99

CHAPTER 4

ACCOUNTING FOR MERCHANDISING BUSINESSES

CLASS DISCUSSION QUESTIONS

1. Merchandising businesses acquire mer-

chandise for resale to customers. It is the

selling of merchandise, instead of a service,

that makes the activities of a merchandising

business different from the activities of a

service business.

3. a. Increase c. Decrease

b. Increase d. Decrease

4. Under the periodic method, the inventory

records do not show the amount available

for sale or the amount sold during the peri-

od. In contrast, under the perpetual method

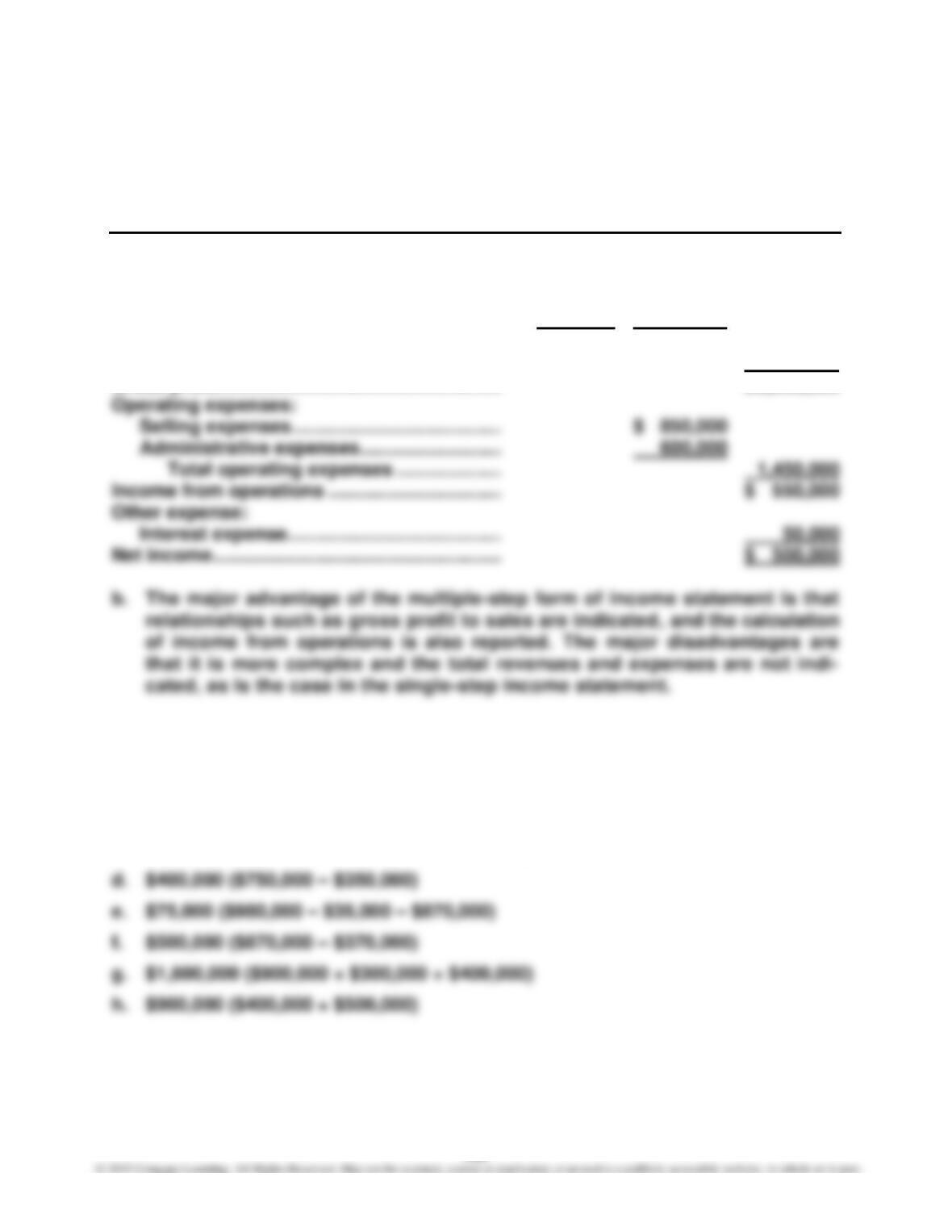

5. The multiple-step form of income statement

contains conventional groupings for reve-

nues and expenses, with intermediate bal-

ances, before concluding with the net in-

come balance. In the single-step form, the

total of all expenses is deducted from the to-

tal of all revenues, without intermediate bal-

ances.

7. Revenues from sources other than the prin-

cipal activity of the business are classified

as other income. Examples of other income

include income from interest, rent, and gains

resulting from the sale of fixed assets.

8. Sales to customers who use bank credit

invoice due within 30 days of date of in-

voice.

b. Payment due within 90 days of date of

invoice.

c. Payment due by the end of the month in

which the sale was made.

b. A debit memorandum issued by the buyer

of merchandise indicates the amount for

which the seller’s account is to be de-

creased (decrease Accounts Payable)

and the reason for the purchases return

or allowance.

11. a. The buyer

b. The seller

12. Since the buyer is paying for the destination

100

EXERCISES

E4–1

a. $1,200,000 ($3,750,000 – $2,550,000)

E4–2

$47,860 million ($69,865 million – $22,005 million)

E4–3

a. Purchases discounts, purchases returns and allowances

E4–4

a. Cost of merchandise sold:

Merchandise inventory, May 1, 20Y1 …….. $ 175,000

Purchases …………………………………………… $1,400,000

Less: Purchases returns and

allowances ……………………………… $20,000

Purchases discounts …………………. 18,000 38,000

b. $940,000 ($2,250,000 – $1,310,000)

E4–5

1. The schedule should begin with the June 1, 20Y8, not the May 31, 20Y9, mer-

chandise inventory.

2. Purchases returns and allowances and purchases discounts should be de-

ducted from (not added to) purchases.

