4-34

PROBLEM 4-35 (CONTINUED)

Cost of goods completed and transferred out during November:

Cost remaining in November 30 work-in-process inventory

Direct material:

Conversion

Total cost of November 30 work in process ……………………………………………. $58,620

Check: Cost of goods completed and transferred out ……..

$323,200

Cost of November 30 work-in-process inventory …

58,620

Total costs accounted for ………………………………….

$381,820

2.

a. Work-in-Process Inventory: Mixing Department …………

85,000

Raw-Material Inventory …………………………………….

70,000

Wages Payable ………………………………………………..

c. Work-in-Process Inventory: Mixing Department …………

Manufacturing Overhead ………………………………….

*$140,000 = (1.50)($70,000) + ($35,000)

Work-in-Process Inventory: Mixing Department ..

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-35

PROBLEM 4-36 (35 MINUTES)

1.

Conversion cost per unit in department I:

*produced units

overhead ingmanufactur labordirect

+

=

*Note that all of the products sold after processing in departments I, II, or III were

produced orginally in department I.

2.

Conversion cost per unit in department II:

*produced units

overhead ingmanufactur labordirect

+

=

3.

Cost of a clear glass sheet:

=

direct material per

unit in department I

+

conversion cost per

unit in department I

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-36

PROBLEM 4-36 (CONTINUED)

4.

Cost of an unetched, colored glass sheet:

=

cost per clear

glass sheet

+

direct material

per unit in department II

+

conversion cost per

unit in department II

5.

Cost of an etched, colored glass sheet:

=

cost per unetched

colored glass sheet

+

conversion cost per

unit in department III

PROBLEM 4-37 (60 MINUTES)

1.

The unit costs and total costs for each of the products manufactured by Plattsburg

Plastics Corporation during the month of March are calculated as follows:

