Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

4-18 Intermediate Accounting, 8/e

CHANGE IN ACCOUNTING ESTIMATE

► A change in accounting estimate is reflected in the financial

EARNINGS PER SHARE

➢ Earnings per share (EPS) is the amount of income reported

expressed on a per share basis.

➢ In its simplest form, EPS is computed by dividing income

T4-13

4-20 Intermediate Accounting, 8/e

EARNINGS PER SHARE

(continued)

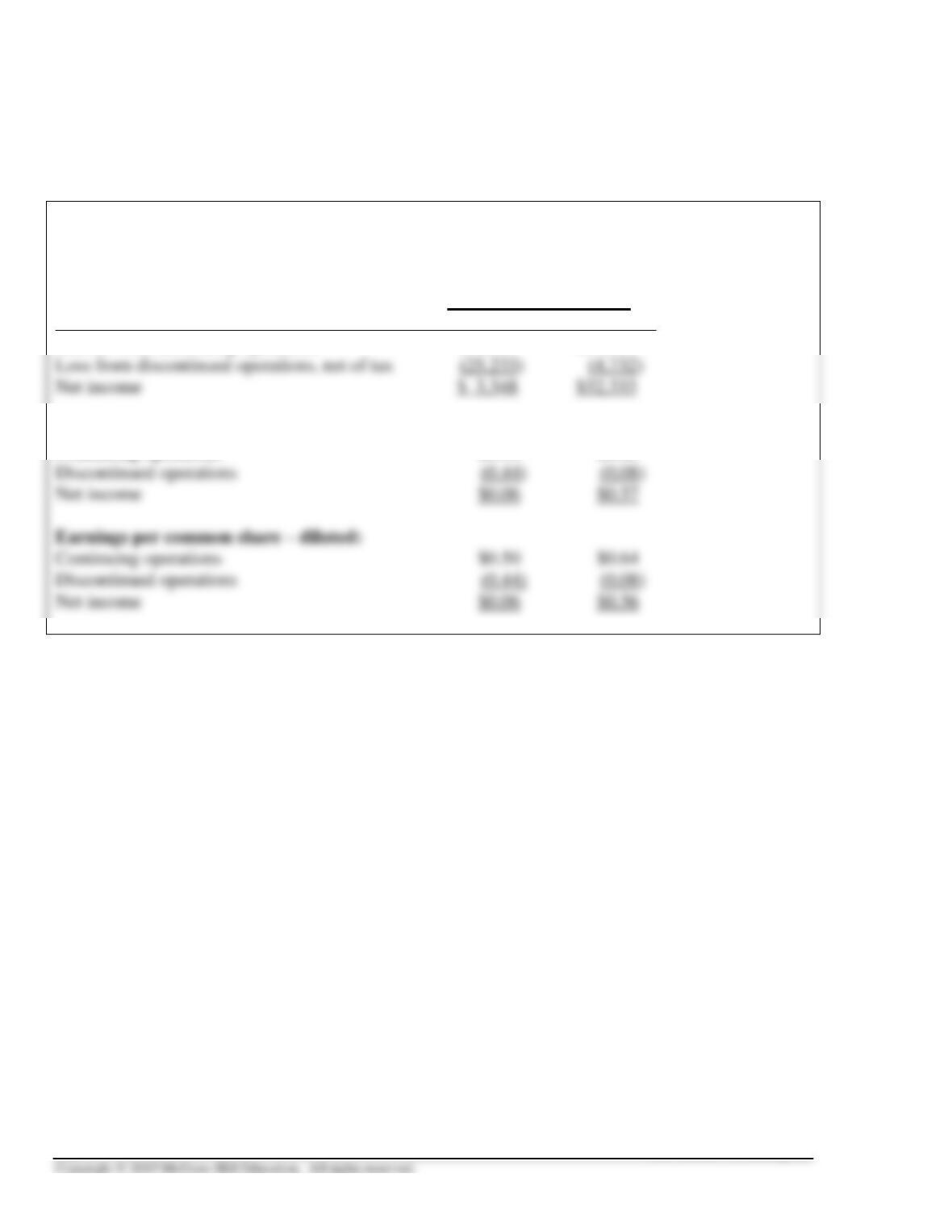

BIG LOTS, INC.