A correct cost of merchandise sold section is as follows:

Cost of merchandise sold:

Merchandise inventory, June 1, 20Y8 …… $ 125,000

Purchases …………………………………………… $875,000

Less: Purchases returns and allowances .. $12,000

E4–6

a. Net sales: $11,810,000 ($12,140,000 – $250,000 – $80,000)

b. Gross profit: $4,810,000 ($11,810,000 – $7,000,000)

E4–7

a. Selling expense, (1), (2), (7), (8)

102

E4–8

ECO-WINDOWS COMPANY

Income Statement

For the Year Ended June 30, 20Y6

Revenues:

Net sales ……………………………………………………………. $9,300,000

Rent revenue ……………………………………………………… 200,000

Total revenues ………………………………………………… $9,500,000

103

E4–9

a.

QUALITY INTERIORS COMPANY

Income Statement

For the Year Ended October 31, 20Y5

Revenue from sales:

Sales ………………………………………………….. $5,000,000

Less: Sales returns and allowances …….. $ 100,000

Sales discounts …………………………. 400,000 500,000

Net sales ………………………………………… $ 4,500,000

Cost of merchandise sold ………………………… 2,500,000

Gross profit ……………………………………………… $ 2,000,000

E4–10

a. $40,000 ($360,000 – $30,000 – $290,000)

b. $175,000 ($290,000 – $115,000)

c. $750,000 ($1,200,000 – $250,000 – $200,000)

104

E4–11

1. Sales returns and allowances and sales discounts should be deducted from

(not added to) sales.

2. Sales returns and allowances and sales discounts should be deducted from

sales to yield “net sales” (not gross sales).

3. Deducting the cost of merchandise sold from net sales yields gross profit.

CARLSBAD COMPANY

Income Statement

For the Year Ended February 28, 20Y9

Revenue from sales:

Sales ………………………………………………….. $4,400,000

Less: Sales returns and allowances …….. $120,000

Sales discounts …………………………. 60,000 180,000

Net sales ………………………………………… $4,220,000

Cost of merchandise sold ………………………… 2,650,000

Gross profit ……………………………………………… $1,570,000

105

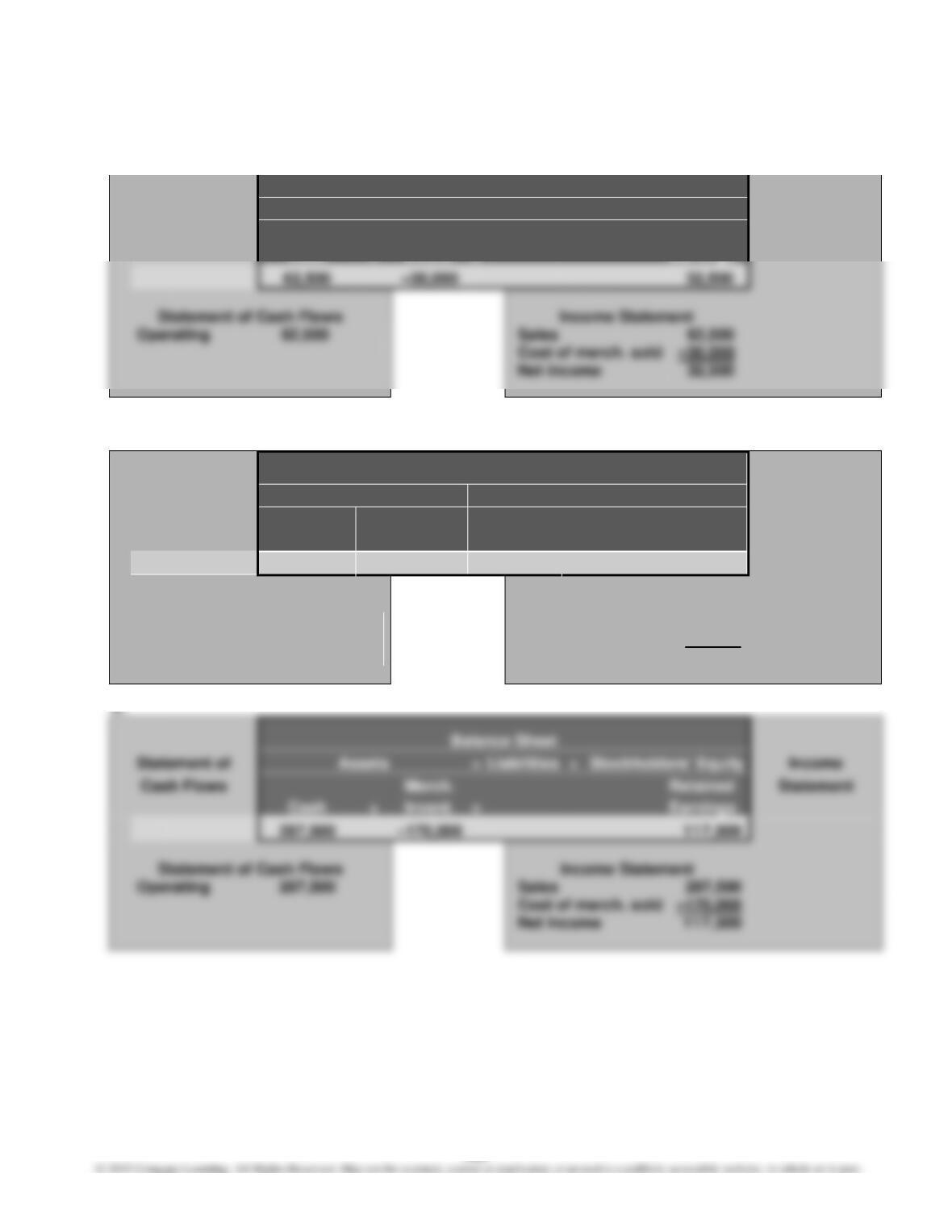

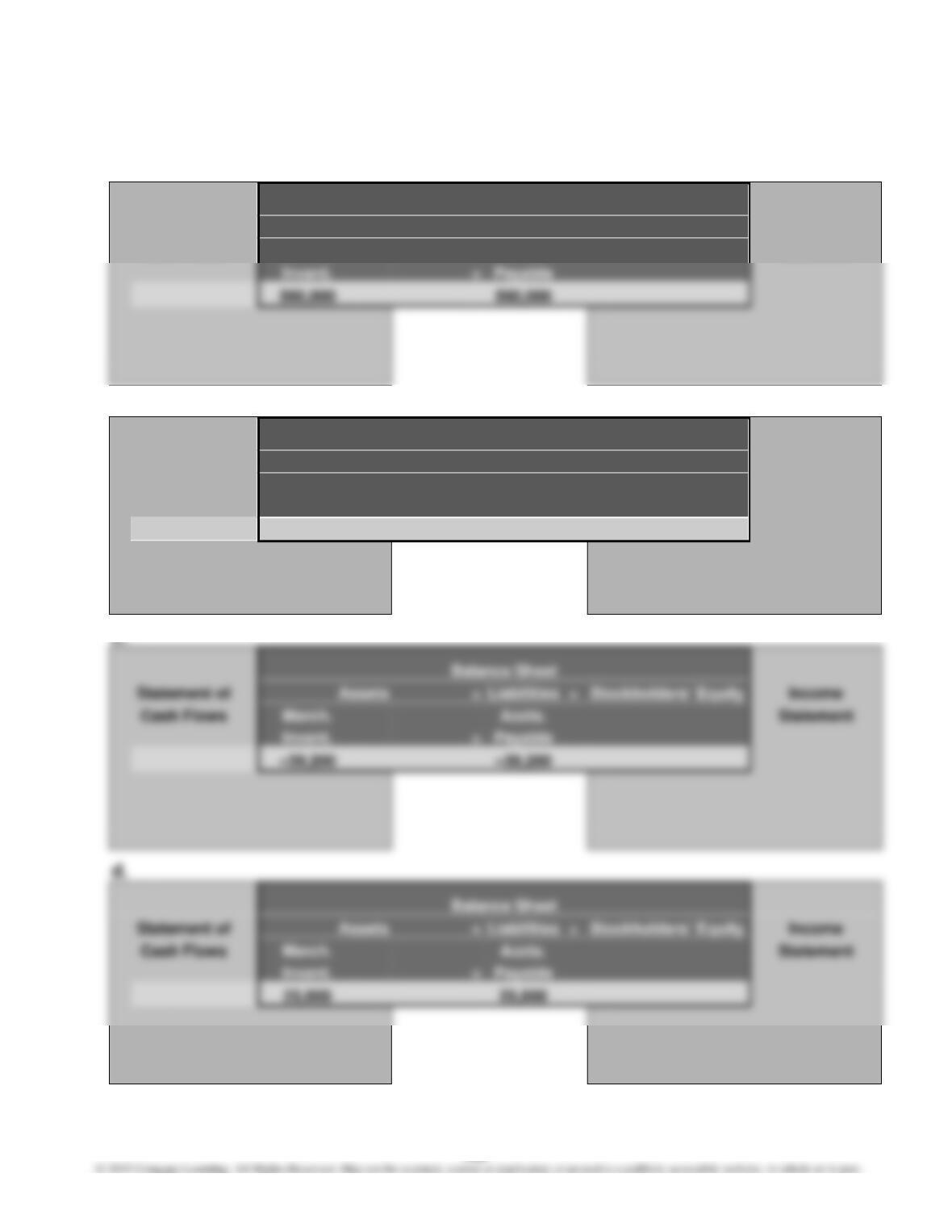

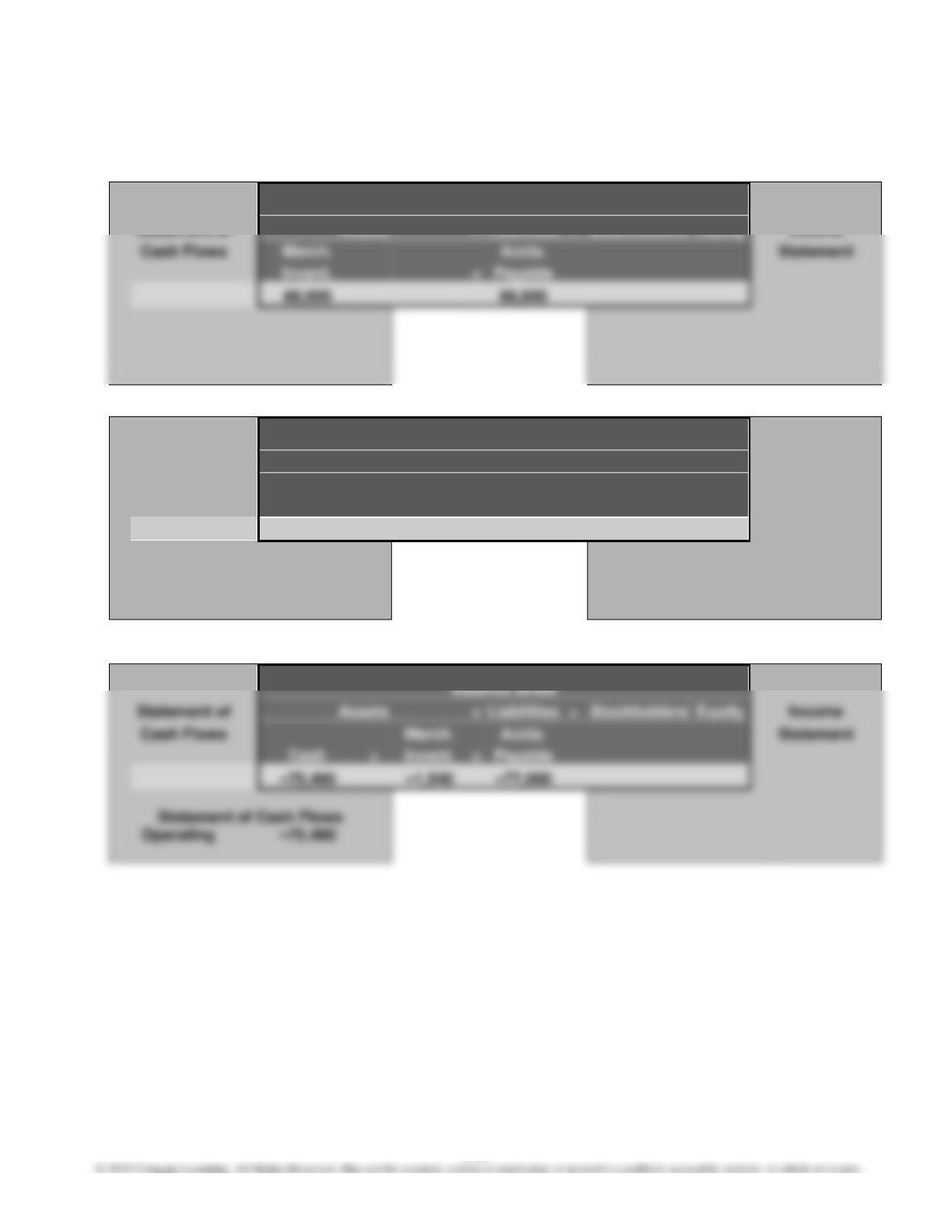

E4–12

a.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Retained

Statement

Cash

+

Invent.

