum. Depreciation 330 (c) 330 660 660

Accounts Payable 895 895 895

Salaries Payable (d) 325 325 325

Unearned Fees 7,000 (f) 3,790 3,210 3,210

Kelly Pitney, Capital 42,300 42,300 42,300

Kelly Pitney, Drawing 10,500 10,500 10,500

Fees Earned 36,210 (f) 3,790 40,000 40,000

Salary Expense 1,380 (d) 325 1,705 1,705

Rent Expense (e) 1,600 1,600 1,600

Supplies Expense (b) 1,370 1,370 1,370

Depreciation Expense (c) 330 330 330

Kelly Consulting

End-of-Period Spreadsheet (Work Sheet)

For the Month Ended May 31, 20Y5

BalanceUnadjusted Adjusted Income

SheetTrial Balance

Debit Credit

Trial Balance StatementAdjustments

CHAPTER 4 Completing the Accounting Cycle

Comp. Prob. 1 (Continued)

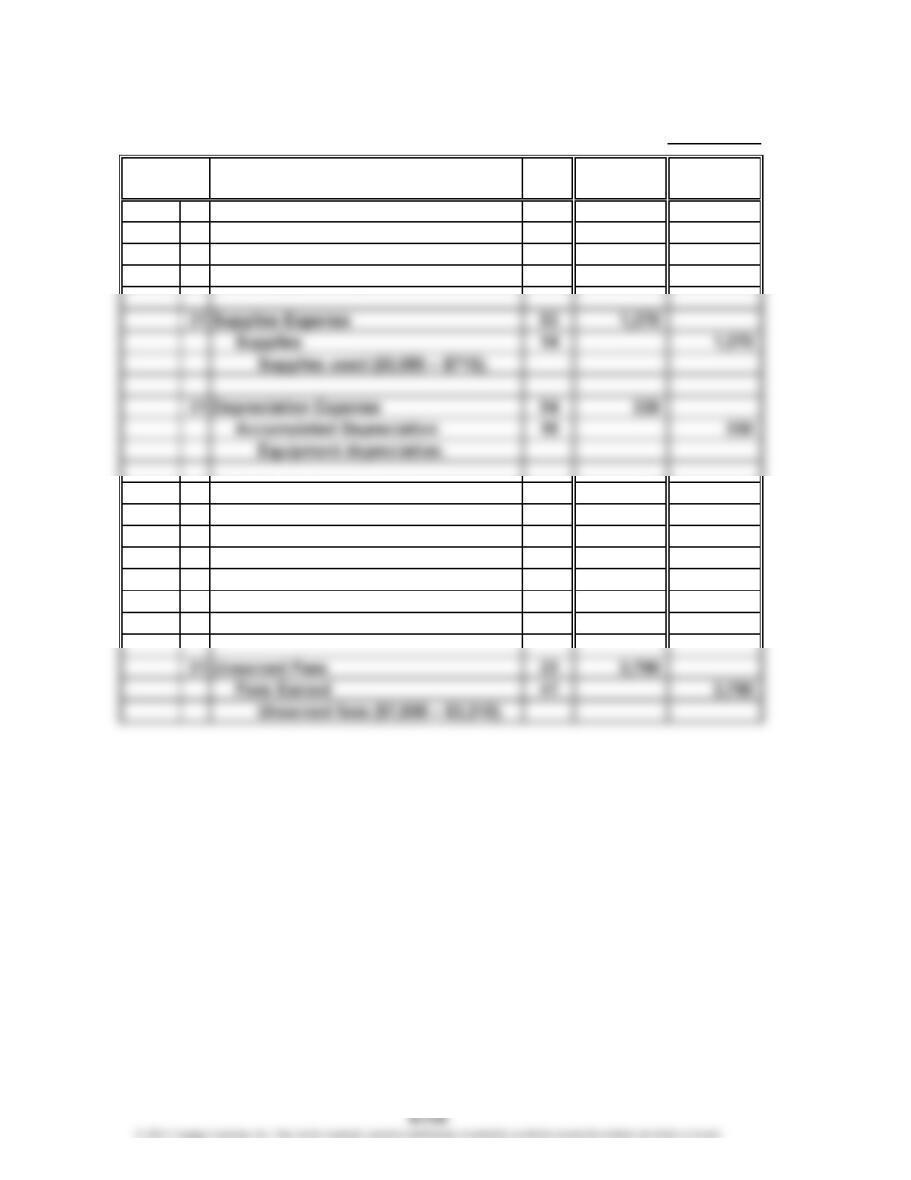

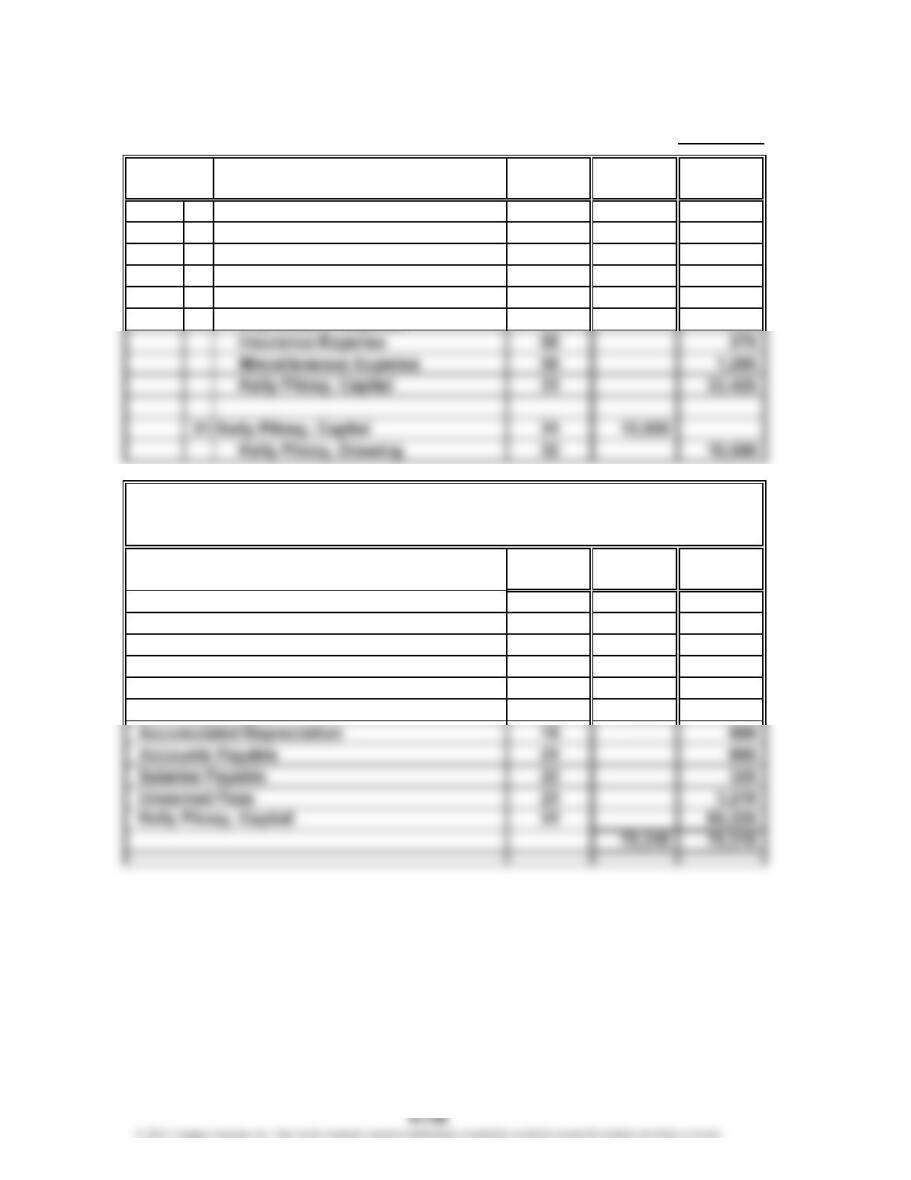

6. Page 7

Post.

Ref. Debit Credit

20Y5

May 31 Insurance Expense 55 275

Prepaid Insurance 16 275

Insurance expired.

31 Salary Expense 51 325

Salaries Payable 22 325

Accrued salaries.

31 Rent Expense 52 1,600

Prepaid Rent 15 1,600

Rent expired.

Date

Adjusting Entries

JOURNAL

CHAPTER 4 Completing the Accounting Cycle

Comp. Prob. 1 (Continued)

7.

Account Debit Credit

No. Balances Balances

Cash 11 44,195

Accounts Receivable 12 8,080

Accounts Payable 21 895

Salaries Payable 22 325

Unearned Fees 23 3,210

Kelly Pitney, Capital 31 42,300

Kelly Pitney, Drawing 32 10,500

Fees Earned 41 40,000

Salary Expense 51 1,705

Rent Expense 52 1,600

Adjusted Trial Balance

May 31, 20Y5

Kelly Consulting

CHAPTER 4 Completing the Accounting Cycle

Comp. Prob. 1 (Continued)

8.

