275

Problem 4-6BA (Concluded)

Part 4

Instructor note: Entries are shown without an account reference column because no posting is required.

2018

Jan. 4 Salaries Expense …………………………………… 1,200

Cash ………………………………………………. 1,200

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

276

SERIAL PROBLEM – SP 4

Serial Problem, Business Solutions (20 minutes) — Part 1

<Note: The general ledger is displayed at the end of Part 2>

Closing entries

2017

Dec. 31 Computer Services Revenue …………………….. 403 31,284

Income Summary ……………………………….. 901 31,284

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

277

Serial Problem, SP 4 (Continued)

Part 2

BUSINESS SOLUTIONS

Post-Closing Trial Balance

December 31, 2017

Debit Credit

Cash ………………………………………………………………………. $ 48,372

Accounts receivable ………………………………………………. 5,668

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

278

Serial Problem, SP 4 (Continued)

[Instructor Note: Ledger includes all entries from prior three months. The Working

Papers shorten the solution by showing account balances as of December 31.]

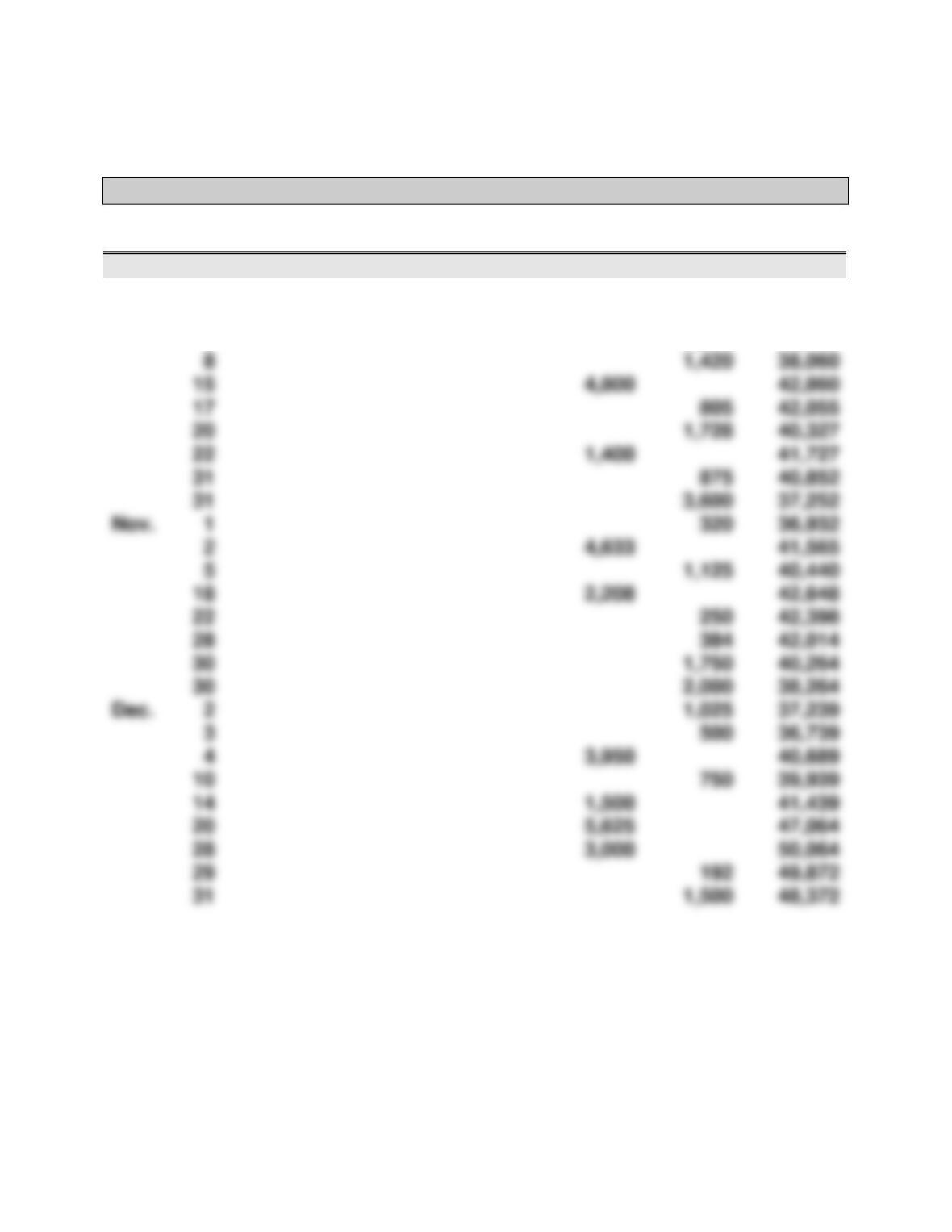

General Ledger

Cash

Acct. No. 101

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

45,000

45,000

2

3,300

41,700

5

2,220

39,480

8

1,420

38,060

42,860

42,055

1,728

40,327

41,727

40,852

3,600

37,252

Nov.

1

36,932

2

41,565

5

1,125

40,440

42,648

42,398

1,750

40,264

2,000

38,264

Dec.

2

1,025

37,239

3

36,739

4

40,689

39,939

41,439

47,064

50,064

49,872

1,500

48,372

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

279

Serial Problem, SP 4 (Continued)

Accounts Receivable

Acct. No. 106

Date

Explanation

PR

Debit

Credit

Balance

Oct.

6

4,800

4,800

Computer Supplies

Acct. No. 126

Date

Explanation

PR

Debit

Credit

Balance

Oct.

3

1,420

1,420

Nov.

5

1,125

2,545

Dec.

1,100

3,645

3,065

Date

Explanation

PR

Debit

Credit

Balance

Oct.

5

2,220

2,220

Dec.

1,665

Date

Explanation

PR

Debit

Credit

Balance

Oct.

2

3,300

3,300

Dec.

2,475

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

8,000

8,000

Date

Explanation

PR

Debit

Credit

Balance

Dec.

1,400

6,200

4,800