Consolidated Statements of Operations (in part)

Thirteen Weeks Ended

(In thousands, except per share amounts) May 3, 2014 May 4, 2013

Income from continuing operations $28,581 $37,065

Earnings per common share – basic:

Continuing operations $0.50 $0.65

Illustration 4-10

T4-13 (continued)

COMPREHENSIVE INCOME

► Comprehensive income is the total nonowner change in equity

for a period.

($ in millions)

Net income $xxx

Other comprehensive income:

Net unrealized holding gains (losses) from investments (net of tax)* $xx

Gains (losses) from and amendments to postretirement

* Changes in the market value of certain investments (described in Chapter 12).

† Gains and losses due to revising assumptions or market returns differing from

expectations and prior service cost from amending the plan (described in

Chapter 17).

Illustration 4-11

➢ The information in the income statement and other

comprehensive income items can be presented either (1) in a

T4-14

4-22 Intermediate Accounting, 8/e

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Comprehensive Income. Both U.S. GAAP and IFRS allow companies to

report comprehensive income in either a single statement of comprehensive

income or in two separate statements.

Other comprehensive income items are similar under the two sets of

STATEMENT OF CASH FLOWS

► OPERATING ACTIVITIES

➢ Inflows and outflows of cash that result from activities

► INVESTING ACTIVITIES

➢ Inflows and outflows of cash related to the acquisition

and disposition of long-term assets (such as property,

► FINANCING ACTIVITIES

➢ Cash inflows and outflows from transactions with

creditors (excluding trade creditors) and owners.

T4-16

4-24 Intermediate Accounting, 8/e

CASH FLOWS FROM OPERATIONS ACTIVITIES

➢ Under the direct method, the cash effect of each operating

T 4-17

CASH FLOWS FROM OPERATIONS ACTIVITIES

(continued)

Arlington Lawn Care (ALC) began operations at the beginning of 2016. ALC’s 2016 income

statement and its year-end balance sheet are shown below ($ in thousands).

ARLINGTON LAWN CARE

Income Statement

For the Year Ended December 31, 2016

Service revenue $90

Operating expenses:

* Includes $6 in insurance expense.

ARLINGTON LAWN CARE

Balance Sheet

At December 31, 2016

Assets Liabilities and shareholders’ equity

Current assets: Current liabilities:

Illustration 4-14

T4-17 (continued)

4-26 Intermediate Accounting, 8/e

CASH FLOWS FROM OPERATIONS ACTIVITIES

(continued)

ARLINGTON LAWN CARE

Statement of Cash Flows

For the Year Ended December 31, 2016

($ in thousands)

Cash Flows from Operating Activities

* Service revenue of $90 thousand, less increase of $12 thousand in accounts

receivable.

Illustration 4-14A

ARLINGTON LAWN CARE

Statement of Cash Flows

For the Year Ended December 31, 2016

($ in thousands)

Cash Flows from Operating Activities

Net income $35

Adjustments for noncash effects:

Illustration 4-14B

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Classification of Cash Flows. Like U.S. GAAP, international standards also require a statement of

cash flows. Consistent with U.S. GAAP, cash flows are classified as operating, investing, or

financing. However, the U.S. standard designates cash outflows for interest payments and cash

Typical Classification of Cash Flows from Interest and Dividends

U.S. GAAP IFRS

Operating Activities Operating Activities

Dividends received

Siemens AG, a German company, prepares its financial statements according to IFRS. In its statement

of cash flows for the first three months of the 2014 fiscal year, the company reported interest and

dividends received as operating cash flows, as would a U.S. company. However, Siemens classified

interest paid as a financing cash flow.