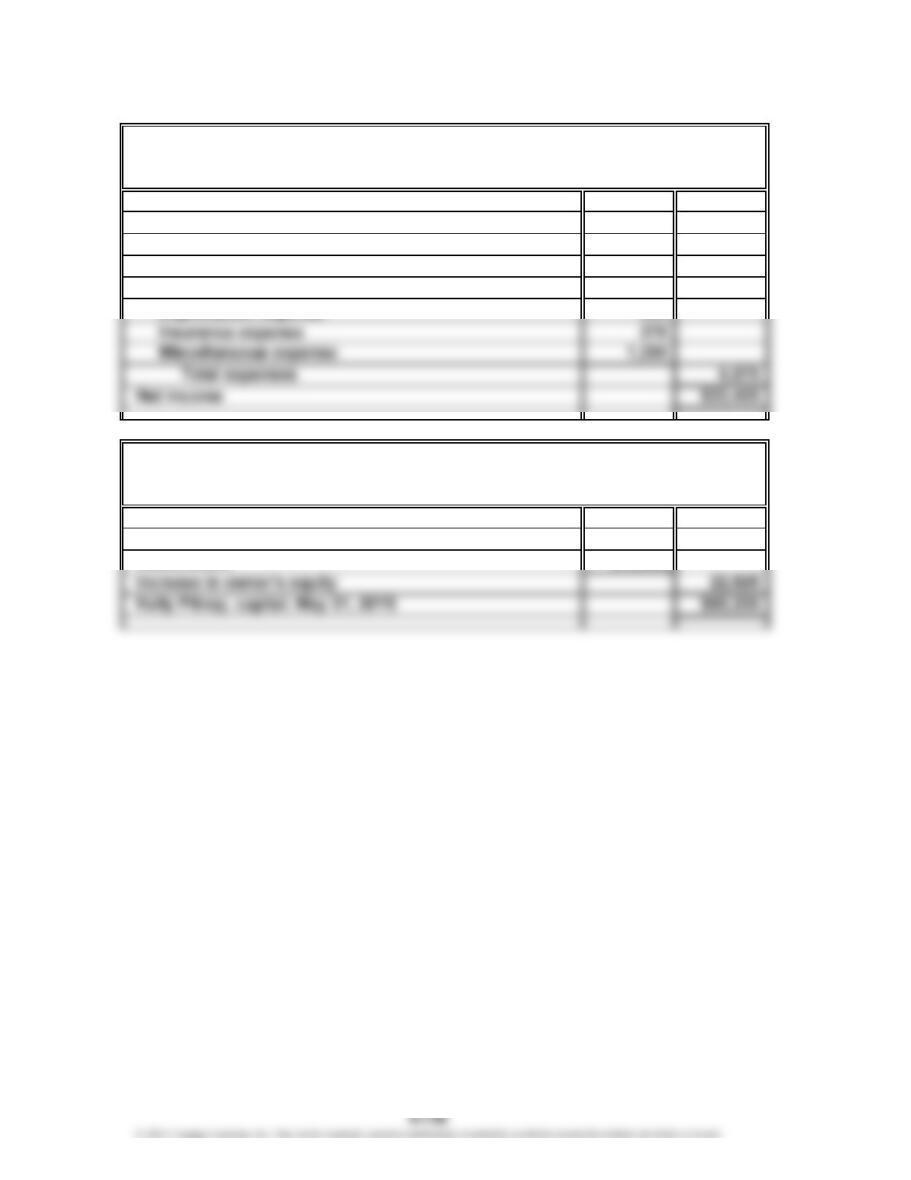

Fees earned $40,000

Expenses:

Salary expense $1,705

Rent expense 1,600

Supplies expense 1,370

Kelly Pitney, capital, May 1, 20Y5 $42,300

Net income for the month $ 33,425

Kelly Consulting

Statement of Owner’s Equity

For the Month Ended May 31, 20Y5

Kelly Consulting

Income Statement

For the Month Ended May 31, 20Y5

CHAPTER 4 Completing the Accounting Cycle

Comp. Prob. 1 (Continued)

Current assets:

Cash $44,195

Total current assets $55,815

Property, plant, and equipment:

Office equipment $14,500

Less accumulated depreciation 660

Total property, plant, and equipment 13,840

Total assets $69,655

Current liabilities:

Liabilities

Kelly Consulting

Balance Sheet

May 31, 20Y5

Assets

CHAPTER 4 Completing the Accounting Cycle

Comp. Prob. 1 (Concluded)

9. Page 8

Post.