1,400

1,400

5,208

5,208

Nov.

8

5,668

2,208

8,668

3,950

3,000

5,668

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

280

Serial Problem, SP 4 (Continued)

Computer Equipment

Acct. No. 167

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

20,000

20,000

Accumulated Depreciation—Computer Equipment

Acct. No. 168

Date

Explanation

PR

Debit

Credit

Balance

Dec.

Date

Explanation

PR

Debit

Credit

Balance

Oct.

Dec.

Date

Explanation

PR

Debit

Credit

Balance

Dec.

Date

Explanation

PR

Debit

Credit

Balance

Dec.

Acct. No. 301

Date

Explanation

PR

Debit

Credit

Balance

Oct.

Dec.

Closing

Closing

Date

Explanation

PR

Debit

Credit

Balance

Nov.

Dec.

Closing

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

281

Serial Problem, SP 4 (Continued)

Computer Services Revenue

Acct. No. 403

Date

Explanation

PR

Debit

Credit

Balance

Oct.

6

4,800

4,800

Depreciation Expense—Office Equipment

Acct. No. 612

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

400

400

31

Closing

Acct. No. 613

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

1,250

31

Closing

1,250

Wages Expense

Acct. No. 623

Date

Explanation

PR

Debit

Credit

Balance

Oct.

31

875

875

Nov.

30

1,750

2,625

Dec.

10

750

31

500

31

Closing

3,875

Acct. No. 637

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

555

555

31

Closing

Acct. No. 640

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

2,475

31

Closing

2,475

12

1,400

6,200

28

5,208

Nov.

2

4,633

8

5,668

24

3,950

Dec.

20

5,625

31

Closing

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

282

Serial Problem, SP 4 (Concluded)

Computer Supplies Expense

Acct. No. 652

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

3,065

3,065

31

Closing

3,065

Acct. No. 655

Date

Explanation

PR

Debit

Credit

Balance

20

1,728

1,728

Dec.

1,025

2,753

31

Closing

2,753

Acct. No. 676

Date

Explanation

PR

Debit

Credit

Balance

Nov.

28

Dec.

29

31

Closing

Acct. No. 677

Date

Explanation

PR

Debit

Credit

Balance

Nov.

22

Dec.

31

Closing

Acct. No. 684

Date

Explanation

PR

Debit

Credit

Balance

17

Dec.