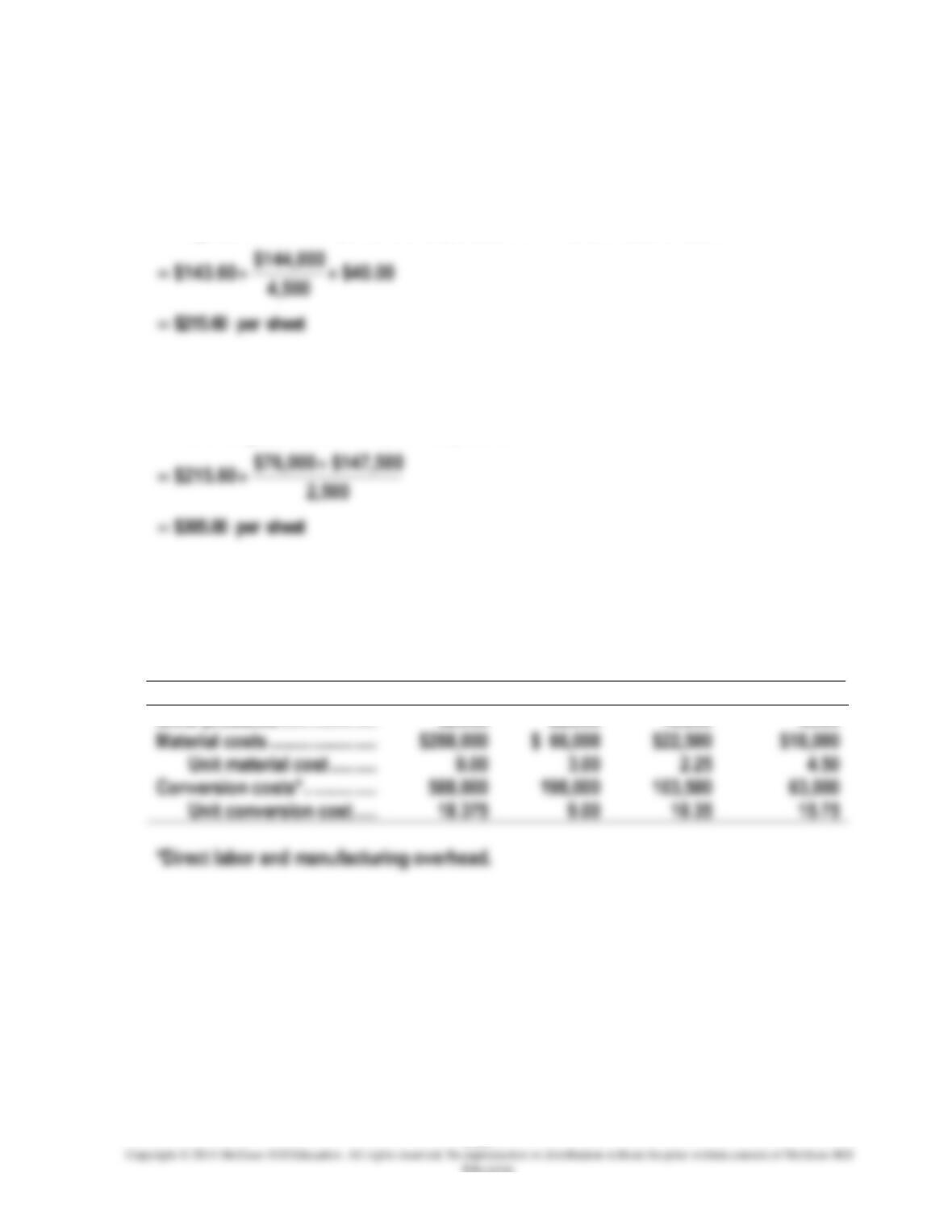

Extrusion

Form

Trim

Finish

Units produced …………………

32,000

22,000

10,000

4,000

Material costs …………………..

$288,000

Unit material cost ……….

Conversion costs* …………….

Unit conversion cost …..

18.375

15.75

*Direct labor and manufacturing overhead.

4-37

PROBLEM 4-37 (CONTINUED)

