E–29

CHAPTER 4

True-False Questions

4–2

must have been, an employer-employee relationship.

4–2

they are not defined as employers under the federal income tax

withholding law.

4–2

excludes partners.

4–2

subtracting from the employee’s gross wages any local and state taxes.

4–3

withheld from the value of meals that employers furnish workers on the

employers’ premises for the employers’ convenience.

4–3

nontaxable income and thus are excluded from federal income tax

withholding.

4–4

added to the employees’ taxable pay on the last payday of the year.

4–5

month are treated as remuneration subject to federal income tax

withholding.

4–5

must report the amount of the cash tips to the employer by the 10th of

the month following the month they receive the tips.

4–5

employee is made from the employee’s wages that are under the

employer’s control.

4–5

reported by tipped employees and the tips that the employer allocates to

the employees.

4–6

from federal income tax withholdings.

4–6

from federal income tax withholding.

4–9

employee’s SIMPLE retirement account.

E–30 Chapter 4/Examination Questions

4–9

extra $10,000 of their wages from federal income tax.

4–9

specified amount of their compensation without paying federal income

taxes on that amount.

4–9

contributions of up to $12,500.

4–9

match the employee’s contribution, dollar-for-dollar, up to 3% of the

employee’s compensation.

4–10

allowances. Evers must claim the three allowances with each of the

two employers during the entire calendar year.

4–11

social security card and place it in the employee’s employment file.

4–11

the employer must withhold according to the withholding tables for

single employees.

4–10

employees who do not itemize deductions on their income tax returns.

4–12

amended Form W-4 on or before May 31.

4–12

the number of allowances claimed. Hunt’s employer must put the new

withholding allowance certificate into effect before the next weekly

payday on August 3.

4–12

increasing the number of withholding allowances claimed.

4–13

not replace it with a valid form. The employer should withhold federal

income taxes at the rate for a single person claiming no exemptions.

4–13

the IRS if the employee has claimed 15 or more withholding allowances.

4–14

withheld from the annuity amounts the person receives.

4–15

method distinguishes unmarried persons from married persons.

4–15

method or the percentage method is used.

Examination Questions/Chapter 4 E–31

4–19

wages, the method of calculating the withholding is the same for

vacation payments as for semiannual bonuses.

4–22

does not use the OASDI/HI tax rates in the formula.

4–23

the close of the calendar year.

4–26

transmitting information returns on Forms W-2.

4–31

filing rather than paper Forms W-2.

4–32

deductions as nontaxable.

Multiple-Choice Questions

4–2

not defined as an employee?

a. Partner who draws compensation for services rendered the

partnership

b. General manager, age 66

c. Payroll clerk hired one week ago

d. Governor of the state of Florida

e. Secretary employed by a not-for-profit corporation

4–3

taxable income subject to federal income tax withholding?

a. Flight on employer-provided airline

b. Personal use of company car

c. Sick pay

d. Employer-paid membership to a country club

e. All of the above are taxable.

4–5

withhold federal income taxes?

a. Advances made to sales personnel for traveling expenses

b. Tipped employee’s monthly tips of $120

c. Deceased person’s wages paid to the estate

d. Minister of Presbyterian church

e. All of the above

E–32 Chapter 4/Examination Questions

4–5

of federal income taxes and social security taxes on tips?

a. Tips amounting to $10 or more in a calendar month must be re-

ported by tipped employees to their employers.

b. The withholding of federal income taxes on employees’ reported

tip income is made from the amount of tips reported by

employees.

c. When employees report taxable tips in connection with employment

in which they also receive regular wages, the amount of tax to be

withheld on the tips is computed as if the tips were a supplemental

wage payment.

d. Employers do not withhold FICA taxes on the tipped employees’

reported tip income.

e. None of the above statements is correct.

4–6

withholding of federal income taxes except:

a. a year-end bonus.

b. kitchen appliances given by manufacturer in lieu of cash wages.

c. dismissal payment.

d. vacation pay.

e. payments made under worker’s compensation law.