=

Earnings

62,500

–30,000

Income Statement

Operating

Sales

Cost of merch. sold

–30,000

Net income

b.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Retained

Statement

Rec.

+

Invent.

=

Earnings

27,800

–16,000

11,800

Income Statement

Sales

27,800

Cost of merch. sold

–16,000

Net income

11,800

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Retained

Statement

Cash

+

Invent.

=

Earnings

117,500

Income Statement

Operating

Sales

Net income

117,500

106

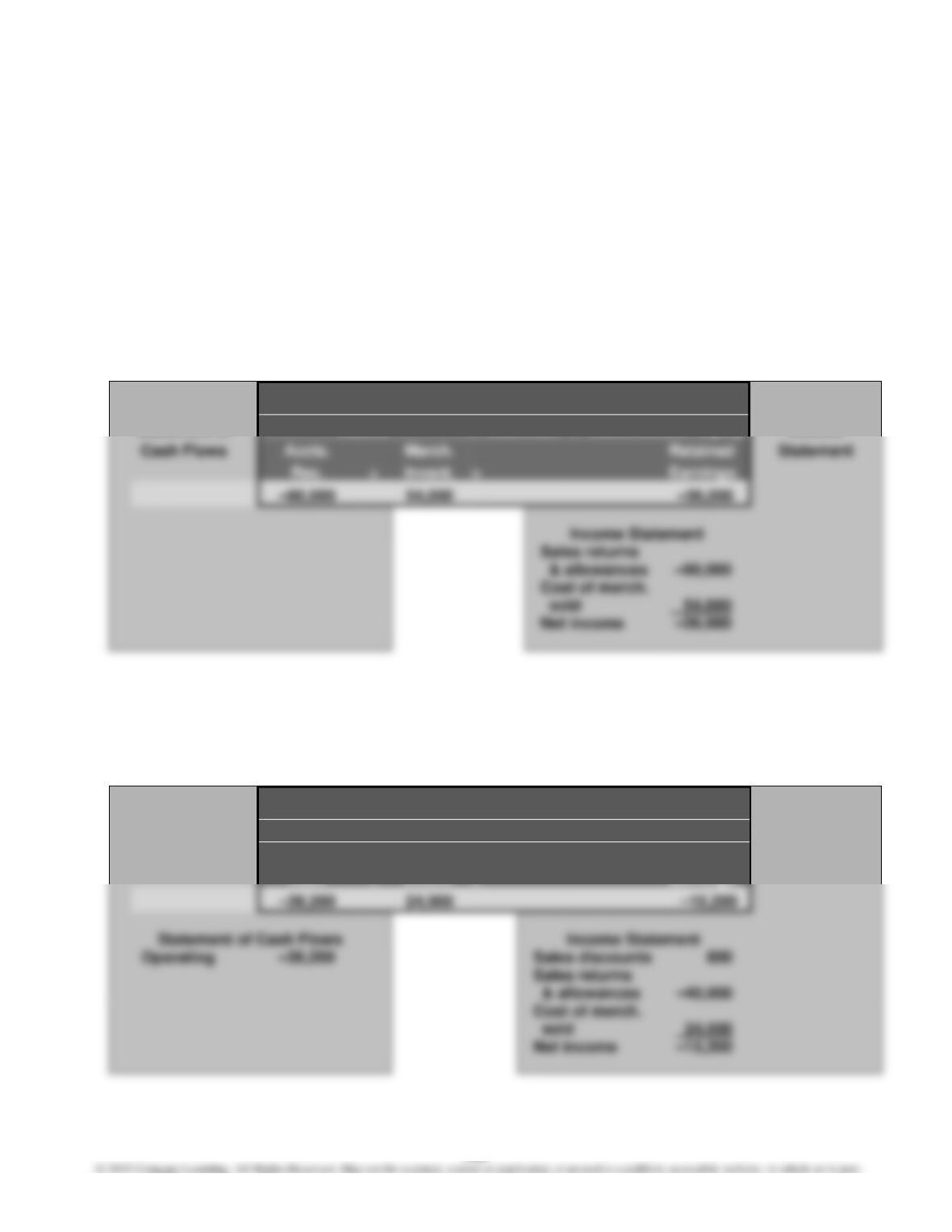

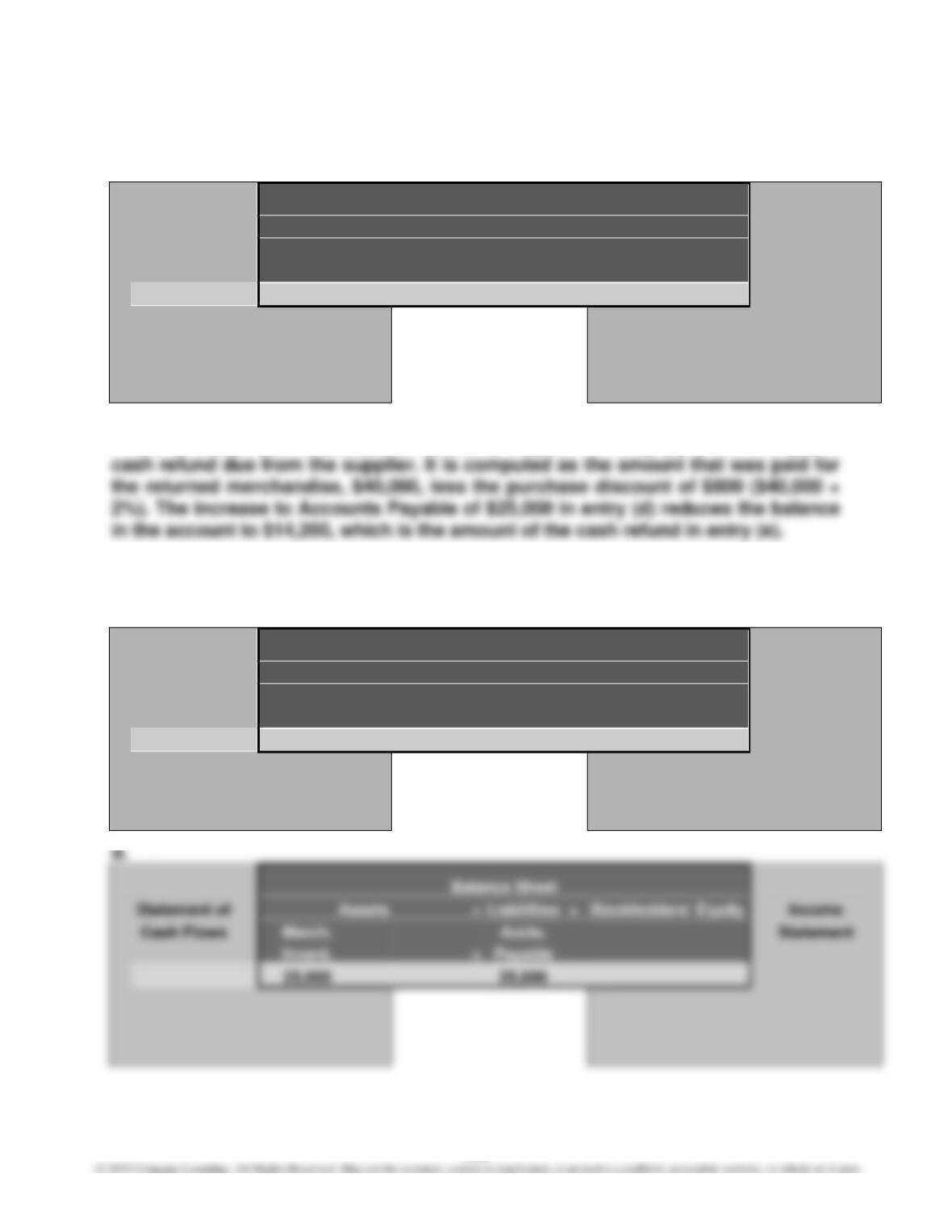

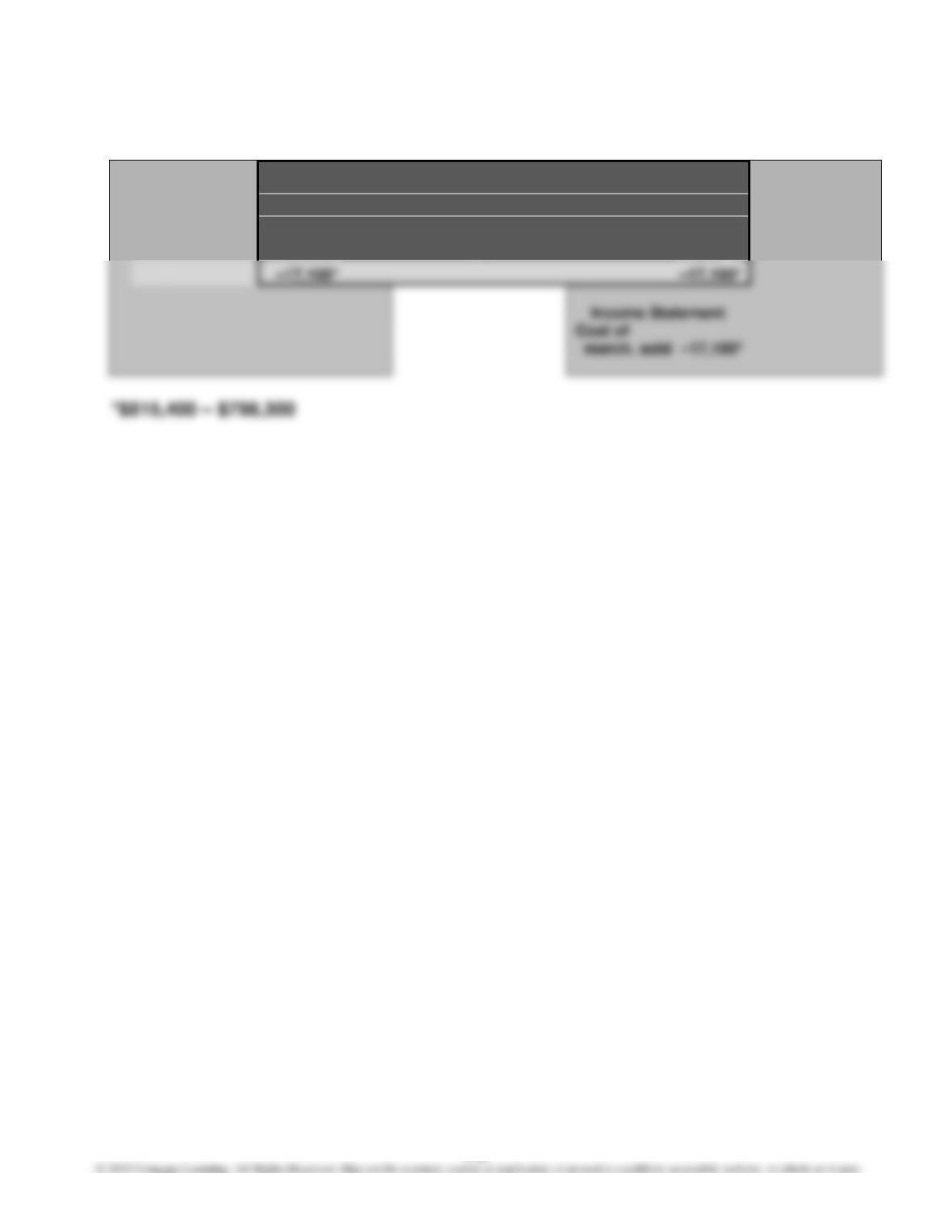

E4–13

It was acceptable to decrease Sales for the $90,000. However, using Sales

Returns and Allowances assists management in monitoring the amount of

returns so that quick action can be taken if returns become excessive.

Accounts Receivable also should have been decreased for $90,000. In addition,

Cost of Merchandise Sold should have been decreased only for the cost of the

merchandise sold, not the selling price. Merchandise Inventory also should have

been increased for the cost of the merchandise returned. The effects on the

accounts and financial statements of correctly recording the returns would have

been as follows:

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Retained

Statement

+

Invent.

