CHAPTER 4

UNDERSTANDING THE ISSUES

1. The intercompany sale will cause both

sales and costs of goods sold to be over-

stated by $50,000 on the consolidated in-

2. Debit Sales and credit Cost of Goods Sold

for $50,000. Debit Cost of Goods Sold and

credit Inventory for $3,000 (1/4 × $12,000).

3. 2015 2016

NCI $ 0 $ 200 ($1,000 × 20%)

Controlling

4. Company S has realized a $50,000 profit;

however, it is not immediate. The profit will

be realized over the 5-year life of the asset.

5. 2015 2016 2017

Realized gain by

reducing depre-

6. a. Company S is better off borrowing the

funds from Company P since it will re-

ceive a lower interest rate (9.5% in-

est expense and interest revenue are

eliminated during the consolidation

process. Only the $40,000 ($500,000 ×

8%) of external interest expense re-

mains on the consolidated statements.

c. Intercompany interest expense and

interest revenue should not appear on

Ch. 4—Exercises 4–2

EXERCISES

EXERCISE 4-1

Pattern Company and Subsidiary Sorel Company

Consolidated Income Statement

For the Year Ended December 31, 2015

Sales ($250,000 + $500,000 – $120,000) …………………………………………………. $630,000

Cost of goods sold [$150,000 + $310,000 – $120,000 + (40% × $30,000)] …… 352,000

Gross profit ………………………………………………………………………………………….. $278,000

Sorel Income Distribution Schedule

Unrealized profit in ending Internally generated income ………. $55,000

inventory (40% × $30,000) …… $12,000

Pattern Income Distribution Schedule

Internally generated income ………. $ 70,000

80% × Sorel adjusted

Pattern Company and Subsidiary Sorel Company

Consolidated Income Statement

For the Year Ended December 31, 2016

Sales ($350,000 + $540,000 – $150,000) …………………………………………………. $740,000

Cost of goods sold [$210,000 + $360,000 – $150,000 – (40% × $30,000)

+ (40% × $25,000)] ………………………………………………………………………….. 418,000

Gross profit ………………………………………………………………………………………….. $322,000

4–3 Ch. 4—Exercises

Exercise 4-1, Concluded

Sorel Income Distribution Schedule

Unrealized profit in ending Internally generated net

inventory (40% × $25,000) …… $10,000 income ………………………………. $74,000

Realized profit in beginning

Pattern Income Distribution Schedule

Internally generated net

income ………………………………. $ 55,000

EXERCISE 4-2

(1) Gross profit recorded on the separate books:

Gross profit—Hide:

Sales ………………………………………………………………………… $400,000

(2) Consolidated gross profit:

Sales ………………………………………………………………………… $416,000

Cost of goods sold to consolidated group* ……………………… 256,000

4–5 Ch. 4—Exercises

EXERCISE 4-3

Source of income components:

Consolidated

Income

Victory Norco Eliminations Statement

Sales ………………………………………………. (220,000) (150,000) (IS) 90,000 (280,000)

Cost of goods sold ……………………………. 150,000 112,500 (IS) (90,000)

(BI) (5,000)

Eliminations and Adjustments:

(IS) Elimination of $90,000 intercompany sales.

(BI) Elimination of 25% profit from beginning inventory; debit would be to Retained Earnings;

allocated 80% to the controlling interest and 20% to the NCI.

(EI) Elimination of 25% profit from ending inventory; credit would be to inventory account.