4–7

a. Health insurance

b. Group-term life insurance (first $50,000 of coverage)

c. Dependent care assistance (first $5,000)

d. Self-insured medical reimbursement plan

e. Educational assistance

4–10

a. amounted to $2,000 in 2018.

b. may be claimed to exempt a portion of the employee’s earnings

from withholding.

c. is indexed for inflation every calendar quarter.

d. may be claimed at the same time with each employer for whom an

employee is working during the year.

e. for one person is a different amount for a single versus a married

taxpayer.

Examination Questions/Chapter 4 E–33

4–11

to you, the payroll manager, when she was hired. You should:

a. tell Beech that it is OK since you know that she was recently

divorced and is reluctant to talk about it.

b. inform Beech that she will have to write the IRS and give her

reasons for refusing to state her marital status.

c. tell Beech that you will have to withhold income taxes as if she

were married and had claimed one allowance.

d. tell Beech that you will have to withhold income taxes according to

the withholding table for a single employee with no allowances.

e. advise Beech to write “It is no business of yours.” in the margin of

her Form W-4.

4–12

he claims two additional withholding allowances. He asks you to

refund the excess taxes that were deducted from January 1 to March 9

when Arch claimed only one withholding allowance. You should:

a. repay the overwithheld taxes on Arch’s next payday.

b. tell Arch that you will spread out a refund of the overwithheld taxes

equally over the next six pays.

c. inform Arch that you are unable to repay the overwithheld taxes

that were withheld before March 9 and that the adjustment will

have to be made when he files his annual income tax return.

d. tell Arch to write the IRS immediately and ask for a refund of the

overwithheld taxes.

e. inform Arch that you will appoint a committee to study his request.

4–13

requires that an employer submit to the agency a copy of each Form W-4:

a. the IRS has requested in writing.

b. on which an employee, usually earning $180 each week at the

time Form W-4 was filed, now claims to be exempt from

withholding.

c. on which an employee claims to be single but has 9 withholding

allowances.

d. on which a married employee claims no withholding allowances.

e. on which a recently divorced employee claims 5 withholding

allowances and authorizes an additional $10 to be withheld each

week.

E–34 Chapter 4/Examination Questions

4–30

distributions from pension and retirement plans?

a. Form W-2c

b. Form 1099-R

c. Form 1099-PEN

d. Form W-3p

e. Form W-4

4–30

conditions except:

a. to report $1,000 of compensation paid to an individual who is not

an employee.

b. to report the wages totaling $600 paid to an independent contractor

during the calendar year.

c. to report dividends totaling $600 paid to an individual during the

calendar year.

d. to report commissions of $500 paid to a self-employed salesman.

e. An information return must be filed under each of the above

conditions.

4–30

landlords?

a. Form 1099–R

b. Form 1099–INT

c. Form 1099–MISC

d. Form 1099–G

e. Form 8027

4–31

to independent contractors in which of the following cases?