Siemens AG

Statement of Cash Flows (partial)

For the First Three Months of Fiscal 2014

(€ in millions)

Cash flows from financing activities:

Transactions with owners (6)

T 4-18

4-28 Intermediate Accounting, 8/e

Suggestions for Class Activities

1. Research Activity

Layne Christensen Company, a leading construction and exploration company, reported

discontinued operations in its income statements for its 2014, 2013, and 2012 fiscal years.

Suggestions:

Have the class access the company’s financial statements for the fiscal year ended January 31,

Points to note:

Layne Christensen completed the sale of its Solmete X operation on July 31, 2013. A gain on sale

2. PetSmart Analysis

Have students, individually or in groups, go to the most recent PetSmart annual report using

EDGAR which can be located at: www.sec.gov. Ask them to:

1. Compare revenues, operating expenses, net income, and net income as a percentage of revenue

dollars with those in the 2014 annual report in Appendix B of the text. Are there any

The following are suggested assignments from the end-of-chapter material that will help your

students develop their communication, research, analysis and judgment skills.

Communication Skills. Integrating Case 4-12 can be adapted to ask students to answer the

Research Skills. In their careers, our graduates will be required to locate and extract relevant

information from available resource material to determine the correct accounting practice,

Analysis Skills. The “Broaden Your Perspective” section includes Analysis Cases that direct

Judgment Skills. The “Broaden Your Perspective” section includes Judgment Cases that require

4-30 Intermediate Accounting, 8/e

Assignment Chart

Learning Est. time

Questions Objective(s) Topic (min.)

4-1

1

Purpose of the income statement

5

4-2

1

Income from continuing operations

5

4-3

1

Operating and nonoperating income

5

4-4

1

Single-step and multiple-step income statements

5

4-13

6

Comprehensive income

5

4-14

7

Purpose of the statement of cash flows

5

4-15

8

Classification of cash flows

5

Brief Learning Est. time

Exercises Objective(s) Topic (min.)

4-1

1

Single-step income statement

10

4-2

1,3

Multiple-step income statement

10

4-3

1,3

Multiple-step income statement

15

4-4

1,3

Multiple-step income statement

15

4-32 Intermediate Accounting, 8/e

Learning Est. time

Exercises Objective(s) Topic (min.)

4-1

1

Operating versus nonoperating income

10

4-2

1,5

Income statement format; single-step and

multiple-step

20

4-3

1,3,5

Income statement format; single-step and

multiple-step

20

4-10

5

Earnings per share

10

4-11

6

Comprehensive income

20

4-12

8

Statement of cash flows; classifications

10

4-13

8

Statement of cash flows preparation

15

4-14

8,9

IFRS; statement of cash flows

5

4-15

8

Indirect method; reconciliation of net income to

cash flows

15

4-24

1 through 4,

5 through 8

Concepts; terminology

15

4-25

A

Interim reporting [Based on Appendix]

10

CPA/CMA Learning Est. time

Exam Questions Objective(s) Topic (min.)

CPA-1

4

Discontinued operations

3

CPA-2

3,4

Income from continuing operations

3

CMA-2

3

Multiple-step income statement

3

Learning Est. time

Problems Objective(s) Topic (min.)

4-1

1,3,4,5

Comparative income statements; multiple-step

format

25

4-2

4

Discontinued operations

25

4-3

4

Income statement presentation

20

4-4

3,4

Income statement presentation; unusual items

10

Star Problems

Learning Est. time

Cases Objective(s) Topic (min.)

Judgment Case 4-1

2,3

Earnings quality

15

Judgment Case 4-2

3

Restructuring costs

15

comprehensive income

Judgment Case 4-10

2

Management incentives for change

15

Research Case 4-11

3

Pro forma earnings

60

Integrating Case 4-12

3

Balance sheet and income statement

35