=

Earnings

E4–14

a. $39,200 [$40,000 – ($40,000 × 2%)]

b.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Retained

Statement

Cash

+

Invent.

=

Earnings

E4–15

a. $12,500

E4–16

a. $9,310 [Purchase of $13,500, less return of $4,000, less discount of $190

[($13,500 – $4,000) × 2%]

b. Merchandise Inventory

E4–17

Offer B is lower than offer A. Details are as follows:

A B

108

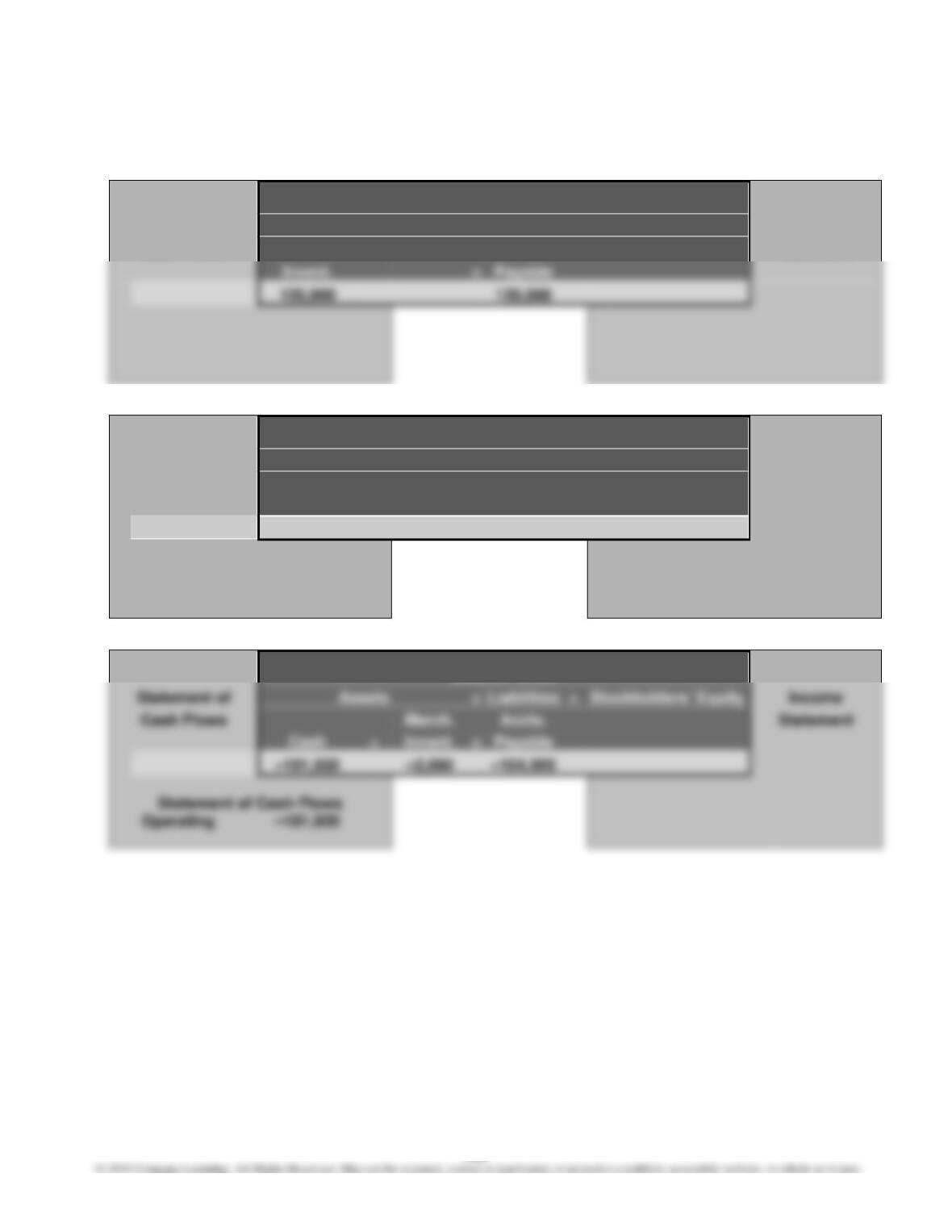

E4–18

a.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Invent.

=

Payable

b.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Invent.

=

Payable

–16,000

–16,000

c.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Statement

=

Payable

Operating

109

E4–19

a.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Invent.

=

Payable

b.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Cash

+

Invent.

=

Payable

–548,800

–11,200

–560,000

Statement of Cash Flows

Operating

–548,800

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Invent.

=

Payable

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Invent.

=

Payable

110

E4–19, Continued

e.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Statement

Cash

=

Payable

14,200

14,200

Statement of

Cash Flows

Operating

14,200

*Note: The decrease of $39,200 to Accounts Payable in entry (c) is the amount of

The alternative entries below yield the same final results.

c.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Statement

Rec.

+

Invent.