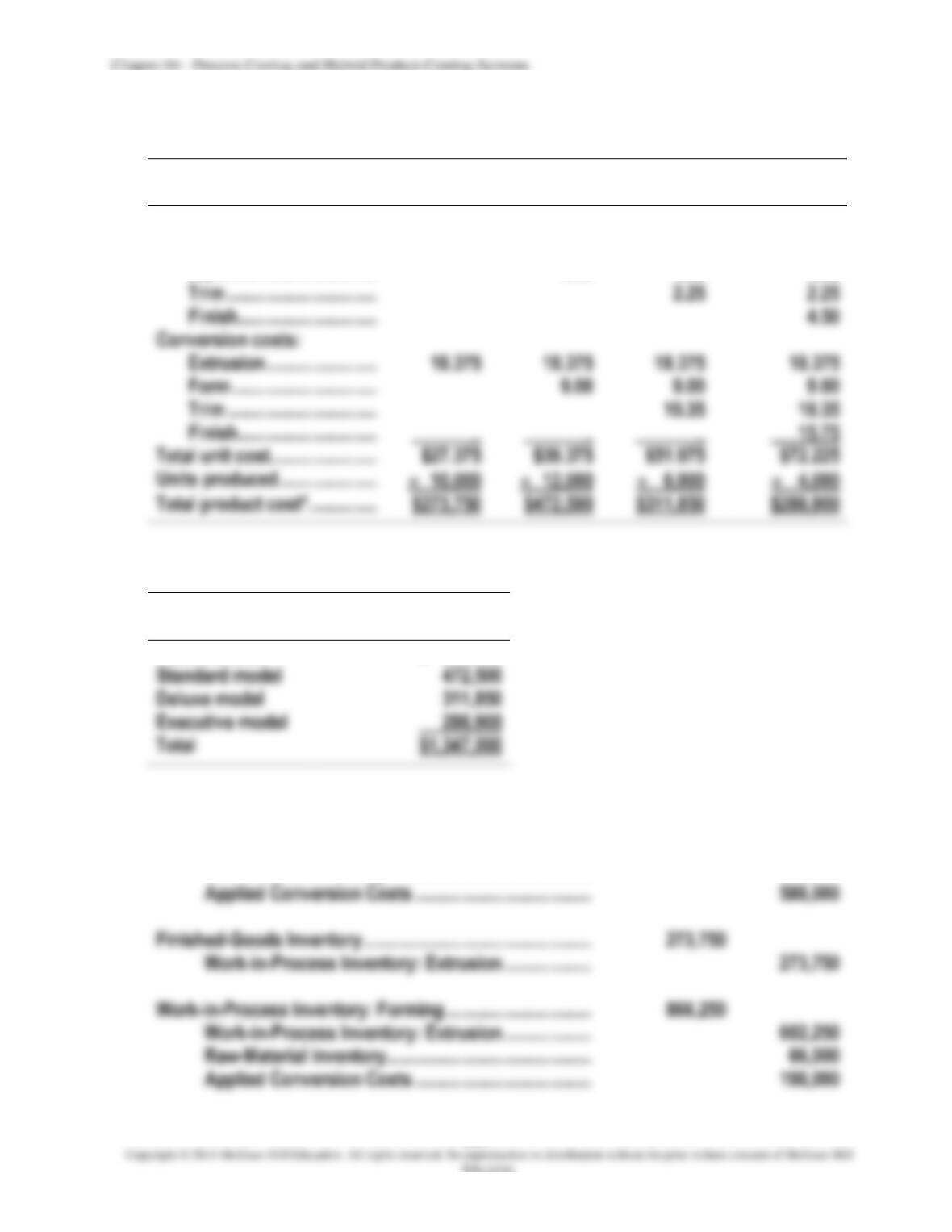

Unit Costs

Plastic

Sheets

Standard

Model

Deluxe

Model

Executive

Model

Material costs:

Extrusion ……………………

$9.00

$9.00

$9.00

$9.00

Form ………………………….

3.00

3.00

3.00

Trim …………………………..

2.25

2.25

Finish …………………………

4.50

Conversion costs:

Extrusion ……………………

Form ………………………….

9.00

9.00

9.00

Trim …………………………..

Finish …………………………

$39.375

$51.975

*Total costs accounted for:

Product

Total

Product Costs

Plastic sheets

$ 273,750

Standard model

Deluxe model

Executive model

288,900

2.

Journal entries:

Work-in-Process Inventory: Extrusion ………………………..

876,000

Raw-Material Inventory ……………………………………..

288,000

Applied Conversion Costs ………………………………..

588,000

Finished-Goods Inventory ………………………………………….

273,750

Work-in-Process Inventory: Extrusion ……………….

273,750

Work-in-Process Inventory: Forming ………………………….

866,250

Work-in-Process Inventory: Extrusion ……………….

602,250

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

PROBLEM 4-37 (CONTINUED)

Finished-Goods Inventory ………………………………………….

472,500

Work-in-Process Inventory: Forming …………………

472,500

519,750

Work-in-Process Inventory: Forming …………………

393,750

Raw-Material Inventory ……………………………………..

Applied Conversion Costs ………………………………..

103,500

Finished-Goods Inventory ………………………………………….

311,850

Work-in-Process Inventory: Trimming ……………….

311,850

288,900

Work-in-Process Inventory: Trimming ……………….

207,900

Raw-Material Inventory ……………………………………..

Applied Conversion Costs ………………………………..

Finished-Goods Inventory ………………………………………….

288,900

Work-in-Process Inventory: Finishing ……………….

288,900

4-39

PROBLEM 4-38 (45 MINUTES)

1.