Subsidiary Norco Company Income Distribution

Unrealized ending inventory Internally generated net

profit …………………………….. (EI) $7,500 income …………………………… $22,500

Realized beginning inventory

profit ………………………………. (BI) 5,000

+

Parent Victory Corporation Income Distribution

Internally generated net

income ………………………………. $35,000

EXERCISE 4-4

(1) In the year of sale, eliminate the $15,000 gain on the sale of the machine, and adjust the

machine to its net book value on the date of the sale. Reduce depreciation expense and

accumulated depreciation by $3,000 to reflect depreciation based on the consolidated book

(2) Gain on Sale of Machinery ………………………………………………. 15,000

Machinery ………………………………………………………………… 15,000

(3) Retained Earnings—Jungle Company ………………………………. 12,000

Accumulated Depreciation ……………………………………………….. 3,000

4–7 Ch. 4—Exercises

EXERCISE 4-5

(1) Gain on Sale of Land ………………………………………………………. 50,000

Gain on Building …………………………………………………………….. 150,000

(2) Retained Earnings—Sayner* ……………………………………………. 38,500

Retained Earnings—Wavemasters** …………………………………. 154,000

Accumulated Depreciation ($150,000 ÷ 20 years)……………….. 7,500

Building ……………………………………………………………………. 150,000

EXERCISE 4-6

In 2016, only a $4,000 loss can be recognized for the sale of the machinery on the consolidated

income statement. This is the amount of the impairment (FV – BV). The remaining $5,000 loss

must be deferred. This loss is deferred in the year of the intercompany sale. During each follow-

ing year of use, the asset and accumulated depreciation accounts are adjusted to reflect the

$10,000 fair value, with an additional entry for the $1,000 of incremental depreciation.

On December 31, 2016, $5,000 of the $9,000 recorded loss should be eliminated.

Machine………………………………………………………………………….. 5,000

Loss on Sale of Machine ……………………………………………… 5,000

4–9 Ch. 4—Exercises

EXERCISE 4-7

Consolidated

Income

Danner Link Eliminations Statement

Sales ………………………………………………. (650,000) (280,000) (F1) 60,000 (870,000)

Cost of goods sold ……………………………. 400,000 190,000 (F1) (40,000) 550,000

Eliminations and Adjustments:

(F1) Eliminate the gain on the intercompany machine sale. The machine account is credited

for the $20,000 gain.

(F2a) Reduce machine depreciation expense to reflect depreciation based on the consolidated

book value of the asset ($20,000 profit ÷ 5 years = $4,000 per year). The debit is to Ac-

cumulated Depreciation.

Subsidiary Link Company Income Distribution

Unrealized gain on sale Internally generated net

of machine………………….. (F1) $20,000 income ………………………… $20,000

Realized gain through use

of machine …………………… (F2a) 4,000

Parent Danner Company Income Distribution

Internally generated net

income ………………………….. $90,000

Gain realized on use of building

EXERCISE 4-8

2015

Subsidiary Sandbar Company Income Distribution

Unrealized profit in ending Internally generated net

inventory (40% × $15,000) …… $6,000 income ………………………………. $250,000

Parent Peninsula Company Income Distribution

Gain on sale of real Internally generated net

estate ……………………………….. $200,000 income ………………………………. $520,000

Realized gain on use of

sold real estate

2016

Subsidiary Sandbar Company Income Distribution

Unrealized profit in ending Internally generated net

inventory (40% × $20,000) …… $8,000 income ………………………………. $235,000

Realized profit in beginning

inventory ……………………………. 6,000

Parent Peninsula Company Income Distribution

Internally generated net

income ………………………………. $340,000

EXERCISE 4-9

(1) Saratoga Windsor

Notes Receivable……….. 50,000 Cash …………………………….. 50,000

Cash ……………………… 50,000 Notes Payable ……………. 50,000

Accrued Interest Interest Expense ……………. 2,000

Receivable ……………… 2,000* Accrued Interest

(2) Eliminations:

(LN1) Notes Payable ………………………………………………………. 50,000

Accrued Interest Payable ……………………………………….. 2,000

Notes Receivable ………………………………………………. 50,000

Accrued Interest Receivable ……………………………….. 2,000

EXERCISE 4-10

(1) Saratoga

May 1 Notes Receivable ……………………………………………………….. 50,000

Cash ……………………………………………………………………… 50,000

To record receipt of note.

