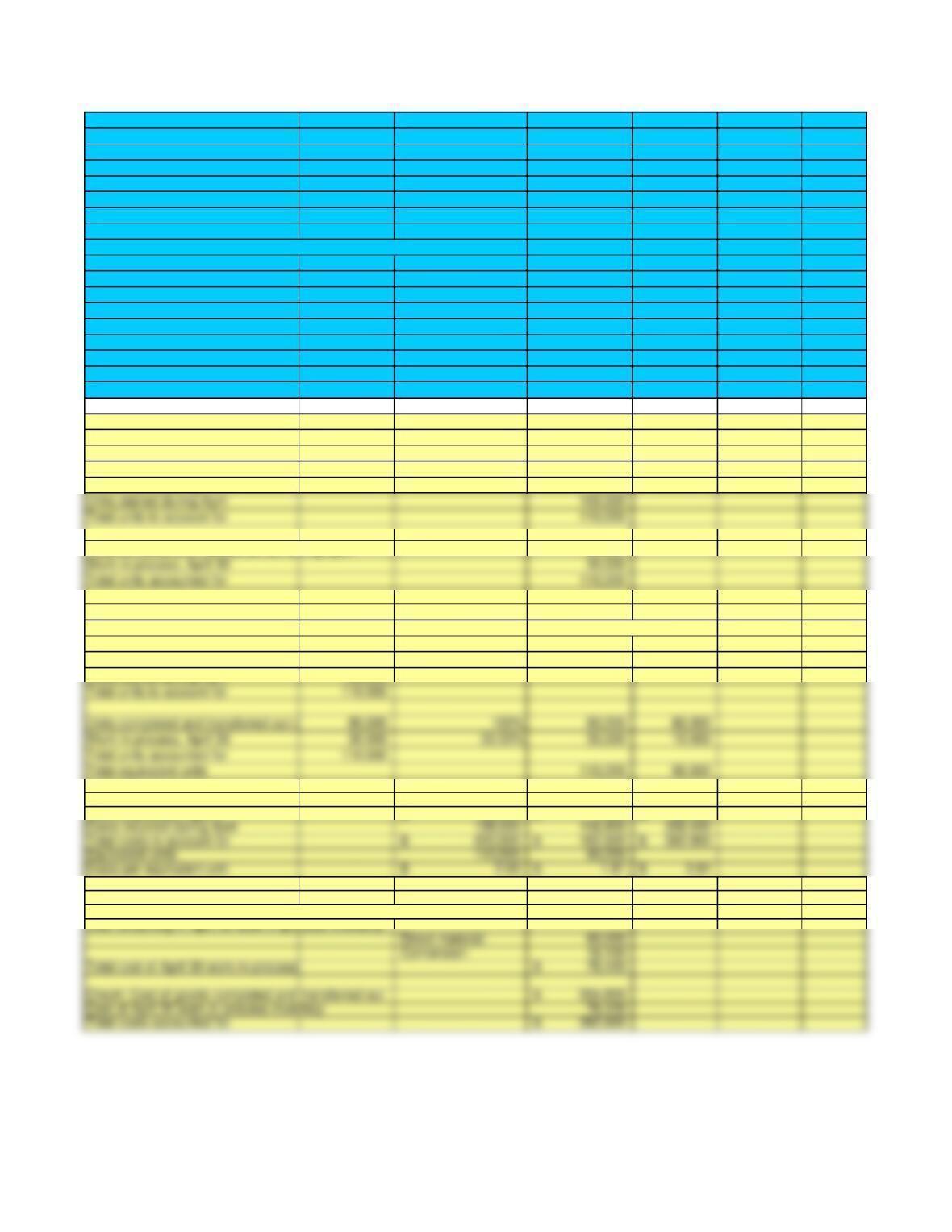

DATA INPUT

Moravia Company

Work in process, April 1 – 10,000 units:

Direct material: 100% complete, cost of 22,000$

Conversion: 20% complete, cost of 4,500

Balance in work in process, April 1 26,500$

Units started during April 100,000

Units completed during April and transferred to finished-goods inventory 80,000

Work in process, April 30:

Direct material: 100% complete

Conversion: 33.33% complete

Costs incurred during April:

Direct material 198,000$

Conversion costs:

Direct labor 52,800$

Applied manufacturing overhead 105,600

Total conversion costs 158,400$

SOLUTION

1. Physical flow of units

Physical Units

Work in process, April 1 10,000

Units complete and transferred out during April 80,000

2. Calculation of equivalent units

Percentage

Physical Units of Completion Direct Material Conversion

Units completed and transferred out during April

Work in process, April 1 10,000 20%

Units started during April 100,000

3. Computation of unit costs Direct Material Conversion Total

Work in process, April 1 22,000$ 4,500$ 26,500$

Costs incurred during April 198,000 158,400 356,400

Equivalent units 110,000 90,000

Costs per equivalent unit 2.00$ 1.81$ 3.81$

4. Analysis of total costs

Costs of goods completed and transferred out during April: 304,800$

Total cost of April 30 work-in-process 78,100$

Check: Cost of goods completed and transferred out 304,800$

Cost of April 30 work-in-process inventory 78,100

Equivalent Units