Ref. Debit Credit

20Y5

May 31 Fees Earned 41 40,000

Salary Expense 51 1,705

Rent Expense 52 1,600

Supplies Expense 53 1,370

10.

Account Debit Credit

No. Balances Balances

Cash 11 44,195

Accounts Receivable 12 8,080

Supplies 14 715

Prepaid Rent 15 1,600

Prepaid Insurance 16 1,225

Office Equipment 18 14,500

JOURNAL

May 31, 20Y5

Closing Entries

Date

Kelly Consulting

Post-Closing Trial Balance

CHAPTER 4 Completing the Accounting Cycle

CP 4-1

1. No. By knowingly recording a personal loan as a normal account receivable, Manny

is reporting financial information that does not accurately reflect the company’s

financial position. Specifically, the company is reporting a noncurrent asset (a

CP 4-2

Solutions to this activity will vary according to the companies selected by the students.

CP 4-3

To: Daniel Nat

From: A+ Student

Re: Balance Sheet Presentation

The balance sheet describes the financial condition of the company as of a given date

and is useful in assessing the company’s financial soundness and liquidity. For balance

sheet information to be useful, it must be presented in a consistent manner and in

conformity with generally accepted accounting principles (GAAP). I have reviewed the

December 31, 20Y4, balance sheet of Asheville Company and have identified

several presentation errors that limit its usefulness. These errors include incorrectly

presenting accounts payable and Daniel Nat, capital as assets and incorrectly reporting

equipment as a liability. In addition, the order of the assets and liabilities reported on

the balance sheet is incorrect.

CASES & PROJECTS

CHAPTER 4 Completing the Accounting Cycle

CP 4-3 (Concluded)

Current assets:

Cash $ 10,000

Accounts receivable 12,500

Total current assets $ 22,500

Property, plant, and equipment:

Land $100,000

Equipment 125,000

Total property, plant, and equipment 225,000

Total assets $247,500

Asheville Company

Balance Sheet

For the Year Ended December 31, 20Y4

Assets

CP 4-4

1. (a) With the decreasing cost of computers and related software, Main Street

Co. may find it desirable to computerize its financial reporting system. In

many cases, the computerization of a manual accounting system reduces the

(c) In designing a computerized financial reporting (accounting) system,

proper accounting principles, concepts, and procedures must be followed.

At a minimum, basic controls such as the use of the double-entry accounting

system should be included. For example, debits must equal credits for all

transactions, and assets must equal liabilities plus owner’s equity. In addition,

the system should be designed to detect obvious errors, such as a credit

(minus) balance for Supplies or Prepaid Insurance. In other words, to design

2. Supplies cannot have a credit balance, because the supplies account is an asset

account. A business cannot have a “negative” asset. Thus, the only way a credit

balance could have occurred in Supplies is as the result of an error in recording one

or more transactions.

CHAPTER 4 Completing the Accounting Cycle

CP 4-5

1. A set of financial statements provides useful information concerning the

economic condition of a company. For example, the balance sheet describes

the financial condition of the company as of a given date and is useful in

2. The following adjustments might be necessary before an accurate set of

financial statements could be prepared:

No supplies expense is shown. The supplies account should be adjusted for

the supplies used during the year.

No depreciation expense or accumulated depreciation is shown for the

building or equipment accounts. An adjusting entry should be prepared for

depreciation expense on each of these assets.

An inquiry should be made as to whether any accrued expenses, such as

wages or utilities, exist at the end of the year.

An inquiry should be made as to whether any prepaid expenses, such as rent

or insurance, exist at the end of the year.

An inquiry should be made as to whether the owner withdrew any funds from

the company during the year. No drawing account is shown in the “Statement

of Accounts.”

CHAPTER 4 Completing the Accounting Cycle

CP 4-5 (Concluded)

3. In general, the decision to extend a loan is based on an assessment of the

profitability and riskiness of the loan. Although the financial statements

provide useful data for this purpose, other factors such as the following

might also be significant:

The due date and payment terms of the loan.

Security for the loan. For example, whether Joan Whalen is willing to pledge

personal assets (collateral) in support of the loan will affect the riskiness