July 1 Accrued Interest Receivable ………………………………………… 500

Interest Revenue …………………………………………………….. 500

Windsor

May 1 Cash …………………………………………………………………………. 50,000

Notes Payable ………………………………………………………… 50,000

Computation of Proceeds

Principal of note ……………………………………………………………… $50,000

Interest due at maturity (6% × $50,000) …………………………….. 3,000

(2) Eliminations:

(LN1) Notes Receivable Discounted …………………………………. 50,000

Notes Receivable ………………………………………………. 50,000

To eliminate intercompany note and reclassify

4–13 Ch. 4—Problems

PROBLEMS

PROBLEM 4-1

Plato Corporation and Subsidiary Solo Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2015

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Plato Solo Dr. Cr. Statement Earnings Sheet

Cash ………………………………………………. 735,000 370,000 …………….. …………….. ………..…… …………….. 1,105,000

Accounts Payable ……………………………. (35,000) (100,000) (IA) 30,000 …………….. …………….. .……………. (105,000)

Common Stock ($10 par)—Plato ……….. (1,000,000) …………….. …………….. …………….. ………..…… …………….. (1,000,000)

Paid-In Capital in Excess of Par—Plato . (1,500,000) …………….. …………….. …………….. ………..…… …………….. (1,500,000)

Retained Earnings—Plato …………………. (5,500,000) …………….. …………….. …………….. …..………… (5,500,000) ……………..

Common Stock ($10 par)—Solo ………… …………….. (400,000) (EL) 400,000 …………….. …………….. .……………. ……………..

Paid-In Capital in Excess of Par—Solo .. …………….. (200,000) (EL) 200,000 …………….. …………….. .……………. ……………..

Problem 4-1, Concluded

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Fair value of subsidiary ………………… $3,300,000 $3,300,000 N/A

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amorti-

Adjustment Key Periods zation

Equipment ………………………………….. $ 300,000 debit D 10 $30,000

Eliminations and Adjustments:

(CY1) Eliminate the entry recording the parent’s share (100%) of the subsidiary’s net income.

(EL) Eliminate the subsidiary’s equity balances.

(D) Distribute excess to equipment.