39,200

–39,200

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Statement

=

Payable

25,000

25,000

E4–19, Concluded

e.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Statement

=

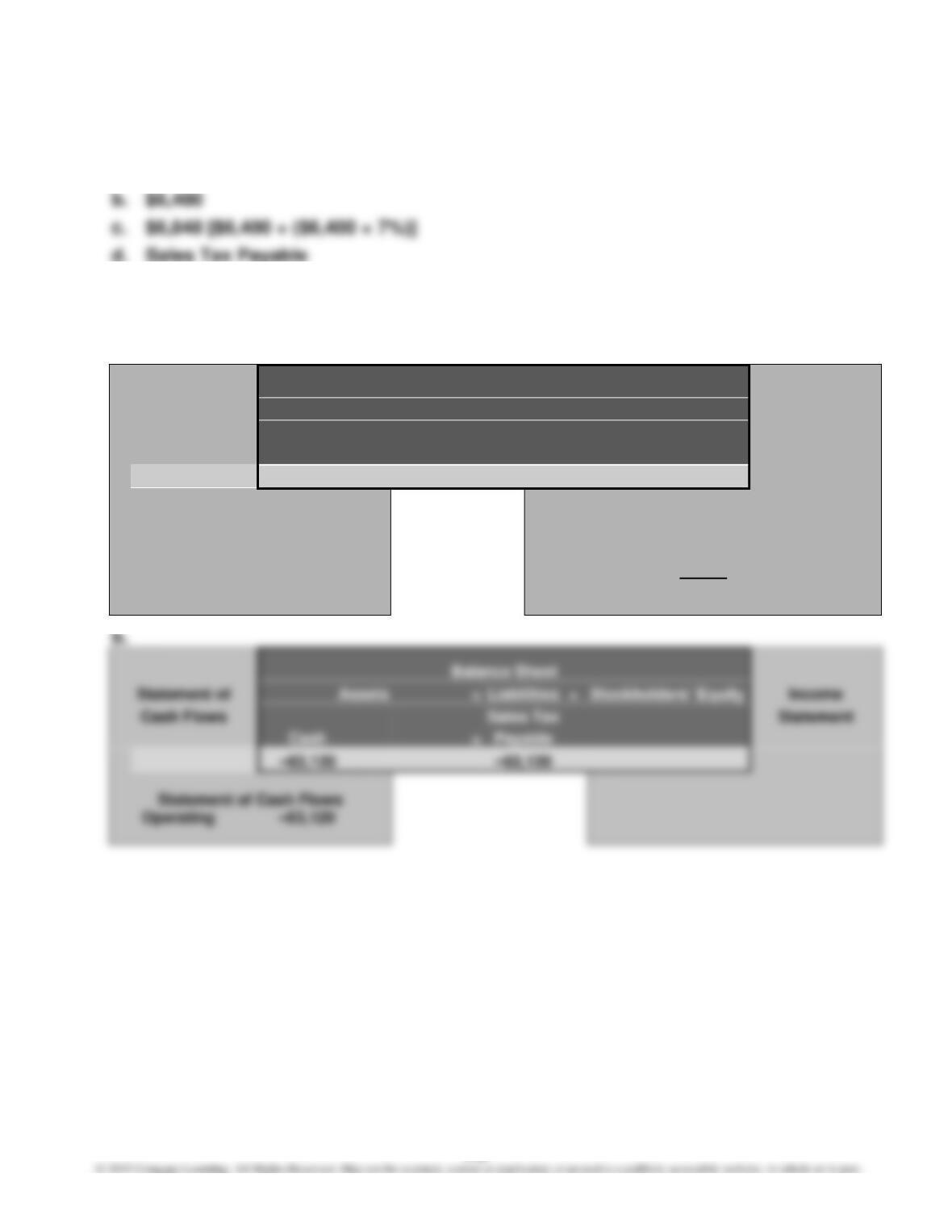

E4–20

a. $7,227 [($8,250 – $950) – ($7,300 × 1%)]

112

E4–21

a. At the time of sale

E4–22

a.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Sales Tax

Retained

Statement

Rec.

+

Invent.

=

Payable

+

Earnings

11,925

–6,750

675

4,500

Income Statement

Sales

11,250

Cost of merch.

sold

–6,750

Net income

4,500

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Sales Tax

Statement

=

Payable

Operating

113

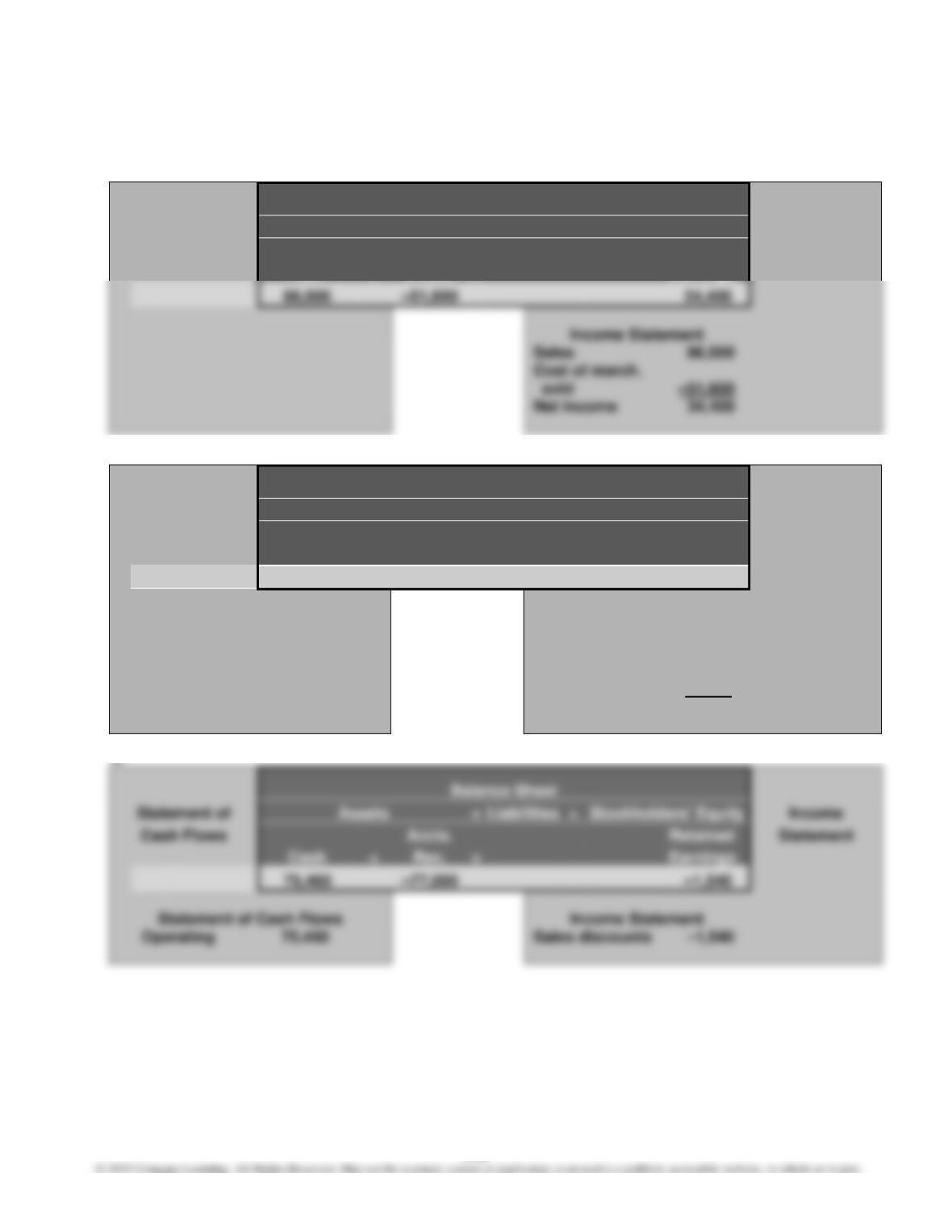

E4–23

a.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Retained

Statement

Rec.