a. When there is a signed contract between the parties

b. When the contractor is paid $400

c. When the contractor is a corporation

d. When the contractor has not provided a taxpayer identification

number and the contract is $600 or more

e. All of the above

Examination Questions/Chapter 4 E–35

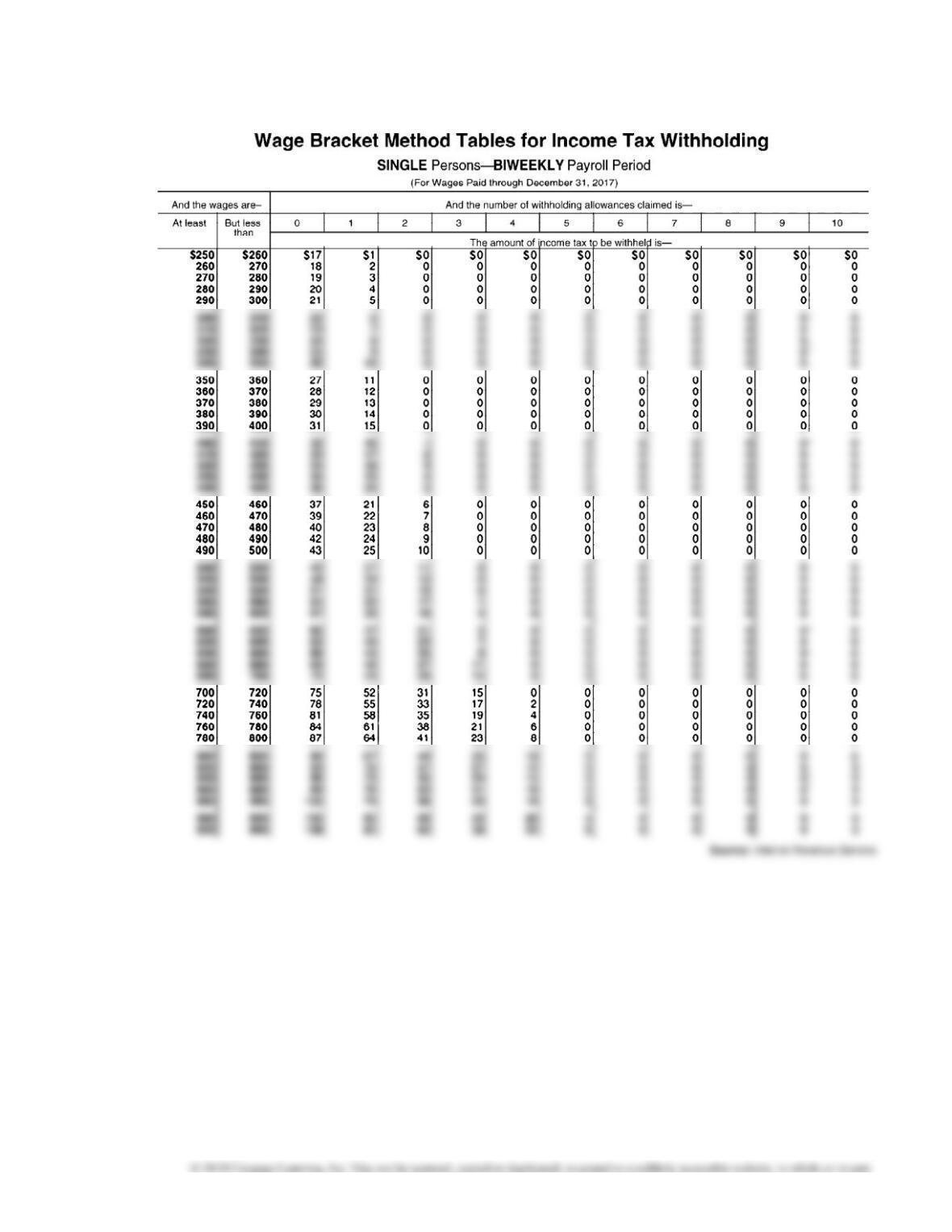

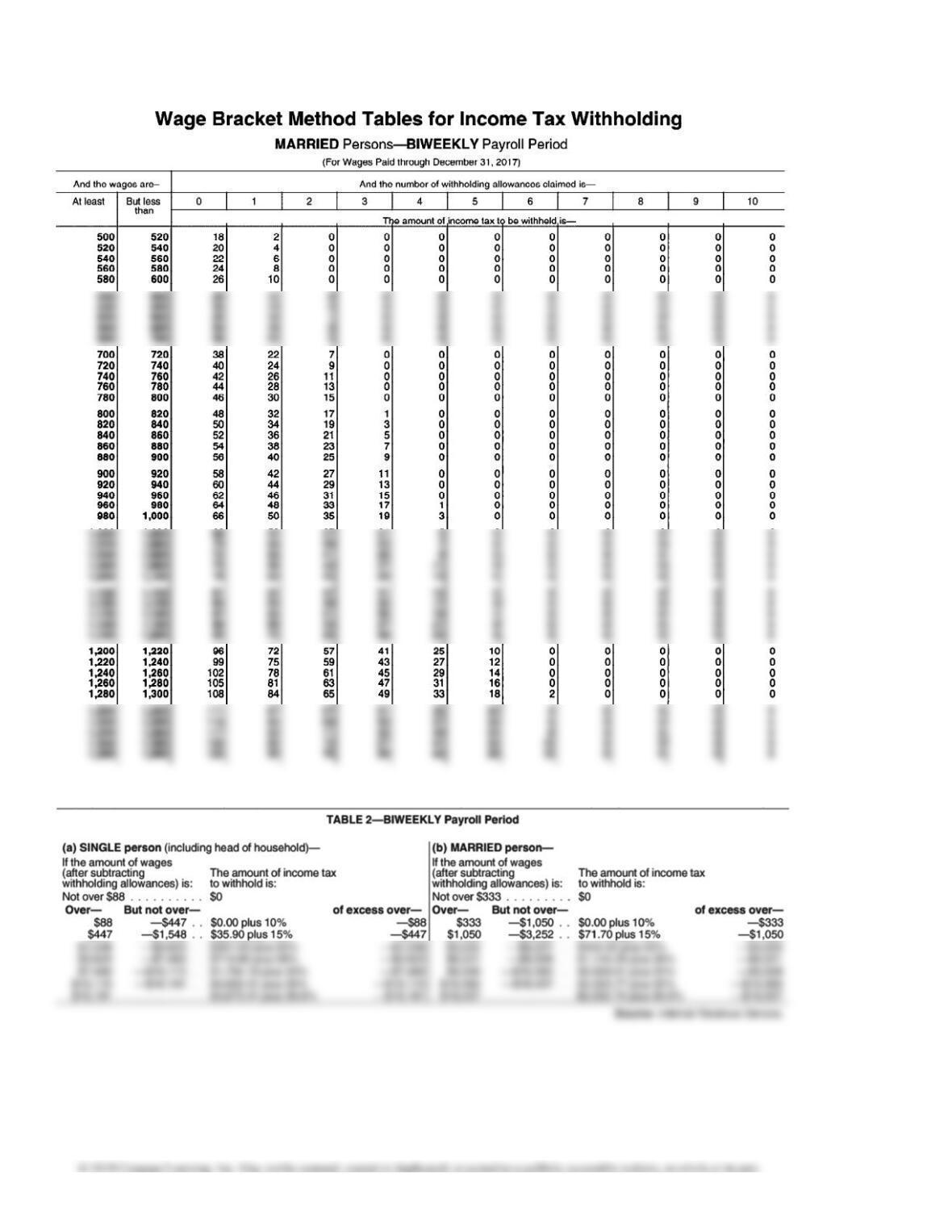

Problem-Solving

Note: Use the tables on the following pages to calculate the answers to the problems

listed.

1. Determine the income tax to withhold from the biweekly wages of the following

employees (wage-bracket):

2. Edward Dorsey is a part-time employee, and during the biweekly pay period he

earned $395. In addition, he is being paid a bonus of $300 along with his regular

pay. If Dorsey is single and claims two withholding allowances, how much would be

deducted from his pay for FIT? (There are two ways to determine his deduction—

do not use table for percentage method.)

3. Mary Matthews made $950 in a biweekly pay period. Only social security (fully

4. Carson Smart is paid $1,200 every two weeks plus a taxable lodging allowance

5. Calculate the amount to withhold from the following employees using the

biweekly table of the percentage method.

E–36 Chapter 4/Examination Questions

6. Use the appropriate table to determine the amount to withhold for federal income

tax from each of the following biweekly wages (biweekly withholding allowance

= $155.80):

Examination Questions/Chapter 4 E–37

E–38 Chapter 4/Examination Questions