PROBLEM 4-2

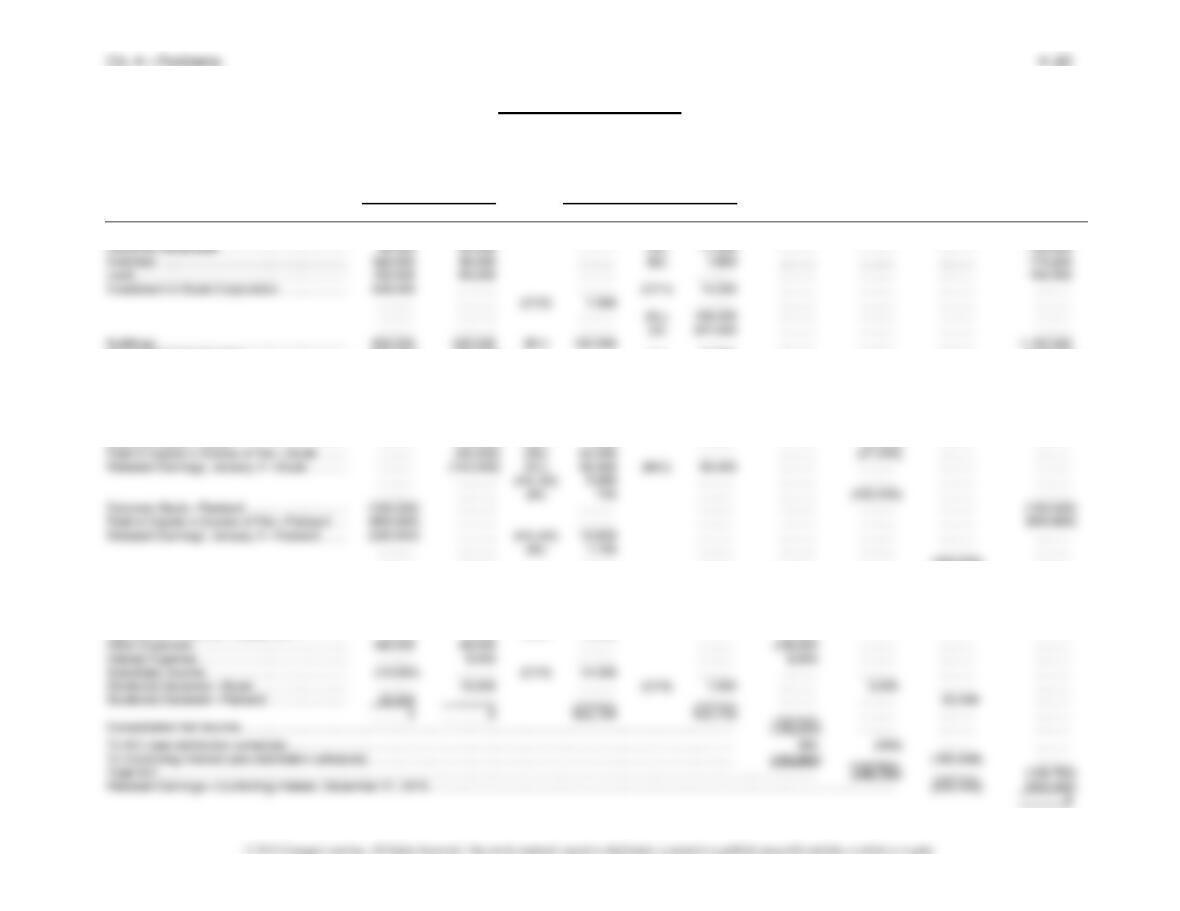

(1) Benton Corporation and Subsidiary Crandel Company

Worksheet for Consolidated Financial Statements

For Year Ended March 31, 2017

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Benton Crandel Dr. Cr. Statement NCI Earnings Sheet

Cash …………………………………………………… 191,200 44,300 …………… …………… …………… …………… ………….. 235,500

Accumulated Depreciation …………………….. (940,000) (210,000) …………… …………… …………… …………… ………….. (1,150,000)

Goodwill ……………………………………………… 60,000 ……………. (D) 162,500 …………… …..………. …………… ………….. 222,500

Accounts Payable ………………………………… (242,200) (106,300) (IAP) 10,000 …………… …………… …………… ………….. ……………

…………… ……………. (IAS) 5,000 …………… …………… …………… ………….. (333,500)

Bonds Payable …………………………………….. (400,000) ……………. …………… …………… …………… …………… ………….. (400,000)

Common Stock—Benton ………………………. (250,000) ……………. …………… …………… ……….….. …………… ………….. (250,000)

Sales ………………………………………………….. (880,000) (630,000) (ISP) 32,000 …………… …….…….. …………… ………….. ……………

…………… ……………. (ISS) 30,000 …………… (1,448,000) …………… ………….. ……….…..

Dividend Income (from Crandel Company) . (24,000) ……………. (CY2) 24,000 …………… …………… …………… ………….. ………..….

Cost of Goods Sold ………………………………. 704,000 504,000 (EIP) 1,200 (BIP) 1,800 …………… ……….….. ………….. ……………

…………… ……………. (EIS) 750 (ISP) 32,000 …………… …………… ………….. …………...

Problem 4-2, Continued

Eliminations and Adjustments:

(CV) Convert to equity method:

Change in equity × 80% = $40,000 × 80% = $32,000.

(CY2) Eliminate intercompany dividends.

Benton, $4,000 × 25% = $1,000.

(ISS) Eliminate sales from Crandel to Benton.

(EIS) Eliminate intercompany profit from ending inventory on sales from Crandel to

Benton, $3,000 × 25% = $750.

(IAS) Eliminate intercompany trade balances on sales from Crandel to Benton.

Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ……………………………………. $562,500 $450,000 $112,500

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………….. $562,500 $450,000 $112,500

Less book value of interest acquired:

Total equity ……………………….. 400,000 $400,000 $400,000

Adjustment of identifiable accounts:

Worksheet

Adjustment Key

Problem 4-2, Concluded

Subsidiary Crandel Company Income Distribution

Unrealized profit in ending Internally generated net

inventory ……………………… (EIS) $750 income …………………………… $45,000

Realized profit in beginning

inventory ………………………… (BIS) 1,000

Parent Benton Corporation Income Distribution

Unrealized profit in ending Internally generated net

inventory ……………………… (EIP) $1,200 income …………………………… $46,000

Realized profit in beginning

(2) Benton Corporation and Subsidiary Crandel Company

Consolidated Income Statement

For Year Ended March 31, 2017

Sales …………………………………………………………………………….. $1,448,000

Cost of goods sold ………………………………………………………….. 1,145,150

Gross profit ……………………………………………………………………. $ 302,850

PROBLEM 4-3

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (70%) (30%)

Company fair value ……………………………………. $550,000 $400,000 $150,000*

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (70%) (30%)

Price paid for investment ……….. $550,000 $400,000 $150,000

Less book value of interest acquired:

Common stock ………………….. $ 10,000

Adjustment of identifiable accounts:

Worksheet Amorti-

Adjustment Key Periods zation

Buildings ……………………………… $150,000 debit D1 20 $ 7,500

Equipment……………………………. 60,000 debit D2 5 12,000

Problem 4-3, Continued

Amortization Schedule

Account adjustments Annual Current Prior

to be amortized Life Amount Year Years Total Key

Buildings 20 $ 7,500 $ 7,500 $ 7,500 $15,000 A1

Subsidiary Stude Corporation Income Distribution

Unrealized profit in ending Internally generated net

inventory ………………………… $ 1,800 income …………………………… $20,000

Amortizations ……………………….. 19,500 Realized profit in beginning

inventory ………………………… 2,500

Parent Packard Corporation Income Distribution

Internally generated net

income ……………………………. $165,000

Problem 4-3, Continued

(2) Packard Corporation and Subsidiary Stude Corporation

Consolidated Income Statement

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Packard Stude Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 66,000 132,000 ……….. ……….. ……….. ……….. ……….. 198,000

Accumulated Depreciation ………………………… (220,000) (65,000) ……….. (A1) 15,000 ……….. ……….. ……….. (300,000)

Equipment ………………………………………………. 150,000 72,000 (D2) 60,000 ……….. ……….. ……….. ……….. 282,000

Accumulated Depreciation ………………………… (90,000) (46,000) ……….. (A2) 24,000 ……….. ……….. ……….. (160,000)

Goodwill …………………………………………………. ……….. ………… (D3) 128,000 ……….. .………. ……….. ……….. 128,000

Accounts Payable ……………………………………. (60,000) (102,000) (IA) 11,000 ……….. ……….. ….……. ……….. (151,000)

Bonds Payable ………………………………………… ……….. (100,000) ……….. ……….. ……..… ……….. ……….. (100,000)

Common Stock—Stude ……………………………. ……….. (10,000) (EL) 7,000 ……….. ……….. (3,000) ……….. ………..

……….. ………… ……….. ……….. ……….. ……….. (309,600) ………..

Sales ……………………………………………………… (800,000) (350,000) (IS) 40,000 ……….. (1,110,000) ……….. ……….. ………..

Cost of Goods Sold ………………………………….. 450,000 208,500 ……….. (IS) 40,000 ……….. …….…. ……….. ………..

……….. ………… (EI) 1,800 (BI) 2,500 617,800 ……….. ……….. ………..

Depreciation Expense—Buildings ………………. 30,000 7,500 (A1) 7,500 ……….. 45,000 ……….. ……….. ………..

Depreciation Expense—Equipment ……………. 15,000 8,000 (A2) 12,000 ……….. 35,000 ……….. ……….. ..………