+

Invent.

=

Earnings

Income Statement

Sales

sold

Net income

b.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Merch.

Retained

Statement

Rec.

+

Invent.

=

Earnings

–9,000

5,000

–4,000

Income Statement

Sales returns

& allowances

–9,000

Cost of merch.

sold

5,000

Net income

–4,000

c.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Retained

Statement

+

=

Earnings

–1,540

Income Statement

Operating

Sales discounts

114

E4–24

a.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Invent.

=

Payable

b.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Accts.

Statement

Invent.

=

Payable

–9,000

–9,000

c.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Statement

=

Payable

Operating

115

E4–25

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Merch.

Retained

Statement

Inventory

=

Earnings

116

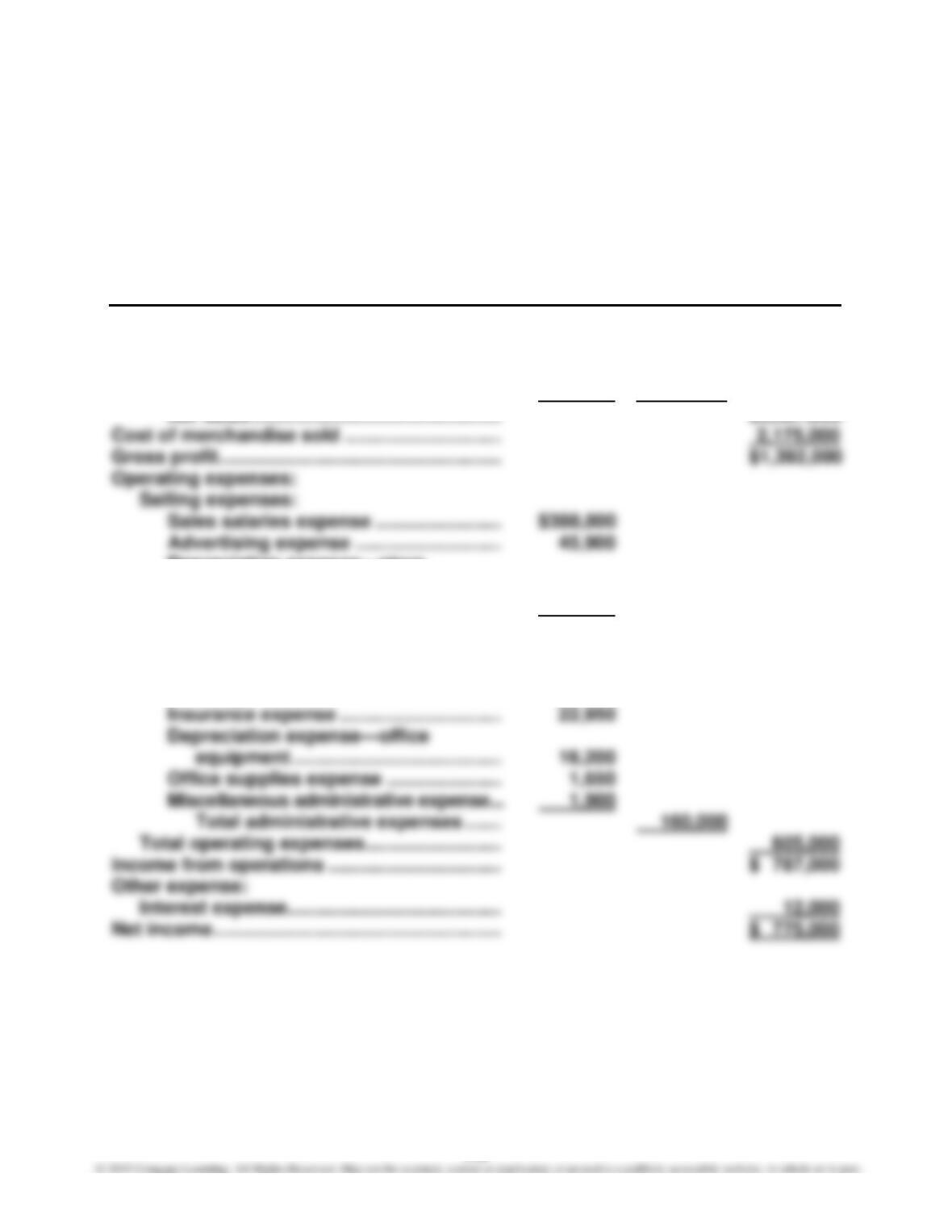

PROBLEMS

P4–1

1.

AQUA CO.

Income Statement

For the Year Ended June 30, 20Y8

Revenue from sales:

Sales ………………………………………………….. $3,625,000

Less: Sales returns and allowances …….. $ 37,800

Sales discounts …………………………. 20,200 58,000

Depreciation expense—store

equipment …………………………………. 8,300

Miscellaneous selling expense ……….. 2,000

Total selling expenses ……………….. $ 445,000

Administrative expenses:

Office salaries expense …………………… $ 77,400

Rent expense …………………………………. 39,900

117

P4–1, Continued

2.

AQUA CO.

Retained Earnings Statement

For the Year Ended June 30, 20Y8

Retained earnings, July 1, 20Y7 …………………………………. $253,800

Net income for the year …………………………………………….. $775,000

P4–1, Continued

3.

AQUA CO.

Balance Sheet

June 30, 20Y8

Assets

Store equipment ………………………………….. $511,500

Less accumulated depreciation …………. 186,700 324,800

Total property, plant, and

equipment ………………………………….. 390,500

Total assets …………………………………………….. $1,031,000

Stockholders’ Equity

Capital stock ……………………………………………. $ 15,000

Retained earnings ……………………………………. 903,800

Total stockholders’ equity ………………………… 918,800

Total liabilities and stockholders’ equity …… $1,031,000