1,305

31

Closing

1,305

Acct. No. 901

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

Closing

31

Closing

31

Closing

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

283

Reporting in Action — BTN 4-1

1. The revenue items from its income statement must be identified, and

those would be credited to Income Summary as step 1 in the closing

2. The total expenses that would be debited to Income Summary as step 2

in the closing entry process must be computed. Apple’s total expenses

3. The balance of Income Summary before it is closed as of its fiscal year–

end September 26, 2015, equals the net income for Apple of $53,394 (in

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

Comparative Analysis — BTN 4-2

1. Apple’s current ratios: ($ in millions)

2. In both years, Google has the higher current ratio (4.67 vs 1.11 for the

current year; 4.69 vs. 1.08 in the prior year), suggesting a better ability

4. Google’s current ratio is above (better than) the industry average for

both years, and Apple’s is below (worse than) the industry average for

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

Ethics Challenge — BTN 4-3

1. There are several courses of action that Tamira could have taken. Two

possibilities follow:

a. She could have consulted with the president and told him that

finalized financial statements would not be ready by the time of the

2. Students may offer one of the above alternatives or another response

they may think of, given the situation. Try to generate a discussion of

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

286

Communicating in Practice — BTN 4-4

TO: _____________________

FROM: _____________________

DATE: ______________________

SUBJECT: CLARIFICATIONS—OBJECTIVE OF THE CLOSING PROCESS

[Following is a sample of what the memorandum’s contents might include.]

When we speak of “closing the books” or the closing process we are not

talking about ending or closing the business nor doing anything that reflects

this thinking in the financial statements. Let me use an analogy to explain the

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

287

Taking It to the Net — BTN 4-5

1. The Motley Fool states that a benchmark of 1.5 is generally regarded as

Teamwork in Action — BTN 4-6

[Note: Each team member will be working on a different component of the solution and will

ultimately combine information and verify the final check figures using the accounting equation.]

1. Accounts and adjusted balances to be extended to Balance Sheet columns

Trial Balance

Adjustments

Balance Sheet

Account Title

Debit

Credit

Debit

Credit

Debit

Credit

Cash …………………………..

$16,000

$16,000

(d) 800

(a) 2,200

$ 7,000

(b) 4,000

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

288

Teamwork in Action (Continued)

2. Adjusted revenue account balance

Trial Balance

Adjustments

Income

Statement

Title

Debit

Credit

Debit

Credit

Debit

Credit

Investigation Fees

Closing entry

Account Titles and Explanation

Debit

Credit

Investigation Fees Earned ……………………………………………

33,800

Income Summary ………………………………………….

33,800

3. Adjusted balances of expense accounts

Title

Trial Balance

Adjustments

Income

Statement

Debit

Credit

Debit

Credit

Debit

Credit

Rent Expense ………………..

15,000

15,000

Insurance Expense ………..

(a) 2,200

Depreciation Expense ……

(b) 4,000

Supplies Expense ………….

(c) 7,000

Closing entry

Account Titles and Explanation

Debit

Credit

Income Summary ……………………………………………………….

28,200

Rent Expense ………………………………………………..

15,000

Insurance Expense ………………………………………..

Depreciation Expense ……………………………………

Supplies Expense ………………………………………….

33,000

33,800

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

Teamwork in Action (Concluded)

4.

D. Noseworthy, Capital

Income Summary

(4)

6,000

34,000

(2)

28,200

33,800

(1)

(3)

33,600

Third and Fourth closing entries

Account Titles and Explanation

Debit

Credit

Income Summary ……………………………………………………….

5,600

D. Noseworthy, Capital ………………………………….

5,600

D. Noseworthy, Capital ………………………………………………..

6,000

D. Noseworthy, Withdrawals ………………………….

6,000

5. Proving the Accounting Equation

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 4

Entrepreneurial Decision — BTN 4-7

1. A classified balance sheet classifies liabilities into current and non–

current. The current liabilities are those that are due in the short-term,

2. To better understand the company’s operations, the entrepreneur must

make sure that all revenues earned in a particular accounting period are

3. Closing procedures will accomplish two objectives for the owner. First,

Hitting the Road — BTN 4-8

There is no formal solution to this field activity. The instructor may wish to

Global Decision — BTN 4-9

1. Current ratio (in millions KRW)

2. Analysis: Samsung’s current ratio improved (is better) for the current