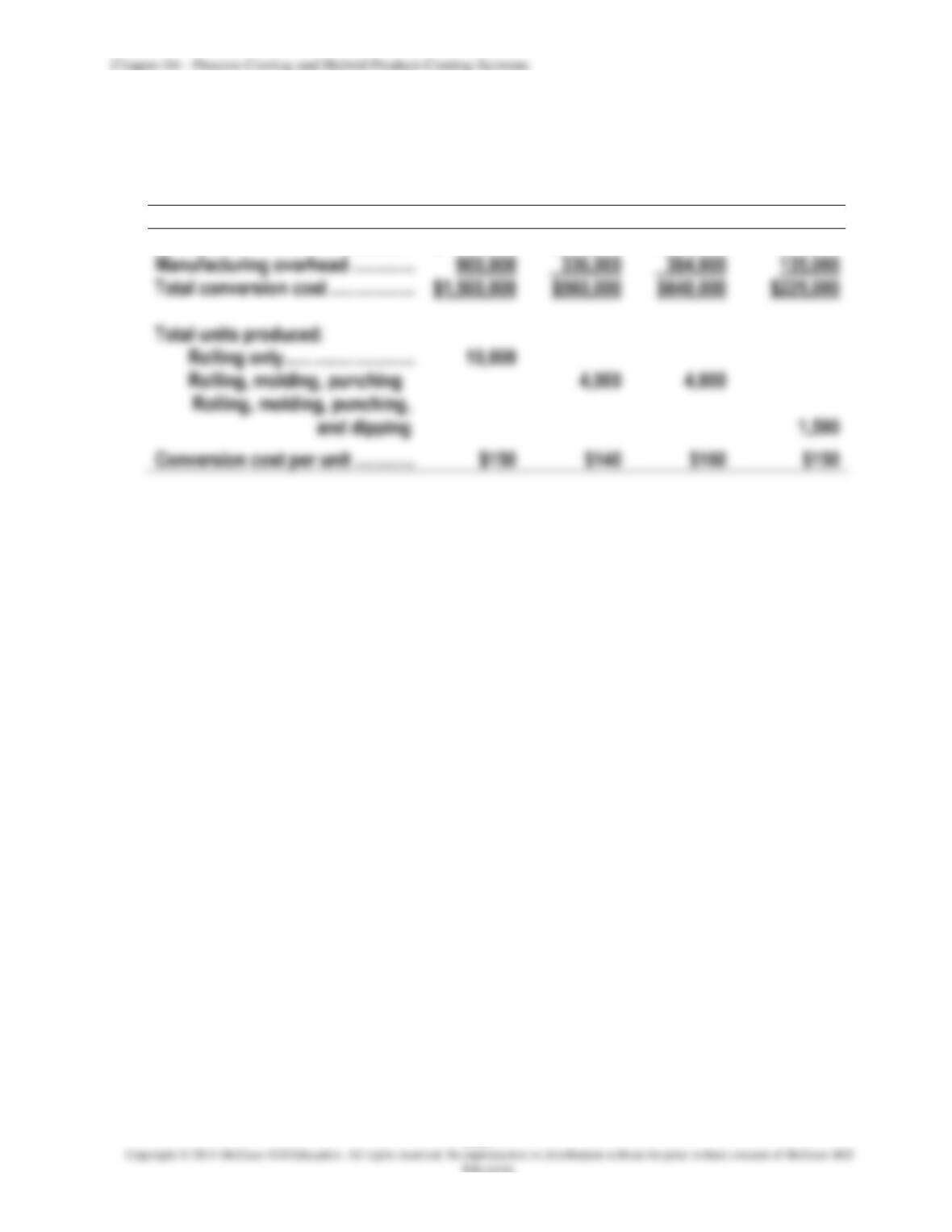

Conversion costs:

Rolling

Molding

Punching

Dipping

Direct labor …………………………….

$ 600,000

$224,000

$256,000

$ 90,000

Manufacturing overhead …………..

Total conversion cost ………………

$1,500,000

$560,000

$640,000

Total units produced:

Rolling only ……………………….

Rolling, molding, punching

Conversion cost per unit ………….

4-40

PROBLEM 4-38 (CONTINUED)

2.

Product costs:

Ceralam

Sheets

Non

Sold

after

reflective

Ceralam

Relective

Ceralam

Total

Rolling

Housings

Housings

Costs

Direct material:

Ceralam sheets ………………..

$ 960,000

$ 400,000

$ 240,000

$1,600,000

Chemical dip …………………..

Conversion costs:

Rolling …………………………..

Molding …………………………..

Punching …………………………

Dipping …………………………..

Total cost ………………………………

Units manufactured ………………..

Unit cost ………………………………..

3.

Journal entries:

3,100,000

Raw-Material Inventory …………………………………………………

Applied Conversion Costs …………………………………………….

*$1,600,000 = direct-material cost for ceralam sheets

4-41

PROBLEM 4-38 (CONTINUED)

Finished-Goods Inventory ………………………………………………………

1,860,000*

Work-in-Process Inventory: Rolling …………………………..

1,860,000

*$1,860,000 = 6,000 ceralam sheets sold after

Cost of Goods Sold ……………………………………………………….

1,860,000*

Finished-Goods Inventory …………………………………………….

1,860,000

1,240,000*

Work-in-Process Inventory: Rolling …………………………..

1,240,000

= $3,100,000 – $1,860,000

Applied Conversion Costs …………………………………………….

1,800,000*

Work-in-Process Inventory: Molding…………………………..

1,800,000

= $1,240,000 + $560,000

Applied Conversion Costs …………………………………………….

*$640,000 = conversion cost in punching operation

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-42

PROBLEM 4-38 (CONTINUED)

Finished-Goods Inventory ………………………………………………………

1,525,000*

Work-in-Process Inventory: Punching …………………………..

1,525,000

Cost of Goods Sold ……………………………………………………….

1,525,000*

Finished-Goods Inventory …………………………………………….

1,525,000

Work-in-Process Inventory: Punching …………………………..

= $1,800,000 + $640,000 – $1,525,000

Raw-Material Inventory ………………………………………………….

Applied Conversion Costs …………………………………………….

*$60,000 = direct-material cost for chemical dip

Finished-Goods Inventory ………………………………………………………

1,200,000*

Work-in-Process Inventory: Dipping …………………………..

1,200,000

Finished-Goods Inventory …………………………………………….

1,200,000

4. In the electronic version of the solutions manual, press the CTRL key and click on

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-43

SOLUTION TO CASE

CASE 4-39 (45 MINUTES)

1.

Equivalent units of material …………………………………………………………………………

8,500

Equivalent units of conversion …………………………..………………………………………..

8,260

2.

Cost per equivalent unit of material ……………………………………………………….

$6.00

Cost per equivalent unit of conversion ……………………………………………………….

$7.00

3.

October 31 work-in-process inventory ……………………………………………………….

Cost of goods completed and transferred out ………………………………………………

$105,300

4.

Weighted-average unit cost of completed leather belts …………………………..

These answers are supported by the following process-costing schedules. The firm’s cost

CALCULATION OF EQUIVALENT UNITS: LYCOMING LEATHER CO. – HARRISBURG PLANT

Weighted-Average Method

Physical

Units

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, October 1 …………

500

30%

Units started during October ……….

8,000

Total units to account for …………….

8,500

Work in process, October 31 ……….

400

40%

Total units accounted for …………….

8,500

Chapter 04 – Process Costing and Hybrid Product-Costing Systems

4-44

CASE 4-39 (CONTINUED)

CALCULATION OF COSTS PER EQUIVALENT UNIT: HARRISBURG PLANT

Weighted-Average Method

Direct

Material

Conversion

Total

Work in process, October 1 …………………………

$ 2,000

$ 2,500

$ 4,500

Costs incurred during October …………………….

Total costs to account for …………………………...

$51,000

$57,820

$108,820

Equivalent units ………………………………………….

8,500

Costs per equivalent unit …………………………….

$6.00

ANALYSIS OF TOTAL COSTS: HARRISBURG PLANT

Weighted-Average Method

Cost of goods completed and transferred out during October:

Cost remaining in October 31 work-in-process inventory:

Direct material:

percost

of number

Conversion:

Total cost of October 31 work in process ………………………………………..

percost

of number

4-45

CASE 4-39 (CONTINUED)

Check: Cost of goods completed and transferred out ……

Cost of October 31 work-in-process inventory …..

Total costs accounted for …………………………………

5.

right-hand column of the equivalent-units part of the table in the solution to

If the units were 50 percent complete as of October 31, there would be 8,300

equivalent units with respect to conversion. (To see this, just change the 160 in the

As controller, Jeff Daley has an ethical obligation to refuse his friend’s

request to alter the estimate of the percentage of completion. What Daley can do is

to help Murray think of some legitimate ways to bring about real cost reductions.

Several ethical standards for management accountants (listed in Chapter 1) apply

in this situation. Among the relevant standards are the following:

Competence: